Xylene Market Report Scope & Overview:

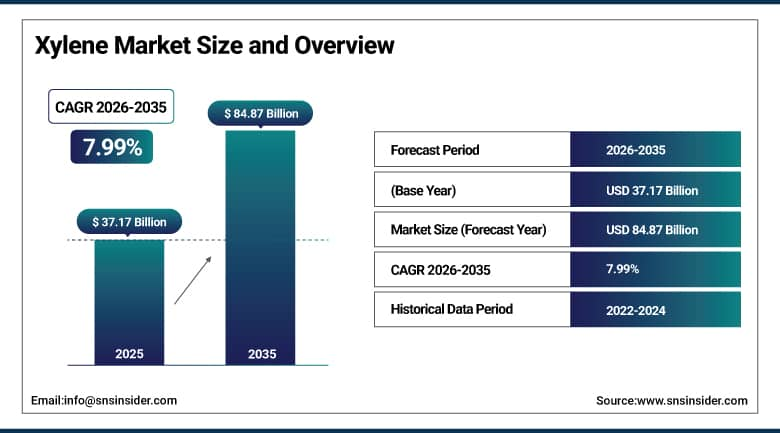

The Xylene Market was valued at USD 37.17 Billion in 2025 and is expected to reach USD 84.87 Billion by 2035, growing at a CAGR of 7.99% from 2026–2035.

The global xylene market is evolving rapidly, driven by demand in petrochemicals, paints and coatings, and adhesives. Xylene is an aromatic hydrocarbon obtained from catalytic reforming and coal carbonisation processes, existing as three structural isomers-ortho-, meta-, and para-xylene-plus mixed xylene whose collective commercial applications span solvent use, polymer monomer production, and specialty chemical synthesis. Para-xylene’s role as the precursor to purified terephthalic acid for polyester fibre and PET plastic production creates the largest single demand category whose packaging and textile industry growth sustains commercial expansion.

In February 2024, ExxonMobil resumed paraxylene production at its Beaumont, Texas facility, contributing 12% of U.S. paraxylene capacity, driven by rising demand for PET plastic production particularly in summer packaging seasons. The resumption reflects the commercial relationship between consumer packaging demand cycles and paraxylene production economics whose margin visibility at above-breakeven PET pricing sustains production investment decisions at existing facilities.

Market Size and Forecast

-

Market Size in 2026E: USD 40.14 Billion

-

Market Size by 2035: USD 84.87 Billion

-

CAGR: 7.99% from 2026 to 2035

-

Fastest Growing Region: North America

-

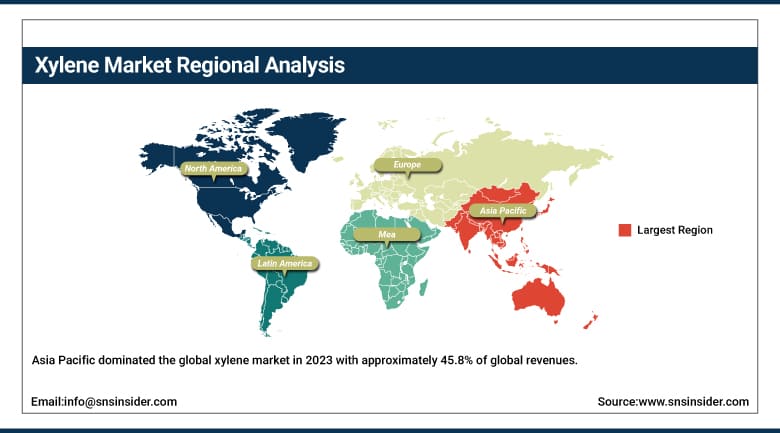

Largest Region: Asia Pacific

To Get More Information On Xylene Market - Request Free Sample Report

Xylene Market Trends

-

Paraxylene demand growth for PET plastic production is compounding with global packaging industry expansion as consumer preference for PET beverage bottles, food containers, and consumer goods packaging sustains above-average PTA and paraxylene procurement.

-

Polyester fibre demand from the global textile industry’s synthetic fibre adoption is creating consistent paraxylene and PTA procurement whose commercial scale compounds with the textile industry’s progressive synthetic fibre share growth over natural fibre alternatives.

-

Bio-based xylene development from lignin and cellulosic biomass sources is attracting R&D investment as petrochemical producers seek renewable feedstock alternatives whose sustainable credentials create commercial differentiation in environmentally conscious procurement markets.

-

Ortho-xylene demand for phthalic anhydride production is growing as construction sector plasticiser requirements and electrical cable PVC insulation create consistent PA procurement that sustains o-xylene commercial demand independently of para-xylene cycle variation.

-

VOC emission regulation tightening for xylene-containing paint and solvent formulations is creating reformulation investment toward lower-VOC alternatives whose commercial impact on solvent-grade xylene demand creates moderate headwind in the application category.

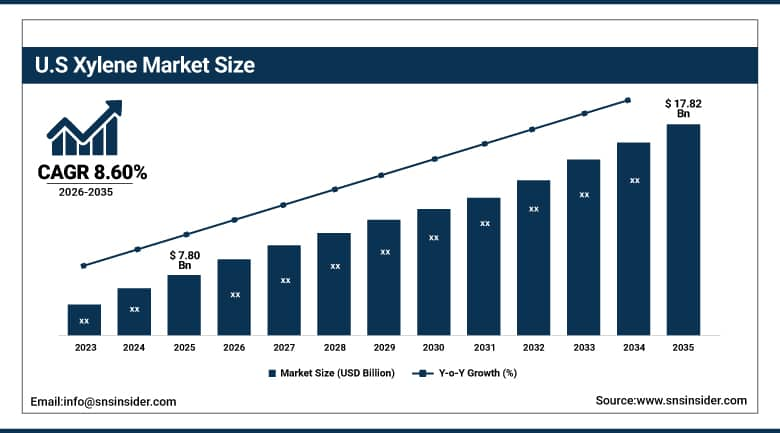

U.S. Xylene Market Outlook

The U.S. Xylene Market was valued at approximately USD 7.80 Billion in 2025 and is expected to reach approximately USD 17.82 Billion by 2035, growing at a CAGR of approximately 8.60%.

The U.S. is the most commercially significant xylene market within the fastest-growing North American region. ExxonMobil’s Beaumont paraxylene facility, Flint Hills Resources, Indorama’s U.S. PTA operations, and INEOS Aromatics collectively define the North American xylene supply and derivative processing landscape. The packaging industry’s PET consumption, the paints and coatings sector’s solvent-grade xylene procurement, and the chemical industry’s intermediate demand collectively sustain consistent U.S. xylene market engagement. The IRA’s domestic manufacturing investment incentive is creating industrial facility investment whose chemical input procurement includes xylene derivative demand.

In March 2023, Saudi Aramco announced plans to build a USD 10 billion oil refinery with 300,000 barrels per day capacity and a petrochemical complex in China with annual production of 1.65 million tonnes of ethylene and 2 million tonnes of paraxylene. The investment demonstrates the commercial scale at which global energy companies are committing to paraxylene production capacity expansion whose demand from China’s packaging and textile industries creates commercially certain procurement that justifies multi-billion-dollar greenfield investment.

Xylene Market Segment Analysis

-

By Type, the Mixed Xylene segment dominated the Xylene Market with approximately 38% share in 2025, while the Para-Xylene segment is the fastest growing segment due to surging PET plastic and polyester fibre demand.

-

By Application, the Solvents segment dominated the Xylene Market with 42.1% share in 2025, while the Terephthalic Acid & PET Production segment is the fastest growing segment driven by packaging and textile industry expansion.

-

By End User, the Packaging segment dominated the Xylene Market with approximately 32% share in 2025, while the Textile & Apparel segment is the fastest growing segment as polyester fibre adoption grows globally.

By Type, mixed xylene dominates, para-xylene grows fastest

Mixed xylene retained the dominant type position with approximately 38% of the xylene market in 2025. Mixed xylene’s commercial primacy reflects its position as the direct output of catalytic reforming and coal carbonisation processes whose commercial supply is available as a blended aromatic stream before the isomer separation processing that produces individual ortho-, meta-, and para-xylene fractions. Mixed xylene’s use as a direct-application solvent in paints, coatings, adhesives, printing inks, and cleaning agents, combined with government investments in refinery expansions that produce mixed xylene as an integrated reformate fraction, sustains its dominant volume position.

Para-xylene is the fastest-growing type because PET plastic and polyester fibre’s dual demand from packaging and textile industries creates above-average purified terephthalic acid procurement whose direct xylene feedstock is para-xylene. The extraordinary scale of global PET bottle production for beverage packaging, the textile industry’s polyester fibre demand from fast fashion and performance sportswear, and the growth of industrial polyester applications collectively create paraxylene demand that grows proportionally with these upstream market expansions.

By Application, solvents dominate, PTA/PET grows fastest

Solvents retained the dominant application position with 42.1% of the xylene market in 2025. Xylene’s solvent properties including rapid evaporation rate, strong dissolving capability for oils, waxes, and resins, and compatibility with a broad range of industrial substrates create demand across paints and coatings, adhesives, printing inks, rubber processing, and industrial cleaning whose combined application volume creates the largest single xylene demand category globally. The construction and automotive refinishing industries’ paint and coating consumption creates consistent solvent-grade xylene procurement whose commercial stability reflects the construction cycle’s relatively stable long-term demand trajectory.

Terephthalic acid and PET production is the fastest-growing application because paraxylene’s conversion to purified terephthalic acid whose subsequent polymerisation with ethylene glycol creates PET resin creates a demand pathway that compounds with the packaging industry’s PET adoption growth and the textile industry’s polyester fibre expansion. Each new PET bottle plant and each new polyester fibre spinning facility creates defined paraxylene demand that sustains above-average segment growth.

By End User, packaging dominates, textile grows fastest

Packaging retained the dominant end-user position with approximately 32% of the xylene market in 2025. The global packaging industry’s extraordinary scale, encompassing PET beverage bottles, food containers, consumer goods packaging, and industrial packaging, creates the largest single end-user xylene demand category whose PTA-PET value chain directly links xylene to the most commercially certain demand in the petrochemical market. Each percentage point increase in global beverage packaging’s PET penetration creates proportional paraxylene procurement that compounds with beverage consumption volume growth. Emerging market urbanisation’s packaged food and beverage adoption creates the most commercially dynamic structural demand growth for PET packaging.

Textile and apparel is the fastest-growing end user because the global textile industry’s progressive adoption of polyester fibre over natural cotton, wool, and silk alternatives creates above-average paraxylene and PTA demand growth. Polyester’s cost advantage over cotton, its performance characteristics in sportswear and outdoor apparel, and its dyeability and wrinkle resistance in fashion apparel collectively sustain its textile market share growth. The fast fashion industry’s high production volume at low per-garment cost creates polyester fibre demand whose commercial scale compounds with fashion cycle acceleration.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

54.6% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

Asia Pacific Xylene Market Insights

Asia Pacific dominated the global xylene market in 2023 with approximately 45.8% of global revenues. China accounts for approximately 54.6% of Asia Pacific revenues through its position as the world's largest PTA, polyester fibre, and PET packaging producer whose integrated paraxylene demand creates the most commercially significant single-country xylene consumption concentration globally. The textile industry’s extraordinary scale in China, Bangladesh, and Vietnam creates consistent polyester fibre paraxylene demand that reinforces Asia Pacific’s market dominance.

India and South Korea are significant secondary markets where petroleum refinery expansions create mixed and para-xylene production capacity, and the domestic packaging and textile industries create consistent xylene derivative procurement that sustains growing regional market engagement.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Xylene Market Insights

North America is the fastest-growing regional xylene market, driven by U.S. packaging industry’s PET demand, the domestic petrochemical sector’s paraxylene production, and IRA manufacturing investment incentives creating chemical industry procurement. The United States accounts for approximately 87.4% of North American revenues through ExxonMobil’s Beaumont facility, Flint Hills Resources, and Indorama’s integrated xylene processing and PTA production.

Canada’s oil sands industry creates BTX aromatics production whose xylene component serves domestic chemical and solvent markets. Mexico’s growing manufacturing sector creates xylene solvent and adhesive demand that complements North American regional procurement.

Europe Xylene Market Insights

Europe is a technically sophisticated xylene market where INEOS Aromatics’ European operations, BASF’s chemical manufacturing, and the automotive coatings industry’s solvent-grade xylene demand create structured institutional procurement. Germany accounts for approximately 22.3% of European revenues through its automotive manufacturing sector’s paint and coating consumption, the chemical industry’s xylene intermediate demand, and INEOS’s European xylene production.

In March 2022, INEOS Aromatics spent USD 70 million to modernise its PTA plant in Indonesia, increasing capacity by 15% from 500,000 to 575,000 tonnes per year and reducing CO2 emissions by 15% per tonne, reflecting the commercial logic of capacity expansion combined with sustainability investment that sustains competitive positioning in a cost-competitive commodity chemical market.

MEA & Latin America Xylene Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through Saudi Aramco’s refinery integration, SABIC’s xylene derivative production, and the USD 10 billion China petrochemical complex investment announced in 2023 demonstrating the commercial scale of Middle Eastern xylene production ambition. Brazil leads Latin American revenues at approximately 44.2% through its packaging industry’s PET demand, Braskem’s petrochemical operations, and the automotive sector’s paint and coating consumption.

UAE’s petrochemical industry development and Egypt’s refinery expansion create significant MEA secondary markets whose xylene production and consumption are growing with regional industrial development investment.

Market Dynamics:

Growth Drivers: PET packaging and polyester fibre demand creating paraxylene procurement and petrochemical refinery expansion

PET packaging and polyester fibre demand is the xylene market’s most commercially certain structural growth driver whose combined downstream volume creates the largest single paraxylene demand category. Global beverage packaging’s PET adoption, the food packaging industry’s PET barrier properties preference, and the textile industry’s polyester fibre dominance collectively create paraxylene demand that grows proportionally with consumer goods and textile production volume growth in both developed and emerging markets. Each new PTA plant and polyester fibre spinning capacity addition creates long-duration paraxylene supply relationships whose multi-decade operational commitment provides commercial certainty for xylene production investment.

Petrochemical refinery expansion investment in India, the Middle East, and Southeast Asia is creating new xylene production capacity whose geographic proximity to growing Asian demand markets improves supply chain economics. Saudi Aramco’s USD 10 billion China petrochemical complex, India’s refinery expansion programmes, and South Korea’s petrochemical capacity investment collectively represent xylene supply additions whose commercial commissioning creates new market participant dynamics that progressively improve Asia Pacific’s self-sufficiency.

Restraints: Crude oil price volatility creating feedstock cost uncertainty and VOC regulation reducing solvent-grade demand

Crude oil and naphtha price volatility creates xylene production cost uncertainty whose impact on margin predictability limits producer investment confidence in capacity expansion at marginal economics. Each crude oil price cycle creates xylene producer margin variation whose combined impact on production investment decision timing creates market supply volatility that affects downstream PTA and polyester production economics. Naphtha’s price sensitivity to crude oil creates feedstock cost variability whose downstream impact on reformate and mixed xylene production cost creates commercial uncertainty across the xylene value chain.

VOC emission regulation tightening for xylene-containing solvent formulations is creating substitution pressure in the paint, coatings, and adhesive application categories where low-VOC and water-based formulation alternatives are progressively gaining specification preference. Each VOC regulation tightening cycle creates reformulation investment whose commercial outcome reduces solvent-grade xylene demand in the regulated market while sustaining demand in less regulated geographies.

Opportunities: Bio-based xylene development and emerging market PET capacity expansion

Bio-based xylene development from renewable biomass feedstocks represents the most commercially transformative long-term opportunity whose successful commercialisation creates sustainable xylene supply chains whose low-carbon credentials command premium pricing in environmentally sensitive procurement markets. Virent’s bioforming process, Anellotech’s biomass catalytic flash pyrolysis for bio-paraxylene, and multiple academic research programmes collectively represent the bio-based xylene innovation pipeline whose commercialisation timeline depends on process economics development.

Emerging market PET and polyester capacity expansion represents the most commercially certain near-term growth opportunity for paraxylene demand. Each new PET recycling plant that recovers paraxylene equivalent from post-consumer PET, and each new polyester fibre facility in South Asia and Southeast Asia, creates paraxylene procurement that compounds with the regional textile and packaging industry’s growth trajectory.

Recent Developments:

-

2024: ExxonMobil resumed paraxylene production at its Beaumont, Texas facility in February 2024, contributing 12% of U.S. paraxylene capacity in response to rising PET demand, particularly for summer packaging season production cycles.

-

2023: Saudi Aramco announced plans to build a USD 10 billion oil refinery and petrochemical complex in China in March 2023, with annual production capacity of 2 million tonnes of paraxylene targeting China's PTA and polyester fibre industry demand.

-

2022: INEOS Aromatics spent USD 70 million to modernise its PTA plant in Indonesia in March 2022, increasing annual capacity by 15% from 500,000 to 575,000 tonnes per year and reducing CO2 emissions by 15% per tonne, demonstrating capacity expansion with sustainability improvement.

Xylene Market Key Players:

-

ExxonMobil Corporation

-

Sinopec Group (CPCC)

-

Reliance Industries Limited

-

INEOS Aromatics

-

Saudi Aramco

-

Flint Hills Resources

-

BP Chemicals

-

TotalEnergies SE

-

Shell Chemicals

-

LyondellBasell Industries

-

SK Innovation

-

GS Caltex

-

Hanwha Solutions

-

Formosa Plastics Corporation

-

SABIC

-

Braskem S.A.

-

Indorama Ventures

-

Lotte Chemical

-

China National Chemical Corporation

-

Kumho Petrochemical

Xylene Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 37.17 Billion |

| Market Size by 2035 | USD 84.87 Billion |

| CAGR | CAGR of 7.99% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Type (Mixed Xylene, Para-Xylene/p-Xylene, Ortho-Xylene/o-Xylene, Meta-Xylene/m-Xylene) • by Application (Solvents, Terephthalic Acid & PET Production, Plasticizers, Paints & Coatings, Adhesives & Sealants, Rubber, Printing Inks, Others) • by End User (Packaging, Automotive, Textile & Apparel, Construction, Electronics, Consumer Goods, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | ExxonMobil Corporation, Sinopec Group (CPCC), Reliance Industries Limited, INEOS, Aromatics, Saudi Aramco, Flint Hills Resources, BP Chemicals, TotalEnergies SE, Shell Chemicals, LyondellBasell Industries, SK Innovation, GS Caltex, Hanwha Solutions, Formosa Plastics Corporation, SABIC, Braskem S.A., Indorama Ventures, Lotte Chemical, China National Chemical Corporation, Kumho Petrochemical |

Frequently Asked Questions

The Xylene Market is expected to grow at a CAGR of 7.99% from 2026 to 2035.

The Xylene Market was valued at USD 37.17 Billion in 2025.

PET packaging industry and polyester fibre demand creating above-average paraxylene procurement growth that compounds with global consumer goods and textile production volume, and petrochemical refinery expansion in Asia and the Middle East creating new xylene production capacity.

Solvents dominated the Xylene Market with 42.1% share in 2025, while the Terephthalic Acid & PET Production segment is the fastest growing.

Asia Pacific dominated the Xylene Market in 2023 with approximately 45.8% share, with China accounting for approximately 54.6% of Asia Pacific revenues. North America is the fastest-growing region.

Get in Touch