Zero-emission Aircraft Market Report Scope & Overview:

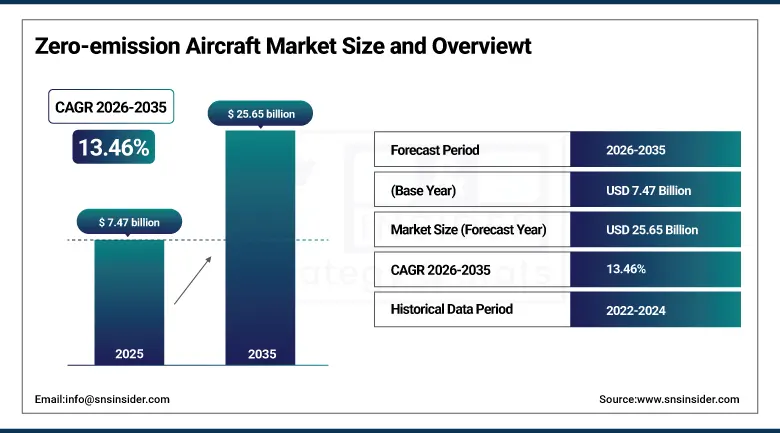

The Zero-emission Aircraft Market was valued at USD 7.47 billion in 2025 and is projected to reach around USD 25.65 billion by 2035, growing at a CAGR of 13.46% from 2026–2035.

The Market for Zero-emission Aircraft is growing at a fast pace due to the focus of the aviation industry on goals related to carbon neutrality, along with emission controls that are tightening globally and the development in technologies used for electric and hydrogen propulsion systems. The investments made in green aviation facilities and the advent of urban air mobility systems coupled with government support for cleaner aircraft are contributing to the rapid growth in this market across commercial, regional, and future mobility systems.

Recent trends reveal increased activities associated with collaborative initiatives and technology validation. There have also been increasing investments in airports’ charging systems, hydrogen refueling stations, and advanced propulsion innovations. Collaboration between aircraft manufacturers, energy firms, and aviation authorities are resulting in an integration of value chain initiatives aimed at reducing commercialization timescales, improving aircraft efficiencies, and transitioning towards zero-emissions aviation networks.

Market Size and Forecast

-

Market Size in 2026: USD 8.23 Billion

-

Market Size by 2035: USD 25.65 Billion

-

CAGR: 13.46% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Zero-emission Aircraft Market - Request Free Sample Report

Zero-emission Aircraft Market Trends

-

Rising investments in hydrogen and electric propulsion technologies are accelerating zero-emission aircraft development.

-

Increasing government net-zero initiatives are driving sustainable aviation adoption globally.

-

Rapid expansion of urban air mobility ecosystems is boosting eVTOL aircraft deployment.

-

Growing use of lightweight materials is improving aircraft efficiency and operational range.

-

Increasing airport investments in hydrogen and charging infrastructure are supporting market growth.

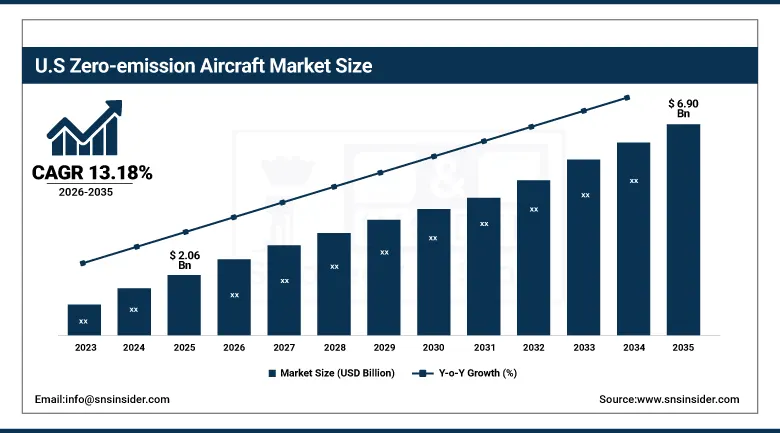

The U.S. Zero-emission Aircraft Market was valued at USD 2.06 billion in 2025 and is expected to reach around USD 6.90 billion by 2035, growing at a CAGR of 13.18% from 2026–2035.

The United States is the leading regional market for zero-emission aircraft due to strong aerospace R&D capabilities, increasing federal support for sustainable aviation initiatives, and growing investments in hydrogen-electric and battery-powered aircraft technologies. Market growth is further supported by the presence of major aircraft manufacturers, emerging aviation startups, and expanding infrastructure development for next-generation aviation systems.

Additionally, recent developments such as Zero Avia advancing hydrogen-electric flight-testing programs and Airbus expanding U.S.-based partnerships for hydrogen aviation infrastructure development are reinforcing long-term market growth and strengthening the sustainable aviation ecosystem.

Zero-emission Aircraft Market Segment Insights

-

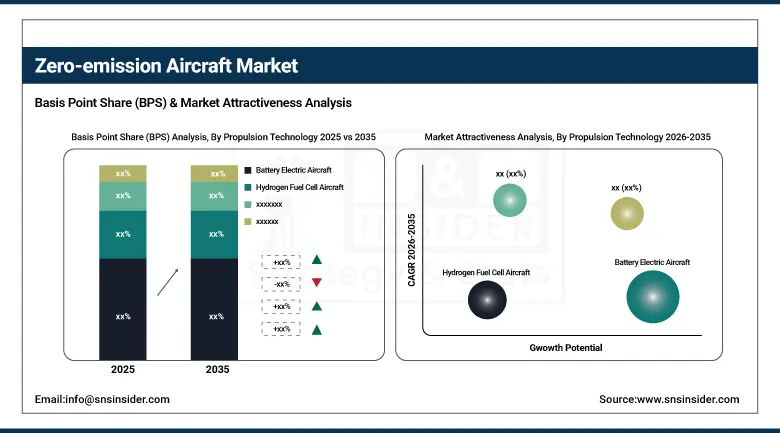

By Propulsion Technology, Battery Electric Aircraft dominated the Luxury Kitchen Appliances Market with 38.34% share in 2025; Hydrogen Fuel Cell Aircraft is fastest growing CAGR.

-

By Aircraft Type, Fixed-Wing Aircraft dominated the Luxury Kitchen Appliances Market with 44.15% share in 2025; Urban Air Mobility (eVTOL) Aircraft is fastest growing CAGR.

-

By Range, Short-Haul (<500 km) dominated the Luxury Kitchen Appliances Market with 33.85% share in 2025; Medium-Haul (1,500–3,000 km) is fastest growing CAGR.

-

By Application, Commercial Passenger Transport Stores dominated the Luxury Kitchen Appliances Market with 46.24% share in 2025; Urban Air Mobility (UAM) is fastest growing CAGR.

Zero-emission Aircraft Market Segment Analysis

By Propulsion Technology, battery electric aircraft segment dominates the zero-emission aircraft market, hydrogen fuel cell aircraft expected to grow fastest

In 2025, the Battery Electric Aircraft segment maintained its dominant position in the Zero-emission Aircraft Market, accounting for 38.34% of total revenue. This leadership is primarily driven by increasing investments in electric propulsion systems, early-stage commercialization of short-haul electric aircraft, and strong adoption across pilot projects and urban mobility applications.

From 2026 to 2035, the Hydrogen Fuel Cell Aircraft segment is projected to record the highest CAGR. This rapid growth is driven by rising industry focus on long-range sustainable aviation, increasing hydrogen infrastructure investments, and expanding partnerships aimed at developing next-generation fuel-cell propulsion systems.

By Aircraft Type, fixed-wing aircraft segment dominates the zero-emission aircraft market, urban air mobility (eVTOL) aircraft expected to grow fastest

In 2025, the Fixed-Wing Aircraft segment held the largest share of 44.15% in the Zero-emission Aircraft Market, supported by ongoing electrification initiatives across regional and commercial aviation sectors and increasing prototype development activities among major aerospace manufacturers.

The Urban Air Mobility (eVTOL) Aircraft segment is expected to register the highest CAGR during 2026–2035. Growth is driven by rapid urbanization, increasing investments in advanced air mobility ecosystems, and rising demand for sustainable short-distance transportation solutions.

By Range, short-haul (<500 km) segment dominates the zero-emission aircraft market:

In 2025, the Short-Haul (<500 km) segment dominated the Zero-emission Aircraft Market with a 33.85% share, driven by current technological limitations of battery systems and stronger deployment feasibility for short-distance operations.

From 2026 to 2035, the Medium-Haul (1,500–3,000 km) segment is expected to record the highest CAGR. This growth is fueled by advancements in hydrogen propulsion systems, increasing aircraft range capabilities, and ongoing investments in sustainable aviation technologies designed for larger commercial operations.

By Application, commercial passenger transport segment dominates the zero-emission aircraft market, urban air mobility (UAM) expected to grow fastest

In 2025, the Commercial Passenger Transport segment maintained its dominant position in the Zero-emission Aircraft Market, accounting for 41.30% of total revenue. Such a leadership is motivated mainly by growing interest of airlines in fleet decarbonization, investments made in sustainable regional aviation, and strong interest in the development of future low emission passengers’ aircraft.

From 2026 to 2035, the Urban Air Mobility (UAM) segment is projected to record the highest CAGR. This rapid growth is driven by increasing development of eVTOL ecosystems, expanding urban transportation initiatives, and rising demand for efficient point-to-point air mobility solutions. Growing investments in smart city infrastructure and advanced mobility platforms are expected to further accelerate segment expansion.

Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

83.16% |

|

Europe |

Germany |

29.58% |

|

Asia Pacific |

China |

39.45% |

|

Middle East & Africa |

UAE |

29.35% |

|

Latin America |

Brazil |

43.56% |

North America Zero-emission Aircraft Market Insights

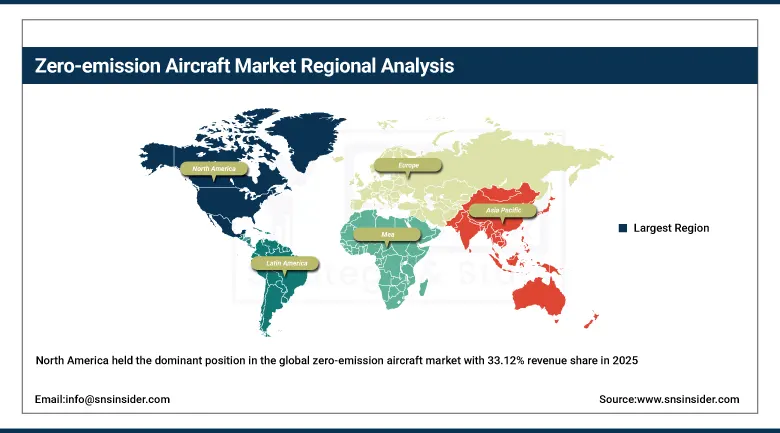

North America held the dominant position in the global zero-emission aircraft market with 33.12% revenue share in 2025, backed by a robust capability for innovation within the aerospace industry, increased investment in aviation technologies that are sustainable, and accelerated progress towards the development of hydrogen-electric and battery-powered aircraft systems. It is due to such advantages that include the existence of some of the leading players in terms of aircraft manufacturers, state-of-the-art aviation infrastructure, and cooperation between aerospace companies, technology providers, and governmental organizations. Market leadership in North America can be attributed to the USA.

Additionally, recent developments such as ZeroAvia advancing hydrogen-electric propulsion testing for larger regional aircraft and Airbus expanding strategic partnerships for hydrogen aviation ecosystem development are strengthening innovation and competitive intensity across the North American zero-emission aviation landscape.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Zero-emission Aircraft Market Insights

The Asia Pacific is projected to register the highest CAGR of 14.44% from 2026–2035, driven by growing government interest in sustainable transport systems, fast advancements in urban air mobility, and growing investments in aviation decarbonization efforts. China, Japan, South Korea, India, Singapore, and Australia will lead demand from their regions thanks to growing investments in aerospace and next generation mobility initiatives. Especially, China and Japan will be the most important growth engines due to growing investments in hydrogen technologies and aircraft research.

Japan strengthened national partnerships supporting hydrogen aviation technology development and airport decarbonization initiatives, while multiple Chinese aerospace firms expanded electric aircraft demonstration programs and advanced air mobility pilot projects across major cities.

Europe Zero-emission Aircraft Market Insights

Europe is expected to continue its importance within the global zero-emissions airplane industry based on the presence of sustainability laws, the implementation of ambitious plans for reducing carbon footprints within the aviation industry, and pioneering innovations related to hydrogen airplanes. The states of Germany, France, the UK, and the Nordic countries are contributing towards market development through investments in research and development and funding of sustainable aviation.

Airbus accelerated development activities linked to hydrogen-powered aviation concepts across Europe, while H2FLY expanded hydrogen-electric aircraft flight demonstrations to support future regional aircraft deployment initiatives.

Latin America, Middle East & Africa (LAMEA) Zero-emission Aircraft Market Insights

The zero emission aircrafts industry in the LAMEA region is experiencing slow growth due to sustainable aviation investments, modernization of airports, and clean transport technology adoption. Important nations in the LAMEA region such as Brazil, UAE, Saudi Arabia, and South Africa are creating opportunities for the sector through aviation infrastructure development and energy transition.In the Middle East region, Saudi Arabia increased clean aviation investments and hydrogen as part of their larger sustainability strategies that are focused on developing transportation ecosystems in the future. In Latin America, Brazil intensified partnerships in the field of sustainable aviation fuels and electric aircrafts.

Zero-emission Aircraft Market Growth Drivers:

Aggressive global aviation decarbonization targets and accelerating hydrogen-electric aircraft investments are creating unprecedented demand across the zero-emission aviation ecosystem:

The main driver of the structural growth of the Zero-emission Aircraft Market is the fast pace of aviation decarbonization strategy along with substantial financial commitments being made towards the development of aircraft technology based on hydrogen and electric energy. Stakeholders including governments, aerospace companies, airlines and technology companies are collectively focusing their efforts towards achieving net-zero aviation targets, thereby ensuring continuous demand for the next generation aircraft propulsion, light-weight materials, hydrogen-based infrastructure and advanced aircraft platforms.

In June 2025, Airbus launched development efforts to further develop hydrogen-powered aircraft systems through infrastructure partnerships and hydrogen aviation programs geared towards hastening commercialization routes. In addition, ZeroAvia conducted large-scale flight-testing projects for regional aircraft use, which marked their continued advancement into technologically viable means of moving into commercially viable zero-emissions aircraft platforms through 2026-2035.

Zero-emission Aircraft Market Restraints

Limited energy density of battery technologies, high hydrogen infrastructure costs, and certification complexity restricting large-scale commercialization of zero-emission aircraft:

One major barrier to the market for zero emission aircrafts is posed by the difficulty of providing adequate energy storage capability and energy efficiency for larger aircrafts. The existing technology for batteries suffers from inadequacies in energy density, range of flight, load carrying ability, and the efficiency of charging. Hydrogen powered aircraft require large amounts of investments in cryogenics for storing hydrogen, facilities for fueling the aircraft at airports, and ground handling facilities for such aircrafts.

Zero-emission Aircraft Market Opportunities

Regional hydrogen aviation ecosystems, next-generation airport infrastructure development, and commercialization of long-range sustainable aircraft platforms:

The scaling of integrated hydrogen aviation ecosystems constitutes the most disruptive long-term value creation potential within the Zero-emission Aircraft Market, where wide-scale adoption of hydrogen generation, distribution and refueling stations would facilitate greater commercialization of zero-emission aircraft outside existing short-range flights. Indeed, the creation of future airport infrastructure featuring state-of-the-art charging systems, hydrogen distribution capabilities and energy management software is leading to the creation of a brand-new aviation industry eco-system designed to accelerate adoption of these technologies. Moreover, ongoing advancements in lightweight materials, dense energy storage capacity and long range hydrogen propulsion systems open the door to the use of such technologies in large regional and commercial airliners, generating a new wave of demand in the 2026-2035 forecast period.

Recent Developments:

-

2026: ZeroAvia accelerated certification pathways for its ZA600 hydrogen-electric powertrain, completing expanded flight-testing campaigns with upgraded fuel cell stacks and electric propulsion systems, while securing additional airline partnerships in North America and Europe for regional turboprop retrofitting programs.

-

2026: Boeing strengthened its sustainable aviation R&D initiatives by expanding hybrid-electric propulsion and hydrogen combustion research programs, focusing on next-generation narrow-body aircraft architectures and improving cryogenic hydrogen storage safety systems for future commercial deployment.

-

2025: Joby Aviation progressed its electric vertical take-off and landing (eVTOL) commercialization strategy by expanding FAA certification flight testing and scaling pre-commercial production of its all-electric air taxi platform, targeting early urban deployment in U.S. metropolitan corridors.

-

2025: Archer Aviation advanced its Midnight eVTOL program through increased flight-testing cadence and manufacturing scale-up initiatives in the United States, supported by airline partnerships and urban air mobility infrastructure development agreements for commercial launch readiness.

-

2025: Rolls-Royce expanded its electric propulsion portfolio for zero-emission aviation by progressing high-power electric engine demonstrator programs and hybrid-electric aircraft propulsion systems aimed at regional aviation and advanced air mobility applications.

Zero-emission Aircraft Market Key Players

-

Airbus SE

-

Boeing Company

-

Embraer S.A.

-

ZeroAvia Inc.

-

Universal Hydrogen Co.

-

Joby Aviation Inc.

-

Archer Aviation Inc.

-

Eviation Aircraft Inc.

-

Heart Aerospace AB

-

Lilium GmbH

-

H2FLY GmbH

-

Pipistrel Aircraft (Textron Inc.)

-

magniX Ltd.

-

Rolls-Royce Electrical

-

Honeywell Aerospace Technologies

-

Safran S.A.

-

GKN Aerospace

-

Collins Aerospace

-

BAE Systems plc

-

Vertical Aerospace Ltd.

Zero-emission Aircraft Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 7.47 Billion |

| Market Size by 2035 | USD 25.65 Billion |

| CAGR | CAGR of 13.46% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Propulsion Technology (Battery Electric Aircraft, Hydrogen Fuel Cell Aircraft, Hydrogen Combustion Aircraft, Hybrid Electric Aircraft) • By Aircraft Type (Fixed-Wing Aircraft, Rotary-Wing Aircraft, Unmanned Aerial Vehicles (UAVs), Urban Air Mobility (eVTOL) Aircraft) • By Range (Short-Haul (<500 km), Regional (500–1,500 km), Medium-Haul (1,500–3,000 km), Long-Haul (>3,000 km)) • By Application (Commercial Passenger Transport, Cargo & Logistics, Military & Defense, Urban Air Mobility (UAM), General Aviation) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Airbus SE, Boeing Company, Embraer S.A., ZeroAvia Inc., Universal Hydrogen Co., Joby Aviation Inc., Archer Aviation Inc., Eviation Aircraft Inc., Heart Aerospace AB, Lilium GmbH, H2FLY GmbH, Pipistrel Aircraft (Textron Inc.), magniX Ltd., Rolls-Royce Electrical, Honeywell Aerospace Technologies, Safran S.A., GKN Aerospace, Collins Aerospace, BAE Systems plc, Vertical Aerospace Ltd. |

Frequently Asked Questions

The Zero-emission Aircraft Market is expected to grow at a CAGR of 13.46% from 2026 to 2035.

The Zero-emission Aircraft Market was valued at USD 7.47 billion in 2025.

Rapid acceleration of aviation decarbonization mandates, combined with large-scale investments in hydrogen-electric propulsion systems, battery-electric aircraft platforms, and urban air mobility infrastructure, is the primary growth driver of the Zero-emission Aircraft Market.

Battery Electric Aircraft dominated the market and Hydrogen Fuel Cell Aircraft is the fast-growing segment in Zero Emission Aircraft Market.

North America dominated the Zero-emission Aircraft Market in 2025.

Get in Touch