3D NAND Flash Memory Market Report Scope & Overview:

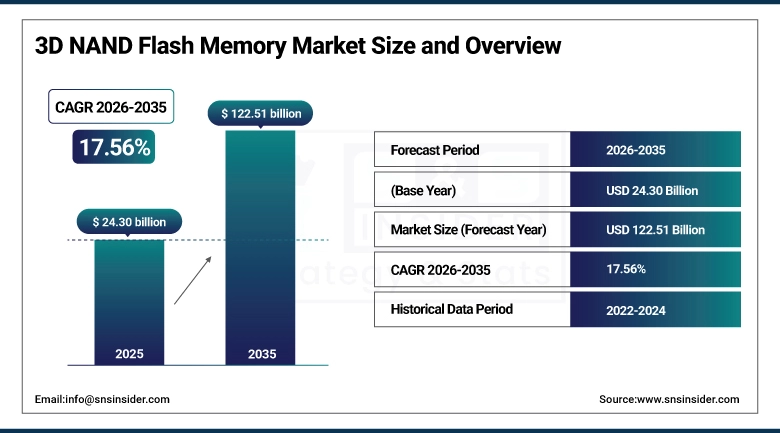

The 3D NAND Flash Memory Market size was valued at USD 24.30 Billion in 2025 and is projected to reach USD 122.51 Billion by 2035, growing at a CAGR of 17.56% during 2026–2035.

The global 3D NAND Flash Memory market is expected to be rapidly growing due to the demand for the low power consumption devices and the increasing use of high capacity storage in the smartphones, laptops and data centres. Key Factors Driving Growth of Stand-Alone Memory Market The increasing demand for cloud computing, artificial intelligence (AI), and big data analytics is pushing for much faster and reliable memory. Storage density and performance are being improved by ongoing technological developments such as upper layer stacking and non-volatile memory endurance. The growth of this 3D NAND market, helped by the ramp-on IoT devices, automotive electronics, and consumer electronics applications, is leading to a modern-age memory application.

3D NAND Flash Memory Market Size and Forecast:

-

Market Size in 2025: USD 24.30 Billion

-

Market Size by 2035: USD 122.51 Billion

-

CAGR: 17.56% during 2026–2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on 3D NAND Flash Memory Market - Request Free Sample Report

3D NAND Flash Memory Market Key Trends:

-

Rising demand for high-capacity and high-performance storage solutions is driving the 3D NAND Flash Memory market.

-

Growing adoption of smartphones, laptops, and data centers is contributing to increased memory requirements.

-

Advancements in 3D stacking technology and multi-layer NAND architectures are improving storage density and reliability.

-

Expansion of cloud computing, AI, and big data analytics is boosting the need for faster memory solutions.

-

Increasing integration of 3D NAND in automotive, IoT, and consumer electronics is supporting market growth.

-

Ongoing R&D and investments by memory manufacturers are driving innovation and adoption globally.

U.S. 3D NAND Flash Memory Market Size Outlook:

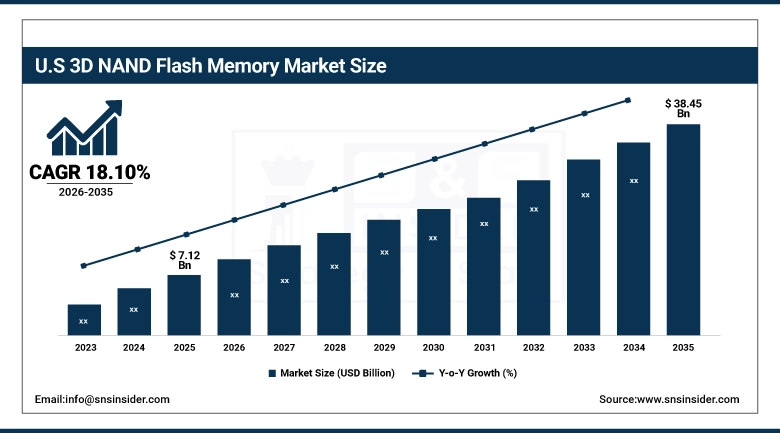

The U.S. 3D NAND Flash Memory Market size was valued at USD 7.12 Billion in 2025 and is projected to reach USD 38.45 Billion by 2035, growing at a CAGR of 18.10% during 2026–2035. The U.S. 3D NAND Flash Memory Market is growing due to rising demand for high-performance storage in smartphones, laptops, and data centers, along with advancements in 3D NAND stacking, cloud computing, AI applications, and the proliferation of IoT and consumer electronics.

3D NAND Flash Memory Market Key Drivers:

-

Rising demand for high-capacity, high-speed storage in smartphones, laptops, data centers, and enterprise applications is driving the market growth.

The cloud computing and increasing usage of AI, IOT connected devices and next-generation computing solutions are increasing the demand for 3D NAND flash memory type. Enjoying benefits such as increased storage density, improved read/write performance, and lower power consumption, it is being implemented in consumer electronics, enterprise storage systems, and in industrial applications.

3D NAND Flash Memory Market Key Restraints:

-

High manufacturing costs, complex fabrication processes, and technological limitations restrict rapid market adoption.

3D NAND flash memory needs cutting-edge semiconductor fabrication plants, tight process technology, and high investment costs at the initial state. Cost Implications of Yield High scaling challenges, potential yield concerns, and specialized equipment requirements make scaling more expensive. However, that process can be slow due to cost and complexity and competition from DRAM and other emerging memory alternatives leads to slow adoption cycles, particularly in smaller manufacturers and low-cost testo fill applications.

3D NAND Flash Memory Market Key Opportunities:

-

Expansion of AI, cloud services, and data-intensive applications presents significant growth potential.

Increase demand for high-density, energy-efficient storage opportunities in AI, machine learning, autonomous vehicles, and 5G infrastructure drives 3D NAND adoption. This facilitates innovation and growth in volumes through higher deployments in data centres, edge computing and high-performance computing systems. The partnership between semiconductor makers and system providers to offer high-density memory, along with developments in stacked technology and high-tier NAND, provide opportunities and possibilities for such products with both high capacity and low cost for worldwide memory market.

3D NAND Flash Memory Market Segments:

-

By Component Type: In 2025, NAND Flash Chips dominated with 58% share; Controllers expected to be the fastest growing segment during 2026–2035.

-

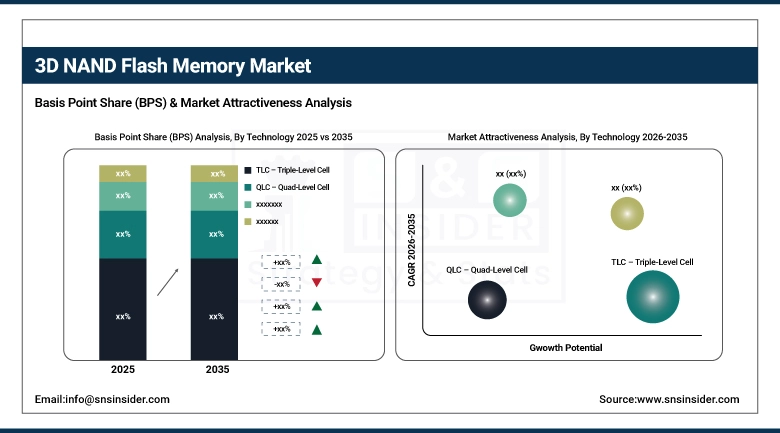

By Technology: In 2025, TLC (Triple-Level Cell) dominated with 54% share; QLC (Quad-Level Cell) expected to grow fastest during 2026–2035.

-

By Application: In 2025, Smartphones & Tablets dominated with 50% share; Data Centres expected to grow fastest during 2026–2035.

-

By End User: In 2025, Consumer Electronics dominated with 52% share; Enterprise & Cloud Storage expected to grow fastest during 2026–2035.

By Type, 3D NAND Dominated While 2D NAND Fastest Growing:

In 2025, 3D NAND took over the market as it was densely packed in terms of storage, cheaper per bit, and superior in terms of performance against the older-style 2D NAND. This technology is the foundation for next-generation devices in smartphones, SSDs and data centers, powering greater than 12 billion units by 2025 shipped worldwide. It stays at the top of the totem pole due to its capacity to scale and energy efficiency.

Demand continues in legacy devices and a variety of cost-sensitive applications, making 2D NAND the fastest growing segment. Growing usage for embedded storage, consumer electronics, and industrial solutions are enhancing the growth. Shipped worldwide 3 billion units of 2D NAND in 2025.

By Technology, TLC Dominated While QLC Fastest Growing:

TLC (Triple-Level Cell) quickly replaced its competitors early in the boom, presenting a good compromise of the average performance, reliability, and cost for consumer electronics, SSDs, and enterprise storage. In 2025, more than 10 billion TLC-based units were shipped, becoming the go-to for manufacturers.

The most rapidly expanding category, QLC (Quad-Level Cell), is a technology associated with high storage density and a low cost per GB. Cloud storage, datacenter and enterprise SSD adoption is here. There were 2.5 billion QLC shipments in 2025, and this is only the beginning of a quick market development.

By Application, Smartphones & Tablets Dominated While Data Centers Fastest Growing:

Due to the sheer number of mobile devices in the world, smartphones & tablets have commanded the bulk of the 3D NAND market thus far as they need the densest, most compact storage possible. The availability of rapid consumer demand and miniaturized device size features that were better refined in 2025 meant 8 billion plus units were now deployed.

Cloud computing, AI, and big data storage needs are a major driving force behind the largest and fastest growing segment of the embedded system and sensors market -- data centers. Expansion of hyperscale data centers in the U.S., China, and Europe created further need for high-capacity low-latency NAND solutions. More than 1.5 billion data center units were shipped globally in 2025.

By End User, Consumer Electronics Dominated While Enterprise & Cloud Storage Fastest Growing:

Consumer Electronics was largest by application owing to extensive usage in smartphones, tablets and laptops. In 2025, the segment represented more than half of shipments worldwide, backed by ongoing product releases along with storage-hungry uses for video gaming and multimedia.

This increase has made Enterprise & cloud storage the fastest growing segment thanks to the growing adoption of the hyperscale servers, the SSD arrays and the new AI-driven workloads. As large-scale high-density storage solutions become an inextricable requirement, over 2 billion units were expected to be shipped across cloud service providers and enterprise IT infrastructures by 2025.

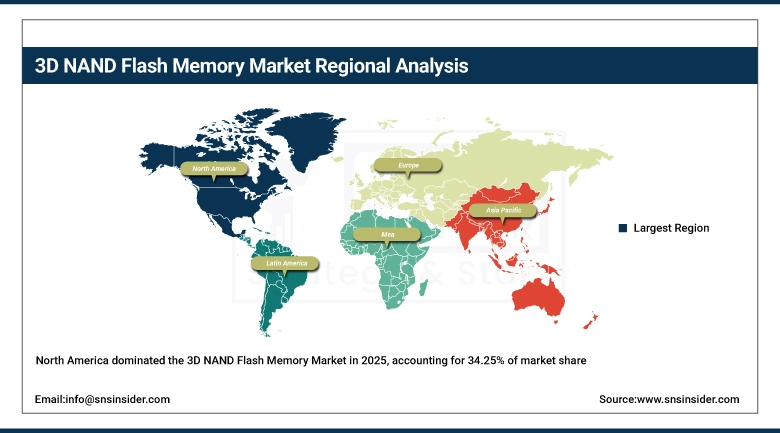

3D NAND Flash Memory Market Regional Analysis:

North America 3D NAND Flash Memory Market Insights:

The North America 3D NAND Flash Memory market, which contributes 34.25% share, is mainly driven by the presence of top semiconductor companies, mature data center infrastructure, along with high penetration of smartphones, laptops, and consumer electronics. The strong presence of R&D facilities, accessibility to high-end manufacturing technologies along with strong cloud computing infrastructural development will continue to demand high density and high performance storage in the U.S. and Canada. The market growth is also high through investments in AI, IoT, and edge computing.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia-Pacific 3D NAND Flash Memory Market Insights:

Asia Pacific 3D NAND Flash Memory Market is expected to register a CAGR of 19.32% during the period, 2026 to 2035. Rapid adoption of smartphones, growth of hyperscale data centers, established manufacturing capabilities in China, South Korea, and Taiwan, and growing demand for high-performance computing solutions in industrial, consumer electronics, and cloud applications has been driving this growth. Export of semiconductor industries supported the government for local production and the growing advanced storage technology investments are some which are adopting these markets.

Europe 3D NAND Flash Memory Market Insights:

Growth in demand for SSDs in enterprise storage, automotive electronics, and industrial automation propels the growth of the Europe 3D NAND Flash Memory market. The increasing adoption of technologies such as AI, cloud computing, and data centers being led by heavy-weight economies like Germany, France, and UK is expected to majorly contribute to the growing demand for high-density memory solutions.

Latin America 3D NAND Flash Memory Market Insights:

More smartphone penetration, extension of IT infrastructure and the increasing adoption of SSDs in businesses and governments is further increasing the growth for the Latin America 3D NAND Flash Memory market. Meanwhile, digital transformation initiatives are increasing storage demand in countries like Brazil, Mexico, and Argentina.

Middle East & Africa (MEA) 3D NAND Flash Memory Market Insights:

MEA 3D NAND Flash Memory market to grow steadily and reach above 20% annual growth fully backed up by the increase in Data Center Development, Cloud and more use of Mobile and Consumer Electronics. With investments in digital infrastructure and enterprise-type storage solutions supporting market growth across key markets including Saudi Arabia, UAE, and South Africa.

3D NAND Flash Memory Market Competitive Landscape:

Samsung Electronics Co. Ltd., the world leader in advanced semiconductor and memory solutions, creates innovative technologies that drive the evolution of 3D NAND flash memory for consumers, enterprises, and data centers. This is mainly due to high density and high performance NAND architectures, large R&D investments, and extensive manufacturing capacity. Early adoption of breakthrough memory technologies, along with supply chain capabilities, have reinforced Samsung's leadership position in the market as demand remains stable based on its strong presence in saturated and emerging markets for high-capacity storage.

-

In 2025, Samsung Electronics advanced 3D NAND technologies with increased layer counts and improved energy efficiency, enhancing storage density and performance for SSDs, smartphones, and cloud data centers, thereby strengthening its market leadership and adoption across multiple industry segments.

Intel Corporation is a leading semiconductor company with a strong presence in the 3D NAND flash memory market, emphasizing enterprise and data center storage solutions. Its market position is driven by cutting-edge technology, high reliability, and strategic partnerships with cloud service providers and hardware manufacturers. Intel’s leadership is supported by extensive R&D in memory architecture, early commercialization of innovative storage solutions, and a global distribution network that ensures continuous market demand.

-

In 2025, Intel Corporation launched next-generation 3D NAND products with improved endurance, lower power consumption, and enhanced scalability for data centers and enterprise applications, reinforcing its technological advantage and expanding adoption in critical high-performance storage segments.

3D NAND Flash Memory Companies are:

-

Samsung Electronics Co., Ltd.

-

Intel Corporation

-

Toshiba Memory Corporation

-

Micron Technology Inc.

-

SK Hynix Inc.

-

Kingston Technology Company, Inc.

-

Crucial Technology

-

Transcend Information Inc.

-

Phison Electronics Corporation

-

Infineon Technologies AG

-

Microchip Technology Inc.

-

ON Semiconductor

-

VIA Technologies Inc.

-

Integrated Silicon Solution Inc.

-

Western Digital Technologies, Inc.

-

ADATA Technology Co., Ltd.

-

Seagate Technology Holdings plc

-

NetApp Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 24.30 Billion |

| Market Size by 2035 | USD 122.51 Billion |

| CAGR | CAGR of 17.56% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component Type: (NAND Flash Chips, Controllers, Packages) • By Technology: (TLC – Triple-Level Cell, QLC – Quad-Level Cell, SLC – Single-Level Cell) • By Application: (Smartphones & Tablets, Data Centers, Laptops & PCs) • By End User: (Consumer Electronics, Enterprise & Cloud Storage, Automotive & Industrial) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Samsung Electronics Co., Ltd., Intel Corporation, Toshiba Memory Corporation, Western Digital Corporation, Micron Technology Inc., SK Hynix Inc., Kingston Technology Company, Inc., Crucial Technology, SanDisk Corporation, Transcend Information Inc., Phison Electronics Corporation, Infineon Technologies AG, Microchip Technology Inc., ON Semiconductor, VIA Technologies Inc., Integrated Silicon Solution Inc., Western Digital Technologies, Inc., ADATA Technology Co., Ltd., Seagate Technology Holdings plc, NetApp, Inc. |

Frequently Asked Questions

Ans: The 3D NAND Flash Memory Market is expected to grow at a CAGR of 17.56% during 2026–2035.

Ans: The 3D NAND Flash Memory Market size was valued at USD 24.30 Billion in 2025 and is projected to reach USD 122.51 Billion by 2035.

Ans: The key drivers of the 3D NAND Flash Memory Market include rising demand for high-density storage solutions, increasing adoption of smartphones, laptops, and enterprise data centers, rapid growth of cloud computing, advancements in memory technologies, and expanding digitalization across industries.

Ans: The 3D NAND Flash Memory segment dominated the market during the projected period.

Ans: North America dominated the 3D NAND Flash Memory Market in 2025.

Get in Touch