3D Printing Gases Market Report Scope & Overview:

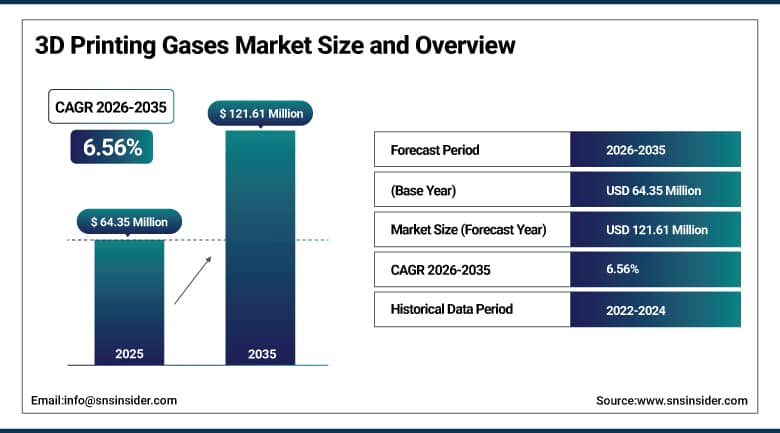

The 3D Printing Gases Market was valued at USD 64.35 Million in 2025 and is expected to reach USD 121.61 Million by 2035, growing at a CAGR of 6.56% from 2026–2035.

The global 3D printing gases market is expanding steadily in tandem with the additive manufacturing industry whose commercial scale-up across aerospace, automotive, healthcare, and industrial sectors create durable demand for high-purity inert and reactive gases. Argon and nitrogen serve as the inert atmosphere gases that prevent oxidation and contamination inside powder bed fusion build chambers, making them non-negotiable process inputs whose purity and supply consistency directly determine the mechanical integrity of printed metal components. Industrial-grade gas demand has expanded by over 18% as metal additive manufacturing transitions from prototyping into serial end-use component production. The market is shaped by the industrial gas majors whose existing production, storage, and distribution infrastructure gives them the supply chain capability to serve additive manufacturing facilities at the specification levels that aerospace, defence, and medical device applications require.

Linde plc is investing in application-specific gas mixture development for metal additive manufacturing customers, including custom argon and nitrogen blend formulations optimised for specific alloy systems and print parameters. This move demonstrates how industrial gas suppliers are transitioning beyond commodity gas supply toward value-added technical service relationships with additive manufacturing customers, with application engineering expertise creating genuine differentiation that pricing alone cannot achieve in a market where industrial gas purity is increasingly a table-stakes commodity.

3D Printing Gases Market Size and Forecast

-

Market Size in 2026E: USD 68.57 Million

-

Market Size by 2035: USD 121.61 Million

-

CAGR: 6.56% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On 3D Printing Gases Market - Request Free Sample Report

3D Printing Gases Market Trends

-

Rising metal additive manufacturing adoption in aerospace and automotive production is significantly increasing demand for high-purity argon and nitrogen inert atmosphere gases across powder bed fusion processes.

-

Growing use of medical-grade 3D printing for implants, surgical instruments, and prosthetics is driving demand for ultra-high-purity gas formulations meeting stringent healthcare regulatory compliance standards.

-

Increasing investment in on-site nitrogen and argon generation systems by large-scale additive manufacturing facilities is improving supply reliability and reducing per-unit gas cost for high-volume operations.

-

Expanding research into reactive gas applications in polymer and composite printing processes is broadening the addressable gas chemistry portfolio beyond the conventional inert gas dominance that currently defines the market.

-

Rising sustainability priorities are accelerating development of lower-emission gas production and recovery technologies that reduce the environmental footprint of additive manufacturing operations across all facility sizes.

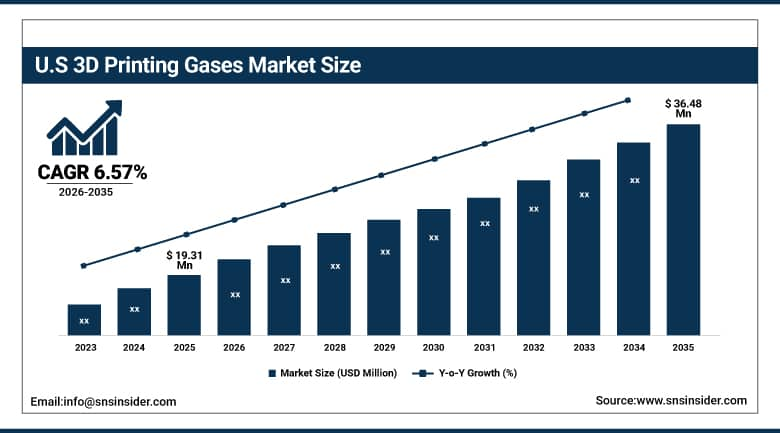

U.S. 3D Printing Gases Market Outlook

The U.S. 3D Printing Gases Market was valued at approximately USD 19.31 Million in 2025 and is expected to reach approximately USD 36.48 Million by 2035, growing at a CAGR of approximately 6.57%.

The United States is the world’s leading additive manufacturing adopter across aerospace, defence, and healthcare sectors whose stringent component quality requirements make high-purity inert gas atmosphere control a non-negotiable production prerequisite. The U.S. aerospace and defence industry’s metal printing programmes for titanium and nickel superalloy flight-critical hardware under FAA and DoD quality standards create exacting gas purity and supply consistency requirements. The healthcare sector’s growing adoption of metal additive manufacturing for patient-specific implants and dental prosthetics under FDA oversight creates a parallel high-value gas demand stream. Major suppliers including Air Liquide, Air Products, Linde, and Airgas serve these requirements through dedicated certification-capable supply programmes that industrial customers require.

Air Products extended its electronics and advanced manufacturing gas supply agreements with multiple additive manufacturing customers in 2024, incorporating new digital supply monitoring and predictive replenishment services that use connected cylinder and bulk tank telemetry to ensure continuous supply availability, eliminating production-interrupting gas depletion events at high-throughput metal printing facilities operating multiple simultaneous build cycles around the clock.

3D Printing Gases Market Segment Analysis

-

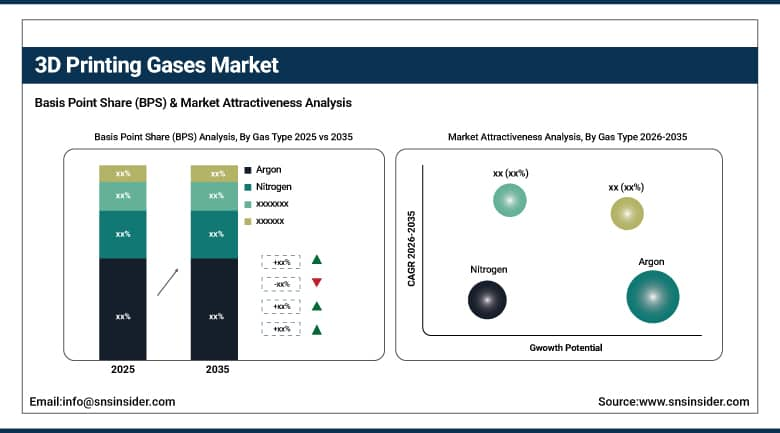

By Gas Type, argon dominated the market in 2025, with share of 39.1% as the preferred inert atmosphere gas for metal powder bed fusion processes, owing to its superior oxidation prevention across titanium, aluminium, and nickel superalloy applications. Nitrogen is the fastest-growing gas type, driven by its cost advantage over argon in applications where its reactivity profile is compatible with the alloy being printed.

-

By Technology, selective laser sintering and direct metal laser sintering collectively dominated the market in 2025 as the most commercially deployed metal additive manufacturing technologies requiring continuous inert atmosphere maintenance throughout build cycles. Electron beam melting is the fastest-growing technology, driven by adoption for high-value titanium and nickel superalloy aerospace components.

-

By Application, aerospace and defence dominated the market in 2025 through its combination of the highest component quality requirements, largest metal additive manufacturing investment, and strictest process control documentation needs. Healthcare is the fastest-growing application, driven by rapidly expanding medical implant, surgical instrument, and dental prosthetic additive manufacturing adoption under regulatory quality frameworks.

By Gas Type, argon dominates, nitrogen grows fastest

Argon retained the dominant gas type position in the 3D printing gases market in 2025, a commercial dominance reflecting its unique combination of chemical inertness across all printable metal alloy systems and physical properties that make it the most effective purge gas for powder bed fusion build chambers. Even trace oxygen or moisture contamination would compromise the mechanical properties and surface integrity of printed components whose quality standards are non-negotiable in aerospace and medical device production. Argon’s heavier-than-air density provides an additional advantage in maintaining inert atmosphere integrity, as the gas naturally settles and displaces lighter oxygen molecules during the purging sequence. The aerospace and defence sector’s titanium and nickel superalloy programmes almost universally specify argon because titanium is reactive with nitrogen at elevated build chamber temperatures, amplifying argon’s market leadership.

Nitrogen is the fastest-growing gas type, driven by its substantially lower production cost relative to argon combined with its technical suitability for the rapidly expanding range of steel, tool steel, aluminium, and polymer-composite printing applications where nitrogen’s slightly lower inertness relative to argon does not compromise component quality outcomes. The cost advantage of nitrogen becomes commercially significant at high-volume industrial manufacturing deployments where the argon-to-nitrogen price differential translates into meaningful per-part production cost savings that procurement teams weigh against technical specification requirements. On-site nitrogen generation through pressure swing adsorption and membrane separation further improves nitrogen’s cost competitiveness relative to delivered argon, enabling large-scale facilities to produce nitrogen supply at costs substantially below cylinder or bulk liquid procurement.

By Application, aerospace & defence dominates, healthcare grows fastest

Aerospace and defence retained the dominant application position in the 3D printing gases market in 2025, reflecting the sector’s combination of the longest metal additive manufacturing deployment history, the largest installed base of powder bed fusion and directed energy deposition systems, and the most demanding component quality and process documentation requirements of any industry vertical. The sector’s adoption of additive manufacturing for flight-critical engine components, structural brackets, heat exchangers, and fuel system parts under AS9100 and NADCAP quality management standards imposes strict requirements on gas purity certification and traceability documentation. The defence sector’s growing interest in distributed additive manufacturing for spare parts production at remote locations creates additional gas supply requirements for portable inert atmosphere generation systems that extend beyond conventional centralised industrial supply models.

Healthcare is the fastest-growing application segment in the 3D printing gases market, driven by the commercial expansion of metal additive manufacturing across orthopaedic implant, spinal fusion hardware, dental prosthetic, and surgical instrument production applications. The medical device manufacturing sector’s regulatory requirements under FDA 21 CFR Part 820 and EU MDR impose particularly stringent process validation, traceability, and purity documentation requirements on every manufacturing input including process gases, creating a compliance-driven commercial opportunity for industrial gas suppliers with the quality management systems and certification infrastructure to serve medical additive manufacturing customers at the documentation depth that regulatory inspections require.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

28.4% |

|

Asia Pacific |

China |

48.6% |

|

Middle East & Africa |

UAE |

32.1% |

|

Latin America |

Brazil |

44.2% |

North America 3D Printing Gases Market Insights

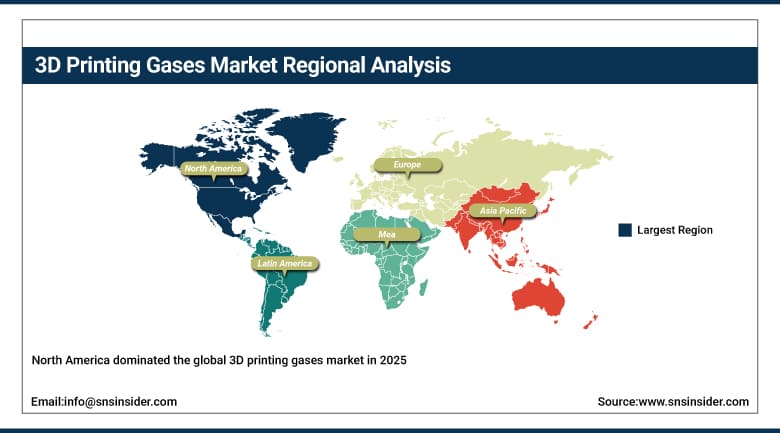

North America dominated the global 3D printing gases market in 2025, with the United States accounting for approximately 82.5% of North American revenues and representing the world’s largest national additive manufacturing market by installed equipment base and industrial adoption breadth. The region’s market leadership is sustained by the concentration of the world’s leading aerospace and defence prime contractors, medical device manufacturers, and automotive OEMs whose metal additive manufacturing programmes create the most commercially valuable industrial gas supply relationships. The distribution infrastructure operated by Linde’s Airgas division, Air Products, Air Liquide America, and Matheson across thousands of cylinder filling stations, bulk liquid delivery networks, and on-site generation installations provides the supply chain depth that reliably serves geographically dispersed additive manufacturing customers.

Canada contributes approximately 17.5% of North American revenues through its growing aerospace manufacturing sector, its medical device manufacturing industry, and advanced manufacturing research institutions whose additive manufacturing programmes create gas demand alongside the commercial production applications sustaining the national industrial consumption base.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe 3D Printing Gases Market Insights

Europe is a technically sophisticated 3D printing gases market where the continent’s advanced aerospace manufacturing ecosystem, exemplified by Airbus’s additive manufacturing programmes across its German, French, Spanish, and UK facilities, and its world-class automotive OEM investment in metal additive manufacturing for tooling, prototype, and increasingly serial production components sustain significant and growing industrial gas demand. Germany accounts for approximately 28.4% of European revenues as the region’s largest national market, driven by its automotive sector’s investment in 3D printing for jigs, fixtures, and structural components and its industrial manufacturing base’s progressive adoption of additive manufacturing for spare parts, tooling, and custom component production across machinery, energy equipment, and defence sectors.

The United Kingdom, France, and the Netherlands are significant secondary European markets where aerospace primes, medical device manufacturers, and advanced manufacturing research institutions sustain commercial gas demand alongside the growing private sector additive manufacturing service bureau industry. Linde AG’s European operations, Air Liquide’s industrial gases division, and Messer Group’s Central European coverage collectively serve the majority of European additive manufacturing gas requirements through established supply infrastructure.

Asia Pacific 3D Printing Gases Market Insights

Asia Pacific is the fastest-growing regional 3D printing gases market, driven by China’s government-supported additive manufacturing development programme, Japan’s precision manufacturing sector’s progressive adoption of metal printing for aerospace and automotive components, and India’s emerging aerospace and defence manufacturing sector whose government initiatives are creating domestic additive manufacturing capacity for previously imported components. China accounts for approximately 48.6% of Asia Pacific revenues through its combination of the world’s fastest-growing industrial 3D printing market, substantial government investment in additive manufacturing capability, and an active domestic industrial gas supply industry whose capacity expansion is keeping pace with additive manufacturing adoption.

Japan and South Korea represent mature secondary Asia Pacific markets where precision engineering culture and above-average industrial quality standards have driven early adoption of metal additive manufacturing, creating commercially valuable premium gas supply relationships with the local subsidiaries of Air Liquide, Linde, and Air Products serving these markets through established industrial gas distribution networks.

MEA & Latin America 3D Printing Gases Market Insights

The Middle East and Africa and Latin America are emerging 3D printing gases markets where development of domestic additive manufacturing capability is being driven by government industrial diversification programmes, defence sector modernisation, and the growing presence of international aerospace and automotive manufacturers establishing regional production operations incorporating 3D printing for tooling, prototype, and component applications. UAE leads MEA revenues at approximately 32.1% of the regional total through Dubai’s advanced manufacturing hub positioning and the UAE government’s explicit commitment to additive manufacturing as a strategic technology under the Dubai 3D Printing Strategy.

Brazil leads Latin American revenues at approximately 44.2% of the regional total through its aerospace manufacturing sector centred on Embraer’s additive manufacturing investment, its automotive OEM base’s tooling and prototype printing programmes, and its medical device industry’s growing adoption of metal additive manufacturing. White Martins (Linde), Air Liquide, and Air Products provide the Brazilian supply infrastructure for commercial additive manufacturing gas requirements.

Market Dynamics

Growth Drivers: Rapid metal additive manufacturing expansion in aerospace, healthcare, and automotive sectors driving sustained high-purity inert gas demand globally

The accelerating commercial adoption of metal powder bed fusion and directed energy deposition technologies across aerospace, healthcare, and automotive manufacturing is creating structurally growing demand for the argon, nitrogen, and helium process gases these technologies require continuously throughout every build cycle. The expanding installed base of industrial metal printers collectively represents a growing population of equipment each requiring regular high-purity gas consumption whose aggregate demand compounds with each year of market expansion.

The transition of additive manufacturing from prototype-focused to serial end-use component production in aerospace and medical device manufacturing is particularly significant for gas demand, as serial production creates continuous high-volume consumption that prototype production’s intermittent usage model does not generate at equivalent scale. Government aerospace and defence manufacturing investment in the U.S., Europe, and Asia Pacific is simultaneously creating new procurement relationships for industrial gas suppliers whose certified quality infrastructure serves the compliance requirements of defence prime contractors.

Restraints: High cost of ultra-high-purity gas grades and helium supply concentration limiting adoption economics in cost-sensitive applications

The premium pricing of ultra-high-purity argon and helium grades required for the most demanding aerospace and medical additive manufacturing applications creates per-part gas cost contributions that are commercially significant at the build cycle frequencies of industrial-scale printing systems, imposing procurement cost discipline on additive manufacturing operators whose process economics must compete with subtractive and casting manufacturing alternatives.

Helium’s particular supply concentration in natural gas fields in the U.S., Qatar, Russia, and Algeria creates both price volatility exposure and supply security risk for the subset of additive manufacturing applications that specifically require helium rather than argon or nitrogen, making helium supply chain resilience a strategic procurement concern for the aerospace and semiconductor manufacturing facilities whose processes cannot substitute alternative inert gases.

Opportunities: On-site gas generation investment, custom mixture development for new alloy systems, and Asia Pacific additive manufacturing expansion creating new demand pools

The investment case for on-site nitrogen and argon generation at high-volume additive manufacturing facilities is improving with each year of declining pressure swing adsorption and membrane separation equipment costs, creating a long-term commercial opportunity for industrial gas companies to transition from delivered gas supply toward on-site generation service contracts that capture installation, maintenance, and monitoring revenue alongside or instead of the product revenue that conventional delivery supply represents.

Custom gas mixture development for emerging alloy systems including copper, tungsten, and refractory metal additive manufacturing applications represents a value-added service opportunity whose margins substantially exceed commodity argon and nitrogen supply. Asia Pacific’s rapidly expanding additive manufacturing base creates the decade’s most commercially significant new regional demand pool for industrial gas suppliers with established local production and distribution infrastructure.

Recent Developments:

-

2025: Linde plc expanded its application engineering service for metal additive manufacturing customers, deploying dedicated gas application specialists at major aerospace and medical device manufacturing clusters across North America and Europe to optimise build chamber gas parameters and develop customer-specific argon and nitrogen supply solutions that improve print quality consistency and reduce per-build gas consumption through precision purge cycle management.

-

2024: Air Liquide announced investments in high-purity gas production capacity expansion across its European manufacturing network, specifically targeting the growing demand from metal additive manufacturing service bureaus and OEM in-house printing operations whose quality requirements for purity certification, traceability documentation, and supply continuity create demand for the premium product and service capabilities that Air Liquide’s industrial gas infrastructure is positioned to deliver.

-

2024: Air Products extended its electronics and advanced manufacturing gas supply agreements with multiple additive manufacturing customers, incorporating new digital supply monitoring and predictive replenishment services that use connected cylinder and bulk tank telemetry to ensure continuous supply availability and eliminate production-interrupting gas depletion events at high-throughput metal printing facilities.

3D Printing Gases Market Key Players

-

Linde plc

-

Air Liquide S.A.

-

Air Products and Chemicals Inc.

-

Messer Group GmbH

-

Airgas Inc. (Linde)

-

Matheson Tri-Gas Inc.

-

Praxair Technology Inc. (Linde)

-

BASF SE

-

Iceblick Ltd.

-

Nippon Sanso Holdings Corporation

-

Taiyo Nippon Sanso Corporation

-

SOL Group

-

Coregas Pty Ltd.

-

Gulf Cryo

-

Ellenbarrie Industrial Gases Ltd.

-

INOX Air Products Pvt. Ltd.

-

Wison Group

-

Universal Industrial Gases Inc.

-

Roberts Oxygen Company Inc.

-

EWS GmbH

3D Printing Gases Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 64.35 Million |

| Market Size by 2035 | USD 121.61 Million |

| CAGR | CAGR of 6.56% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Gas Type (Argon, Nitrogen, Helium, Carbon Dioxide, Gas Mixtures, Others) • By Technology (Selective Laser Sintering, Direct Metal Laser Sintering, Electron Beam Melting, Fused Deposition Modelling, Others) • By Application (Aerospace & Defence, Automotive, Healthcare & Medical, Industrial Manufacturing, Electronics, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Linde plc, Air Liquide S.A., Air Products and Chemicals Inc., Messer Group GmbH, Airgas Inc. (Linde), Matheson Tri-Gas Inc., Praxair Technology Inc. (Linde), BASF SE, Iceblick Ltd., Nippon Sanso Holdings Corporation, Taiyo Nippon Sanso Corporation, SOL Group, Coregas Pty Ltd., Gulf Cryo, Ellenbarrie Industrial Gases Ltd., INOX Air Products Pvt. Ltd., Wison Group, Universal Industrial Gases Inc., Roberts Oxygen Company Inc., EWS GmbH |

Frequently Asked Questions

The 3D Printing Gases Market is expected to grow at a CAGR of 6.56% from 2026 to 2035.

The 3D Printing Gases Market was valued at USD 64.35 Million in 2025.

Accelerating commercial adoption of metal powder bed fusion and directed energy deposition technologies across aerospace, healthcare, and automotive manufacturing.

Argon dominated as the preferred inert atmosphere gas for metal powder bed fusion processes across aerospace and healthcare applications.

North America dominated the 3D Printing Gases Market in 2025, with the United States accounting for approximately 82.5% of North American revenues.

Get in Touch