Autonomous Vehicle Sensor Market Report Scope & Overview:

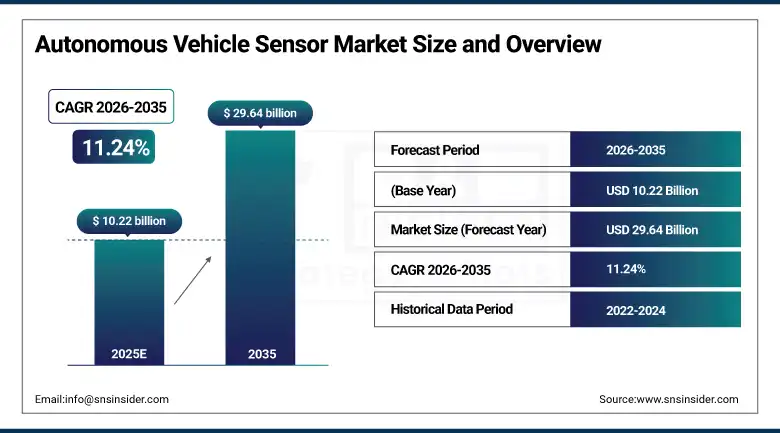

Autonomous Vehicle Sensor Market was valued at USD 10.22 billion in 2025 and is expected to reach USD 29.64 billion by 2035, growing at a CAGR of 11.24% from 2026 to 2035.

Road safety has long been one of the most persistent and costly challenges facing modern transportation systems, and the inadequacy of human perception in real traffic environments is now widely acknowledged as the root cause of over 90 percent of all vehicular accidents recorded globally each year. Autonomous vehicle sensors have stepped into this critical gap as the foundational layer of machine-driven perception, enabling vehicles to continuously read their environment with a level of accuracy, consistency, and speed that human drivers simply cannot replicate. LiDAR systems construct precise three-dimensional maps of the surrounding space, radar modules detect moving objects through rain, fog, and darkness, high-resolution cameras decode lane markings and traffic signs, and ultrasonic sensors manage low-speed proximity hazards in parking and urban environments. When these technologies operate together within a well-designed sensor fusion architecture, the resulting perception capability is vastly more reliable than any single sensing modality alone. Automotive original equipment manufacturers across North America, Europe, China, Japan, and South Korea are now embedding increasingly capable sensor suites into vehicles at every price point, from basic ADAS features in entry-level compact cars to full Level 4 autonomy in purpose-built robotaxi and autonomous truck platforms. The trajectory from partial assistance to full self-driving capability is being navigated at pace, powered by advances in solid-state LiDAR miniaturization, millimeter-wave radar resolution, AI-accelerated sensor fusion software, and regulatory frameworks that are steadily broadening the geographic footprint where autonomous driving is legally permitted.

Autonomous vehicles operating at Level 3 and above now carry sensor arrays that process hundreds of gigabytes of raw perception data per hour, and the ability to fuse that information reliably across all weather conditions, light levels, and traffic scenarios has become the central engineering challenge separating leading players from the rest of the field, with sensor accuracy at the 99.99 percent reliability threshold increasingly regarded by regulators, insurers, and OEMs as the minimum acceptable standard for any commercially deployed driverless system.

Autonomous Vehicle Sensor Market Size and Forecast

-

Market Size in 2025: USD 10.22 Billion

-

Market Size by 2035: USD 29.64 Billion

-

CAGR: 11.24% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026 to 2035

-

Historical Data: 2022 to 2024

To Get more information On Autonomous Vehicle Sensor Market - Request Free Sample Report

Autonomous Vehicle Sensor Market Trends

-

Rapid scaling of solid-state LiDAR technology across both passenger and commercial vehicle segments as falling unit costs, improved detection range, and compact form factors make integration into standard vehicle platforms economically and structurally practical for mass-market OEM deployment.

-

Accelerating transition toward centralized sensor fusion architectures in which high-performance system-on-chip processors consolidate data streams from LiDAR, radar, cameras, and ultrasonic arrays into a unified real-time environmental model that supports faster and more reliable automated decision-making.

-

Growing adoption of 4D imaging radar systems capable of measuring the velocity, range, azimuth, and elevation of surrounding objects simultaneously, providing a substantial upgrade over conventional 2D radar in complex urban driving scenarios involving pedestrians, cyclists, and dense traffic.

-

Rising investment by automotive OEMs and Tier-1 suppliers in AI-native sensor processing platforms that apply deep learning algorithms directly at the sensor edge, reducing latency, bandwidth requirements, and computational load on central vehicle processors while improving object classification accuracy.

-

Expanding regulatory mandates across the European Union, United States, China, and Japan requiring the fitment of forward collision warning, automatic emergency braking, lane departure warning, and blind spot detection systems across progressively broader vehicle categories, driving substantial incremental sensor volume growth.

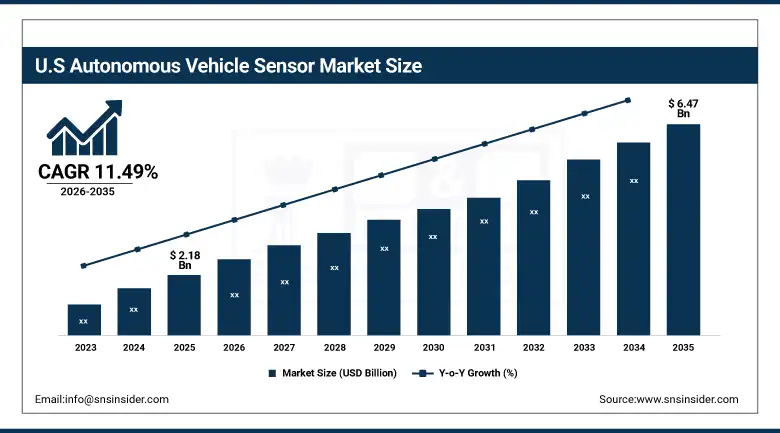

U.S. Autonomous Vehicle Sensor Market was valued at USD 2.18 billion in 2025 and is expected to reach USD 6.47 billion by 2035, registering a CAGR of 11.49% during 2026 to 2035.

The United States stands at the technological frontier of autonomous vehicle sensor development, anchored by the world's most active concentration of autonomous vehicle testing programs, the deepest pool of venture and corporate investment capital directed at autonomy technology, and a regulatory environment in which federal agencies and state governments are progressively constructing the legal framework necessary for large-scale commercial autonomous vehicle deployment. California remains the epicenter of AV sensor innovation, hosting testing programs operated by Waymo, Cruise, Zoox, Nuro, Aurora, and dozens of smaller technology developers whose fleets collectively accumulate millions of miles of real-world sensor data annually. The National Highway Traffic Safety Administration's increasing emphasis on mandatory ADAS fitment is simultaneously driving sensor demand across the mainstream automotive market, as every new vehicle safety mandate directly translates into additional camera, radar, or sensor unit volume for suppliers. Silicon Valley's integrated ecosystem of sensor hardware startups, AI software companies, semiconductor designers, and automotive systems integrators creates a competitive innovation environment that continues to produce both incremental refinements to existing sensor technologies and genuinely disruptive architectural advances.

The convergence of federal infrastructure investment under the IIJA, state-level autonomous vehicle pilot programs spanning commercial trucking corridors and urban robotaxi zones, and the deepening strategic alignment between major automotive OEMs and semiconductor companies including Nvidia, Qualcomm, and Mobileye is creating an innovation and deployment ecosystem in the United States that will sustain sensor market growth well beyond the near-term ADAS wave, positioning the country as both the world's largest single national market and its most important source of next-generation sensing technology through 2035.

Autonomous Vehicle Sensor Market Segment Insights

-

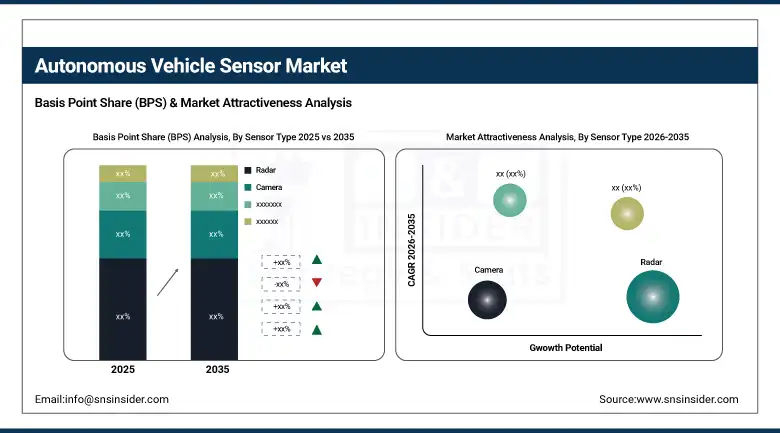

Based on Sensor Type, Radar accounted for the largest market share of 30% in 2025; LiDAR is expected to be the fastest growing sensor type during the forecast period.

-

Based on Vehicle Type, Passenger vehicles accounted for the largest market share of 64% in 2025; Commercial vehicles are expected to record the fastest growth through the forecast period.

-

Based on Level of Autonomy, Level 1 systems accounted for the largest market share of 39% in 2025; Level 4 and 5 systems are expected to be the fastest growing segment through 2035.

Autonomous Vehicle Sensor Market Segment Analysis

By Sensor Type, Radar dominates, LiDAR expected to grow fastest

Radar sensors maintained their position as the leading sensor type in the autonomous vehicle sensor market in 2025, accounting for approximately 30% of total revenue. The segment's established dominance is rooted in radar's combination of mature technology, competitive pricing relative to alternatives, and a performance envelope that covers the most safety-critical driving scenarios including high-speed forward collision detection, adaptive cruise control, and blind spot monitoring under virtually all weather and lighting conditions. Millimeter-wave radar operates effectively through heavy rain, fog, dust, and bright sunlight that can degrade camera and early-generation LiDAR performance, making it the foundation of every credible ADAS safety architecture. The increasing shift toward 4D imaging radar, which adds elevation measurement to the traditional range-velocity-azimuth capability of conventional systems, is extending radar's functional reach into applications that previously required LiDAR, further reinforcing its central role in both ADAS and autonomy platforms.

LiDAR is projected to record the highest growth rate among all sensor types through 2035, with its adoption accelerating rapidly as solid-state architectures eliminate the mechanical rotating components that made early LiDAR systems expensive, fragile, and impractical for production vehicle integration. The combination of falling hardware costs, rising detection range and resolution, and shrinking form factors is enabling LiDAR to move from specialist robotaxi and premium passenger vehicle programs into mainstream automotive platforms. Automotive-grade solid-state LiDAR modules are now entering production at price points that make integration economically viable for mid-range passenger vehicles, and the expanding fitment of Level 3 and Level 4 autonomy systems across commercial trucking, autonomous shuttle, and robotaxi platforms is generating high-volume procurement orders that will sustain strong LiDAR market growth throughout the forecast period.

By Vehicle Type, Passenger vehicles dominate, Commercial vehicles expected to grow fastest

The passenger vehicle category held around 64% share within the vehicle type category in 2025 on the back of high production of passenger cars around the world and the penetration of advanced driver assistance system features within all types of vehicles ranging from luxury vehicles to economy hatchbacks. Regulatory requirements for collision warning, automatic emergency braking, and lane assistance have made the integration of sensors not just a premium offering but a standard feature in all kinds of passenger vehicles. Consumer demand for connected, safe, and increasingly autonomous vehicles is generating commercial demand for more advanced sensor technology beyond what is required by regulation.

Commercial vehicles represent the fastest growing vehicle segment for autonomous vehicle sensors through 2035, propelled by the powerful economic case for automation in freight logistics, last-mile delivery, and public transit applications. Autonomous trucking programs led by operators including Aurora, Kodiak, and Gatik are demonstrating measurable cost reductions in fuel efficiency, driver labor, and operational safety across highway freight corridors, accelerating fleet operator interest in autonomous sensor systems at scale. Regulatory progress in permitting Level 4 truck operations on designated highway routes in the United States and Europe is creating the policy foundation for commercial deployment, while the persistent shortage of qualified long-haul truck drivers in major economies provides a powerful economic incentive for fleet operators to absorb the capital cost of autonomous sensor integration.

By Level of Autonomy, Level 1 dominates, Level 4 and 5 expected to grow fastest

Level 1 automation systems retained the largest share of the autonomy segment in 2025, accounting for approximately 39% of market revenue, reflecting the massive installed base of vehicles equipped with single-axis driver assistance features such as adaptive cruise control and lane-keeping assist. The volume dominance of Level 1 is fundamentally a function of scale: regulatory mandates requiring basic safety systems across virtually all new passenger vehicles sold in major markets create an enormous and predictable base load of sensor demand that will persist throughout the forecast period. Entry-level camera and radar sensors deployed in Level 1 systems represent the broadest and most cost-sensitive portion of the sensor market, where competition between established Tier-1 suppliers and emerging challengers is intense.

Level 4 and Level 5 autonomy systems are projected to experience the highest compound annual growth rate between 2026 and 2035 as fully autonomous vehicle programs transition from testing and pilot operations to commercial fleet deployment in robotaxi, autonomous trucking, and urban mobility applications. Each Level 4 or Level 5 vehicle requires a significantly more sophisticated and higher-value sensor array than any lower-automation platform, incorporating multiple long-range LiDAR units, redundant radar arrays, high-resolution cameras with full 360-degree field coverage, and ultrasonic proximity sensors, creating a per-vehicle sensor content value several times greater than a comparably sized Level 2 platform. Expanding regulatory approvals for fully autonomous commercial operations in the United States, China, Germany, and the United Kingdom are directly enabling this growth by creating the legal framework within which Level 4 fleet operators can generate the revenue needed to justify large-scale sensor procurement.

Autonomous Vehicle Sensor Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

42% |

|

Europe |

Germany |

28% |

|

Asia Pacific |

China |

35% |

|

Middle East & Africa |

Israel |

18% |

|

Latin America |

Brazil |

22% |

North America Autonomous Vehicle Sensor Market Insights

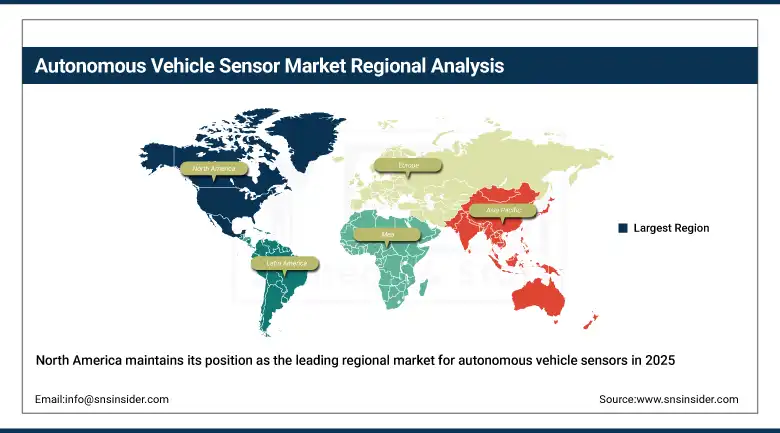

North America maintains its position as the leading regional market for autonomous vehicle sensors in 2025, contributing approximately 42% of global market revenue. The United States anchors regional dominance through its unparalleled concentration of autonomous vehicle development activity, the world's largest and most mature ADAS-equipped passenger vehicle fleet, and federal regulatory initiatives that are progressively requiring more sophisticated sensor-based safety features across vehicle categories. California's corridor of autonomous vehicle technology companies has established a self-reinforcing innovation ecosystem that consistently produces the sensor hardware and software advances that eventually find their way into production vehicles globally. Canada is contributing meaningfully through its growing autonomous vehicle research infrastructure centered in Toronto and Waterloo, supported by federal funding for connected and automated vehicle programs. The U.S. market alone is expected to grow from USD 2.18 billion in 2025 to USD 6.47 billion by 2035.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Autonomous Vehicle Sensor Market Insights

The Asia Pacific region is the most dynamic growth region in the world when it comes to the demand for sensors for autonomous vehicles, with China being the largest market for vehicles with sensors in terms of volume, as well as an important hub for technological developments of sensors. Chinese car manufacturers, among which BYD, SAIC, GAC, and other native EV brands are notable examples, implement LiDAR, radar, and high-resolution cameras in their product portfolios due to competitive pressure and government support for intelligent cars. Intelligent connectivity and autonomy are two key components of the Chinese government's strategy for New Energy Vehicles, and the market is further supported by government procurement, R&D grants, and infrastructure for V2X communications. Japan and South Korea also play a significant role due to their presence on the global automotive market, with Toyota, Honda, Hyundai, and Kia developing autonomous vehicle solutions.

Europe Autonomous Vehicle Sensor Market Insights

Europe is well-established in the global autonomous vehicle sensors market due to the presence of high-end automobile manufacturers on the continent whose vehicles have been ahead of others when it comes to integrating ADAS features. Germany plays an important role in the European market since it houses Volkswagen Group, BMW, Mercedes-Benz, and Continental, which are all companies deeply involved in autonomous driving technology. Some of the biggest sensor buyers in the world come from Europe. The mandate of the EU General Safety Regulation that requires all new cars in Europe to come with emergency lane-keeping, intelligent speed assistance, and advanced emergency braking from mid-2024 is contributing to high sensor demand in Europe. European Tier-1 suppliers such as Bosch, Continental, Valeo, and ZF are not only supplying OEMs but also innovating in sensor technology, making Europe a manufacturing and development hub for sensors in addition to being an important end market for sensors.

Middle East & Africa and Latin America Autonomous Vehicle Sensor Market Insights

The Middle East and Africa and Latin America regions represent emerging growth opportunities for the autonomous vehicle sensor market, with adoption currently concentrated in premium import vehicles and early-stage autonomous testing programs. Israel is disproportionately influential in the MEA region through its globally significant autonomous vehicle technology sector, home to Mobileye, one of the world's leading ADAS and autonomy platform developers, as well as a dense ecosystem of sensor and autonomy startups that serve OEM customers across North America, Europe, and Asia. The Gulf Cooperation Council states are actively developing smart mobility infrastructure and have launched autonomous shuttle and robotaxi pilot programs that are creating early demand for high-specification sensor systems. Brazil leads Latin American adoption as the region's largest automotive market, with OEM production facilities increasingly incorporating globally-standard ADAS equipment, and government road safety initiatives supporting the broader adoption of collision avoidance technologies.

Autonomous Vehicle Sensor Market Growth Drivers:

Escalating mandatory ADAS fitment requirements and road safety regulations creating structural sensor volume demand globally

The single most consistent and predictable driver of long-term sensor market growth is the worldwide expansion of government mandates requiring the fitment of sensor-based safety systems across progressively broader categories of road vehicles. Unlike market demand driven by consumer preference, which can fluctuate with economic conditions and product cycles, regulatory requirements create legally binding and time-defined procurement obligations that translate directly into sensor volume irrespective of broader automotive market conditions. The European Union's General Safety Regulation, the United States NHTSA's progressive ADAS requirements, China's intelligent vehicle standards, and equivalent frameworks across Japan, South Korea, Australia, and major Latin American economies are collectively creating a regulatory wave that will drive hundreds of millions of additional sensor units into global vehicle production over the course of the forecast period. Each new mandate adds both the direct sensor requirement and the associated wiring, processing, and integration infrastructure, making regulatory compliance a significant and growing portion of overall vehicle bill of materials for OEMs worldwide.

The convergence of road safety regulation, consumer demand for convenience features, and the commercial imperative to develop fully autonomous revenue-generating platforms across robotaxi, commercial trucking, and last-mile delivery applications is producing a multi-layered demand structure for autonomous vehicle sensors that is simultaneously driven by volume at the low end of the autonomy spectrum and by high unit value at the fully autonomous end, creating a uniquely resilient and compounding growth profile across the full forecast horizon.

Autonomous Vehicle Sensor Market Restraints

High component costs and weather-related performance limitations constraining rapid advancement to higher autonomy levels

Despite the substantial progress achieved in reducing sensor production costs over the past several years, the total sensor system cost of a vehicle equipped for Level 3 or Level 4 autonomous operation remains a meaningful barrier to rapid mass-market penetration beyond the premium vehicle segment. A fully capable Level 4 sensor suite incorporating multiple LiDAR units, 4D radar arrays, a comprehensive camera system, and the associated processing hardware can add several thousand dollars to vehicle manufacturing costs, representing a significant proportion of overall vehicle selling price in volume segments where cost sensitivity is high. Beyond cost, the variable performance of current sensor technologies in adverse weather conditions including heavy rain, snow, fog, and ice continues to represent a genuine reliability limitation that autonomous vehicle developers must address before fully driverless operation can be safely and legally extended to the full range of geographic and climatic environments in which road vehicles operate.

Autonomous Vehicle Sensor Market Opportunities

Solid-state sensor cost reduction, commercial fleet automation, and V2X infrastructure creating high-value growth vectors

The transition of LiDAR technology from mechanical spinning designs to solid-state architectures represents one of the most significant cost reduction and performance improvement opportunities currently reshaping the sensor market, with solid-state LiDAR unit prices falling toward the threshold that makes integration economically viable in mainstream passenger vehicles and simultaneously enabling the high-reliability, high-volume production required for fleet-scale commercial deployment. The commercial vehicle automation opportunity is equally compelling, as the economics of eliminating driver labor costs across long-haul trucking, port logistics, mining, and urban delivery operations justify substantially higher sensor investment than the passenger vehicle market, creating a premium value segment that will grow rapidly as regulatory approvals expand. The concurrent build-out of Vehicle-to-Everything communication infrastructure in major cities across China, the United States, South Korea, and Europe is creating the complementary data layer that allows sensors onboard individual vehicles to be augmented by roadside infrastructure perception, improving overall system safety and enabling autonomy in scenarios where individual vehicle sensor coverage alone would be insufficient.

Recent Developments:

-

2026: Mobileye announced the commercial launch of its SuperVision Level 3 automated driving system across a major European OEM's premium sedan lineup, integrating a dense array of cameras, radar, and ultrasonic sensors with its proprietary EyeQ6 chip platform to enable hands-free driving across highway and urban environments without requiring LiDAR, demonstrating the viability of camera-first autonomy architectures at scale.

-

2025 (October): NVIDIA Corporation entered a strategic partnership with Uber to supply its DRIVE AGX Hyperion 10 platform for the deployment of the world's largest Level 4-ready robotaxi fleet, targeting 100,000 autonomous vehicles beginning in 2027, incorporating a comprehensive sensor stack designed to meet the redundancy and reliability standards required for fully driverless commercial operations.

-

2025 (August): FORVIA HELLA introduced its fifth-generation steer-by-wire sensor platform, delivering enhanced precision for electric steering systems in premium vehicle programs across Germany and China and marking a significant step toward the sensor-integrated chassis architectures that fully autonomous vehicles require for reliable dynamic control independent of mechanical steering feedback.

-

2025 (May): Continental AG announced that cumulative production of its automotive radar sensors had exceeded 200 million units globally, underscoring its manufacturing scale leadership in the ADAS sensor market while simultaneously unveiling its next-generation compact radar module targeting Level 2 and Level 3 passenger vehicle platforms with improved object classification and reduced form factor.

-

2025 (April): Mercedes-Benz entered a strategic collaboration with Luminar Technologies to co-develop and integrate next-generation Halo LiDAR sensors across future vehicle models targeting higher levels of automated driving functionality, accelerating the company's advanced perception roadmap and deepening the integration between premium automotive design requirements and cutting-edge LiDAR hardware development.

Autonomous Vehicle Sensor Market Key Players

-

Robert Bosch GmbH

-

Continental AG

-

Denso Corporation

-

Valeo SA

-

Aptiv PLC

-

ZF Friedrichshafen AG

-

Mobileye Global Inc.

-

Velodyne Lidar Inc.

-

Luminar Technologies Inc.

-

Innoviz Technologies Ltd.

-

NXP Semiconductors N.V.

-

Texas Instruments Incorporated

-

STMicroelectronics N.V.

-

Infineon Technologies AG

-

Hella GmbH & Co. KGaA (FORVIA HELLA)

-

Hesai Technology Co. Ltd.

-

Ouster Inc.

-

Quanergy Systems Inc.

-

Cepton Technologies Inc.

-

Veoneer Inc.

Autonomous Vehicle Sensor Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 10.22 Billion |

| Market Size by 2035 | USD 29.64 Billion |

| CAGR | CAGR of 11.24% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Sensor Type (LiDAR, Radar, Camera, Ultrasonic, Infrared) • By Vehicle Type (Passenger, Commercial) • By Level of Autonomy (Level 1, Level 2, Level 3, Level 4 & 5) • By Application (Collision Detection, Adaptive Cruise Control, Traffic Sign Recognition, Parking Assistance, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Robert Bosch GmbH, Continental AG, Denso Corporation, Valeo SA, Aptiv PLC, ZF Friedrichshafen AG, Mobileye Global Inc., Velodyne Lidar Inc., Luminar Technologies Inc., Innoviz Technologies Ltd., NXP Semiconductors N.V., Texas Instruments Incorporated, STMicroelectronics N.V., Infineon Technologies AG, Hella GmbH & Co. KGaA (FORVIA HELLA), Hesai Technology Co. Ltd., Ouster Inc., Quanergy Systems Inc., Cepton Technologies Inc., Veoneer Inc. |

Frequently Asked Questions

North America dominated the Autonomous Vehicle Sensor Market in 2025 with approximately 42% of global revenue, anchored by the United States through its unmatched concentration of autonomous vehicle development programs, deep ADAS fitment across the mainstream passenger vehicle fleet, and a rapidly expanding commercial autonomous trucking sector supported by favorable regulatory progress and substantial private investment.

The Passenger Vehicle segment dominated with approximately 64% of vehicle type segment revenue in 2025, reflecting the large scale of global passenger car production, the deepening regulatory requirement for safety sensor fitment, and strong consumer demand for ADAS features across price segments.

The Radar segment dominated the Autonomous Vehicle Sensor Market in 2025 with approximately 30% of total revenue, driven by its all-weather reliability, cost competitiveness, and central role in the full range of ADAS safety features deployed across passenger and commercial vehicle platforms globally.

The escalating global regulatory requirement for sensor-based vehicle safety systems, combined with the rapid expansion of autonomous driving programs across robotaxi, commercial trucking, and passenger vehicle platforms, is the primary structural driver, reinforced by continuous advances in LiDAR cost reduction, AI-powered sensor fusion, and the build-out of supportive intelligent transportation infrastructure across major automotive markets.

The Autonomous Vehicle Sensor Market was valued at USD 10.22 billion in 2025.

The Autonomous Vehicle Sensor Market is expected to grow at a CAGR of 11.24% from 2026 to 2035.

Get in Touch