Bioprosthetics Market Report Scope & Overview:

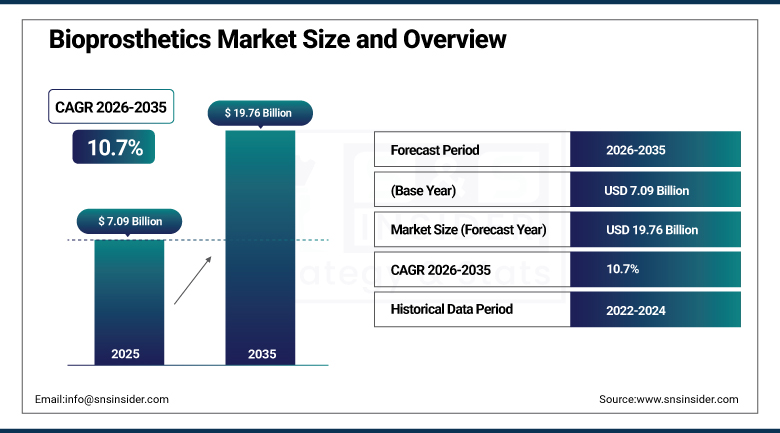

The Bioprosthetics Market was valued at USD 7.09 Billion in 2025 and is expected to reach USD 19.76 Billion by 2035, growing at a CAGR of 10.7% from 2026–2035.

Market for bioprosthetics across the globe is witnessing remarkable growth. Bioprosthetics refer to bio-material tissue implants, which have the added advantage of excellent biocompatibility and lesser thrombogenicity and hence better integration with body tissues as compared to other alternatives. Cardiovascular diseases, aging population, and improvements in technology for tissue processing are some of the factors responsible for driving average growth rates in this industry. The most dominant market share is enjoyed by the cardiovascular sub-segment with about 81% contribution towards the market revenues on account of bioprosthetic heart valve replacement and vascular grafting.

Edwards Lifesciences received FDA approval for the RESILIA tissue technology platform applied to the INSPIRIS RESILIA aortic valve in 2025, demonstrating superior anti-calcification performance relative to conventional glutaraldehyde-preserved tissue valves.

Market Size and Forecast:

-

Market Size in 2026E: USD 7.85 Billion

-

Market Size by 2035: USD 19.76 Billion

-

CAGR: 10.7% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Bioprosthetics Market- Request Free Sample Report

Bioprosthetics Market Trends:

-

Expanding adoption of transcatheter bioprosthetic valve implantation (TAVI) across broader patient populations is driving market growth.

-

Advances in tissue engineering are improving biocompatibility, durability, and natural tissue integration of bioprosthetic implants.

-

Development of anti-calcification technologies is extending implant lifespan and reducing structural deterioration.

-

Bioengineered vascular grafts are gaining traction due to improved patency rates and reduced immunogenicity.

-

3D printing and computational modeling are enabling customized, patient-specific bioprosthetic implant solutions

U.S. Bioprosthetics Market Outlook:

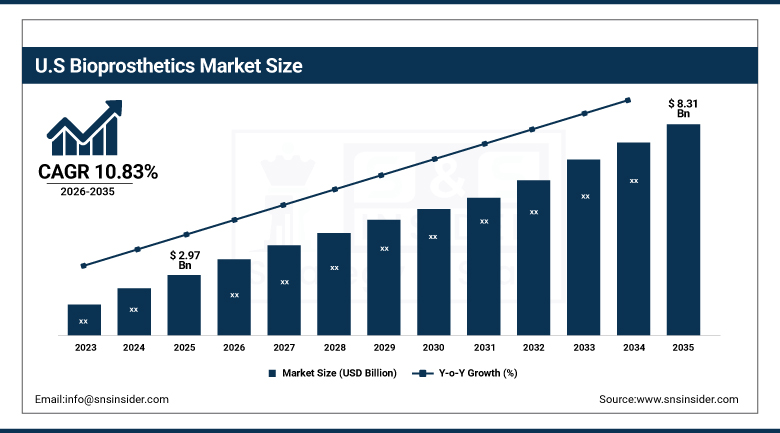

The U.S. Bioprosthetics Market was valued at approximately USD 2.97 Billion in 2025 and is expected to reach approximately USD 8.31 Billion by 2035, growing at a CAGR of approximately 10.83%.

The United States is the largest market for bioprosthetic devices in the world. Companies such as Edwards Lifesciences, Medtronic, and Abbott have their headquarters in the U.S. and together represent the cutting edge of bioprosthetic heart valve technology. Coverage by the CMS for TAVI in intermediate and low-risk patients has greatly increased the number of bioprosthetic valve procedures eligible for reimbursement. Funding from NIH on tissue engineering technologies provides the fuel for innovation to develop new bioengineered bioprosthetic products. Commercial acumen of the U.S. market is apparent in the higher-than-average usage of TAVI procedures, RESILIA tissue technology commercialization, and bioengineered human tissue vascular grafts.

Humacyte received FDA Breakthrough Device Designation for its Human Acellular Vessel in 2025, advancing the first bioengineered human tissue vascular graft programme toward commercial approval for arteriovenous access and below-knee reconstruction indications.

Bioprosthetics Market Segment Analysis:

-

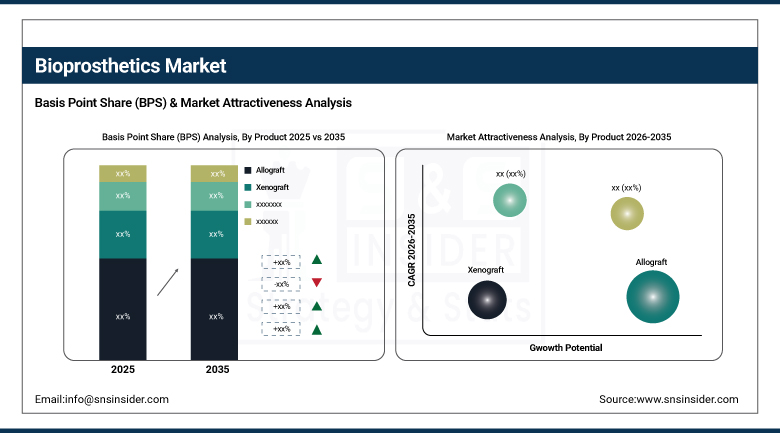

By Product, the Allograft segment dominated the bioprosthetics market with 68% share in 2025, while the Xenograft segment is the fastest growing with a CAGR of approximately 12.5%.

-

By Application, the Cardiovascular segment dominated the bioprosthetics market with approximately 81% share in 2025, while the Orthopaedic segment is the fastest growing with a CAGR of approximately 14.2% as biologic tissue augmentation for rotator cuff repair, tendon reconstruction, and cartilage restoration gains clinical adoption.

-

By End User, the Hospitals segment dominated the bioprosthetics market with approximately 72% share in 2025, while the Ambulatory Surgical Centers segment is the fastest growing with a CAGR of approximately 13.8% as minimally invasive bioprosthetic procedures migrate from hospital to outpatient settings.

By Product, allografts dominate, xenografts grow fastest

Allografts retained the dominant product position with 68% of the bioprosthetics market in 2025. Their commercial primacy reflects the multiple clinical advantages that human tissue-sourced bioprosthetics provide over animal-derived and synthetic alternatives. Allografts’ long-term stability reflects their natural human tissue architecture whose collagen matrix, mechanical properties, and cellular signaling residues create superior host tissue integration relative to cross-species xenograft alternatives. Allografts’ lower immunogenicity compared to xenografts reduces the inflammatory response that contributes to early structural valve deterioration, creating longer expected durability that sustains clinical preference particularly in younger bioprosthetic valve recipients whose remaining life expectancy creates above-average implant longevity requirements.

Xenografts are the fastest-growing product segment at approximately 12.5% CAGR because porcine and bovine tissue processing technology advances are progressively improving xenograft’s clinical performance profile. Advanced decellularization techniques that remove xenoantigenic material while preserving the extracellular matrix scaffold, anti-calcification treatments including the RESILIA platform and ThermaFix processing, and polymer-reinforced xenograft designs are collectively improving durability, reducing calcification rates, and extending xenograft functionality into patient populations where conventional glutaraldehyde-fixed xenograft tissue durability was previously clinically inadequate. The commercial availability of porcine and bovine tissue at scale provides xenograft manufacturing economics that allograft’s human donor dependency cannot match.

By Application, cardiovascular dominates, orthopedic grows fastest

Cardiovascular retained the dominant application position with approximately 81% of the bioprosthetics market in 2025. The extraordinary clinical scale of the cardiovascular bioprosthetics market reflects the extraordinary prevalence of valvular heart disease whose definitive treatment through surgical or transcatheter bioprosthetic valve replacement creates the largest single bioprosthetic implant procedure volume globally. Aortic stenosis affects approximately 2-5% of adults over 65, whose global elderly population growth creates a structurally expanding bioprosthetic valve procedure volume that compounds with the progressive expansion of TAVI from high-risk toward lower-risk patient populations. Vascular graft applications in peripheral arterial disease bypass and haemodialysis access creation further sustain cardiovascular’s commercial dominance.

Orthopaedic is the fastest-growing application at approximately 14.2% CAGR because biological tissue augmentation for rotator cuff tendon repair, Achilles tendon reconstruction, anterior cruciate ligament revision, and articular cartilage restoration is progressively replacing or supplementing synthetic mesh and autologous tissue approaches whose complication rates and donor site morbidity create clinical motivation for biologic alternative development. The LifeCell AlloDerm and Strattice acellular tissue matrix platforms represent the commercial precedent for dermal allograft orthopaedic augmentation whose clinical adoption is generating growing procedure volume across sports medicine and reconstructive orthopaedic surgery.

By End User, hospitals dominate, ambulatory centres grow fastest

Hospitals retained the dominant end user position with approximately 72% of the bioprosthetics market in 2025. Bioprosthetic implantation in cardiac surgery, vascular surgery, and complex orthopaedic reconstruction requires the anaesthesia, perfusion, post-operative monitoring, and surgical team expertise that only hospital-level facilities can provide. Open heart surgery for surgical aortic valve replacement and TAVI cardiac catheterisation laboratory infrastructure is each hospital-capital-intensive procedure environments whose procedural complexity and post-operative care requirements preclude outpatient migration for the majority of bioprosthetic cardiac implantation procedures.

Ambulatory surgical centres are the fastest-growing end user at approximately 13.8% CAGR because procedure migration for certain bioprosthetic implantation categories is progressively qualifying lower-complexity procedures for outpatient delivery. TAVI’s patient selection evolution toward lower surgical risk has progressively identified a subset of TAVI patients whose same-day discharge is clinically safe, creating CMS reimbursement pathway development that is progressively enabling TAVI at hybrid ASC-hospital facilities. Orthopaedic biologic tissue augmentation for soft tissue repair represents the most commercially significant ASC bioprosthetic application where existing outpatient arthroscopy infrastructure accommodates rotator cuff and ligament biologic augmentation procedures.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Bioprosthetics Market Insights

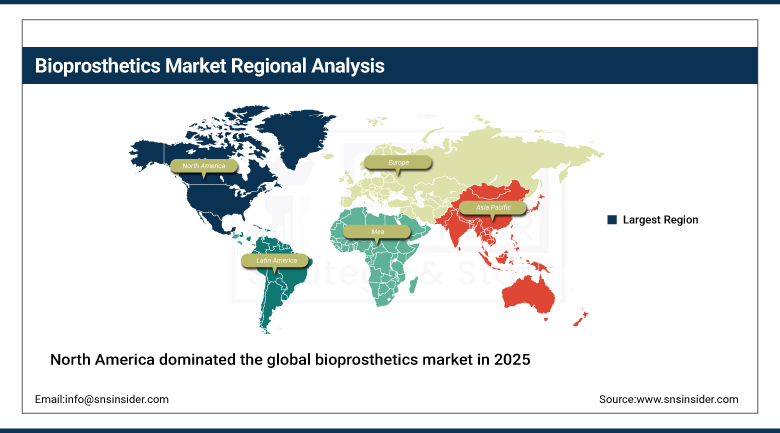

North America dominated the global bioprosthetics market in 2025, accounting for approximately 42% of global revenues. The United States accounts for approximately 87.4% of North American revenues through its combination of the world’s leading bioprosthetic technology developers, the most advanced TAVI clinical programme, and the most comprehensive Medicare reimbursement infrastructure for bioprosthetic cardiac procedures. Edwards Lifesciences, Medtronic, Abbott, LeMaitre Vascular, LifeCell, and Humacyte collectively represent the most commercially significant bioprosthetics company concentration of any national market.

Canada contributes approximately 12.6% of North American revenues through its publicly funded cardiovascular surgery and orthopaedic programmes, academic medical Centre tissue engineering research investment, and progressive reimbursement for TAVI in approved patient populations that sustains consistent bioprosthetic valve procurement.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Bioprosthetics Market Insights

Europe is a technically sophisticated bioprosthetics market where CE marking regulatory pathways, European Society of Cardiology treatment guidelines for bioprosthetic valve selection, and the commercial presence of Sorin Group (LivaNova), AutoTissue, and European academic tissue banks create a complete bioprosthetics ecosystem. Germany accounts for approximately 22.3% of European revenues through its advanced cardiac surgery infrastructure, above-average bioprosthetic valve implantation rates, and the regulatory rigour of the German Medical Devices Act that sustains premium product specification.

The United Kingdom, France, and the Netherlands are significant secondary European markets where NHS and equivalent national health system cardiac surgery programmes, orthopaedic biological tissue bank networks, and growing TAVI clinical adoption create consistent bioprosthetic procurement. European tissue banking regulation under EU Tissues and Cells Directive creates the quality infrastructure that sustains allograft supply to clinical programmes across member states.

Asia Pacific Bioprosthetics Market Insights

Asia Pacific is the fastest-growing regional bioprosthetics market, driven by rapidly expanding cardiovascular disease burden, growing cardiac surgery infrastructure investment, and above-average population ageing rates across China, Japan, South Korea, India, and Australia. China accounts for approximately 44.8% of Asia Pacific revenues through its expanding cardiac surgery capacity, government healthcare infrastructure investment, and the growing adoption of bioprosthetic heart valve alternatives to mechanical valves whose anticoagulation requirements create lifestyle and compliance challenges for Chinese patient populations.

India represents the most commercially dynamic emerging market within Asia Pacific, where the combination of high rheumatic heart disease prevalence, rapidly expanding private hospital cardiac surgery capacity, and Ayushman Bharat health insurance scheme’s progressive coverage expansion are creating growing bioprosthetic valve and vascular graft procurement across a patient population whose disease burden substantially exceeds current treatment capacity.

MEA & Latin America Bioprosthetics Market Insights

The Middle East and Africa and Latin America are growing bioprosthetics markets where cardiovascular disease burden, healthcare infrastructure investment, and supportive reimbursement scheme development are creating structured demand. Saudi Arabia leads MEA revenues at approximately 31.2% through Vision 2030’s healthcare investment, the Ministry of Health’s cardiac surgery programme, and above-average private healthcare sector technology adoption whose premium clinical standards create receptivity to advanced bioprosthetic implant specifications.

Brazil leads Latin American revenues at approximately 44.2% through its large cardiovascular surgery infrastructure, ANVISA regulatory framework that enables bioprosthetic device approval, and the SUS public health system’s cardiac surgery programme that provides bioprosthetic valve access across Brazil’s geographically extensive hospital network. Braile Biomedica’s domestic bioprosthetic heart valve manufacturing creates a local supply alternative to international products that sustains Brazilian market development independent of import pricing dynamics.

Market Dynamics:

Growth Drivers: Cardiovascular disease prevalence and TAVI expanding bioprosthetic valve patient population

Rising cardiovascular disease and valvular heart disease prevalence is the bioprosthetics market’s most structurally reliable growth driver. Aortic stenosis prevalence of 2-5% in adults over 65, combined with global elderly population growth, creates a continuously expanding bioprosthetic valve procedure volume whose demographic trajectory is commercially certain. Each year of global population ageing creates incremental valvular disease prevalence that sustains bioprosthetic implantation procedure growth independent of technology cycle variation.

TAVI programme expansion from high-risk toward intermediate and low surgical risk patient populations is creating above-average bioprosthetic valve procurement growth because each successive risk stratification approval substantially expands the eligible patient population. The original TAVI indication for inoperable patients created a defined initial market. Intermediate-risk approval doubled the addressable population. Low-risk approval further expanded it. Clinical guideline evolution is progressively considering TAVI as first-line therapy for any patient needing aortic valve replacement regardless of surgical risk, creating a commercial adoption trajectory whose endpoint is TAVI as the universal standard of care for aortic stenosis.

Restraints: Structural valve deterioration limiting durability in younger patients and allograft supply chain constraints

Structural valve deterioration remains the most clinically significant limitation of bioprosthetic heart valves. Conventional glutaraldehyde-preserved bioprosthetic valves demonstrate 10-15-year durability in older patients but accelerated calcification and leaflet failure in recipients under 60 whose higher metabolic activity creates above-average tissue stress. This durability limitation historically restricted bioprosthetic valve recommendation to elderly patients for whom remaining life expectancy would not exceed implant longevity. Anti-calcification technology development is progressively addressing this constraint but clinical outcome data for newer preservation technologies requires the decade-scale follow-up that is still accumulating for most novel platforms.

Allograft supply chain constraints create commercial limitations on the 68%-dominant product segment whose human tissue donor dependency creates geographic procurement variability and regulatory complexity that manufacturing scale cannot eliminate through conventional capacity investment. Human tissue banking requires donor screening, processing quality assurance, and regulatory compliance infrastructure whose cost and regulatory burden creates supply constraints that xenograft’s manufacturing scalability does not face.

Opportunities: Bioengineered tissue products and transcatheter orthopaedic biologic applications

Bioengineered tissue products represent the most commercially transformative bioprosthetics opportunity because they overcome the fundamental limitations of both allograft and xenograft supply chains by creating manufactured biological tissue that is not dependent on donor availability or cross-species immunogenicity management. Humacyte’s Human Acellular Vessel, LifeNet Health’s processed allograft portfolio, and academic tissue engineering programmes collectively represent the innovation pipeline whose successful commercialisation will create new premium bioprosthetic categories whose manufactured nature enables the supply chain predictability that donor-dependent bioprosthetics cannot achieve.

Transcatheter orthopaedic biologic tissue delivery represents an emerging application category whose catheter-delivered biologic matrices for joint cartilage, tendon insertion, and intervertebral disc restoration create bioprosthetic orthopaedic applications that do not require open surgical access. Each new FDA clearance for catheter-delivered orthopaedic biologic creates a minimally invasive alternative to open surgical repair whose patient preference and lower complication rate creates commercial adoption momentum across the large orthopaedic repair market.

Recent Developments:

-

2025: Edwards Lifesciences received FDA approval for RESILIA tissue technology applied to the INSPIRIS RESILIA aortic valve, demonstrating superior anti-calcification performance relative to conventional glutaraldehyde-preserved tissue valves and reflecting the commercial direction toward extended-durability bioprosthetic heart valve platforms.

-

2025: Humacyte received FDA Breakthrough Device Designation for its Human Acellular Vessel bioengineered vascular graft, advancing the first commercially developed bioengineered human tissue vascular conduit toward regulatory approval for arteriovenous access and below-knee vascular reconstruction indications.

-

2024: Medtronic received CE mark for its Evolut TAVI system in additional low-risk patient population indications in 2024, expanding the reimbursable bioprosthetic valve patient population across European markets and creating structured growth in TAVI bioprosthetic valve procurement whose addressable volume scales with approved surgical risk category expansion.

Bioprosthetics Market Key Players:

-

Edwards Lifesciences Corporation

-

Medtronic

-

Abbott (St. Jude Medical)

-

LivaNova (Sorin Group)

-

LeMaitre Vascular

-

Carmat

-

Maquet Getinge Group

-

LifeCell Corporation

-

Humacyte

-

CryoLife

-

AutoTissue GmbH

-

Braile Biomedica

-

Aortech International

-

Neovasc

-

Labcor Laboratorios

Bioprosthetics Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 7.09 Billion |

| Market Size by 2035 | USD 19.76 Billion |

| CAGR | CAGR of 10.7% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Allograft, Xenograft, Synthetic Bioprosthetics) • By Application (Cardiovascular, Orthopaedic, Dental, Ophthalmologic, Others) • By End User (Hospitals, Specialty Centers, Ambulatory Surgical Centers, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Edwards Lifesciences Corporation, Medtronic, Abbott (St. Jude Medical), LivaNova (Sorin Group), LeMaitre Vascular, Carmat, Maquet Getinge Group, LifeCell Corporation, Humacyte, CryoLife, AutoTissue GmbH, Braile Biomedica, Aortech International, Neovasc, and Labcor Laboratorios |

Frequently Asked Questions

The Bioprosthetics Market is expected to grow at a CAGR of 10.7% from 2026 to 2035.

The Bioprosthetics Market was valued at USD 7.09 Billion in 2025.

Rising cardiovascular disease and valvular heart disease prevalence creating growing bioprosthetic implantation demand, and TAVI programme expansion from high-risk toward low-risk patient populations progressively multiplying the reimbursable bioprosthetic heart valve addressable patient population.

Allograft dominated the Bioprosthetics Market with 68% share in 2025, while Xenograft is the fastest growing with a CAGR of approximately 12.5%.

North America dominated the Bioprosthetics Market in 2025 with approximately 42% of global revenues.

Get in Touch