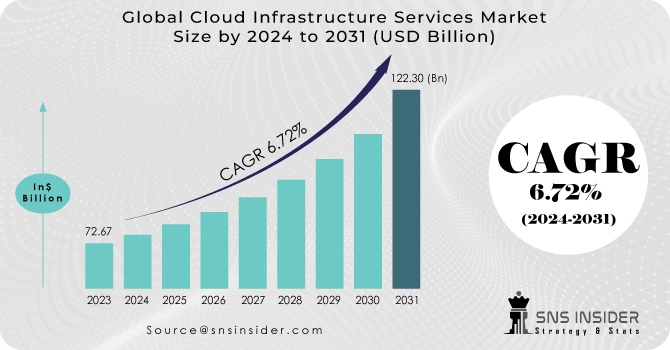

Cloud Infrastructure Services Market size was valued at USD 72.67 Bn in 2023 and is expected to reach USD 122.30 Bn by 2031, and grow at a CAGR of 6.72 % over the forecast period 2024-2031.

The Major drivers for the cloud infrastructure services market include cost-effectiveness, scalability, flexibility, and security, leading to accelerated Time-to-Market (TTM) and rapid application development. The growing need to reduce operational costs and IT infrastructure maintenance also drives organizations to adopt cloud services. the increase in global data volumes and the adoption of cloud technologies for improved security of data, integrity, and service delivery drives the market growth.

Get More Information on Cloud Infrastructure Services Market - Request Sample Report

The virtualization of infrastructure across a network or the internet is known as cloud infrastructure. Software as a service, platform as a service, infrastructure as a service, cloud business process as a service, content delivery network /application delivery network, and colocation hosting are examples of delivery methods used by cloud infrastructure. The Cloud Infrastructure Service Market benefits from urbanization and digitalization, the mainstreaming of edge computing, and increased investment.

Market Dynamics

Drivers:

Cloud infrastructure services offer cost savings through pay-as-you-go models, eliminating the need for upfront hardware investments.

Cloud services allow businesses to scale their infrastructure up or down based on demand, offering flexibility and agility.

Cloud infrastructure enables businesses to reach global markets without the need for physical infrastructure in every location.

Cloud providers often offer advanced technologies such as AI, machine learning, and big data analytics, enhancing overall system performance.

Cloud services provide robust disaster recovery solutions, ensuring business continuity in case of unexpected events.

Cloud infrastructure services function on a pay-as-you-go basis, meaning businesses are charged solely for the resources utilized, eliminating the necessity of upfront hardware investments. This method drastically cuts down initial capital costs and grants companies the ability to adjust resource allocation as required. The absence of physical hardware purchases and maintenance further drives cost savings and enhances resource allocation efficiency. Moreover, the pay-as-you-go model offers increased flexibility and adaptability to evolving business needs, avoiding rigid infrastructure commitments. In essence, it fosters a more economical and efficient approach to IT infrastructure management.

Restraints:

Data breaches and cyber threats remain a major concern for businesses considering cloud adoption.

Organizations may become overly dependent on cloud providers, leading to potential vendor lock-in and limited control over infrastructure.

Meeting regulatory and compliance requirements, especially in highly regulated industries, can be challenging in a cloud environment.

Dependence on internet connectivity and shared resources in a cloud environment can lead to performance variability issues.

Opportunities:

The adoption of hybrid cloud solutions presents opportunities for businesses to leverage the benefits of both public and private cloud infrastructures.

Cloud providers can develop industry-specific solutions tailored to the needs of sectors such as healthcare, finance, and retail.

The growth of IoT devices and edge computing creates opportunities for cloud providers to offer edge-based infrastructure services.

Integrating AI and automation into cloud infrastructure services can improve efficiency, security, and cost-effectiveness.

Challenges:

There is a shortage of skilled professionals with expertise in cloud technologies, leading to challenges in implementation and management.

Migrating legacy systems and applications to the cloud can be complex, requiring careful planning and execution.

Avoiding vendor lock-in and maintaining flexibility to switch between cloud providers without significant disruptions is a challenge for businesses.

Impact of Russia-Ukraine War:

The Russia-Ukraine war has led to increased concerns about cybersecurity and data sovereignty, prompting businesses to reassess their reliance on cloud infrastructure services. Supply chain disruptions, particularly in semiconductor manufacturing, may affect the availability and pricing of cloud hardware. Geopolitical tensions could also impact data center locations and data transfer regulations, potentially causing disruptions in service delivery and compliance requirements. Overall, the uncertainty and instability resulting from the conflict may lead to cautious investment decisions and strategic reevaluations within the cloud infrastructure services market.

Impact of Economic Downturn:

During an economic downturn, businesses often prioritize cost-cutting measures, leading to increased adoption of cloud infrastructure services due to their cost-effective nature. Companies seek to reduce capital expenditures by leveraging pay-as-you-go models and outsourcing IT infrastructure management to cloud providers. The downturn also drives demand for scalable solutions as businesses aim to efficiently manage fluctuating workloads without heavy upfront investments. However, the downturn may also result in delayed or reduced IT spending overall, impacting the pace of cloud adoption and expansion in some sectors. Overall, the cloud infrastructure services market experiences mixed effects during economic downturns, balancing increased demand for cost savings with potential constraints on overall IT budgets.

Market segmentation

By Service

Compute Service

Storage Service

Disaster Recovery and Backup Service

Networking Service

Desktop Service

Managed Hosting

On the basis of services market is divided into computing, storage, disaster recovery, networking, desktop, and managed hosting services. Organizations of all sizes and industries are adopting these services to boost efficiency, reduce server space costs, and ensure data accessibility. The disaster recovery and backup services are projected to have the highest growth rate during forecast period while, the storage services held the largest market share more than 28%. Cloud infrastructure services have become integral to business operations due to their user-friendly nature, cost-effectiveness, and adaptability.

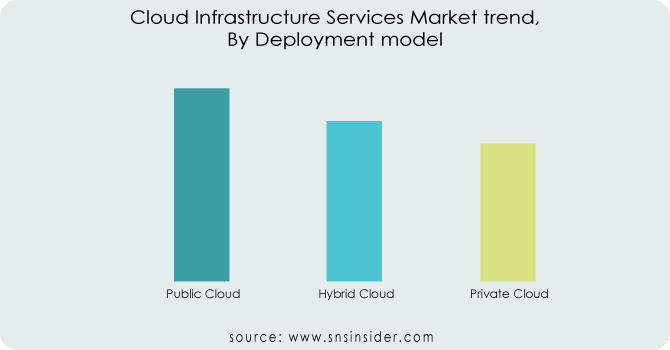

By Deployment model

Public Cloud

Private Cloud

Hybrid Cloud

On the basis of Deployment model the public cloud segment is dominates the market with holding revenue share of more than 39% projected to maintain the largest market share. Among deployment models, the public cloud is noted for its simplicity, easy deployment, and minimal initial investment. Users benefit from scalability, reliability, flexibility, utility-style costing, and location-independent services, without the burden of infrastructure management responsibilities.

Get Customized Report as per Your Business Requirement - Request For Customized Report

By Organization size

Small and Medium-sized Enterprises (SMEs)

Large Enterprises

By Vertical

Banking, Financial Services, and Insurance (BFSI)

IT and Telecommunications

Government and Public Sector

Retail and Consumer Goods

Manufacturing

Energy and Utilities

Media and Entertainment

Healthcare and Life Sciences

Others

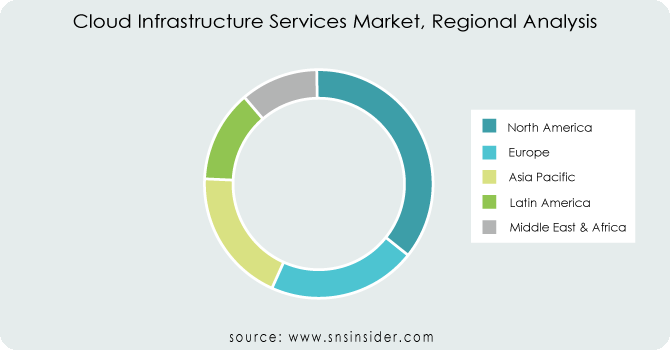

Regional Analysis

North America dominates the global cloud infrastructure services market, with holding Revenue share of more than 38%, driven by increasing widespread adoption of cloud-based IT services and substantial investments in IT infrastructure research and development. The U.S. dominates this industry, benefiting from key vendors' presence and a growing adoption rate of cloud services to cut data center costs and increase business continuity. Major players such as Google, Amazon, and Microsoft further Helps to drive market growth. The Asia Pacific (APAC) region is growing with a significant growth Rate with the highest expected compound annual growth rate (CAGR). The region's focus on rapid, cost-effective service delivery and security in cloud operations is Drive the global cloud infrastructure services market forward.

REGIONAL COVERAGE:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Key Players

The major key players are AWS, Microsoft, Google, IBM, Alibaba, Rackspace, Oracle, Fujitsu, Digitalocean, Vmware & Other Players and other key players mentioned in the final report.

| Report Attributes | Details |

| Market Size in 2022 | US$ 72.67 Bn |

| Market Size by 2030 | US$ 122.30 Bn |

| CAGR | CAGR of 6.72 % From 2023 to 2030 |

| Base Year | 2022 |

| Forecast Period | 2023-2030 |

| Historical Data | 2020-2021 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Service (Compute Service, Storage Service, Disaster Recovery and Backup Service, Networking Service, Desktop Service, Managed Hosting) • by Deployment Model (Public Cloud, Private Cloud, Hybrid Cloud) • by Organization Size (Small and Medium-sized Enterprises (SMEs) and Large Enterprises) • by Industry Vertical (Banking, Financial Services, and Insurance (BFSI), IT and Telecommunications, Government and Public Sector, Retail and Consumer Goods, Manufacturing, Energy and Utilities, Media and Entertainment, Healthcare and Life Sciences, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | AWS, Microsoft, Google, IBM, Alibaba, Rackspace, Oracle, Fujitsu, Digitalocean, and Vmware. |

| Key Drivers | • Cloud infrastructure services offer cost savings through pay-as-you-go models, eliminating the need for upfront hardware investments. • Cloud services allow businesses to scale their infrastructure up or down based on demand, offering flexibility and agility. |

| Market Challenges | • There is a shortage of skilled professionals with expertise in cloud technologies, leading to challenges in implementation and management. • Migrating legacy systems and applications to the cloud can be complex, requiring careful planning and execution. |

Ans. The Compound Annual Growth rate for the Cloud Infrastructure Services Market over the forecast period is 7.62 %.

Ans. The projected market size for the Cloud Infrastructure Services Market is USD 122.30 Bn by 2031.

Ans: The Public cloud Deployment segments dominated the Cloud Infrastructure Services Market with the highest revenue share.

Ans: Yes, you can ask for the customization as per your business requirement.

Ans:

TABLE OF CONTENTS

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Industry Flowchart

3. Research Methodology

4. Market Dynamics

4.1 Drivers

4.2 Restraints

4.3 Opportunities

4.4 Challenges

5. Impact Analysis

5.1 Impact of Russia-Ukraine Crisis

5.2 Impact of Economic Slowdown on Major Countries

5.2.1 Introduction

5.2.2 United States

5.2.3 Canada

5.2.4 Germany

5.2.5 France

5.2.6 UK

5.2.7 China

5.2.8 Japan

5.2.9 South Korea

5.2.9 India

6. Value Chain Analysis

7. Porter’s 5 Forces Model

8. Pest Analysis

9. Cloud Infrastructure Services Market, By Service

9.1 Introduction

9.2 Trend Analysis

9.3 Compute Service

9.4 Storage Service

9.5 Disaster Recovery and Backup Service

9.6 Networking Service

9.7 Desktop Service

9.8 Managed Hosting

10. Cloud Infrastructure Services Market, By Deployment model

10.1 Introduction

10.2 Trend Analysis

10.3 Public Cloud

10.4 Private Cloud

10.5 Hybrid Cloud

11. Cloud Infrastructure Services Market, By Organization size

11.1 Introduction

11.2 Trend Analysis

11.3 Small and Medium-sized Enterprises (SMEs)

11.4 Large Enterprises

12. Cloud Infrastructure Services Market, By Vertical

12.1 Introduction

12.2 Trend Analysis

12.3 Banking, Financial Services, and Insurance (BFSI)

12,4 IT and Telecommunications

12.5 Government and Public Sector

12.6 Retail and Consumer Goods

12.7 Manufacturing

12.8 Energy and Utilities

12.9 Media and Entertainment

12.10 Healthcare and Life Sciences

12.11 Others

13. Regional Analysis

13.1 Introduction

14.2 North America

14.2.1 USA

14.2.2 Canada

14.2.3 Mexico

14.3 Europe

14.3.1 Eastern Europe

14.3.1.1 Poland

14.3.1.2 Romania

14.3.1.3 Hungary

14.3.1.4 Turkey

14.3.1.5 Rest of Eastern Europe

14.3.2 Western Europe

14.3.2.1 Germany

14.3.2.2 France

14.3.2.3 UK

14.3.2.4 Italy

14.3.2.5 Spain

14.3.2.6 Netherlands

14.3.2.7 Switzerland

14.3.2.8 Austria

14.3.2.9 Rest of Western Europe

14.4 Asia-Pacific

14.4.1 China

14.4.2 India

14.4.3 Japan

14.4.4 South Korea

14.4.5 Vietnam

14.4.6 Singapore

14.4.7 Australia

14.4.8 Rest of Asia Pacific

14.5 The Middle East & Africa

14.5.1 Middle East

14.5.1.1 UAE

14.5.1.2 Egypt

14.5.1.3 Saudi Arabia

14.5.1.4 Qatar

14.5.1.5 Rest of the Middle East

14.5.2 Africa

14.5.2.1 Nigeria

14.5.2.2 South Africa

14.5.2.3 Rest of Africa

14.6 Latin America

14.6.1 Brazil

14.6.2 Argentina

14.6.3 Colombia

14.6.4 Rest of Latin America

15. Company Profiles

15.1 AWS

15.1.1 Company Overview

15.1.2 Financials

15.1.3 Products/ Services Offered

15.1.4 SWOT Analysis

15.1.5 The SNS View

15.2 Microsoft

15.2.1 Company Overview

15.2.2 Financials

15.2.3 Products/ Services Offered

15.2.4 SWOT Analysis

15.2.5 The SNS View

15.3 Google

15.3.1 Company Overview

15.3.2 Financials

15.3.3 Products/ Services Offered

15.3.4 SWOT Analysis

15.3.5 The SNS View

15.4 IBM

15.4 Company Overview

15.4.2 Financials

15.4.3 Products/ Services Offered

15.4.4 SWOT Analysis

15.4.5 The SNS View

15.5 Alibaba

15.5.1 Company Overview

15.5.2 Financials

15.5.3 Products/ Services Offered

15.5.4 SWOT Analysis

15.5.5 The SNS View

15.6 Rackspace

15.6.1 Company Overview

15.6.2 Financials

15.6.3 Products/ Services Offered

15.6.4 SWOT Analysis

15.6.5 The SNS View

15.7 Oracle

15.7.1 Company Overview

15.7.2 Financials

15.7.3 Products/ Services Offered

15.7.4 SWOT Analysis

15.7.5 The SNS View

15.8 Fujitsu

15.8.1 Company Overview

15.8.2 Financials

15.8.3 Products/ Services Offered

15.8.4 SWOT Analysis

15.8.5 The SNS View

15.9 Digitalocean

15.9.1 Company Overview

15.9.2 Financials

15.9.3 Products/ Services Offered

15.9.4 SWOT Analysis

15.9.5 The SNS View

15.10 Vmware

15.10.1 Company Overview

15.10.2 Financials

15.10.3 Products/ Services Offered

15.10.4 SWOT Analysis

15.10.5 The SNS View

16. Competitive Landscape

16.1 Competitive Benchmarking

16.2 Market Share Analysis

16.3 Recent Developments

16.3.1 Industry News

16.3.2 Company News

16.3.3 Mergers & Acquisitions

17. USE Cases and Best Practices

18. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

The 5G Fixed Wireless Access (FWA) Market size was valued at USD 24.66 Bn in 2022 and is expected to reach USD 337.75 Bn by 2030, and grow at a CAGR of 38.7% over the forecast period 2023-2030.

The Serverless Security Market size was valued at USD 1.79 Bn in 2022 and is expected to reach USD 15.69 Bn by 2030, and grow at a CAGR of 31.12 % over the forecast period 2023-2030.

The Passive Authentication Market size was valued at USD 2.29 Bn in 2022 and is expected to reach USD 11.37 Bn by 2030, and grow at a CAGR of 22.14 % over the forecast period 2023-2030.

The Smart Space Market size was USD 39.2 billion in 2022 and is expected to Reach USD 108.7 billion by 2030 and grow at a CAGR of 13.6 % over the forecast period of 2023-2030.

The Trade Management Software Market size was valued at USD 1.25 billion in 2022 and is expected to grow to USD 2.70 billion by 2030 and grow at a CAGR of 10.12 % over the forecast period of 2023-2030.

The AI Orchestration Market size was USD 6.9 billion in 2022 and is expected to Reach USD 35.22 billion by 2030 and grow at a CAGR of 22.5 % over the forecast period of 2023-2030.

Hi! Click one of our member below to chat on Phone

© 2024 All Rights Reserved by SNS Insider Pvt Ltd