Cosmetic Packaging Market Key Insights:

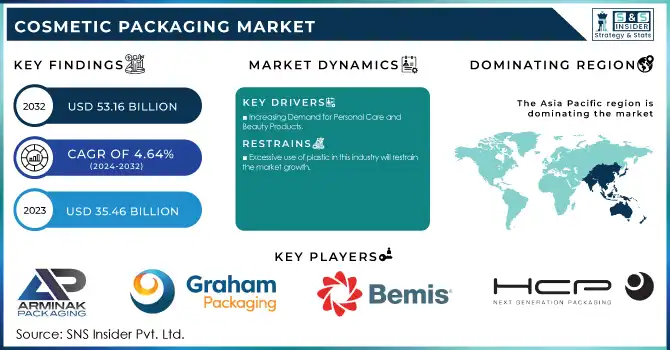

The Cosmetic Packaging Market was valued at USD 35.46 billion in 2023 and is projected to reach USD 53.16 billion by 2032, growing at a CAGR of 4.64% during the forecast period.

Get More Information on Cosmetic Packaging Market - Request Sample Report

The market is projected to grow over the forecast period due to an increase in demand for cosmetic products owing to changes in packaging types, innovative designs of containers, and a growing youth population.

Moreover, the market is expected to show strong growth over the forecast period due to increased demand for cosmetics on account of changing attitudes towards care between men and women. For the marketing of cosmetic products, producers are using large-scale advertising in a variety of media. The innovation of packaging will play a key role in attracting consumers over the coming years and is likely to have an impact on the growth of the entire packaging sector.

Moreover, the growth opportunities of the cosmetics sector have been greatly expanded in developing countries like China and Japan as a result of increasing consumer spending and changing lifestyles. Consequently, as the demand for cosmetic products rises globally over the forecast period, it will have a direct impact on this sector's market and increase its global growth. Product and packaging innovation is being driven by a growing number of new entrants to the cosmetics sector, who are seeking competitive advantage. The cosmetic packaging market is projected to experience growth in the coming years, driven by these factors.

Demand for cosmetic products has also been influenced by the increasing penetration of eCommerce and online shopping in both rural and city areas. For example, there are 97% of total US sales made on the internet by Glossier Inc. Businesses are also switching their sales to online platforms as a result of an increase in internet usage. Therefore, the growth of the packaging industry has been affected by a general increase in demand for beauty products.

In addition, companies are beginning to target a specific segment of consumers called the Middle Class. This has resulted in the packaging industry's demand being affected so companies are adopting products with less packaging capacity. By adopting new packaging techniques, the introduction of environmental and Green Packaging is having a strong impact on the development of the entire industry. In addition, the growth of this sector is aided by new innovations in its product lines.

However, the most commonly used packaging material in this industry is plastic, most of which ends up in landfills. According to the Environmental Protection Agency, nearly 70% of plastic waste from the cosmetics industry is not recycled and ends up in landfills. Additionally, the majority of the packaging is made of single-use plastic paper, a significant portion of which is multi-layered to give it a more premium look, contributing to the excessive use of plastic. Excessive use of plastics is expected to hamper the market growth due to increased public awareness and government initiatives.

MARKET DYNAMICS

KEY DRIVERS:

-

Increasing Demand for Personal Care and Beauty Products

The expansion of the beauty and personal care industry is a major factor driving the cosmetic packaging market. There has also been a growing demand for innovative packaging solutions to differentiate products and provide consumers with choices, in view of the continued growth of market demand for cosmetics worldwide.

-

The rise of the online market has had a positive impact on cosmetic packaging markets

RESTRAIN:

-

Excessive use of plastic in this industry will restrain the market growth.

OPPORTUNITY:

-

Emerging markets like the Asia Pacific, Latin America, and the Middle East are showing a marked increase in demand for cosmetics.

Such areas offer cosmetic packaging producers an opportunity for expansion and to tap into a new consumer base. Success can be achieved through adapting packaging designs, materials and marketing strategies in response to the preferences and cultural characteristics of these markets.

-

The introduction of customized packaging options that enable product differentiation by consumers is a way for cosmetics manufacturers to capitalize on this trend.

CHALLENGES:

-

Reducing waste from packaging and increasing recycling packaging rates are key challenges.

IMPACT OF RUSSIA-UKRAINE WAR

The effects of the Ukraine war are on the global cosmetics industry, with producers using a variety of things such as alcohol made from grain and beets to make perfumes and sunflower oil for cosmetic purposes. At the same time, the price of glass and paper has risen as a result of the energy crisis caused by the war, and the new containment in China has made it impossible for companies to obtain packaging for their luxury cosmetic products.

As Russia's invasion of Ukraine adds further disruption to the supply chain for beauty products, which leads to higher prices due to robust demand, European perfume and cosmetic manufacturers face a shortage of paper, glass, or some key oils and alcohol.

The $ 550 billion global cosmetics sector is grappling with the fallout from the war because producers use alcohol derived from grains and organic beets to make perfumes, and sunflower-seed oils to be used in cosmetics from all the main crops of Ukraine. In Russia, several top beauty brands and retail outlets have suspended their operations due to the ongoing conflict in Ukraine according to an expert who says that these actions are aligned with a widespread consumer sentiment and growing difficulties for doing business there.

The invasion by Russia hit the Ukrainian cosmetics sector hard, forcing many manufacturers to temporarily stop production and close their shops. The market for Personal Care Products in this country is expected to generate sales of US$ 2.9 billion by 2022. However, Russia’s invasion has halted activity in this fast-growing domestic industry. According to United Nations estimates, Ukraine's GDP would fall by 10%, forcing many national producers out of business.

IMPACT OF ONGOING RECESSION

In the beauty industry, lipstick effectiveness, also known as the lipstick index, is regarded as the leading economic indicator in the field. The concept is that during times of recession or other financial stress, women make self-initiated purchases that lift their emotions without going over their budget. The lipstick is just right.

The effect of lipstick may not have had a major impact on the traditional business world, but new data from global market tracking firm NPD Group shows that sales of lipsticks and other lip makeup in the first quarter were down year-on-year. It increased by 50 % and is growing more than twice as fast as before.

In 2022, roughly $430 billion worth of revenues were generated by the beauty market, which covers skincare, fragrance, makeup and hair care. In 2022, the United States' prestige beauty products sales increased by 16 %. Even after recession it is expected that beauty products and cosmetics market will grow by 2.5% in US.

KEY MARKET SEGMENTATION

By Material

-

Plastic

-

Paper

-

Glass

-

Metal

-

Others

The market for cosmetic packaging is segmented according to material types, namely plastic, paper, metal and glass. The largest market share was held by the plastic segment, which is expected to grow significantly in the near future. The manufacturers have a strong preference for Rigid Plastic Packaging, because of its wide use and low costs. Companies prefer plastic for packaging purposes so that they can package the product in smaller units, which is contributing to segment growth.

By Product Type

-

Tubes

-

Bottles

-

Jars & Containers

-

Tins & Cans

-

Blister & Strip Packs

-

Others

By Application

-

Skin Care

-

Hair Care

-

Nail Care

-

Makeup

-

Perfumes

-

Others

The makeup segment is expected to show the highest growth amongst other segments, with a 5.7% compound annual growth rate during the forecast period. The growth of the market has been affected to a large extent by an increasing number of working women in recent years and one of the major factors underpinning this segment's growth.

REGIONAL ANALYSIS

The Asia Pacific region leads with a share of 45.0%, and is expected to grow significantly over the next few years. The majority of this share is held by Japan, which is expected to grow at the rate of 5.5% per annum over the forecast period for Asia Pacific. The market in this region is being driven by the introduction of new product varieties, as well as increasing consumer acceptance due to growing awareness about various benefits such as sun protection.

During the forecast period, Middle East & Africa is projected to register a 5.3% compound annual growth rate. Muslim-majority countries such as Saudi Arabia and the UAE are expected to see increased demand for cosmetics in the near future. Rising demand for halal cosmetics is boosting the market in the region. Therefore, increased demand from the cosmetics industry leads to increased demand from the packaging industry.

Get Customized Report as per your Business Requirement - Request For Customized Report

REGIONAL COVERAGE:

North America

-

US

-

Canada

-

Mexico

Europe

-

Eastern Europe

-

Poland

-

Romania

-

Hungary

-

Turkey

-

Rest of Eastern Europe

-

-

Western Europe

-

Germany

-

France

-

UK

-

Italy

-

Spain

-

Netherlands

-

Switzerland

-

Austria

-

Rest of Western Europe

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Vietnam

-

Singapore

-

Australia

-

Rest of Asia Pacific

Middle East & Africa

-

Middle East

-

UAE

-

Egypt

-

Saudi Arabia

-

Qatar

-

Rest of Middle East

-

-

Africa

-

Nigeria

-

South Africa

-

Rest of Africa

-

Latin America

-

Brazil

-

Argentina

-

Colombia

-

Rest of Latin America

Key Players

Some major key players in the Cosmetic Packaging market are AREMIX Packaging, Graham Packaging Company, Bemis Company Inc, HCP Packaging, Silgan Holdings, Albea, Libo Cosmetics, RPC Group Plc, AptarGroup Inc, DS Smith and other players.

RECENT DEVELOPMENTS

-

Baralan is showing off innovative glass packaging techniques at Luxe Pack New York. In addition to its newest jars, bottles and accessories, the company specializing in primary packaging of cosmetics and beauty products introduced a selection of solutions that focus on airless glass containers.

-

Geka, The all new, patented shadow printing service has just begun to be offered by the Geka Beauty brand of medmix.

-

An Italian company, Minelli, specializing in the manufacture of custom and standard wooden parts, has launched its new low carbon premium packaging product “mPackting” that is targeted at the beauty industry.

| Report Attributes | Details |

| Market Size in 2023 | US$ 37.95 Bn |

| Market Size by 2031 | US$ 55.35 Bn |

| CAGR | CAGR of 4.8% From 2024 to 2031 |

| Base Year | 2023 |

| Forecast Period | 2024-2031 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Material (Plastic, Paper, Glass, Metal, Others) • By Product Type (Tubes, Bottles, Jars & Containers, Tins & Cans, Blister & Strip Packs, Others) • By Application (Skin Care, Hair Care, Nail Care, Makeup, Perfumes, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]). Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia Rest of Latin America) |

| Company Profiles | AREMIX Packaging, Graham Packaging Company, Bemis Company Inc, HCP Packaging, Silgan Holdings, Albea, Libo Cosmetics, RPC Group Plc, AptarGroup Inc, DS Smith |

| Key Drivers | • Increasing Demand for Personal Care and Beauty Products • The rise of the online market has had a positive impact on cosmetic packaging markets |

| Market Restraints | • Excessive use of plastic in this industry will restrain the market growth. |

Frequently Asked Questions

Ans: The Asia Pacific region leads with a share of 45.0%, and is expected to grow over the forecast period.

Ans: Excessive use of plastic in this industry will restrain market growth.

Ans: Increasing Demand for Personal Care and Beauty Products.

Ans: The Cosmetic Packaging Market size was USD 36.21 billion in 2022 and is expected to Reach USD 51.49 billion by 2030.

Ans: The Cosmetic Packaging Market is expected to grow at a CAGR of 4.5 %.

Get in Touch