Data Centre Cooling Market Report Scope & Overview:

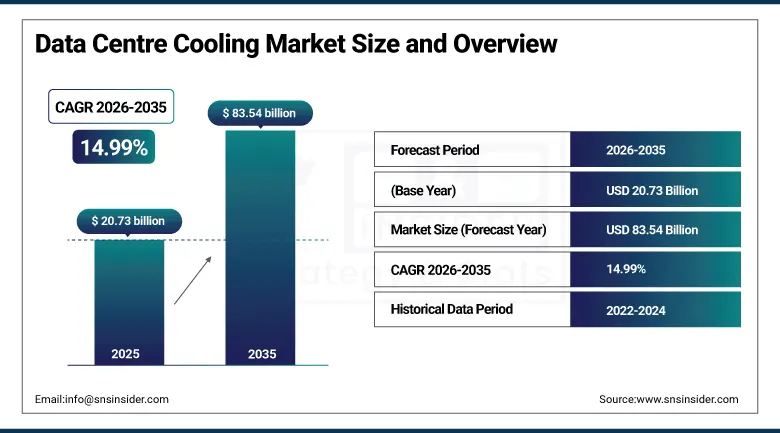

The Data Centre Cooling Market was valued at USD 20.73 Billion in 2025 and is expected to reach USD 83.54 Billion by 2035, growing at a CAGR of 14.99% from 2026–2035.

The global data centre cooling market is growing rapidly. AI training, inference, and high-performance computing workloads are generating unprecedented heat densities that legacy air cooling cannot manage. Data centres account for 1–2% of global electricity consumption, with cooling representing 30–40% of that footprint. Hyperscale operators, cloud providers, and colocation facilities are investing in energy-efficient liquid cooling, direct-to-chip cooling, and AI-driven thermal management to reduce power usage effectiveness and meet net zero commitments. Edge computing proliferation is extending cooling investment beyond centralised hyperscale campuses into distributed network infrastructure globally.

Schneider Electric partnered with NVIDIA in 2024 to develop optimised power and cooling infrastructure for AI data centre deployments, delivering reference designs combining direct liquid cooling for GPU racks with AI-driven DCIM software. The partnership targets hyperscale operators upgrading existing facilities for GPU-dense AI workloads where traditional air-cooled CRAC unit infrastructure cannot maintain inlet temperatures within GPU operating specifications at the rack densities that AI training clusters require.

Market Size and Forecast

-

Market Size in 2026E: USD 23.84 Billion

-

Market Size by 2035: USD 83.54 Billion

-

CAGR: 14.99% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Data Centre Cooling Market - Request Free Sample Report

Data Centre Cooling Market Trends

-

AI and GPU workload proliferation is driving rack power densities above 30–60 kW per rack, making liquid cooling adoption a capital prerequisite rather than an optional efficiency improvement for high-density deployments.

-

Liquid cooling investment is accelerating across direct-to-chip, rear-door heat exchanger, and immersion cooling formats as operators seek thermal management solutions compatible with next-generation GPU server specifications.

-

AI-driven DCIM platforms are enabling real-time cooling optimisation that reduces energy consumption by 15–25% by dynamically adjusting output to actual server thermal load rather than fixed conservative setpoints.

-

Modular and prefabricated data centre deployment is driving demand for integrated, factory-assembled cooling solutions whose rapid deployment capability reduces construction timelines for edge and enterprise capacity expansion.

-

Free cooling and economiser technologies are extending their operational windows as adiabatic coolers and indirect evaporative systems reduce mechanical refrigeration hours and lower annual PUE across temperate climate facilities.

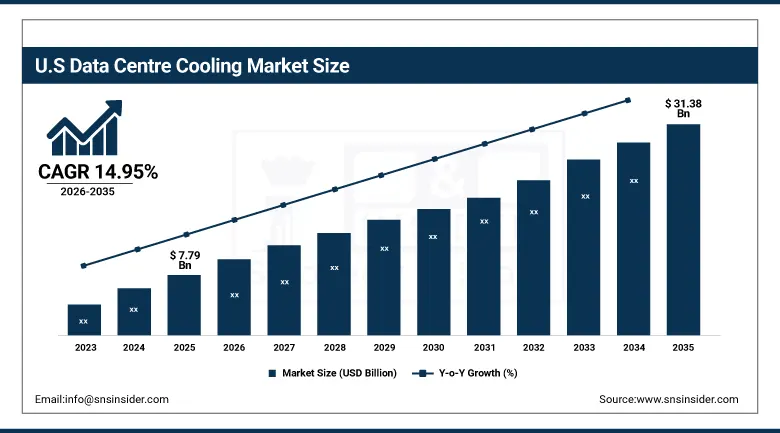

U.S. Data Centre Cooling Market Outlook

The U.S. Data Centre Cooling Market was valued at approximately USD 7.79 Billion in 2025 and is expected to reach approximately USD 31.38 Billion by 2035, growing at a CAGR of approximately 14.95%.

The U.S. is the world’s largest data centre cooling market. It hosts the highest density of hyperscale facilities globally. Amazon, Microsoft, Google, and Meta operate hundreds of campus locations whose AI infrastructure upgrade programmes create the most commercially significant cooling procurement environment in the market. IRA tax credits for energy-efficient building systems create financial incentives for cooling technology upgrades. Northern Virginia’s data centre corridor, the world’s fastest-growing data centre market, is simultaneously facing power and cooling water constraints that drive premium investment in efficient cooling technology.

Vertiv launched its CoolPhase Flex two-phase direct liquid cooling system in 2025, targeting GPU rack densities exceeding 50 kW for AI training infrastructure. The system enables operators to deploy liquid cooling within existing facility envelopes without full-facility infrastructure replacement, directly addressing the commercial challenge of upgrading operating data centres for high-density AI workloads on accelerated deployment timelines.

Data Centre Cooling Market Segment Analysis

-

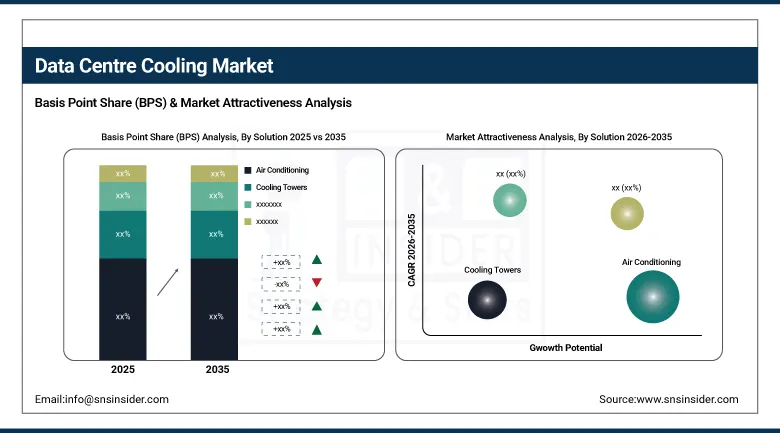

By Solution, the Air Conditioning/CRAC segment dominated the Data Centre Cooling Market with approximately 52% share in 2025, while the Liquid Cooling Systems segment is the fastest growing with a CAGR of approximately 22.5% during 2026–2035.

-

By Data Center Type, the Enterprise Data Center segment dominated the Data Centre Cooling Market with approximately 65% share in 2025, while the Edge Data Center segment is the fastest growing with a CAGR of approximately 18.7% during 2026–2035.

-

By Cooling Technique, the Air-Based segment dominated the Data Centre Cooling Market with approximately 68% share in 2025, while the Liquid-Based segment is the fastest growing with a CAGR of approximately 24.3% during 2026–2035.

-

By End User, the IT & Telecom segment dominated the Data Centre Cooling Market with approximately 38% share in 2025, while the BFSI segment is the fastest growing with a CAGR of approximately 17.2% during 2026–2035.

By Solution, air conditioning dominates, liquid cooling grows fastest

Air conditioning and CRAC/CRAH systems retained the dominant solution position with approximately 52% of the data centre cooling market in 2025. Their prevalence reflects the global installed base reality. Most enterprise and mid-scale data centres were built with room-based air-cooling infrastructure whose replacement follows planned refresh cycles. Traditional air cooling remains effective for rack densities below 10 kW. The commercial market for air cooling solutions continues generating substantial procurement through facility maintenance, system refresh, and new construction where rack densities remain within manageable thresholds.

Liquid cooling systems are the fastest-growing solution at approximately 22.5% CAGR because AI infrastructure deployment has fundamentally changed data centre thermal requirements. NVIDIA H100 and H200 GPU servers generate 5–10 kW per server and require 20–50+ kW per rack in dense AI training configurations. Air cooling cannot maintain inlet temperatures at these densities without compromising server reliability. Each new AI training cluster commissioned creates a defined liquid cooling procurement requirement. Hyperscalers, GPU cloud providers, and AI-native enterprises are making liquid cooling mandatory infrastructure for high-performance deployments.

By Data Center Type, enterprise dominates, edge grows fastest

Enterprise data centres retained the dominant type position with approximately 65% of the data centre cooling market in 2025. The global enterprise installed base encompasses hundreds of thousands of corporate, government, educational, and institutional facilities whose aggregate cooling procurement substantially exceeds hyperscale by facility count. Enterprise cooling procurement spans facility upgrades, energy efficiency improvements, capacity expansion for cloud workload repatriation, and AI infrastructure additions that create consistent multi-dimensional demand across the segment annually.

Edge data centres are the fastest-growing type at approximately 18.7% CAGR because 5G network densification, IoT data processing, and real-time latency-sensitive applications require compute infrastructure positioned closer to end users. Edge facilities typically operate in space and power-constrained environments without specialist facilities teams. This creates demand for self-contained, low-maintenance cooling solutions including precision air conditioners, integrated thermal management modules, and weatherised outdoor enclosures whose geographic distribution creates a structurally expanding addressable market.

By Cooling Technique, air-based dominates, liquid-based grows fastest

Air-based cooling retained the dominant technique position with approximately 68% of the data centre cooling market in 2025. Its incumbency reflects legacy infrastructure investment, operational familiarity, and continuing viability for the majority of deployed server rack densities. Room-based air distribution, hot aisle and cold aisle containment, and precision CRAC units collectively serve the installed base effectively at densities that represent the majority of current enterprise deployment. Economiser technologies including air-side economisers and indirect evaporative cooling are progressively improving energy efficiency, extending air-based cooling’s commercial viability.

Liquid-based cooling is the fastest-growing technique at approximately 24.3% CAGR because GPU thermal output has crossed the threshold at which air cooling transitions from adequate to operationally impractical. Direct liquid cooling routes coolant through cold plates mounted directly on server components, eliminating the air-path thermal resistance that limits conventional heat removal capacity. Immersion cooling submerges entire server boards in dielectric fluid, achieving the highest heat removal efficiency of any technique. Submer, Green Revolution Cooling, and Asperitas are expanding immersion capacity while Vertiv and Schneider Electric scale direct-to-chip deployments.

By End User, IT & telecom dominates, BFSI grows fastest

IT and telecom retained the dominant end user position with approximately 38% of the data centre cooling market in 2025. Cloud service providers, telecommunications operators, managed hosting companies, and enterprise IT departments collectively represent the highest-volume procurement category. Hyperscale cloud operators including AWS, Microsoft Azure, and Google Cloud alone operate hundreds of global campus locations whose combined cooling infrastructure investment exceeds the entire market value of many other industry verticals. The AI infrastructure investment wave is concentrated within this segment.

BFSI is the fastest-growing end user at approximately 17.2% CAGR because financial services data infrastructure combines the highest uptime standards of any commercial industry with growing computational intensity from real-time risk analytics, algorithmic trading, fraud detection, and digital banking platforms. Banking regulators require documented operational resilience for critical infrastructure including data centre cooling systems. Each financial services digital transformation programme that increases computational density creates proportional cooling upgrade investment whose compliance urgency sustains procurement through economic cycle variation.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Data Centre Cooling Market Insights

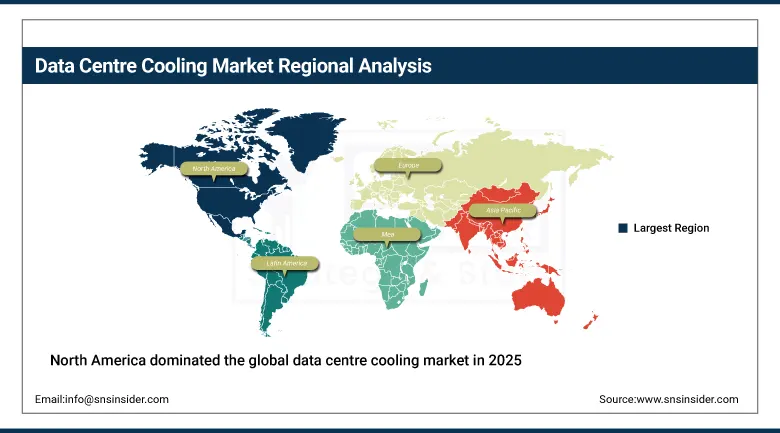

North America dominated the global data centre cooling market in 2025, accounting for approximately 43.5% of global revenues. The United States holds approximately 87.4% of North American revenues. The U.S. is home to the world’s largest hyperscale data centre fleet and the highest GPU cluster deployment density. Northern Virginia, Dallas, Phoenix, and Chicago are the world’s highest-density data centre markets, each generating cooling procurement of extraordinary commercial scale. AI infrastructure investment by AWS, Microsoft, Google, and Meta is creating the fastest-growing data centre cooling demand wave in the market’s history.

Canada contributes approximately 12.6% of North American revenues through its growing colocation markets in Toronto and Vancouver, favourable cold climate conditions that reduce mechanical cooling energy requirements, and federal government data centre investment. Quebec’s hydroelectric power and cool climate create particularly compelling economics for hyperscale deployment where extended free cooling hours reduce annual cooling energy cost substantially.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Data Centre Cooling Market Insights

Europe is a technically sophisticated data centre cooling market where the EU Energy Efficiency Directive’s PUE requirements, national renewable energy targets, and the Frankfurt-Amsterdam-London data centre triangle’s hyperscale and colocation infrastructure create structured demand.

Germany accounts for approximately 22.3% of European revenues through Frankfurt’s position as Europe’s largest data centre hub, high-standard German industrial cooling manufacturers, and EU Taxonomy green investment classification that incentivises energy-efficient cooling upgrades.

The Netherlands, United Kingdom, and Ireland are significant secondary markets where Amsterdam’s internet exchange concentration, London’s financial services data centre density, and Dublin’s hyperscale expansion create consistent cooling investment. Nordic markets including Sweden and Norway are growing rapidly as their cold climate, renewable energy, and land availability attract hyperscale investment that leverages natural free cooling economics to achieve the lowest achievable annual PUE.

Asia Pacific Data Centre Cooling Market Insights

Asia Pacific is the fastest-growing regional data centre cooling market, driven by extraordinary construction investment across China, India, Singapore, Japan, and South Korea. China accounts for approximately 44.8% of Asia Pacific revenues through the government’s New Infrastructure Programme, the hyperscale facilities of Alibaba Cloud, Tencent, and Baidu, and domestic cooling manufacturers whose production scale creates competitive supply. Government-mandated PUE limits are simultaneously creating mandatory energy-efficient cooling upgrade requirements across the Chinese data centre fleet.

India and Southeast Asia represent the most commercially dynamic emerging markets where rapid cloud adoption, government digital infrastructure investment, and hyperscale operator entry are creating first-time large-scale facility construction requiring comprehensive cooling infrastructure. Singapore’s resumption of new data centre approvals and Indonesia’s digital economy investment are creating significant capacity additions whose cooling requirements sustain regional market growth.

MEA & Latin America Data Centre Cooling Market Insights

The Middle East and Africa and Latin America are growing data centre cooling markets where hyperscale investment, government cloud adoption, and data sovereignty regulation are driving new facility construction. UAE leads MEA revenues at approximately 38.4% through Dubai and Abu Dhabi’s hyperscale programmes, extreme summer ambient temperatures that intensify cooling requirements, and the UAE government’s national AI and cloud strategy investment.

Brazil leads Latin American revenues at approximately 44.2% through its large cloud service provider market in São Paulo, energy sector data centre infrastructure, and LGPD data sovereignty motivation for local capacity. The tropical climate’s year-round cooling requirement and growing hyperscale investment from AWS, Google, and Microsoft whose Brazilian capacity is expanding create consistent high-value cooling procurement across the forecast period.

Growth Drivers: AI workload heat density requiring liquid cooling and hyperscale data centre expansion creating record procurement

AI infrastructure deployment is the data centre cooling market’s most commercially consequential immediate growth driver. NVIDIA’s GPU roadmap continues increasing per-chip thermal design power with each generation. The H200 exceeds 700W TDP. These power levels create rack thermal loads requiring liquid cooling investment as a capital prerequisite for AI infrastructure deployment. Each exabyte of AI training capacity commissioned creates a defined cooling capital requirement whose commercial value scales with infrastructure investment and accelerates as GPU performance continues advancing.

Hyperscale capacity expansion by cloud providers is creating the largest sustained data centre construction investment wave in computing history. AWS, Microsoft Azure, Google Cloud, and Meta collectively announced over USD 200 billion in combined data centre capital investment programmes for 2024–2026. Each campus commissioned requires cooling infrastructure representing 15–25% of total facility capital expenditure. The cooling market’s commercial growth is directly and proportionally linked to this construction momentum whose multi-year programme commitments create commercially certain demand.

Restraints: High liquid cooling retrofit cost in legacy facilities and water consumption concerns in drought-affected regions

Liquid cooling retrofit cost in operating legacy data centres is the primary adoption barrier. Retrofitting a live facility with direct-to-chip or immersion cooling requires careful migration planning, temporary cooling redundancy, and mechanical infrastructure modification. This creates capital cost substantially above greenfield deployment. Many enterprise operators defer liquid cooling until scheduled facility refresh or new capacity construction, extending air cooling’s operational lifespan beyond its thermal management optimality for density-limited environments.

Water consumption concerns are creating operational risk in drought-affected geographies. Evaporative cooling systems that deliver best-in-class energy efficiency consume substantial water volumes. Phoenix, Arizona and locations across the U.S. Southwest face regulatory and social licence pressure over water consumption. Local authority restrictions can limit cooling technology selection and increase energy cost relative to water-unlimited locations, creating a geographic constraint on optimal cooling technology deployment strategy.

Opportunities: AI data centre premium cooling market, cooling-as-a-service managed model, and greenfield emerging market construction integrating liquid cooling as standard

The AI-as-a-Service infrastructure build-out creates the most commercially significant near-term premium cooling market. CoreWeave, Lambda Labs, and hyperscale GPU cloud providers are building dedicated AI training campuses whose entire cooling infrastructure is specified for high-density liquid cooling from inception. These greenfield deployments eliminate retrofit complexity and maximise liquid cooling revenue per megawatt of facility power capacity, creating the highest-value per-installation cooling procurement relationships in the market.

Cooling-as-a-service represents a commercially attractive managed model whose recurring revenue structure benefits infrastructure providers deploying and operating cooling systems under performance-based contracts. This model transfers capital expenditure burden from data centre operators to vendors, potentially accelerating adoption among enterprises whose capital allocation constraints defer upgrades. Vertiv and Schneider Electric are developing service model offerings whose managed operations capability creates long-term customer relationships beyond transactional equipment sales.

Recent Developments:

-

2024: Schneider Electric partnered with NVIDIA to develop optimised power and cooling reference designs for AI data centre GPU deployments, combining direct liquid cooling with AI-driven DCIM software to help hyperscale operators manage thermal and power challenges of high-density AI workloads.

-

2025: Vertiv launched its CoolPhase Flex two-phase direct liquid cooling system, targeting GPU rack densities exceeding 50 kW for AI training infrastructure, enabling operators to deploy liquid cooling within existing facility envelopes without full-facility infrastructure replacement.

-

2025: Green Revolution Cooling expanded its immersion cooling deployment capacity with new single-phase dielectric fluid formulations achieving improved thermal conductivity for hyperscale AI and HPC deployments, targeting operators seeking the lowest achievable PUE through full-immersion cooling architecture.

Data Centre Cooling Market Key Players

-

Schneider Electric

-

Vertiv Group Corp.

-

Johnson Controls

-

Rittal

-

Stulz

-

Emerson Electric

-

Airedale International

-

DataSpan

-

Green Revolution Cooling

-

Submer Technologies

-

CoolIT Systems

-

Asperitas

-

Delta Electronics

-

Mitsubishi Electric

-

Daikin Industries

-

Alfa Laval

-

Condair Group

-

Munters Group

-

LiquidStack

-

Iceotope Technologies

Data Centre Cooling Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 20.73 Billion |

| Market Size by 2035 | USD 83.54 Billion |

| CAGR | CAGR of 14.99% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Solution (Air Conditioning, Cooling Towers, Liquid Cooling Systems, CRAC/CRAH, Economizer Systems, Others) • by Data Center Type (Enterprise Data Center, Edge Data Center) • by Cooling Technique (Air-Based, Liquid-Based) • by End User (IT & Telecom, BFSI, Government, Healthcare, Retail, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Schneider Electric, Vertiv Group Corp., Johnson Controls, Rittal, Stulz, Emerson Electric, Airedale International, DataSpan, Green Revolution Cooling, Submer Technologies, CoolIT Systems, Asperitas, Delta Electronics, Mitsubishi Electric, Daikin Industries, Alfa Laval, Condair Group, Munters Group, LiquidStack, Iceotope Technologies |

Frequently Asked Questions

The Data Centre Cooling Market is expected to grow at a CAGR of 14.99% from 2026 to 2035.

The Data Centre Cooling Market was valued at USD 20.73 Billion in 2025.

AI and GPU workload deployment creating rack heat densities that require liquid cooling investment, hyperscale cloud providers committing over USD 200 billion in data centre capital investment for 2024–2026, and energy efficiency regulations mandating PUE improvements that drive cooling technology upgrades.

Air-Based cooling dominated the Data Centre Cooling Market with approximately 68% share in 2025, while Liquid-Based is the fastest growing at approximately 24.3% CAGR during 2026–2035.

North America dominated the Data Centre Cooling Market in 2025 with approximately 43.5% of global revenues, with the United States holding approximately 87.4% of North American revenues.

Get in Touch