Digital Substation Market Report Scope & Overview:

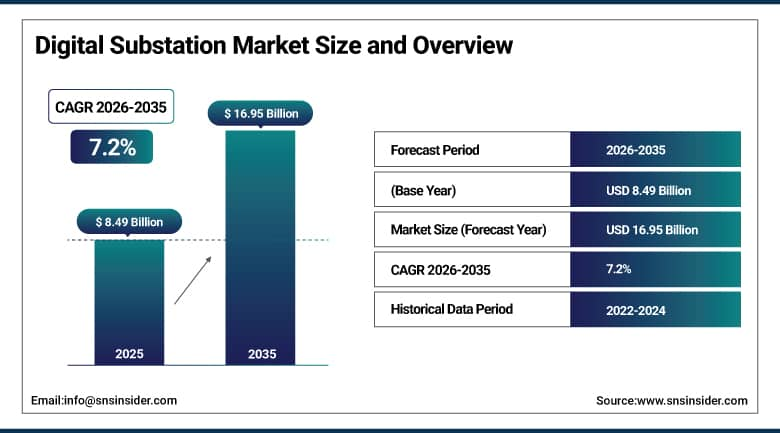

The Digital Substation Market was valued at USD 8.49 Billion in 2025 and is expected to reach USD 16.95 Billion by 2035, growing at a CAGR of 7.2% from 2026–2035.

The global digital substation market is growing at a steady and commercially significant pace. Digital substations replace traditional electromechanical protection and control systems with intelligent electronic devices, fiber-optic process bus communication, and digital SCADA platforms operating under IEC 61850 communication standards, fundamentally transforming how electrical power is controlled, monitored, and protected at the substation level. The market is growing rapidly due to rising grid modernisation efforts, energy efficiency needs, and renewable energy integration. Digital substations leverage automation, advanced communication networks, and intelligent electronic devices to enhance power distribution reliability while reducing maintenance costs and power losses.

In July 2023, ABB Ltd. launched an advanced IED platform with enhanced cybersecurity features, ensuring secure data transmission in digital substations. The platform’s integrated cybersecurity architecture addresses the growing vulnerability of grid-connected digital systems to cyber-attack whose operational technology network exposure creates critical infrastructure risk that unprotected legacy communication protocols cannot mitigate. ABB’s cybersecurity-integrated IED demonstrates the commercial direction of digital substation hardware development toward security-by-design whose protection capability creates compliance value for regulated utility procurement programmes.

Market Size and Forecast:

-

Market Size in 2026E: USD 9.10 Billion

-

Market Size by 2035: USD 16.95 Billion

-

CAGR: 7.2% from 2026 to 2035

-

Fastest Growing Region: North America (11.5% CAGR)

-

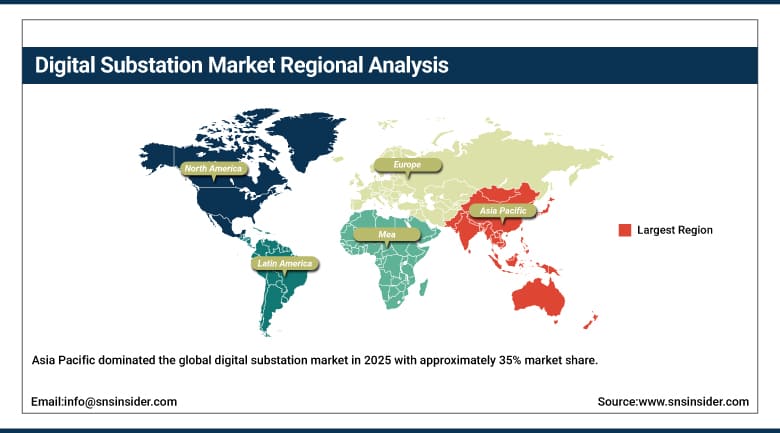

Largest Region: Asia Pacific (35%)

To Get More Information On Digital Substation Market - Request Free Sample Report

Digital Substation Market Trends:

-

Adoption of the IEC 61850 standard is accelerating digital substation deployment by enabling seamless interoperability, standardized communication, and multi-vendor integration across power networks

-

Increasing focus on cybersecurity is driving investment in secure digital substation architectures, advanced network protection solutions, and operational technology (OT) security systems

-

Digital twin technology is gaining traction for asset management, predictive maintenance, performance optimization, and virtual testing of substation operations

-

Growing integration of renewable energy sources is increasing demand for advanced digital substations capable of managing grid stability, power quality, and variable energy generation

-

Expansion of electric vehicle charging infrastructure is driving modernization of distribution networks and creating additional demand for intelligent digital substation solutions that support higher power loads and grid flexibility

U.S. Digital Substation Market Outlook:

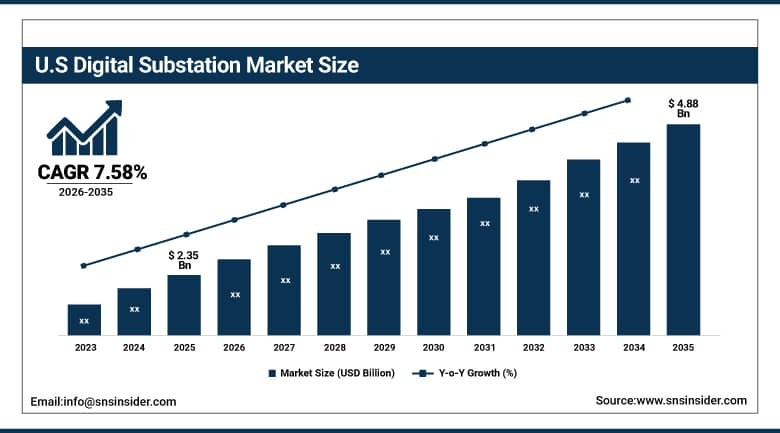

The U.S. Digital Substation Market is estimated to be USD 2.35 Billion in 2025 and is projected to reach USD 4.88 Billion by 2035, growing at a CAGR of 7.58% during 2026–2035.

The U.S. Digital Substation Market is the most commercially significant national market within the fastest-growing North American region. ABB, Siemens, GE Grid Solutions, Schneider Electric, and Eaton’s U.S. operations collectively define the domestic digital substation commercial landscape. The U.S. Department of Energy’s Grid Modernisation Initiative, IRA’s grid infrastructure investment incentive, and NERC’s Critical Infrastructure Protection cybersecurity standards create structured utility procurement motivation. The extraordinary U.S. renewable energy buildout creates proportional digital substation investment that compounds with the utility sector’s grid reliability programme.

Siemens AG introduced its SIPROTEC 5 Protection Relay Series in 2023 for high-performance grid automation and fault detection, featuring IEC 61850 native communication, integrated cybersecurity, and universal hardware platform that supports all protection, automation, and control functions in a single device. The SIPROTEC 5’s consolidation of multiple traditional relay functions creates installation cost reduction through fewer devices, reduced wiring, and simpler maintenance that creates economic motivation for digital substation upgrade beyond pure performance improvement.

Digital Substation Market Segment Analysis:

-

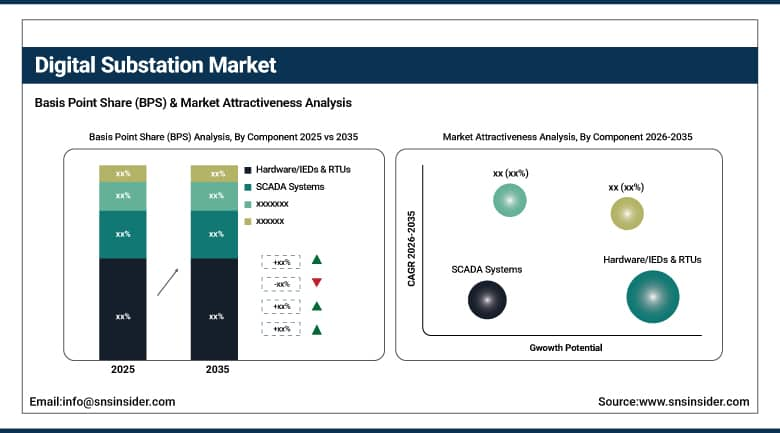

By Component, the Hardware segment dominated the Digital Substation Market with 53% share in 2025, while the SCADA segment is projected to grow at the highest CAGR.

-

By Type, the Distribution Substation segment dominated the Digital Substation Market with 61% share in 2025, while the Transmission Substation segment is expected to witness the highest CAGR of 8.0%.

-

By End User, the Utility segment dominated the Digital Substation Market with 52% share in 2025, while the Transportation segment is expected to grow at the highest CAGR of 8.7%.

-

By Installation Type, the Retrofit Installation segment dominated the Digital Substation Market with approximately 58% share in 2025, while the New Installation segment is the fastest growing.

By Component, hardware dominates, SCADA grows fastest

Hardware retained the dominant component position with 53% of the digital substation market in 2025. Hardware’s commercial primacy reflects the foundational infrastructure requirement that every digital substation programme requires before communication networks and SCADA create operational value. Intelligent electronic devices’ role as the protection, control, and monitoring foundation of every digital substation creates consistent per-substation hardware procurement whose aggregate across thousands of annual digital substation projects creates commercial scale. Merging units whose analogue-to-digital conversion at the process level eliminates copper pilot wiring between switchgear and protection relays, fiber-optic process bus infrastructure, and remote terminal units collectively create hardware procurement whose commercial value reflects the physical infrastructure investment in every digital substation programme.

SCADA is the fastest-growing component because the digital substation’s data generation capability creates supervisory control and monitoring platform demand whose analytics, visualization, and operational intelligence value compounds with the digital substation installed base’s expansion. Each digital substation that connects to the utility’s SCADA network creates data stream consumption whose aggregate from hundreds of substations creates centralized grid intelligence whose operational value sustains software procurement investment.

By Type, distribution dominates, transmission grows fastest

Distribution substations retained the dominant type position with 61% of the digital substation market in 2025. Distribution’s commercial primacy reflects the vastly greater number of distribution substations relative to transmission alternatives, whose combined procurement creates commercial scale that transmission’s higher per-substation investment cannot match by project count. Each urban distribution substation serving residential and commercial load creates digital upgrade procurement whose aggregate across the global distribution network’s extensive asset base creates consistent commercial volume. The distribution network’s progressive urban density increase from EV charging, heat pump electrification, and data center load creates upgrade motivation that sustains distribution digital substation investment.

Transmission substations are the fastest-growing type at 8.0% CAGR because high-voltage transmission infrastructure’s extraordinary investment momentum, driven by renewable energy’s geographic remoteness from consumption centers and HVDC interconnection projects, creates per-project digital substation procurement whose scale reflects the transmission system’s power capacity. Each new renewable energy transmission corridor creates digital substation specification at both generation connection and load center injection points whose premium specification reflects the transmission system’s power handling requirement.

By End User, utilities dominate, transportation grows fastest

Utilities retained the dominant end-user position with 52% of the digital substation market in 2025. The utility sector’s systematic grid modernisation programme, driven by government policy mandates, renewable integration requirements, and reliability improvement motivation, creates the most commercially concentrated digital substation procurement environment. Each utility’s capital expenditure programme that includes digital substation investment creates structured commercial relationships with ABB, Siemens, GE Grid Solutions, and Schneider Electric whose combined market position defines the utility procurement landscape. NERC’s critical infrastructure protection standards create compliance-driven procurement motivation that sustains utility digital substation investment independently of discretionary capex cycle variation.

Transportation is the fastest-growing end user at 8.7% CAGR because metro rail electrification, high-speed rail’s traction substation investment, and the EV charging network’s distribution infrastructure upgrade collectively create structured transportation sector digital substation procurement. Each new metro system’s traction substation programme creates digital specification whose IEC 61850 communication and remote monitoring capability creates operational efficiency improvement over conventional electromechanical alternatives. The EV charging infrastructure’s distribution network upgrade creates digital substation investment that compounds with the EV market’s extraordinary adoption pace.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

Asia Pacific Digital Substation Market Insights

Asia Pacific dominated the global digital substation market in 2025 with approximately 35% market share. China accounts for approximately 44.8% of Asia Pacific revenues through its extraordinary smart grid infrastructure investment, the State Grid Corporation’s digital substation programme, and the renewable energy buildout’s grid connection investment. The region’s rapid urbanization and industrialization create consistent distribution substation investment that sustains Asia Pacific’s commercial leadership.

India’s government smart grid programme, Japan’s advanced grid infrastructure, and South Korea’s smart energy investment create significant secondary markets whose combined procurement reinforces Asia Pacific’s dominant regional position.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Digital Substation Market Insights

North America is the fastest-growing regional digital substation market with 11.5% CAGR, driven by IRA’s grid infrastructure investment incentive, DOE’s Grid Modernisation Initiative, and NERC’s cybersecurity standards creating structured compliance procurement. The United States accounts for approximately 87.4% of North American revenues through ABB, Siemens, GE Grid Solutions, and Schneider Electric’s commercial operations.

Canada contributes approximately 12.6% of North American revenues through its hydro and renewable energy grid modernisation, the transmission infrastructure upgrade for clean energy export, and the distribution network’s digital substation investment.

Europe Digital Substation Market Insights

Europe is a technically sophisticated digital substation market where the EU Green Deal’s renewable energy integration, Directive 2009/72/EC’s smart grid mandate, and ABB’s and Siemens’ European commercial leadership create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its extraordinary renewable energy transition’s grid investment, Siemens AG’s domestic market presence, and the transmission grid’s digital upgrade programme.

France, the United Kingdom, and the Netherlands are significant secondary markets where offshore wind connection investments, nuclear power plant modernisation, and EV charging infrastructure create consistent digital substation procurement.

MEA & Latin America Digital Substation Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through its Vision 2030 renewable energy investment, the NEOM smart city’s grid infrastructure, and the national grid’s digitalization programme. Brazil leads Latin American revenues at approximately 44.2% through its renewable energy grid connection investment, Eletrobras’ modernisation programme, and the distribution network’s digital upgrade.

Market Dynamics:

Growth Drivers: Grid modernisation investment and renewable energy integration requiring digital protection flexibility

Rising grid modernisation efforts, energy efficiency needs, and renewable energy integration are SNS Insider’s confirmed primary growth drivers. The energy transition’s requirement for bidirectional power flow management, distributed generation protection, and real-time grid intelligence creates digital substation investment whose technical necessity sustains procurement across utility budget cycles. Each government renewable energy target creates proportional grid infrastructure investment whose digital substation component compounds with clean energy capacity addition.

Government stimulus programmes for grid infrastructure investment, including the U.S. IRA’s USD 65 billion grid investment, the EU’s REPowerEU initiative, and China’s smart grid programme, create the most commercially certain near-term demand driver whose non-discretionary infrastructure investment creates predictable digital substation procurement that sustains commercial relationships.

Restraints: High initial investment cost and cybersecurity vulnerability of OT-connected digital systems

Digital substation’s higher initial capital investment relative to conventional electromechanical alternatives creates procurement barriers for utilities in cost-constrained developing market contexts whose revenue-to-investment ratios create economic motivation for lower-cost conventional specification. Each utility whose regulatory framework creates insufficient return on advanced infrastructure investment creates specification pressure toward minimum compliance cost rather than premium digital capability.

Operational technology network’s connection to corporate IT infrastructure creates cybersecurity attack surface exposure whose critical infrastructure risk creates security investment requirement that increases total digital substation system cost above hardware specification alone.

Opportunities: EV charging grid infrastructure and digital twin asset management

EV charging infrastructure’s distribution network upgrade creates structured near-term digital substation procurement whose grid reinforcement investment compounds with the EV market’s extraordinary adoption pace. Each new high-power DC charging hub whose load creates distribution transformer and substation upgrade creates digital specification motivation.

Digital twin deployment for substation lifecycle management creates premium software and analytics procurement whose predictive maintenance, virtual testing, and operational optimization value sustains commercial relationships beyond initial hardware investment.

Recent Developments:

-

2023: ABB Ltd. launched an advanced IED platform with enhanced cybersecurity features in July 2023, ensuring secure data transmission in digital substations and addressing the growing OT network vulnerability of grid-connected digital systems.

-

2023: Siemens AG introduced its SIPROTEC 5 Protection Relay Series in 2023 for high-performance grid automation and fault detection, featuring IEC 61850 native communication, integrated cybersecurity, and universal hardware platform.

-

2024: Schneider Electric expanded its EcoStruxure digital substation solution portfolio in 2024 with new IEC 61850 process bus-compatible IEDs and enhanced ADMS integration for utility-scale distribution automation and renewable energy management.

Digital Substation Market Key Players:

-

ABB Ltd.

-

Siemens AG (SIPROTEC)

-

GE Grid Solutions (GE Vernova)

-

Schneider Electric SE

-

Eaton Corporation

-

Honeywell International Inc.

-

NR Electric Co., Ltd.

-

Tekvel LLC

-

Ametek Inc.

-

Littelfuse Inc.

-

Rockwell Automation Inc.

-

Cisco Systems Inc. (Industrial Networking)

-

Hitachi Energy Ltd.

-

OMICRON Electronics GmbH

-

Atos SE

-

Schweitzer Engineering Laboratories (SEL)

-

TE Connectivity Ltd.

-

Phoenix Contact GmbH & Co. KG

-

Fujitsu Limited

-

Ingeteam Power Technology S.A.

Digital Substation Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 8.49 Billion |

| Market Size by 2035 | USD 16.95 Billion |

| CAGR | CAGR of 7.2% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Component (Hardware/IEDs & RTUs, Fiber-Optic Communication Networks, SCADA Systems, Software & Services) • by Type (Distribution Substation, Transmission Substation) • by Installation Type (New Installation, Retrofit Installation) • by Voltage Level (Up to 220 kV, 220–500 kV, above 500 kV) • by End User (Utility, Heavy Industries, Transportation, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | ABB Ltd., Siemens AG (SIPROTEC), GE Grid Solutions (GE Vernova), Schneider Electric SE, Eaton Corporation, Honeywell International Inc., NR Electric Co., Ltd., Tekvel LLC, Ametek Inc., Littelfuse Inc., Rockwell Automation Inc., Cisco Systems Inc. (Industrial Networking), Hitachi Energy Ltd., OMICRON Electronics GmbH, Atos SE, Schweitzer Engineering Laboratories (SEL), TE Connectivity Ltd., Phoenix Contact GmbH & Co. KG, Fujitsu Limited, Ingeteam Power Technology S.A. |

Frequently Asked Questions

The Digital Substation Market is expected to grow at a CAGR of 7.2% from 2026 to 2035.

The Digital Substation Market was valued at USD 8.49 Billion in 2025.

Rising grid modernisation efforts, energy efficiency needs, and renewable energy integration requiring digital protection flexibility, with government smart grid infrastructure investment creating structured procurement that sustains digital substation market expansion.

Hardware dominated the Digital Substation Market with 53% share in 2025 as confirmed by SNS Insider, while SCADA is projected to grow at the highest CAGR.

Transmission Substation is expected to witness the highest CAGR of 8.0% during the forecast period, while Distribution Substation dominated with 61% share in 2025.

Get in Touch