Disposable Endoscopes Market Report Scope & Overview:

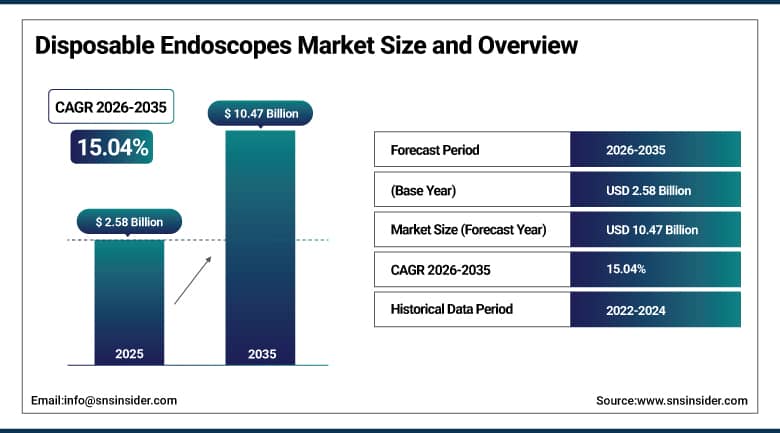

The Disposable Endoscopes Market was valued at USD 2.58 Billion in 2025 and is expected to reach USD 10.47 Billion by 2035, growing at a CAGR of 15.04% from 2026–2035.

Roughly 50 million endoscopic procedures happen worldwide every year, and a growing share of them now use a scope that gets thrown away after a single patient rather than sterilized and reused. That shift is being driven almost entirely by infection control concerns, cross-contamination risk from reprocessed endoscopes has been a persistent headache in hospital settings, and single-use devices simply eliminate that risk outright. Flexible disposable endoscopes have taken over most of pulmonology, urology, and gastroenterology, while rigid disposable types handle more basic orthopedic and gynecological applications. As hospitals and ambulatory surgical centers keep prioritizing patient safety over the lower per-unit cost of reusable scopes, this market keeps expanding at a pace that's unusual even by medical device standards.

The flexible disposable endoscope had more than 60% share of global market demand in 2025 due to increased utilization in pulmonary medicine and gastroenterology practices. The domination of this product form in two specialized medical disciplines speaks volumes about the location of growth in this market.

Market Size and Forecast

-

Market Size in 2026E: USD 2.97 Billion

-

Market Size by 2035: USD 10.47 Billion

-

CAGR: 15.04% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Disposable Endoscopes Market - Request Free Sample Report

Disposable Endoscopes Market Trends

-

Over 15 million single-use bronchoscopies were conducted worldwide in 2025, with that number expected to surpass 30 million within a decade.

-

Disposable endoscopes were used in over 10 million urology procedures in 2025, and adoption is projected to nearly double by 2035 as kidney stone and prostate cases keep rising.

-

Ambulatory surgical centers performed roughly 8 million disposable endoscope-based procedures in 2025, a number expected to exceed 15 million by 2035.

-

Online healthcare marketplaces delivered about half a million single-use endoscopes last year, with volume projected to top 1.5 million by 2035.

-

More than 20 million disposable endoscopes were used in hospitals worldwide in 2025, and demand is expected to exceed 35 million by 2035.

The U.S. Disposable Endoscopes Market Outlook

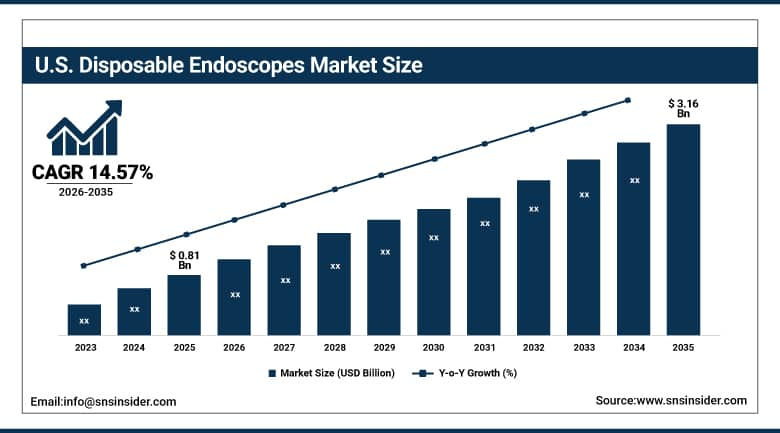

The U.S. Disposable Endoscopes Market was valued at approximately USD 0.81 Billion in 2025 and is expected to reach approximately USD 3.16 Billion by 2035, growing at a CAGR of approximately 14.57%.

More than 4.2 million endoscopic surgeries have been conducted across the nation in the year 2025 mainly because of the availability of advanced facilities in the hospitals, infections control measures, and increased application of single-use instruments. The introduction of the technology in hospitals and ambulatory surgery centers can be considered one of the most significant growth drivers for the technology, with over 15,000 hospitals and clinics in the nation able to conduct bronchoscopy using over 500,000 disposable endoscopes.

In August 2025, Boston Scientific launched Endura Weight Loss Solutions that include procedures such as endoscopic sleeve gastroplasty and intragastric balloon. This is an indication of how the scope of single-use endoscopic platforms is growing beyond diagnosis to treatment and bariatric care too.

Disposable Endoscopes Market Segmentation Analysis

-

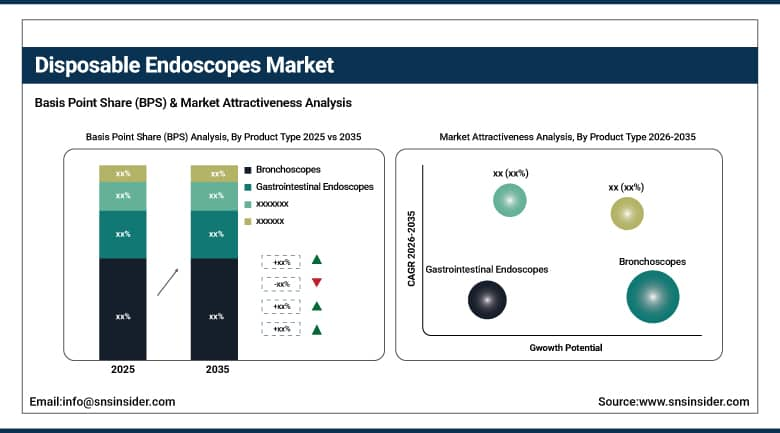

By Product Type, bronchoscopes held the largest share at 28.45% in 2025, while gastrointestinal endoscopes is the fastest-growing segment with a CAGR of 16.21%.

-

By Application, pulmonology contributed the highest share at 34.12% in 2025, while gastroenterology is expected to expand at the fastest CAGR of 16.53%.

-

By End User, hospitals accounted for the largest share at 55.36% in 2025, while ambulatory surgical centers are expected to record the fastest growth at a CAGR of 17.02%.

-

By Distribution Channel, direct sales comprised 50.27% share in 2025, while online platforms are projected to grow at the fastest CAGR of 17.98%.

By Product Type, bronchoscopes dominate, gastrointestinal endoscopes grow fastest

The demand for bronchoscopes continues to rise around the globe due to their widespread applicability in pulmonology procedures and interventions that have seen over 4.5 million procedures performed in 2025. The scope of this application ensures that the category remains the frontrunner.

There were around 2.9 million endoscopy procedures done using gastroenterology endoscopes in 2025, with more than 5.5 million procedures expected by 2033 due to increased prevalence of gastrointestinal diseases coupled with an increasing number of hospitals and diagnostic centers.

By Application, pulmonology dominates, gastroenterology grows fastest

It is estimated that pulmonology procedures will account for more than 5.2 million endoscopy procedures by 2025 because of the increasing incidence of lung diseases globally.

The fast adoption of gastroenterology procedures that reduce chances of cross-contamination involves the use of disposables and is expected to total approximately 4.1 million procedures by 2025. The increasing popularity of infection-free endoscopy as well as the demand for colonoscopy will ensure that disposable endoscopy procedures surpass 8 million procedures by 2033.

By End User, hospitals dominate, ambulatory surgical centers grow fastest

Hospitals continue to be the largest end user, carrying out more than 6 million disposable endoscope procedures in 2025 thanks to high patient volumes and genuine infection prevention need.

The ambulatory surgical centers will have carried out around 2.7 million procedures by 2025 and will definitely be using more than 5 million by 2033 as more surgeries and diagnostic procedures become outpatient procedures, with the single use endoscopes being used for their efficiency and safety.

By Distribution Channel, direct sales dominate, online platforms grow fastest

Direct sales provided nearly 5.5 million single-use endoscopes in 2025, since hospitals and large clinics tend to prefer purchasing directly from manufacturers rather than going through intermediaries.

Around 0.85 million units were purchased via the Internet in 2025, mostly by small clinics and laboratories. The overall digitization initiative would help the Internet-based purchases exceed 2.0 million units by 2033, providing convenience, efficiency, and ease for smaller and medium sized medical establishments around the world.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

70.0% |

|

Europe |

Germany |

30.0% |

|

Asia Pacific |

China |

50.0% |

|

Latin America |

Brazil |

55.0% |

|

Middle East & Africa |

Saudi Arabia |

28.0% |

North America Disposable Endoscopes Market Insights

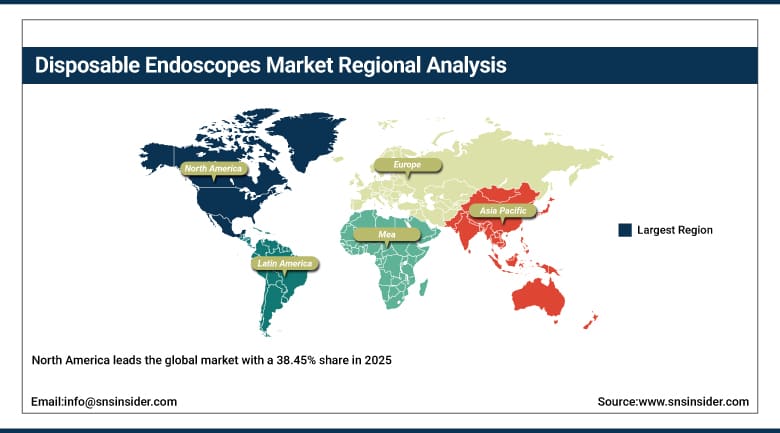

North America leads the global market with a 38.45% share in 2025, supported by advanced healthcare infrastructure and strong infection-control initiatives. More than 6 million endoscopic procedures were conducted in the region in 2025 for bronchoscopy, gastroenterology, and urology alone.

With more than 4.2 million procedures performed by U.S. hospitals and ambulatory surgical centers using single-use devices specifically to avert cross-contamination, that high procedural volume continues driving market growth through 2035. Canada contributes a smaller but consistent share of regional demand as well.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Disposable Endoscopes Market Insights

Europe commands significant growth in this market, with over 6,800 hospitals and 9,500 ambulatory surgical centers performing more than 5.8 million endoscopic procedures annually. Germany, France, and the UK are increasing their procedural capabilities and moving towards single-use products, with more than 65% of Western European hospitals adopting single-use endoscopes exclusively to prevent infections.

More than 30% of Europe’s disposable endoscope market, measured in units, is accounted for by Germany in 2025, driven by more than 2,100 hospitals and ambulatory surgery centers performing a large number of gastrointestinal and respiratory procedures. Strong infection-control focus and EU-supported initiatives continue positioning Germany as a hub for disposable endoscope deployment and innovation across the continent.

Asia Pacific Disposable Endoscopes Market Insights

Asia Pacific is expected to grow at a CAGR of 16.07% through 2035, emerging as the fastest-growing region globally. The region includes more than 8,500 hospitals and 12,000 ambulatory surgical centers performing over 7 million endoscopic procedures per year.

Rising infection control requirements, increasing numbers of procedures performed on the gastrointestinal and pulmonary tract, and governmental backing for healthcare are some of the factors driving the market growth; meanwhile, the Asia Pacific is estimated to account for nearly one-third of the total adoption of disposable endoscopes by 2033. In particular, China dominates the region, as there are more than 4,200 hospitals and 6,500 ASCs performing over 3.5 million endoscopy procedures annually.

MEA & Latin America Disposable Endoscopes Market Insights

The market of Latin America is expected to experience significant expansion till 2033, being led by Brazil with nearly 55% share of regional procedures and with more than 1,200 high volume hospitals and ambulatory surgical centers performing endoscopy, followed by Mexico and Argentina.

The Middle East and Africa market is also set to expand significantly, with more than 1,800 hospitals and ambulatory surgical centers functioning in the region by 2025. The early adopter in the market is Saudi Arabia because of Vision 2030 and advanced hospital infrastructure in the country, followed by South Africa with growing demand for advanced disposable endoscope technologies.

Growth Drivers: Rising hospital-acquired infections drive single-use adoption worldwide

The increasing global burden of hospital-acquired infections is accelerating adoption of single-use disposable endoscopes across healthcare systems. The number of hospital-acquired infections in the US alone reached 7 million in 2025. This is the reason why there has been a shift from reusing medical devices to using disposables.

It is estimated that over 45 million endoscopy procedures will be done in 2033, ensuring safety from cross-contamination. The main goal of infection-free patient management has been one of the major reasons for the fast adoption of disposable endoscopes in various clinical settings.

Restraints: High device costs and limited reimbursement restrict adoption

Expensive disposable endoscopes and a lack of insurance coverage represent real market restraints, particularly in underdeveloped healthcare regions. Disposable flexible endoscopes are designed for single use, while reusable scopes handle hundreds of cases, a cost differential that matters a lot at scale.

Hospitals performing over 5,000 procedures annually face genuine operational and logistical challenges, causing nearly 35% of small and mid-sized Asia-Pacific clinics to delay adopting single-use devices. This continues to slow entry of safer, infection-free endoscopy technology into more healthcare settings worldwide.

Opportunities: Demand for infection-free procedures drives advanced imaging innovation

Rising demand for infection-free procedures is expected to create opportunities for next-generation integrated imaging disposable endoscopes. More than 40% of new endoscopes are projected to include high-definition imaging by 2033, increasing diagnostic accuracy.

Clinical surveys demonstrate approximately 36% shorter procedural times relative to standard reusable scopes. Improved ergonomics and intuitive operation continue driving hospital and ASC adoption, and by 2026, disposable endoscopes with integrated imaging are projected to account for nearly 12% of new installations.

Recent Developments:

-

2025: In February 2025, Ambu A/S launched the aScope 5 Uretero, a single-use ureteroscope with high-definition imaging for urological procedures.

-

2025: In February 2025, Karl Storz unveiled the Slimline C-MAC S, a single-use video laryngoscope enhancing airway management in hospitals.

-

2025: In August 2025, Boston Scientific introduced Endura Weight Loss Solutions, including endoscopic sleeve gastroplasty and intragastric balloon procedures.

Disposable Endoscopes Market key players are:

-

Karl Storz GmbH & Co. KG

-

Pentax Medical (HOYA Corporation)

-

Fujifilm Holdings Corporation

-

Medtronic

-

Stryker Corporation

-

STERIS plc

-

Baxter International Inc.

-

Verathon Inc.

-

Richard Wolf GmbH

-

CooperSurgical Inc.

-

Coloplast A/S

-

Micro-Tech (Nanjing) Co., Ltd.

-

3NT Medical Ltd.

-

ScoutCam Inc.

-

OTU Medical Inc.

-

Innovex Medical Co.

-

Flexible Medical Systems Ltd.

Disposable Endoscopes Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.58 Billion |

| Market Size by 2035 | USD 10.47 Billion |

| CAGR | CAGR of 15.04% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Bronchoscopes, Urologic Endoscopes, Arthroscopes, Laparoscopes, Gastrointestinal Endoscopes, Others) • By Application (Pulmonology, Urology, Gastroenterology, Orthopedics, Gynecology, Others) • By End User (Hospitals, Ambulatory Surgical Centers, Specialty Clinics, Diagnostic Centers, Others) • By Distribution Channel (Direct Sales, Distributors, Online Platforms, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Ambu A/S, Boston Scientific Corporation, Karl Storz GmbH & Co. KG, Olympus Corporation, Pentax Medical (HOYA Corporation), Fujifilm Holdings Corporation, Medtronic, Stryker Corporation, STERIS plc, Baxter International Inc., Verathon Inc., Richard Wolf GmbH, CooperSurgical Inc., Coloplast A/S, Micro-Tech (Nanjing) Co., Ltd., 3NT Medical Ltd., ScoutCam Inc., OTU Medical Inc., Innovex Medical Co., Flexible Medical Systems Ltd. |

Frequently Asked Questions

North America, with a 38.45% share, driven by advanced healthcare infrastructure, high procedural volumes, and strong adoption of single-use devices.

Rising global hospital-acquired infections, increasing endoscopic procedure volumes, and a growing focus on infection-free patient care are the primary growth drivers.

The market was valued at USD 2.58 Billion in 2025 and is expected to reach USD 10.47 Billion by 2035.

The global Disposable Endoscopes Market is projected to grow at a CAGR of 15.04% from 2026 to 2035.

Asia-Pacific, projected to grow at a CAGR of 16.07%, supported by rising infection-control initiatives, expanding hospitals, and growing endoscopic procedure volumes.

Get in Touch