Endometriosis Treatment Market Report Scope & Overview:

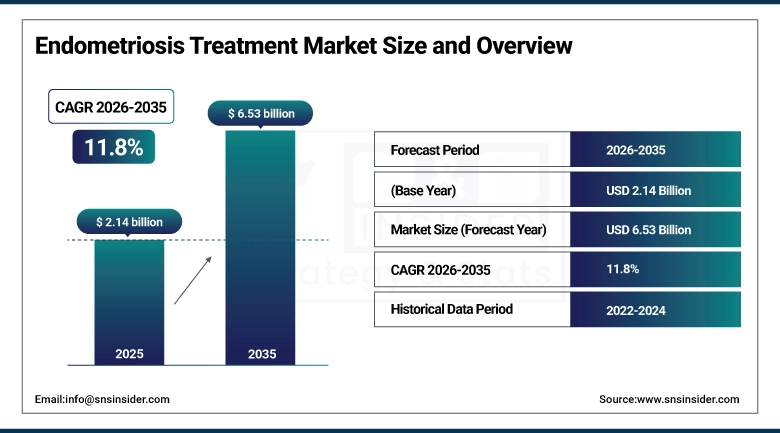

The Endometriosis Treatment Market size was estimated at USD 2.14 billion in 2025 and is expected to reach USD 6.53 billion by 2035 and grow at a CAGR of 11.8% over the forecast period of 2026-2035.

The global endometriosis treatment market is witnessing continuous growth owing to a high prevalence rate of this problem, increasing awareness on issues of women's reproductive health, and increasing demand for an efficient and effective solution of chronic pain problems. Increasing application of new-generation hormone-based treatment, non-invasive procedures, and improved medication delivery are becoming key factors in changing approaches to this issue in hospitals and ambulatory settings. All these factors are complemented by the persisting problem of chronic pelvic pain, late diagnostics, and improved medical infrastructure. Significant investments in research and development into novel and more effective treatment solutions are currently made by healthcare service providers and pharma companies.

For instance, in March 2024, a study published in the Journal of Minimally Invasive Gynecology reported that early adoption of hormone-based combination therapies led to a 78% reduction in symptom recurrence, highlighting growing clinical confidence in advanced treatment protocols.

Endometriosis Treatment Market Size and Forecast:

-

Market Size in 2025: USD 2.14 billion

-

Market Size by 2035: USD 6.53 billion

-

CAGR: 11.8% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Endometriosis Treatment Market - Request Free Sample Report

Endometriosis Treatment Market Trends

-

Rising preference for hormonal therapies and oral contraceptives as the initial therapy for treating pain and inhibiting disease progression among identified patients.

-

Minimally invasive laparoscopic approach is being adopted among gynecological care centers on a scale to enhance the diagnostic and treatment efficiency and decrease the recovery time.

-

Increasing research interest in potential non-hormonal and more targeted therapies to meet unmet clinical needs and reduce the adverse effects of long-term hormone use.

-

Increases synergy of additive treatment, drug regimen, and surgical approaches to optimize chronic disease management outcomes

-

More awareness campaigns and screening initiatives to promote early diagnosis and to allow timely intervention in women of reproductive age all over the world.

-

Increasing adoption of personalized therapeutics approaches enabled by concurrent developments in both biomolecular identification and individualized treatment planning.

-

Increased regulatory and clinical focus to improve women’s health outcomes, leading to innovation and availability of new endometriosis therapies.

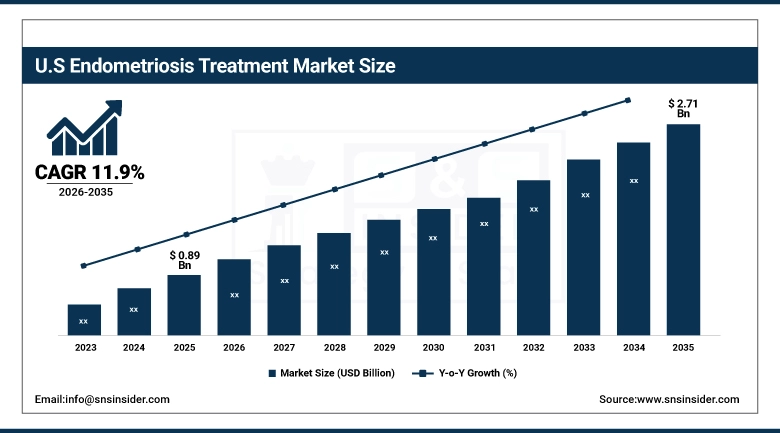

The U.S. Endometriosis Treatment Market Size was valued at USD 0.89 billion in 2025 and is predicted to reach USD 2.71 billion by 2035, growing at a CAGR of 11.9% during the forecast period 2026-2035. The United States dominates the global endometriosis treatment market, due to its advanced healthcare system, high level of endometriosis awareness and extensive funding in research related to women's health. Market growth is anticipated due to the presence of large pharmaceutical companies, high rate of diagnosis and increased minimally invasive surgeries. Additionally, supportive reimbursement policies, ongoing clinical trials, and advancements in hormonal and non-hormonal therapies are leading to higher adoption of treatment options.

Endometriosis Treatment Market Growth Drivers:

-

Rising Disease Awareness and Increasing Diagnosis Rates are Driving the Endometriosis Treatment Market Growth

Increased awareness about endometriosis as a chronic condition in women, along with advancements in diagnosis techniques and increased screenings, is aiding the growth of the market. Increased education efforts by healthcare professionals and support groups have been instrumental in diagnosing endometriosis early on and hence preventing under-diagnosis, which is one of the major concerns in the endometriosis field. Additionally, increased availability of better imaging technologies and less invasive diagnostic methods has made detection more accurate and enabled treatment for more number of people, thus increasing the demand for treatments in this market.

For instance, in March 2024, a global awareness initiative led by leading women’s health organizations resulted in a 22% increase in early-stage endometriosis diagnoses across participating healthcare networks, directly contributing to higher treatment adoption rates.

Endometriosis Treatment Market Restraints:

-

Limited Long-Term Treatment Efficacy and Side Effects are Hampering the Endometriosis Treatment Market Growth

The current therapeutic landscape for endometriosis includes mostly hormone therapy and pain relief drugs; however, their efficacy may be limited to the extent where these methods fail to produce significant outcomes. The re-emergence of symptoms post-treatment and issues related to fertility, hormone levels, and general health may become a hindrance to both patients' willingness to comply and the success of the process itself. In addition, individual reactions to treatment and the lack of a universal cure add up to the challenges of the issue. As a result, the utilization of existing therapies is restricted, which hampers the market development as a whole.

Endometriosis Treatment Market Opportunities:

-

Emergence of Novel Therapeutics and Personalized Treatment Approaches Unlock Significant Growth Opportunities for the Endometriosis Treatment Market

The endometriosis treatment market is expected to see favorable growth on the back of continued advancements in targeted therapies, the introduction of non-hormonal treatment options, and the move of personalized medicine into routine practice which is expected to continue market shake up in the near-future. Herein we summarize the need for such new therapies to meet the unmet needs for biologic therapeutics, selective progesterone receptor modulators and genetic approaches having increased efficacy with reduced side effects. Furthermore, incorporation of precision medicine practices is increasing patient response rates and satisfaction levels.

For instance, in July 2024, a leading pharmaceutical company reported that its investigational non-hormonal therapy demonstrated a 37% reduction in chronic pelvic pain during Phase II clinical trials, highlighting the potential of next-generation treatments in transforming endometriosis care.

Endometriosis Treatment Market Segment Analysis

-

By type, in 2025, hormone therapy and pain medications held the largest share with approximately 77.9% and is expected to grow at a CAGR of 9.6% over the forecast period, respectively.

-

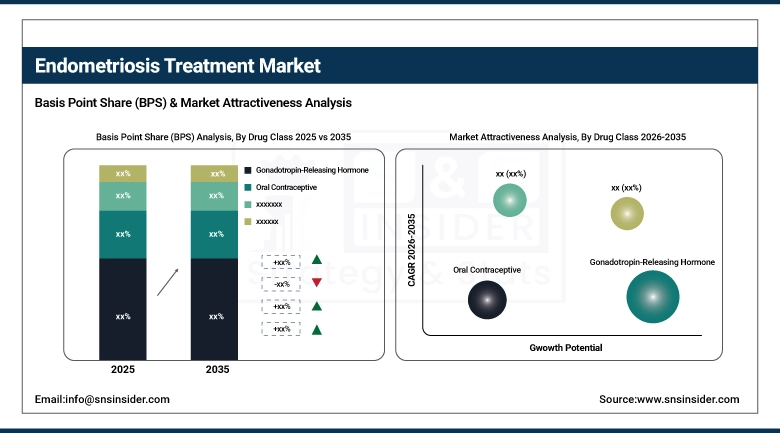

By drug class, gonadotropin-releasing hormone had the most share with nearly 50.0% in 2025, while growth of oral contraceptives is expected to maintain a steady pace at the rate of 11.1% CAGR.

-

By route of administration, the oral segment dominated the market in 2025, with a share of approximately 49.1%, and injectable route of administration is expected to grow at a CAGR of 12.2%

-

By distribution channel, retail pharmacies accounted for a share of roughly 52.3% in 2025, and are poised to grow at the fastest CAGR of 12.9% during the forecast period.

By Type, Hormone Therapy Leads the Market, While Pain Medication Maintains Steady Growth

Hormone therapy occupied the dominant position in the industry as of 2025, accounting for 77.9% of total revenues share. This dominance was attributed to the use of hormonal therapy to inhibit estrogen production and manage symptoms associated with endometriosis. It has been established that such therapy will stay at the center stage for a long time to come, as patients need management of symptoms, especially when suffering from the severe form of endometriosis. In its turn, pain medications accounted for only 22.1% of the revenues share generated in 2025; however, its CAGR for 2026–2035 was projected at 9.6%. NSAIDs and analgesics have been traditionally used for managing symptoms; they cannot help cure the disease and are not innovative.

By Drug Class, Gonadotropin-Releasing Hormone Dominates, While Oral Contraceptives Show Consistent Uptake

In 2025, the gonadotropin-releasing hormone segment held a share of 50.0%, due to its effectiveness in inhibiting hormone secretion from the ovaries while also decreasing the growth of lesions in cases of advanced endometriosis. Drugs in this component are usually administered in cycles due to their high efficacy. Oral contraceptives formed a market share of around 28.5% and were anticipated to record a CAGR of 11.1% during the forecast period owing to their easy access, low cost, and extensive usage in the treatment of early-stage endometriosis. NSAIDs held a market share of 15.9% in 2025 and continued to provide complementary treatment, whereas the others component, holding a market share of 5.6%, indicated new treatment approaches and combinations.

By Route of Administration, Oral Segment Leads, While Injectable Segment Gains Momentum

The oral route of administration was the leading mode of delivery, accounting for roughly 49.1% of the market share. This can be attributed to high patient acceptance of non-invasive and convenient delivery modes, as well as the prevalence of hormonal drugs and analgesics in oral form. injectable segment constituted 30.8% of the market and were forecasted to record a CAGR of 12.2% from 2026 to 2035, driven by an increasing demand for long-acting hormone treatments, which boost compliance and efficacy.

By Distribution Channel, Retail Pharmacies Dominate, While Hospital Pharmacies Maintain Strong Presence

The retail pharmacies category was dominant in the market share, accounting for around 52.3%. The retail pharmacies were attributed to the extensive market reach, convenience, and increased dispensation of medicines to patients with chronic ailments. Consumers tended to fill routine prescriptions at retail pharmacies for chronic diseases. In contrast, hospital pharmacies segment accounted for approximately 29.9% of the overall market size attributable to direct prescriptions by physicians and management of pronounced cases in a clinical setting. The others segment (17.8%), which includes online pharmacies and other non-traditional dispensers, would remain the largest and continue to grow. Finally, the retail pharmacies would witness the highest growth rate in the industry, estimated at 12.9%.

Endometriosis Treatment Market Regional Highlights:

North America Endometriosis Treatment Market Insights:

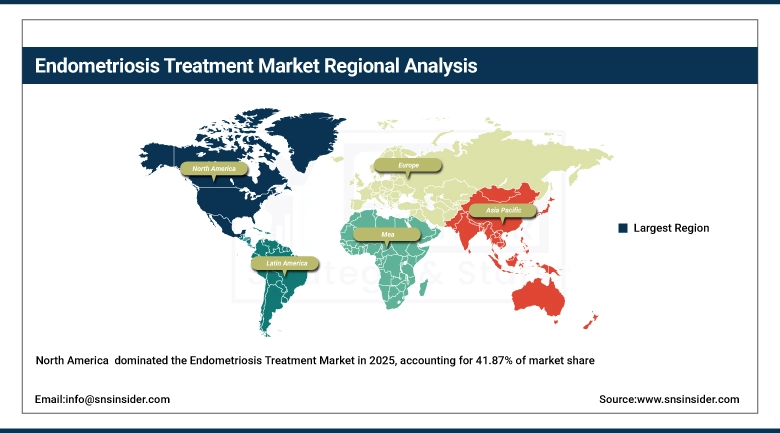

In 2025, North America accounted for 41.87% of the total revenue in global endometriosis treatment market. The region where North America is highly focused due to the best healthcare system, a high level of awareness regarding women's health, and better endometriosis diagnosis and treatment technologies lead to the high share of North America in the global market. The United States continues to lead the North America endometriosis market due to high diagnosis of endometriosis, availability of specialty gynecologists and availability of advanced hormonal therapies and analgesics. Market in North America is anticipated to continue dominating the global market share and revenue generation during the forecast years 2026 to 2035.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Endometriosis Treatment Market Insights:

Asia Pacific is the most lucrative region in the global endometriosis treatment market with a growth rate of 11.8%. In China, India, Japan, and South Korea, enhancements in medical services foundations, rising awareness regarding reproductive health problems, and government-initiated campaigns have propelled the growth of the market in the region. In addition, growth in healthcare infrastructure in these regions, increase in number of patients and better screening methods contribute to the growth of market. Advancements in treatment methods and increased spending on healthcare facilities has also fueled market growth.

Europe Endometriosis Treatment Market Insights:

Europe is currently the second-largest regional for endometriosis treatment, enabled by the existence of strong healthcare services for citizens, awareness initiatives, straightforward protocols for diagnosis and treatment of endometriosis. Germany, the UK, France, and Italy are among the key countries fueling growth in this regional market as they have stronger penetration of advanced treatment procedures as well as more patient empowerment initiatives. Clearly government funded healthcare, advances in diagnostic procedures, and the growing trend in minimally invasive procedures will drive market growth.

Latin America (LATAM) and Middle East & Africa (MEA) Endometriosis Treatment Market Insights:

The endometriosis treatment market is expanding slowly in Latin America and ME&A owing to improvements in health care infrastructure, increased awareness levels, and increased investments in women's health care services. Some of the major markets showing positive trends are Brazil, Mexico, United Arab Emirates, and Saudi Arabia owing to the growing availability of gynecology health care services. Increased spending on health care, coupled with increased training and patient education initiatives, is driving the market growth. The adoption of effective treatment solutions and health care reforms will contribute toward the future market growth until 2035.

Endometriosis Treatment Market Competitive Landscape:

AbbVie Inc. (est. 2013) is a global leader in biopharmaceutical innovation, offering a comprehensive portfolio of hormone therapies, GnRH modulators, and targeted treatments for chronic gynecological conditions. The company leverages its advanced R&D capabilities and proprietary drug platforms to deliver effective endometriosis management solutions across hospital, specialty clinic, and outpatient care settings worldwide.

-

In January 2025, AbbVie expanded the clinical application of its oral GnRH antagonist therapy with improved dosing flexibility and long-term symptom control, enabling better patient adherence and outcomes across North America and Europe.

Pfizer Inc. (est. 1849) is a diversified global pharmaceutical company with a dedicated women’s health portfolio providing hormone-based therapies, pain management drugs, and reproductive health solutions. Pfizer integrates its therapeutic offerings with clinical research and digital health platforms to deliver comprehensive disease management and treatment accessibility for endometriosis patients globally.

-

In June 2024, Pfizer introduced an enhanced hormone therapy regimen designed to reduce pelvic pain and inflammation, strengthening its presence in the women’s health therapeutics segment across developed and emerging markets.

Bayer AG (est. 1863) is a global provider of pharmaceutical and healthcare solutions, specializing in hormone therapies and reproductive health treatments. The company’s portfolio of oral contraceptives and hormonal agents serves major healthcare markets across Europe, North America, and Asia Pacific, combining clinical efficacy with improved patient safety and tolerability.

-

In October 2024, Bayer expanded its hormonal therapy portfolio for endometriosis treatment into Asia Pacific markets, collaborating with regional healthcare providers to enhance access to advanced therapeutic options across Japan and Australia.

Endometriosis Treatment Market Key Players:

-

AbbVie Inc.

-

Pfizer Inc.

-

Bayer AG

-

Takeda Pharmaceutical Company Limited

-

Novartis AG

-

AstraZeneca plc

-

Ferring Pharmaceuticals

-

Teva Pharmaceutical Industries Ltd.

-

GlaxoSmithKline plc

-

Merck & Co., Inc.

-

ObsEva SA

-

Theramex

-

Mylan N.V.

-

Amgen Inc.

-

Sanofi S.A.

-

Gedeon Richter Plc.

-

Lupin Limited

-

Zydus Lifesciences Ltd.

-

Dr. Reddy’s Laboratories Ltd.

-

Sun Pharmaceutical Industries Ltd.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.14 Billion |

| Market Size by 2035 | USD 6.53 Billion |

| CAGR | CAGR of 11.8% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Pain Medication, Hormone Therapy) • By Drug Class (NSAIDs, Oral Contraceptives, Gonadotropin-Releasing Hormone, and Others) • By Route of Administration (Oral, Injectable, and Others) • By Distribution Channel (Hospital pharmacy, Retail pharmacy, and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | AbbVie Inc., Pfizer Inc., Bayer AG, Takeda Pharmaceutical Company Limited, Novartis AG, AstraZeneca plc, Ferring Pharmaceuticals, Teva Pharmaceutical Industries Ltd., GlaxoSmithKline plc, Merck & Co., Inc., ObsEva SA, Theramex, Mylan N.V., Amgen Inc., Sanofi S.A., Gedeon Richter Plc., Lupin Limited, Zydus Lifesciences Ltd., Dr. Reddy’s Laboratories Ltd., Sun Pharmaceutical Industries Ltd. |

Frequently Asked Questions

Ans: The Endometriosis Treatment Market is projected to grow from USD 2.14 billion in 2025 to USD 6.53 billion by 2035, registering a CAGR of 11.8% during the forecast period of 2026 to 2035, driven by rising diagnosis rates and expanding treatment adoption.

Ans: The Endometriosis Treatment Market is primarily driven by increasing disease awareness, improved diagnostic capabilities, growing demand for hormonal therapies, and rising adoption of minimally invasive surgical procedures for long-term symptom management.

Ans: In the Endometriosis Treatment Market, hormone therapy dominates with a market share of approximately 77.9% in 2025, supported by its effectiveness in controlling disease progression and managing chronic pelvic pain.

Ans: North America leads the Endometriosis Treatment Market with over 41.87% share in 2025, attributed to advanced healthcare infrastructure, strong awareness, and high adoption of innovative treatment solutions.

Ans: Key trends in the Endometriosis Treatment Market include increasing use of combination therapies, growing focus on non-hormonal treatments, rising adoption of personalized medicine, and continuous advancements in drug development and delivery technologies.

Get in Touch