Field Communication Devices Market Report Scope & Overview:

The Field Communication Devices Market size was valued at USD 3.48 Billion in 2025E and is projected to reach USD 6.21 Billion by 2033, growing at a CAGR of 7.57% during 2026-2033.

The Field Communication Devices Market analysis highlights the growing demand for robust and reliable wired and wireless communication solutions in the industrial, oil & gas, chemicals, power generation sectors. Improved deployment of sophisticated field devices is being made possible through the proliferation of IoT-based and automated systems. HART and Modbus protocols are popular, with digital protocols and wireless products gaining ground quickly. Use of approved devices is promoted by regulation and standards like ISO, CE, RoHS. The long-term market growth is being driven by technological innovation and sustainability trends alongside digital connectivity.

By 2025, over 70% of new industrial field communication deployments will support IoT integration, enabling real-time monitoring and predictive maintenance in oil & gas and power plants.

Market Size and Forecast:

-

Market Size in 2025E: USD 3.48 Billion

-

Market Size by 2033: USD 6.21 Billion

-

CAGR: 7.57% from 2026 to 2033

-

Base Year: 2025

-

Forecast Period: 2026–2033

-

Historical Data: 2022–2024

To Get more information On Field Communication Devices Market - Request Free Sample Report

Field Communication Devices Market Trends

-

The shift from wired to wireless communication devices is accelerating due to IoT, remote monitoring, and cost-effective installation across industrial, chemical, and power generation sectors.

-

Integration of field devices with IoT and Industry 4.0 platforms enables real-time monitoring, predictive maintenance, and improved operational efficiency in process and discrete industries.

-

Digital protocols like Modbus, Foundation Fieldbus, and PROFIBUS are increasingly adopted over legacy HART systems, driving faster, more reliable communication and interoperability in industrial networks.

-

ISO, CE, and RoHS compliance requirements are driving the adoption of certified devices, ensuring safety, durability, and adherence to global industrial standards.

-

Rapid industrialization, energy infrastructure development, and smart factory initiatives in Asia-Pacific, LATAM, and MEA are fueling demand for wired and wireless field communication devices.

The U.S. Field Communication Devices Market size was valued at USD 0.67 Billion in 2025E and is projected to reach USD 1.24 Billion by 2033, growing at a CAGR of 8.01% during 2026-2033. Field Communication Devices Market growth is driven by increasing industrial automation, energy infrastructure and smart grid upgradation projects. Growing adoption of IoT-enabled devices leads to improved real-time tracking and operational efficiency. The expansion of oil and gas, chemicals, power generation industries drives the need for wired and wireless communication networks. Regulatory compliancy with ISO, CE and OSHA standards promotes the use of approved devices.

Field Communication Devices Market Growth Drivers:

-

Industrial Automation and IoT Integration Accelerate Demand for Field Communication Devices Market Globally

The Field Communication Devices Market growth is expanding due to Increasing automated industrial systems and IOT enabled solutions for real times monitoring, predictive maintenance and operational efficiency are majorly driving the growth of field communication devices market. Rising demand is also driven by power generation, oil & gas, chemicals and water treatment. Use of wireless and digital signals provides more freedom and less installation expense. ISO, CE and RoHS certification promote use of certified devices across industries in all parts of the world.

By 2025, over 75% of new predictive maintenance systems in oil & gas will rely on IoT-enabled field communication devices for real-time asset health monitoring.

Field Communication Devices Market Restraints:

-

High Installation Costs and Legacy System Dependencies Limit Market Expansion and Adoption Rates

Expensive installation and integration of new field communication devices becomes an obstacle in the case of small and medium enterprises. The existing wired technology in most of the industrial plants restricts replacement by the legacy systems. However, this can also be seen as a barrier, due to limited understanding of the long-term efficiency and return on investment (ROI) of their communication solutions. It's also the very high amounts of skilled labor needed and difficulties dealing with different regional regulations that are holding it back from wider use in some markets.

Field Communication Devices Market Opportunities:

-

Rising Wireless Deployment and Digital Protocol Adoption Present Growth Potential for Field Communication Devices

The Field Communication Devices Market is witnessing strong opportunities as advancements in wireless communication devices, IoT integration and higher-level digital protocols such as Modbus and Foundation Fieldbus. Developing APAC, LATAM and MEA are industrializing quickly and require more up to date equipment. Growth is also stimulated by smart factory initiatives and adoption of renewable energy infrastructure. Vendors targeting cost-effective, scalable, and green solutions can address new potential markets and increase penetration in wired and wireless communications.

By 2025, Asia-Pacific is projected to account for over 45% of global field communication device installations, driven by smart factory investments in China, India, and Southeast Asia.

Field Communication Devices Market Segment Analysis

-

By product, Wired Communication Devices led the market with a 60.35% share in 2025, while Wireless Communication Devices were the fastest-growing segment, registering a CAGR of 9.30%.

-

By application, Power Generation dominated with a 35.21% share in 2025, while the Chemicals segment was the fastest-growing with a CAGR of 8.10%.

-

By protocol, HART led the market with a 40.32% share in 2025, while Modbus was the fastest-growing protocol segment with a CAGR of 7.50%.

-

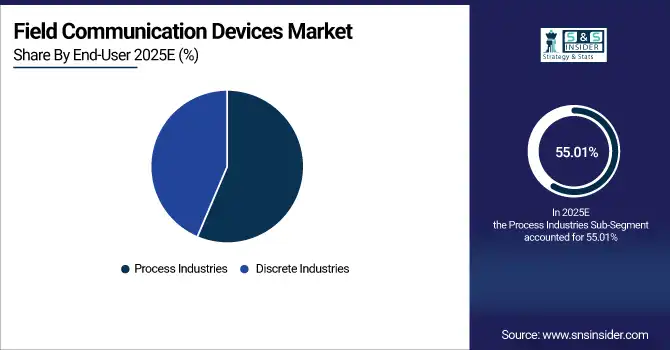

By end-user, Process Industries held a 55.01% share in 2025, while Discrete Industries were the fastest-growing segment with a CAGR of 6.50%.

By Product, Wired Communication Devices Leads Market While Wireless Communication Devices Registers Fastest Growth

By Product, Wired Communication Devices dominate the market on account of their reliability, established performance standards and widespread application in industrial and power generation. They are used with older systems and infrastructure that require constant data transfer. Wireless Communication Devices are growing the fastest, led by integration with IoT, remote monitoring capabilities, and lowered installation expenses. Manufacturers are now spending capital on state-of-the-art wireless technologies that enable security, performance and scale. The move towards Industry 4.0 & smart factories is driving wireless adoption.

By Application, Power Generation Dominate While Chemicals Shows Rapid Growth

On the basis of application, Power Generation holds the largest share of Field Communication Devices Market, driven by massive infrastructure projects and the demand for precise and real-time information in power generation utilities. Industrial automation, grid modernization and clean energy enablement create demand for wired and wireless secure devices. Chemicals is the fastest-growing application, on account of process automation, safety monitoring, and regulatory compliance needs. Rise in adoption of IoT-based devices and advanced protocols also boost the market growth.

By Protocol, HART Lead While Modbus Registers Fastest Growth

By Protocol, HART segment is dominate the market and widely deployed in legacy industrial networks, simple to integrate and proliferated worldwide as a standard. HART oriented devices are compatible with the installed base and provide dependable performance in process monitoring. The fastest-growing segment is Modbus, supported by digital transformation initiatives, smart factory adoption and IoT integration. Increasing need for better and faster communication and cross device compatibility is paving the way for Modbus.

By End-User, Process Industries Lead While Discrete Industries Grow Fastest

Based on End-User, Process Industries dominate the market, as their operations are continuous and need high reliable communication devices for safety, control & monitoring. These wired and wireless devices are widely used in industries such as oil & gas, power generation, and chemicals. Fastest growing end-user segment is Discrete Industries, due to modernization projects, automation and digital integration in automotive, electronics and manufacturing industries. Factors propelling the market include optimized productivity, IOT adoption and industry era 4.0 initiative

Field Communication Devices Market Regional Analysis:

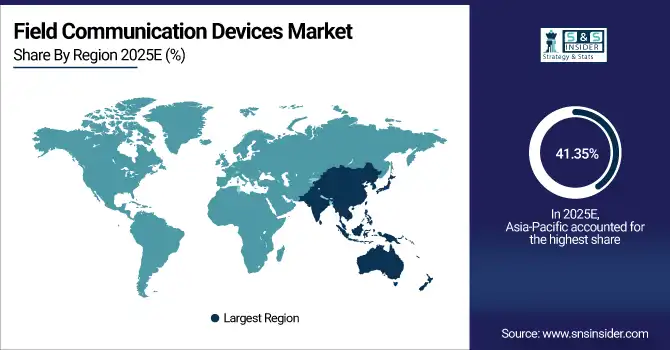

Asia-pacific Field Communication Devices Market Insights

In 2025 Asia-Pacific dominated the Field Communication Devices Market and accounted for 41.35% of revenue share, this leadership is due to the rapid industrialization and energy infrastructure development and increasing automation. Growing adoption of IoT based devices in manufacturing, chemicals and power generation is a key factor driving the demand. Countries such as China, India, Japan, and South Korea are expected to focus on smart factories and industrial automation with huge investments.

Get Customized Report as per Your Business Requirement - Enquiry Now

-

China Field Communication Devices Market Insights

China is one of the largest markets in Asia Pacific, due to its booming industrial sector, its projects and initiatives to make cities smart and adopt renewable energy. Deployment of digital procedures and wireless communication equipment is finally gaining denixityn chemical and power plants.

North America Field Communication Devices Market Insights

North America is expected to witness the fastest growth in the Field Communication Devices Market over 2026-2033, with a projected CAGR of 8.17% due to mature industrial field and majority of players are using automation technologies. Demand is led by the US in oil & gas, chemicals and power generation. The explosion of smart grids, renewable energy and data centers is fuelling the demand for a wide variety of wired and wireless transmission equipment. Market acceptance is enabled by compliance to regulations, standards and technological innovations.

-

U.S. Field Communication Devices Market Insights

The market in the U.S. is primarily influenced by the investments in industrial automation, smart grid, and energy infrastructure. There is a need for IoT connected and wireless field level devices to drive operational. Certification driven solutions are also seen globally, thanks to regulatory pressures (e.g. OSHA, ISO or CE regulations), which push the demand for certified solutions.

Europe Field Communication Devices Market Insights

In 2025, Europe is a developed market with consistent demand in industrial, power generation and chemical industries. Germany leads the region with its advanced production, infrastructure initiatives and use of sustainable energy. Quality standards such as CE, ISO and RoHS certified encourage the use of approved devices. Industrial automation, IoT adoption and smart factory projects are the major drivers. Market expansion is reinforced also by technological improvements and ecological concerns.

-

Germany Field Communication Devices Market Insights

Germany has stronger industrial and energy sectors for given a lead to the Europe Field Communication Devices Market. Automation, smart factories and regulatory issues fuel wire and wireless adoption. Strong industry focus on Industry 4.0 and renewable energy projects adds to demand.

Latin America (LATAM) and Middle East & Africa (MEA) Field Communication Devices Market Insights

The Field Communication Devices Market is experiencing moderate growth in the Latin America (LATAM) and Middle East & Africa (MEA) regions, due to the industrialization, development of energy infrastructure and automation programmes. An increasing demand for field communication devices is driven by oil & gas, chemicals, and power generation sectors. There is increased regulation and standardization in place everywhere. Growing IoT is driving the market, due to infrastructure investment and smart industrial projects.

Field Communication Devices Market Competitive Landscape:

Siemens AG is a global powerhouse in industrial automation and Field Communication Devices (FDCs), providing wired FDC solutions, such as HART, PROFIBUS and Modbus. Its equipment is employed in power generation, oil & gas, chemicals and the discrete industries. Siemens also focuses on integration of the IoT, smart factory solutions, and ensuring that goods being delivered for production are secure according to regulation and reliable in communication.

-

In November 2024, Siemens announced the launch of the Simatic RF18xC series communication modules, enhancing RFID cloud connectivity with compact, IP67-rated devices suitable for harsh industrial environments.

ABB Ltd offers a wide variety of advanced field communication devices designed for both process and discrete industry applications. Comprising wired and wireless offering communicating via HART, Modbus and Foundation Fieldbus Protocol. It operates in the industrial automation, energy infrastructure and IoT-based monitoring space through its products. ABB guarantees high reliability, global standards and easy integration in its digital industrial environment.

-

In July 2025, ABB released the P-300 All-Rounder pressure transmitter, part of its new P-series, offering enhanced performance for various industrial applications. The P-300 features advanced digital communication options, higher accuracy, and reduced maintenance requirements, targeting chemical, oil & gas, and power generation industries.

The Emerson Electric Co. provides high performance field communicators for industrial automation, including wired and wireless HART and Modbus and FOUNDATION Fieldbus devices. Its offerings improve the monitoring of real-time, predictive maintenance and operations. With a focus on safety, reliability, drive for continuous improvement and performance monitoring Emerson serves the power generation oil & gas chemical and manufacturing sectors world-wide.

-

In November 2024: Emerson proposed to acquire the remaining shares of AspenTech for $15.1 billion, aiming to sharpen its focus on industrial automation. The acquisition is expected to strengthen Emerson’s software and analytics capabilities, enabling improved predictive maintenance and operational efficiency for customers globally.

Schneider Electric SE provides wired and wireless communication products for use in industrial, energy, and automation markets. Supporting HART, Modbus and PROFIBUS communication protocols Schneider is also sharply focused on smart grid, process automation as well as IoT-enabled operations. The company is focused on energy efficiency, emissions reduction, use of alternative energy sources and methodical refurbishment and the integration of digital industrial projects to increase operational control.

-

In July 2025, Schneider Electric announced the acquisition of the remaining 35% stake in its Indian joint venture from Temasek for €5.5 billion ($6.4 billion) in cash, aiming to accelerate decision-making and enhance its strategic focus on India.

Field Communication Devices Market Key Players:

Some of the Field Communication Devices Market Companies are:

-

Siemens AG

-

ABB Ltd.

-

Emerson Electric Co.

-

Schneider Electric SE

-

Rockwell Automation, Inc.

-

Honeywell International Inc.

-

Yokogawa Electric Corporation

-

Endress+Hauser Group

-

General Electric Company

-

Mitsubishi Electric Corporation

-

Omron Corporation

-

Phoenix Contact GmbH & Co. KG

-

Pepperl+Fuchs SE

-

Moxa Inc.

-

Advantech Co., Ltd.

-

Belden Inc.

-

Banner Engineering Corp.

-

National Instruments Corporation

-

Hitachi, Ltd.

-

WAGO Kontakttechnik GmbH & Co. KG

| Report Attributes | Details |

|---|---|

| Market Size in 2025E | USD 3.48 Billion |

| Market Size by 2033 | USD 6.21 Billion |

| CAGR | CAGR of 7.57% From 2026 to 2033 |

| Base Year | 2025E |

| Forecast Period | 2026-2033 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Wired Communication Devices, Wireless Communication Devices) • By Application (Oil & Gas, Chemicals, Water & Wastewater, Power Generation, Pharmaceuticals, Food & Beverages, and Others) • By Protocol (HART, PROFIBUS, Modbus, Foundation Fieldbus, and Others) • By End-User (Process Industries, Discrete Industries) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Siemens AG, ABB Ltd., Emerson Electric Co., Schneider Electric SE, Rockwell Automation, Inc., Honeywell International Inc., Yokogawa Electric Corporation, Endress+Hauser Group, General Electric Company, Mitsubishi Electric Corporation, Omron Corporation, Phoenix Contact GmbH & Co. KG, Pepperl+Fuchs SE, Moxa Inc., Advantech Co., Ltd., Belden Inc., Banner Engineering Corp., National Instruments Corporation, Hitachi, Ltd., WAGO Kontakttechnik GmbH & Co. KG |

Frequently Asked Questions

Asia-Pacific dominated the Field Communication Devices Market in 2025.

The Wired Communication Devices segment dominated during the projected period.

Growth is driven by rising adoption of industrial automation, IoT integration, and digital communication across process and discrete industries.

The market was valued at USD 3.48 Billion in 2025E and is projected to reach USD 6.21 Billion by 2033.

The Field Communication Devices Market is expected to grow at a CAGR of 7.57% during 2026–2033.

Get in Touch