Fluorescent In Situ Hybridization Probe Market Report Scope & Overview:

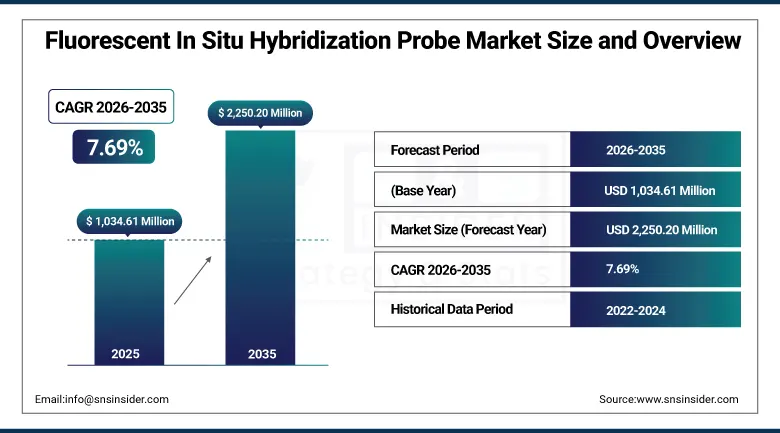

The Fluorescent In Situ Hybridization Probe Market was valued at USD 1,034.61 Million in 2025 and is expected to reach USD 2,250.20 Million by 2035, growing at a CAGR of 7.69% from 2026 to 2035.

The Fluorescent In Situ Hybridization (FISH) Probe Market is growing due to the rise in incidences of cancer and genetic disorders, resulting in the need for precise molecular diagnostic products. Growing adoption of personalized medicines, increasing applications in companion diagnostics, and innovations in genomics research are fueling market growth. The advent of technology in probe development, automation, and imaging equipment is increasing testing accuracy and efficiency. Moreover, rising investments in precision oncology, rising research activities, and expanding healthcare infrastructure in developing countries are promoting the use of FISH probes.

According to the World Health Organization (WHO), approximately 20 million new cancer cases and 9.7 million cancer deaths were recorded globally in 2022, significantly increasing the demand for molecular diagnostic techniques such as Fluorescent In Situ Hybridization (FISH) for cancer detection and treatment selection. Furthermore, the International Agency for Research on Cancer (IARC) projects that the annual number of new cancer cases will exceed 35 million by 2050, representing a 77% increase compared with 2022 levels, reinforcing the long-term demand for advanced FISH probe technologies.

Market Size and Forecast:

-

Market Size in 2025: USD 1,034.61 Million

-

Market Size in 2026E: USD 1,114.18 Million

-

Market Size by 2035: USD 2,250.20 Million

-

CAGR: 7.69% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Fluorescent In Situ Hybridization Probe Market - Request Free Sample Report

Fluorescent In Situ Hybridization Probe Market Trends

-

Rising prevalence of genetic disorders and cancer driving demand for fluorescent in situ hybridization (FISH) probes for accurate molecular diagnostics

-

Growing adoption of personalized medicine increasing the use of FISH-based testing for biomarker identification and targeted therapy selection

-

Increasing application of FISH probes in prenatal testing, cytogenetics, and oncology research supporting early disease detection and genetic analysis

-

Expanding investments in molecular diagnostics and genomic research accelerating the development of advanced, high-specificity FISH probe technologies

-

Continuous advancements in probe design, fluorescence labeling, and automated imaging systems enhancing diagnostic accuracy, sensitivity, and laboratory efficiency

The U.S. Fluorescent In Situ Hybridization Probe Market Outlook:

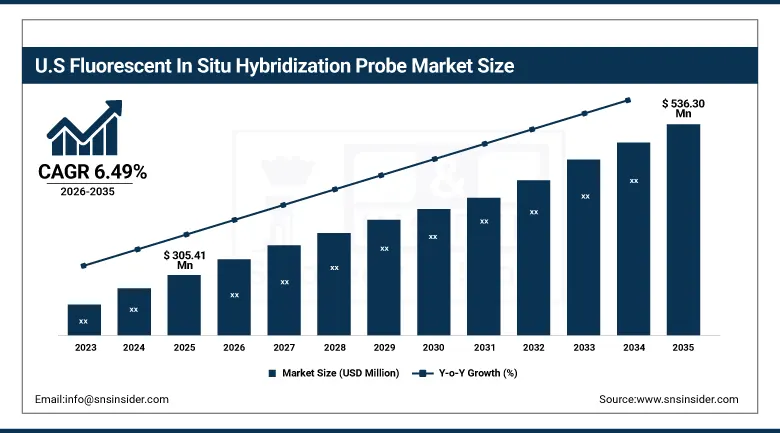

The U.S. Fluorescent In Situ Hybridization Probe Market was valued at approximately USD 305.41 Million in 2025 and is expected to reach approximately USD 536.30 Million by 2035, growing at a CAGR of approximately 6.49%.

In the U.S., the FISH probe market is expanding as a result of rising investments in the field of precision medicine, rising funds from the NIH for research on genetics, and regulatory measures aimed at speeding up the approval of diagnostic products. The FISH probe market in the United States is heavily driven by the FDA approval of FISH companion diagnostics, as this approval makes it mandatory to conduct FISH testing for targeted therapies.

This regulatory backing ensures sustained demand, fuelling consistent market growth and strengthening overall national market growth, with the American Cancer Society reporting that over 2 million new cancer cases were expected in the U.S. in 2025 excluding non-melanoma skin cancers, illustrating the large and growing oncology patient pool that drives FISH testing demand.

Fluorescent In Situ Hybridization Probe Market Segment Analysis:

-

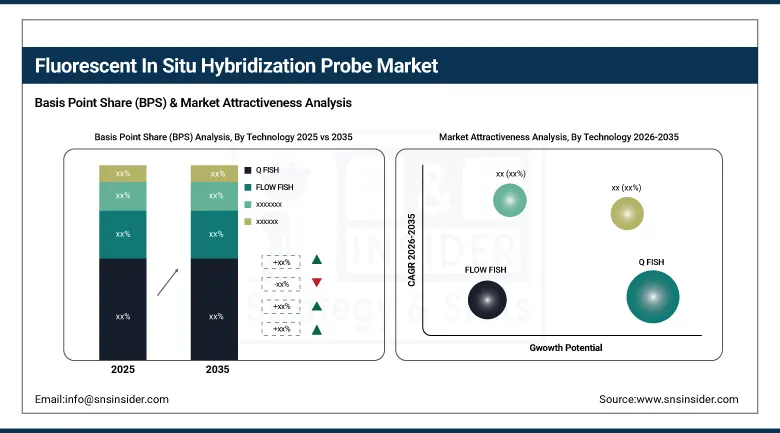

By Technology, Q FISH segment dominated the Fluorescent In Situ Hybridization Probe Market in 2025 with 58% share; FLOW FISH segment is the fastest growing segment.

-

By Type, DNA segment dominated the market in 2025 with 76% share; RNA segment is the fastest growing segment.

-

By Application, Cancer Research segment dominated the market in 2025 with 64% share; Genetic Diseases segment is the fastest growing segment.

-

By End-Use, Clinical segment dominated the market in 2025 with 49% share; Companion Diagnostics segment is the fastest growing segment.

By Technology, Q FISH segment dominates the Fluorescent In Situ Hybridization Probe Market, FLOW FISH segment expected to grow fastest

The Q FISH segment dominated the Fluorescent In Situ Hybridization Probe Market in 2025 with a 58% share as it is highly accurate for the detection of chromosomes and telomeres in quantitative manner. This technique is widely applied in diagnostics of cancer, cytogenetic applications, and clinical research laboratories as it provides accurate visualization of the chromosomal abnormalities and genetic changes. Rising need for efficient molecular diagnostics methods along with rising application in oncology research and personalized medicine is propelling the growth of the Q FISH segment.

The FLOW FISH segment is the fastest growing as it allows combining the use of flow cytometry and fluorescence in situ hybridization techniques in order to achieve fast and efficient cellular analysis. FLOW FISH provides enhanced sensitivity and reproducibility in the detection of the telomere length and immune cells. Rising need for advanced cell based tests and genetic analysis is leading to the growing acceptance of the FLOW FISH technique.

By Type, DNA segment dominates the Fluorescent In Situ Hybridization Probe Market, RNA segment expected to grow fastest

The DNA segment dominated the market in 2025 with a 76% share owing to its widespread applications in identifying chromosomal aberrations, gene amplification, gene deletion and other structural variations. DNA FISH probes have found a lot of popularity in fields like oncology, prenatal diagnosis and cytogenetics since they are extremely accurate in providing genetic data. Increased incidences of cancer and genetic disorders and increasing molecular diagnostics applications will keep this segment leading the market.

The RNA segment is the fastest growing because of increasing interest in gene expression studies and transcript-level molecular diagnostics. RNA FISH allows for visualization of RNA molecules within individual cells and is increasingly being used for advanced studies related to oncology, infectious disease and developmental biology. Increasing applications of single cell analysis and biomarker discovery are driving up the demand for RNA FISH probes.

By Application, Cancer Research segment dominates the Fluorescent In Situ Hybridization Probe Market, Genetic Diseases segment expected to grow fastest

The Cancer Research segment dominated the market in 2025 with a 64% share due to the extensive use of FISH probes in detecting chromosomal abnormalities, gene rearrangements, and cancer biomarkers. This technique aids in the diagnosis, prognosis, and treatment of tumor types. Factors such as the increase in the global prevalence of cancer, increased research into oncology, and the growth of precision medicine are propelling the dominance of the segment.

The Genetic Diseases segment is the fastest growing due to the rising demand for the detection of genetic chromosomal abnormalities and rare genetic diseases. FISH probes help in the fast detection of gene deletions, duplications, and translocation. Growth drivers include expanded newborn screening programs, awareness about genetic testing, and advances in molecular diagnostics.

By End-Use, Clinical segment dominates the Fluorescent In Situ Hybridization Probe Market, Companion Diagnostics segment expected to grow fastest

The Clinical segment dominated the market in 2025 with a 49% share due to the heavy usage of FISH Probes for disease diagnosis and therapy in hospitals, diagnostic laboratories, and pathology centers. This technique is commonly used in oncology, prenatal testing, and cytogenetics because of its high accuracy and specificity. Increasing requirements for accurate diagnosis and individualized treatment methods will continue fueling market dominance of this segment.

The Companion Diagnostics segment is the fastest growing driven by an increasing preference for targeted therapies and individualized medicines. FISH Probes are important for determining specific genetic markers and hence patient suitability for precise treatments in oncology. Growing regulatory clearances of such targeted therapies, increasing pharmaceutical research, and collaboration of diagnostic companies with drug manufacturing companies will drive demand for companion diagnostics.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.47% |

|

Europe |

Germany |

28.47% |

|

Asia Pacific |

China |

38.47% |

|

Middle East & Africa |

UAE |

22.84% |

|

Latin America |

Brazil |

43.84% |

North America Fluorescent In Situ Hybridization Probe Market Insights

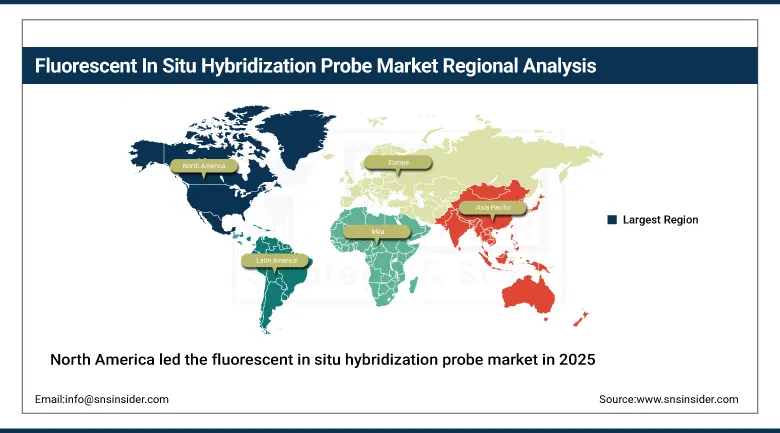

North America led the fluorescent in situ hybridization probe market in 2025, powered by strong adoption of precision medicine, robust research funding, and top-ranked biomedical research institutions whose clinical and research infrastructure sustains consistent FISH probe demand. North America leads the market, powered by precision medicine initiatives, strong reimbursement frameworks, and robust research infrastructure, with the United States accounting for approximately 82.47% of regional revenue through high cancer prevalence and advanced genetic testing adoption.

According to the Centers for Disease Control and Prevention (CDC), cancer remains the second leading cause of death in the United States, underscoring the continued need for advanced molecular diagnostic technologies such as Fluorescent In Situ Hybridization (FISH) for early detection and precision treatment. Additionally, the National Institutes of Health (NIH) invested more than USD 8 billion in cancer research during FY2024, supporting innovations in molecular diagnostics, genomic medicine, and precision oncology that are driving the adoption of FISH probe technologies.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Fluorescent In Situ Hybridization Probe Market Insights

Europe held a significant share of global Fluorescent In Situ Hybridization Probe revenues, with Germany favourable to FISH probe adoption due to the high presence of pharmaceutical and biotechnology industry, reinforced by intense regulations of its healthcare sector insisting on accurate diagnostics. Germany accounts for approximately 28.47% of European revenues through companies including Agilent Technologies and QIAGEN that have large market share and include a wide selection of FISH probes used in oncology and screening of genetic disorders.

According to the European Commission, Europe's Beating Cancer Plan mobilizes €4 billion to strengthen cancer prevention, diagnosis, treatment, and research, supporting the adoption of advanced molecular diagnostic technologies such as Fluorescent In Situ Hybridization (FISH). Additionally, according to the European Society for Medical Oncology (ESMO), approximately 2.7 million new cancer cases are diagnosed annually across Europe, driving the demand for accurate genomic and cytogenetic testing to enable early diagnosis and personalized treatment strategies.

Asia Pacific Fluorescent In Situ Hybridization Probe Market Insights

Asia Pacific is the fastest-growing region with a CAGR of 8.56% during the forecast timeframe, reflecting rising healthcare spending, improved diagnostic capabilities, and government-backed genomic research across the region. India, China, and Japan are key growth engines due to expanding molecular pathology labs and increased awareness of personalised medicine, with China accounting for approximately 38.47% of Asia Pacific revenues through its growing R&D efforts and robust government interest in molecular diagnostics.

According to the World Health Organization (WHO), Asia accounts for nearly 50% of global cancer cases, creating substantial demand for advanced molecular diagnostic technologies, including Fluorescent In Situ Hybridization (FISH). Additionally, China's National Health Commission (NHC) reports that the country records more than 4 million new cancer cases annually, making it one of the world's largest oncology diagnostic markets.

Furthermore, according to the Indian Council of Medical Research (ICMR), India reports approximately 1.5 million new cancer cases annually, with increasing investments in genomic diagnostics and precision medicine further supporting the adoption of FISH probe technologies.

MEA & Latin America Fluorescent In Situ Hybridization Probe Market Insights

Middle East and Latin America are growing Fluorescent In Situ Hybridization Probe markets where expanding healthcare infrastructure, growing cancer diagnostic capacity, and rising genetic testing awareness are creating increasing commercial demand. The UAE leads MEA revenues at approximately 22.84% of the regional total through its growing investment in advanced diagnostic infrastructure and expanding precision oncology capability across its healthcare system. Brazil leads Latin American revenues at approximately 43.84% of the regional total through its expanding cancer diagnostic capacity, growing molecular pathology laboratory network, and increasing adoption of precision medicine practices across its healthcare system.

Market Dynamics:

Drivers: Rising cancer prevalence and precision medicine adoption drive FISH probe market growth.

The growing use of precision medicine and the rising incidence of cancer around the world are key factors contributing to the growth of the fluorescent in situ hybridization probe market, which will witness more than 19.3 million cancer cases diagnosed globally in 2023, driving the need for early and accurate diagnoses that increasingly rely on the detection of chromosomal abnormalities via the use of FISH. The application of FISH probes enables the detection of chromosomal abnormalities and helps oncologists design personalized treatments whose usage is increasingly being driven by an expanded list of FDA approved targeted cancer drugs requiring FISH biomarker validation prior to the start of treatment.

Restraints: High testing costs and skilled workforce shortages limit FISH probe adoption.

Increasing utilization of precision medicine and increasing prevalence of cancer worldwide are two important drivers for the market growth of the fluorescent in situ hybridization probe market due to the expected occurrence of more than 19.3 million cancer patients worldwide in 2023, which will make early diagnosis of cancer imperative through the use of FISH probes that detect chromosomal abnormalities, thus helping oncologists develop personalized treatments. The usage of the FISH probes in developing personalized treatments is increasingly becoming a necessity due to a larger list of FDA-approved targeted cancer medicines, whose efficacy depends on FISH biomarkers validation before treatment commences.

Opportunities: Multiplex FISH innovations and AI image analysis create significant market opportunities.

Development of multiplex FISH probes, automation of hybridization methods, and use of AI for image analysis are key innovations in the technology space that are being commercially developed to make FISH testing more efficient and solve the laborious problems associated with traditional FISH testing that have made large-scale deployment problematic. Each time a multiplex probe can be developed to simultaneously test for several genetic targets in one test lowers the per patient sample and reagents needed along with increasing information density, adding value to the products that can command a higher price than traditional single target FISH probes.

Recent Developments:

-

2025: Cynvenio Biosystems launched its CLEAR Liquid Biopsy FISH Panel, designed to detect multiple chromosomal abnormalities in circulating tumour cells through minimally invasive blood-based testing, expanding FISH accessibility for patients with challenging biopsy access.

-

2023: Oxford Gene Technology, a Sysmex Corporation company, announced that eight of its CytoCell FISH probes had been certified for clinical use in line with Europe's In Vitro Diagnostics Regulation, expanding regulatory-compliant FISH probe availability across European clinical laboratories.

-

2023: Agilent Technologies expanded its portfolio of SureFISH probes, aiming to create the largest offering of oligonucleotide-based fluorescent in situ hybridization assays on the market for oncology research and genetic disorder screening applications.

Fluorescent In Situ Hybridization Probe Market Key Players are:

-

Abbott Laboratories

-

Agilent Technologies, Inc.

-

F. Hoffmann-La Roche Ltd.

-

Thermo Fisher Scientific Inc.

-

Revvity, Inc. (PerkinElmer)

-

Bio-Techne Corporation (Advanced Cell Diagnostics)

-

Oxford Gene Technology (Sysmex Corporation)

-

MetaSystems Hard & Software GmbH

-

Leica Biosystems (Danaher Corporation)

-

Empire Genomics, LLC

-

Cytocell Ltd. (Oxford Gene Technology)

-

ZytoVision GmbH

-

Creative Bioarray

-

Genemed Biotechnologies, Inc.

-

Biocare Medical, LLC

-

Kreatech Diagnostics (Leica Biosystems)

-

Applied Spectral Imaging (ASI)

-

Empire Genomics Europe Ltd.

-

Molecular Instruments, Inc.

-

BioView Ltd.

Fluorescent In Situ Hybridization Probe Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1,034.61 Million |

| Market Size by 2035 | USD 2,250.20 Million |

| CAGR | CAGR of 7.69% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology [Q FISH, FLOW FISH, Others] • By Type [DNA, RNA] • By Application [Cancer Research, Genetic Diseases, Other] • By End-Use [Research, Clinical, Companion Diagnostics] |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Abbott Laboratories, Agilent Technologies, Inc., F. Hoffmann-La Roche Ltd., Thermo Fisher Scientific Inc., Revvity, Inc. (PerkinElmer), Bio-Techne Corporation (Advanced Cell Diagnostics), Oxford Gene Technology (Sysmex Corporation), MetaSystems Hard & Software GmbH, Leica Biosystems (Danaher Corporation), Empire Genomics, LLC, Cytocell Ltd. (Oxford Gene Technology), ZytoVision GmbH, Creative Bioarray, Genemed Biotechnologies, Inc., Biocare Medical, LLC, Kreatech Diagnostics (Leica Biosystems), Applied Spectral Imaging (ASI), Empire Genomics Europe Ltd., Molecular Instruments, Inc., BioView Ltd. |

Frequently Asked Questions

The Fluorescent In Situ Hybridization Probe Market is expected to grow at a CAGR of 7.69% from 2026 to 2035.

The Fluorescent In Situ Hybridization Probe Market was valued at USD 1,034.61 Million in 2025.

Rising cancer cases, precision medicine adoption, AI-enabled FISH technologies, companion diagnostics, and biomarker collaborations are driving market growth globally.

The DNA probes segment dominated the Fluorescent In Situ Hybridization Probe Market.

North America dominated the Fluorescent In Situ Hybridization Probe Market in 2025.

Get in Touch