Front-of-the-Meter Battery Market Report Scope & Overview:

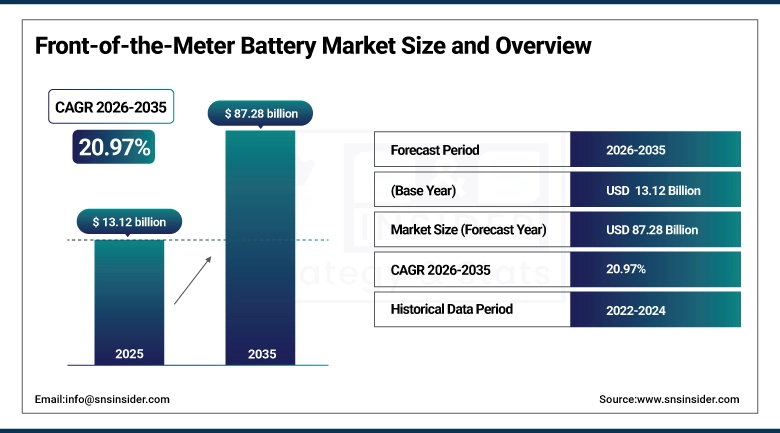

The Front-of-the-Meter Battery Market was valued at USD 13.12 billion in 2025 and is expected to reach USD 87.28 billion by 2035, growing at a CAGR of 20.97% from 2026-2035.

The Front of the Meter Battery Market is growing with the increasing trend of the usage of renewable energy resources, the increasing trend of the usage of electricity, and the need to ensure the reliability of the grid. The government is also supporting the growth of the Front of the Meter Battery Market. Technological advancements in energy storage solutions and the reduction in the prices of batteries are also boosting the growth of the Front of the Meter Battery Market. Utilities and third parties are investing in large-scale battery storage solutions.

The growth in the Front-of-the-Meter Battery Market is also seen in the United States, where the utility-scale battery storage capacity increased to over 26 GW in 2024 after the installation of approximately 10.4 GW of new battery storage. This is the second-highest increase in utility-scale battery storage after solar energy in the United States.

In Europe, approximately 4.9 GW or 12.1 GWh of utility-scale battery storage capacity was added in 2024. This increased the overall grid-connected storage capacity to over 13 GW.

Front-of-the-Meter Battery Market Size and Forecast

-

Market Size in 2025: USD 13.12 Billion

-

Market Size by 2035: USD 87.28 Billion

-

CAGR: 20.97% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Front-of-the-Meter Battery Market - Request Free Sample Report

Front-of-the-Meter Battery Market Trends

-

Rising demand for grid-scale energy storage to balance renewable generation is driving the front-of-the-meter (FTM) battery market.

-

Growing adoption across utility, industrial, and microgrid applications is boosting market growth.

-

Expansion of solar and wind energy integration is fueling deployment of large-scale battery systems.

-

Increasing focus on peak load management, frequency regulation, and grid reliability is shaping adoption trends.

-

Advancements in lithium-ion, flow, and solid-state battery technologies are enhancing performance and lifespan.

-

Rising investments in clean energy infrastructure and decarbonization initiatives are supporting market expansion.

-

Collaborations between utilities, battery manufacturers, and technology providers are accelerating innovation and global adoption.

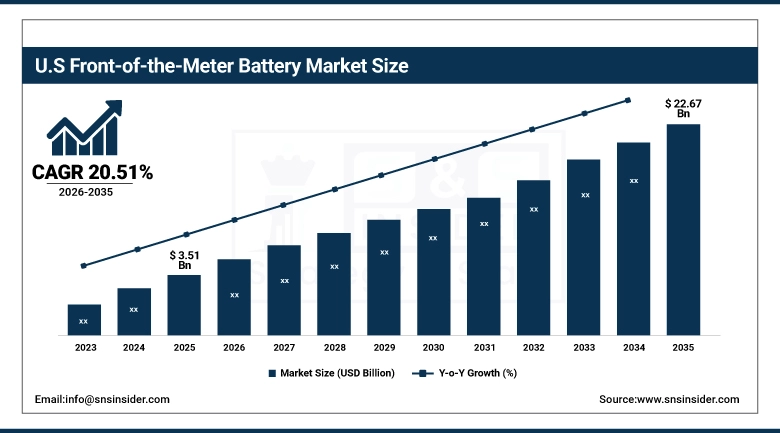

U.S. Front-of-the-Meter Battery Market Size Outlook:

The U.S. Front-of-the-Meter Battery Market was valued at USD 3.51 billion in 2025 and is expected to reach USD 22.67 billion by 2035, growing at a CAGR of 20.51% from 2026-2035. The US Front of the Meter Battery market is increasing due to factors such as renewable energy integration, government incentives, grid modernization, and increasing electricity demand.

Front-of-the-Meter Battery Market Growth Drivers:

-

Increasing need for grid stability and energy reliability is driving Front-of-the-Meter battery market expansion globally

The rising need to use more electricity, as well as the complexity involved in managing it, has led to a real-time solution to manage the grid. This has been achieved through the use of batteries, which provide regulation in terms of frequency, voltage, as well as managing peak loads to avoid blackouts. This technology has ensured the reliability of the grid, which has enabled the efficient supply of electricity to meet the needs of those who require it. The rising need to use more energy, as well as the effects of urbanization and industrialization, has led to the use of FTM batteries as a technology to manage the grid effectively.

According to the United States Energy Information Administration, the use of batteries in the grid can offer several services, including capacity reserves, energy arbitrage, as well as ancillary services, which help ensure the stability of the grid.

At the end of 2023, the utilities in the United States were operating 15,814 MW (~15.8 GW) of capacity, which was connected to the grid, with a significant amount used in the management of the grid, including the regulation of frequency, load management, as well as peak shaving, thereby playing a frontline role in the management of the grid.

Front-of-the-Meter Battery Market Restraints:

-

Limited availability of raw materials for battery manufacturing is restraining the growth of Front-of-the-Meter storage systems

Materials such as lithium, cobalt, and nickel that are critical for the production of high-performance batteries face scarcity due to geopolitical challenges and mining difficulties. This scarcity affects the cost and time required for the production of the final product. Furthermore, the recycling technology is still in its infancy and cannot be relied upon to mitigate the scarcity of critical raw materials. Moreover, environmental regulations for mining and sourcing critical raw materials add to the complexities in the production process. This makes the supply chain for energy storage solutions unpredictable in terms of cost and availability. This scarcity is still hindering the large-scale implementation of Front-of-the-Meter battery technology worldwide.

Front-of-the-Meter Battery Market Opportunities:

-

Integration of advanced battery technologies presents significant growth opportunities in Front-of-the-Meter energy storage

New battery technologies, such as solid-state batteries, flow batteries, and hybrid battery technology, promise greater efficiency, longer battery life, and greater energy density. This provides an opportunity to implement FTM battery technology in various applications, including grid stabilization, renewable energy integration, and peak shaving. Energy storage companies can use R&D to create cost-effective solutions to meet growing needs in the utility sector and industries. An expansion of smart grid infrastructure in global markets also provides an opportunity to use FTM battery technology. Companies that innovate in technology development can gain a greater share of the market, making it a lucrative opportunity in the energy storage sector to integrate FTM battery technology into the global market.

|

Project Name |

Grid Integration Role |

|

Victorian Big Battery (Australia) |

Provides large-scale grid reliability support, frequency regulation, and renewable energy integration, helping stabilize peak demand and reduce system costs. |

|

Gannawarra Energy Storage System (Australia) |

Stores excess solar generation and supplies power to the grid, supporting renewable balancing, frequency regulation, and flexible grid operations. |

|

Ballarat Energy Storage System (Australia) |

Enhances grid stability by smoothing renewable energy fluctuations, improving voltage control, and supporting local network reliability. |

|

Dalrymple ESCRI Battery (Australia) |

Delivers critical grid stability services, including frequency control ancillary services (FCAS), while enabling higher renewable energy penetration. |

Front-of-the-Meter Battery Market Segment Highlights

-

By Application, Grid Services dominated the Front-of-the-Meter Battery Market with ~31% share in 2025; Renewable Integration fastest growing (CAGR).

-

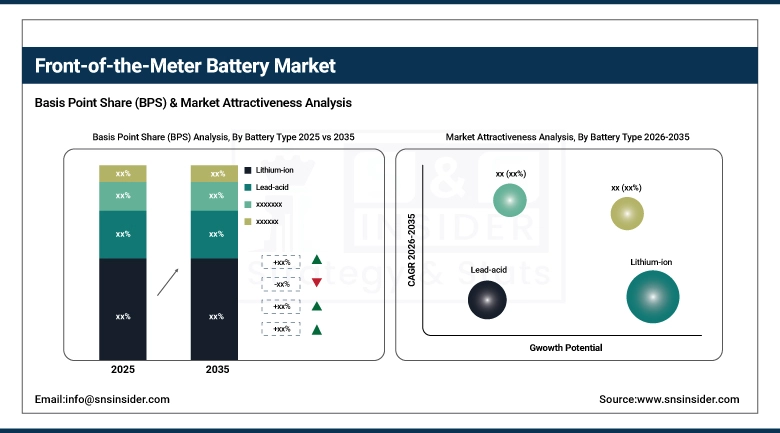

By Battery Type, Lithium-ion dominated the Front-of-the-Meter Battery Market with ~70% share in 2025; Flow Batteries fastest growing (CAGR).

-

By Ownership Model, Utility Owned dominated the Front-of-the-Meter Battery Market with ~51% share in 2025; Third Party Owned (IPP/ESCO) fastest growing (CAGR).

-

By Capacity, Above 50 MW dominated the Front-of-the-Meter Battery Market with ~61% share in 2025; 10–50 MW fastest growing (CAGR).

By Battery Type, Lithium-ion segment dominates the Market, Flow Batteries expected to grow fastest

The Lithium-ion segment held the highest share in the Front-of-the-Meter Battery Market in 2025 due to its high energy density, longer cycle life, reduced costs, and increasing adoption in utilities for large-scale storage applications, making it the most preferred choice for efficient energy storage solutions in the grid.

The Flow Batteries segment is likely to register the fastest CAGR in the Front-of-the-Meter Battery Market during the period from 2026 to 2035 due to its ability to store energy for a longer period, making it scalable and flexible for large-scale renewable energy applications, thus attracting investments in utility-scale applications for grid support.

By Application, Grid Services segment dominates the Market, Renewable Integration expected to grow fastest

The Grid Services segment accounted for the largest market share in the Front-of-the-Meter Battery Market in 2025. The segment is expected to grow because grid services are vital for the stability of the grid and the management of peak demand. Energy storage solutions are required for the uninterrupted supply of electricity. In addition, grid services are required for the efficient integration of renewable energy sources and the reliability of the grid.

The Renewable Integration segment is expected to register the highest growth rate in the Front-of-the-Meter Battery Market during the forecast period of 2026-2035. The increasing use of solar and wind energy requires the use of energy storage solutions for balancing the intermittency of the sources and the uninterrupted supply of electricity.

By Ownership Model, Utility Owned segment dominates the Market, Third Party Owned (IPP/ESCO) expected to grow fastest

Utility Owned segment led the Front-of-the-Meter Battery Market in 2025, as utilities prefer to have direct control over their energy storage assets to optimize their grid management, provide reliable grid services, and optimize their renewable energy integration in an efficient manner to ensure long-term reliability while taking advantage of regulatory incentives and avoiding reliance on third-party providers.

Third Party Owned (IPP/ESCO) segment is expected to record the fastest growth rate during 2026-2035, as independent power producers/ESCOs are investing in FTM batteries to provide flexible financial options to utilities, minimize their capital expenditures, and accelerate their large-scale energy storage solutions.

By Capacity, Above 50 MW segment dominates the Market, 10–50 MW expected to grow fastest

The Above 50 MW segment accounted for the largest market share in the Front of Meter Battery Market in 2025, as utilities and large-scale projects favor large-scale solutions for grid stability, renewable energy integration, and peak shaving, as large-scale batteries provide greater efficiencies, economics, and the capability of handling large energy loads in the transmission and distribution networks.

The 10-50 MW segment is expected to grow at the highest CAGR from 2026 to 2035, as mid-scale projects provide better deployment ease, fewer investment risks, and flexibility for integration into renewable energy grids, making it an ideal solution for urban, industrial, and energy storage expansion needs without the necessity for extremely large-scale solutions.

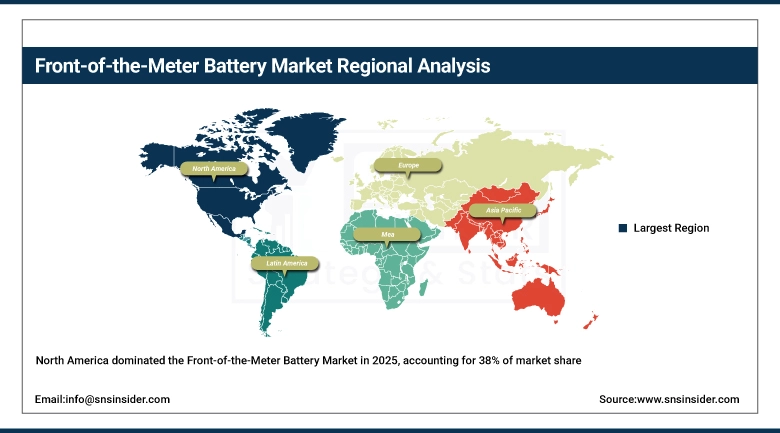

Front-of-the-Meter Battery Market Regional Analysis

North America Front-of-the-Meter Battery Market Insights

In 2025, North America held the largest share of the front of the meter battery market in terms of revenue at about 38% and is expected to continue to lead the market. This is because the region was the first to adopt advanced energy storage technologies. In addition, the region has a strong grid infrastructure and favorable government policies. High investment in the region by utilities and the need for grid stability, as well as the need to decarbonize the energy sector, have all contributed to the region’s leadership. The region is also home to a large number of energy storage companies and projects.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Front-of-the-Meter Battery Market Insights

The Asia Pacific segment is expected to witness the highest growth with a CAGR of around 22.08% during the forecast period of 2026 to 2035. This is because the countries in the Asia Pacific are rapidly industrializing and are increasing the capacity of renewable energy. Also, the governments are offering high incentives for the adoption of clean energy. For instance, countries such as China, India, and Japan are investing heavily in the development of Front-of-the-Meter battery plants.

Europe Front-of-the-Meter Battery Market Insights

The region of Europe has contributed a considerable share to the Front of the Meter Battery Market due to favorable government initiatives towards renewable energy integration, stringent carbon emission reduction targets, and rising investments in large-scale battery energy storage solutions. Countries such as Germany, the UK, and France are focusing on grid modernization and stabilization through renewable energy integration and rising battery solutions adoption.

Middle East & Africa and Latin America Front-of-the-Meter Battery Market Insights

The Middle East & Africa front-of-the-meter battery market is driven by factors such as increasing investments in renewable energy projects, rising energy demand, and government initiatives to boost grid reliability. Likewise, the Latin America front-of-the-meter battery market is driven by factors such as increasing capacity additions of solar and wind power, supportive policies, and the need for large-scale energy storage solutions to ensure grid stability.

Front-of-the-Meter Battery Market Competitive Landscape:

Tesla, Inc.

Tesla, Inc. is a leading company in the provision of electric vehicles, renewable energy solutions, and battery storage products. Tesla's Megapack utility-scale battery storage products are utilized for grid stability, renewable energy integration, and energy arbitrage. Tesla focuses on front-of-the-meter applications, where energy storage is combined with solar and wind power for improved reliability. Tesla is expanding production capacity, with a Shanghai factory for Megapack products, aiming to accelerate the energy transition, increase grid stability, and facilitate the adoption of utility-scale battery storage products for the modern energy landscape.

-

2023: Tesla deployed 14.7 GWh of utility-scale Megapack systems globally, advancing grid-connected installations and supporting front-of-the-meter renewable integration and energy storage initiatives.

-

2024: Tesla set a 2024 record with 31.4 GWh deployed in utility-scale energy storage, highlighting rapid front-of-the-meter grid storage growth worldwide.

-

2025: Tesla began production at its Shanghai Megapack factory, its first overseas utility-scale battery plant, boosting global deployment capacity for front-of-the-meter storage.

Fluence Energy

Fluence Energy is a global energy storage technology and services company that focuses on providing utility-scale battery energy storage solutions and software-enabled grid optimization. The company helps provide front-of-the-meter solutions for frequency response, peak shaving, and integration of renewables. Fluence Energy is dedicated to providing high-capacity, integrated battery energy storage solutions by focusing on local manufacturing, software, and project expertise. The company’s installations across the globe provide reliable energy storage solutions, helping utilities and independent power producers manage energy demand, integrating intermittent renewables, and supporting decarbonization.

-

2024: Fluence surpassed 20 GWh of deployed and contracted battery storage globally, demonstrating continued growth in front-of-the-meter energy storage solutions.

-

2024: Fluence opened the 200 MW/400 MWh Rangebank BESS in Victoria, Australia, the region’s second-largest grid battery supporting renewables and peak demand.

-

2025: Fluence delivered its first domestically manufactured BESS using U.S. components, strengthening supply chains for utility-scale front-of-the-meter energy storage.

-

2025: Fluence was selected to supply a 55 MW/110 MWh flagship Finnish grid storage system, enhancing front-of-the-meter frequency regulation and grid balancing services.

BYD Company Limited

BYD Company Limited is a Chinese multinational company that deals with the manufacture of electric vehicles, batteries, and other energy storage solutions. The company’s utility-scale BESS solutions are geared towards grid reliability and security, integration with renewable energy sources, and high availability. BYD Company Limited deals with the development of scalable battery solutions that are geared towards increasing the flexibility of the grid and the decarbonization of the grid. The company uses lithium iron phosphate chemistry and other modern designs to develop safe and efficient energy storage solutions for the front-of-the-meter market and other renewable energy solutions.

-

2025: BYD announced a 100 MW/400 MWh energy storage project in Central California, achieving high reliability and availability among statewide grid-scale battery installations.

Sungrow Power Supply Co., Ltd.

Sungrow Power Supply is a global leader in providing solar inverters, energy storage solutions, and renewable energy solutions. Its front-of-the-meter BESS solutions help provide grid-scale renewable integration, frequency regulation, and peak load management solutions. At Sungrow, there is a focus on providing liquid-cooled solutions, which help provide high-capacity solutions with long-duration operation. Sungrow works with various utility companies and independent power producers to provide efficient solutions for energy storage, helping them achieve their renewable energy goals.

-

2024: Sungrow’s PowerTitan liquid-cooled BESS will supply the 200 MW/800 MWh Vilvoorde project for ENGIE in Belgium, supporting one of Europe’s largest grid-scale storage deployments.

Front-of-the-Meter Battery Companies are:

-

Tesla, Inc.

-

Samsung SDI

-

Contemporary Amperex Technology Co. Limited (CATL)

-

Fluence Energy

-

BYD Company Limited

-

ABB Ltd.

-

NEC Energy Solutions

-

Hitachi Energy

-

General Electric (GE) Renewable Energy

-

NextEra Energy Resources

-

Saft Groupe S.A. (TotalEnergies)

-

Sungrow Power Supply Co., Ltd.

-

Powin Energy

-

EVE Energy Co., Ltd.

-

Vestas Wind Systems A/S

-

EnerSys

-

Leclanché SA

-

Wärtsilä Corporation

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 13.12 Billion |

| Market Size by 2035 | USD 87.28 Billion |

| CAGR | CAGR of 20.97% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Battery Type (Lithium-ion, Lead-acid, Flow Batteries, Others) • By Application (Grid Services, Renewable Integration, Peak Shaving, Frequency Regulation, Others) • By Ownership Model (Utility-Owned, Third-Party Owned, Customer-Owned) • By Capacity (Below 10 MW, 10–50 MW, Above 50 MW) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Tesla, Inc., LG Energy Solution, Samsung SDI, Contemporary Amperex Technology Co. Limited (CATL), Fluence Energy, BYD Company Limited, Siemens Energy, ABB Ltd., NEC Energy Solutions, Hitachi Energy, General Electric (GE) Renewable Energy, NextEra Energy Resources, Saft Groupe S.A. (TotalEnergies), Sungrow Power Supply Co., Ltd., Powin Energy, EVE Energy Co., Ltd., Vestas Wind Systems A/S, EnerSys, Leclanché SA, Wärtsilä Corporation. |

Frequently Asked Questions

North America dominated the Front-of-the-Meter Battery Market in 2025.

The Utility-Owned segment dominated the Front-of-the-Meter Battery Market in 2025.

Rapid adoption of renewable energy sources is fueling demand for large-scale Front-of-the-Meter battery storage solutions globally.

The Front-of-the-Meter Battery Market was valued at USD 13.12 billion in 2025.

The Front-of-the-Meter Battery Market is expected to grow at a CAGR of 20.97% from 2026 to 2035.

Get in Touch