Gold Mining Market Report Scope & Overview:

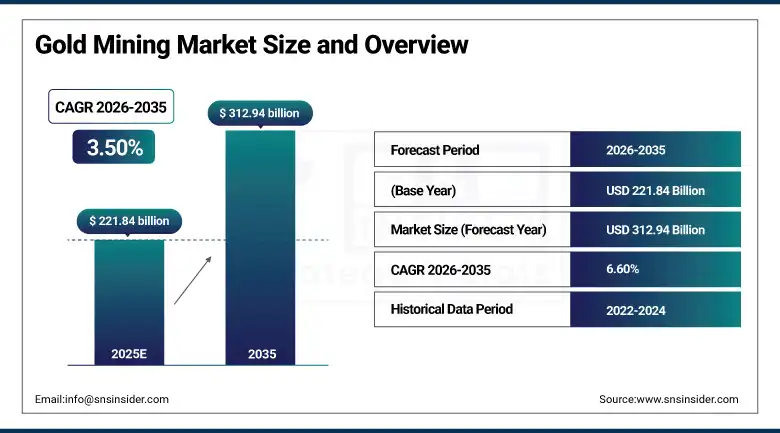

The Gold Mining Market was valued at USD 221.84 billion in 2025 and is expected to reach USD 312.94 billion by 2035, growing at a CAGR of 3.50% from 2026-2035.

Gold Mining Market repeatedly shows itself highly resistant and demonstrates excellent structural growth backed by gold`s traditional status of trustful safe haven investment asset, one of the main industrial material and an outstanding part of the world jewellery market. Increasing geopolitical uncertainty, volatility in monetary policy and inflation concerns have reinforced the demand for gold from both institutional and retail investors, with tighter commodity prices encouraging investment in new exploration and production. Industries are also undergoing technological transformation through automation, AI-based exploration analytics, satellite Geospatial technology and hybrid and electric mining equipment are being employed.

In a further endorsement of this trend, the World Gold Council reported that central banks worldwide bought in excess of 1,000 tonnes of gold in 2023 the second consecutive year of record central bank buying reiterating gold's solidifying status as a strategic reserve asset and keeping prices at levels which directly encourage investment in mining and expansion of production globally.

Moreover the U.S. Geological Survey (USGS) reported that world gold mine production is placed at around 3,300 tonnes in 2023 and the identified world gold resource base of more than 100000 tonnes which secures a several year's heritage of the foundation accessible for growth throughout in anybody year. According to the USGS, Australia and South Africa also stand out as the two most important centres of the world's identified gold resources, offering a solid long-term base for continued exploration and production activity.

Gold Mining Market Size and Forecast

-

Market Size in 2025: USD 221.84 Billion

-

Market Size by 2035: USD 312.94 Billion

-

CAGR: 3.50% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information On Gold Mining Market - Request Free Sample Report

Gold Mining Market Trends

-

Increasing automation in mining operations including autonomous haulage systems, remote drilling platforms, and AI-driven ore sorting is improving productivity and reducing labour costs.

-

Expansion of underground mining techniques including block caving and sub-level stopping is enabling economic access to deeper, high-grade gold deposits previously inaccessible.

-

Integration of AI and advanced data analytics into exploration programs is significantly improving drill target accuracy and reducing exploration expenditure per ounce discovered.

-

Growing adoption of blockchain-based gold traceability platforms is enhancing supply chain transparency, supporting responsible sourcing commitments, and meeting rising ESG compliance requirements.

-

Development of hybrid and battery-electric mining equipment is gaining momentum as producers seek to reduce underground diesel emissions, lower ventilation costs, and decrease carbon footprints.

-

Strategic mergers and acquisitions among major producers are consolidating ore reserves, operational scale, and geographic diversification to strengthen competitive positioning in a high-cost environment.

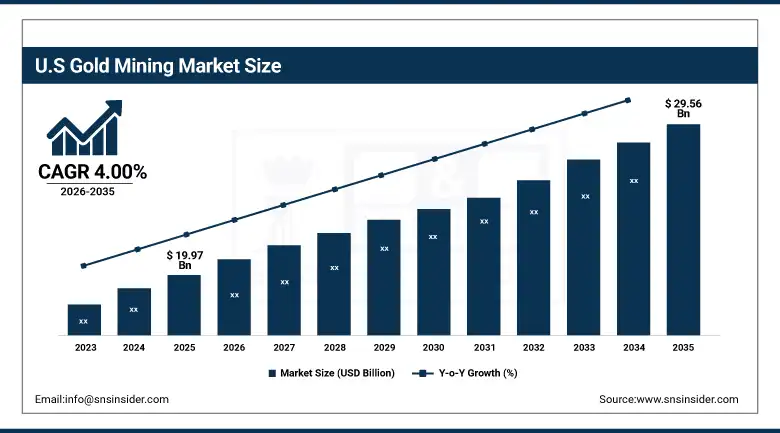

U.S. Gold Mining Market was valued at USD 19.97 billion in 2025 and is expected to reach USD 29.56 billion by 2035, growing at a CAGR of 4.00% from 2026–2035.

The U.S. Gold Mining Market is anchored by major production districts in Nevada the most prolific gold-producing state alongside significant operations in Alaska, Colorado, and Montana. The Nevada Gold Mines joint venture involving Barrick Gold and Newmont which is the single largest gold mining complex in the world helps illustrate how strategically vital U.S. production is to global gold supply. Robust mining regulations at the federal and state level, excellent infrastructure, and a trained labor pool continue to attract investment in domestic gold production and exploration.

Followed by the fact that the Nevada is classified as the worlds 4th largest gold producer as a standalone jurisdiction, producing around 4.5 million troy ounces per year according to data from the US Geological Survey.

The BLM, which manages federal lands where much of the country gold-mining activity takes place, has been abbreviating permit processes to shorten approvals of permits for exploration and development project work, facilitating continued investment in the U.S. gold-mining industry.

Gold Mining Market Segment Highlights

-

By Mining Type, Open-Pit Mining dominated the Gold Mining Market with 52% share (Hard Rock) in 2025; Underground Mining fastest growing (CAGR) due to deeper deposit access.

-

By Mining Equipment, Excavators dominated with 35% share in 2025; Mineral Processing Equipment fastest growing (CAGR).

-

By End-Use, Investment segment dominated with 60% share in 2025; Industrial segment fastest growing (CAGR) driven by electronics and technology sector demand.

Gold Mining Market Segment Analysis

By Mining Type, Open-Pit Mining segment dominates the Gold Mining Market, Underground Mining segment expected to grow fastest

In 2025, Open-Pit Mining continued to hold the largest share of the Gold Mining Market, representing nearly 52% of the hard rock mining subsegment. He said high equipment utilization, the lower costs of drilling and blasting, and the potential for deploying high-capacity loading and hauling fleets close to surface make Open-Pit methods an extraction method of choice for large low-grade near-surface gold deposits with favorable economics. Diversified operations like Barrick Gold's Cortez Complex in Nevada, USA, and Newmont's Boddington mine in Australia highlight the scale benefits of open-pit gold.

The Underground Mining segment is expected to witness the highest growth rate between 2026 and 2035, as high-grade surface deposits are increasingly exhausted, thus requiring mining companies to expand their portfolio and add higher-grade underground resources so as to maintain production levels. Deep underground mining is becoming safer and more economical due to mechanized tunnelling advances, paste backfill systems, and battery-electric underground equipment.

By Mining Equipment, Excavators segment dominates the Gold Mining Market, Mineral Processing Equipment segment expected to grow fastest

Excavators dominated the equipment segment, with a market share of ~35% in 2025 owing to their widespread use across surface and underground gold mining activities for stripping overburden, loading ore and materials handling. Cat, Komatsu and Hitachi high-performance hydraulic excavators are capital equipment required at every major gold mine in the world. Solid baseline demand is maintained by the changeout cycle for excavators at high-utilization mining operations, as well as ongoing commissioning of new open-pit mines in Africa and Latin America.

Through 2035, the Mineral Processing Equipment segment is projected to register the highest growth rate, as a result of an expanding investment in advanced ore processing technologies such as high-pressure grinding rolls (HPGR), bio leaching systems, and digital process optimization platforms. Due to falling output volumes and declining ore grades at mature mines, production at the front line of the gold sector is increasingly reliant on improved recovery technologies, in order to remain economically viable in the face of heightened costs from lower grades. Emerging innovations to support sustainable green processing including integrated closed-loop water usage, and elimination of mercury amalgamation extraction are becoming increasingly regulatory and investor focused, which are fuelling grow by directing more capital towards existing and new modernised mineral processing infrastructure at mining operations.

By End-Use, Investment segment dominates the Gold Mining Market, Industrial segment expected to grow fastest

Gold Investment accounted for around 60% of the share for Gold Mining End-Use market in 2025, further, this shows the unassailable position of Gold as the safest haven asset in the world. Investment demand has remained strong, thanks to central bank gold accumulation with back-to-back years of purchases greater than 1,000 tonnes according to the World Gold Council coupled with ongoing retail investor demand for gold bars, coins and gold-backed exchange-traded funds (ETFs). We have seen institutional and private investors alike, globally turning to gold as a safe and secure store of value in times of rising geopolitical tensions, fears of currency depreciation, and post-pandemic inflationary pressures.

Gold consumption in electronics, semiconductor manufacturing, medical devices, and emerging clean energy technologies is projected to drive the Industrial segment with the highest CAGR through 2035. Gold's unusual combination of electrical conductivity, corrosion resistance and reliability at sub-microscopic scales have made it invaluable in advanced electronics manufacturing, from high-performance semiconductor packaging, printed circuit boards and connector plating.

Gold Mining Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

Asia Pacific |

China |

50% |

|

North America |

United States |

70% |

|

Europe |

Russia |

55% |

|

Middle East & Africa |

Ghana |

25% |

|

Latin America |

Peru |

35% |

Asia Pacific Gold Mining Market Insights

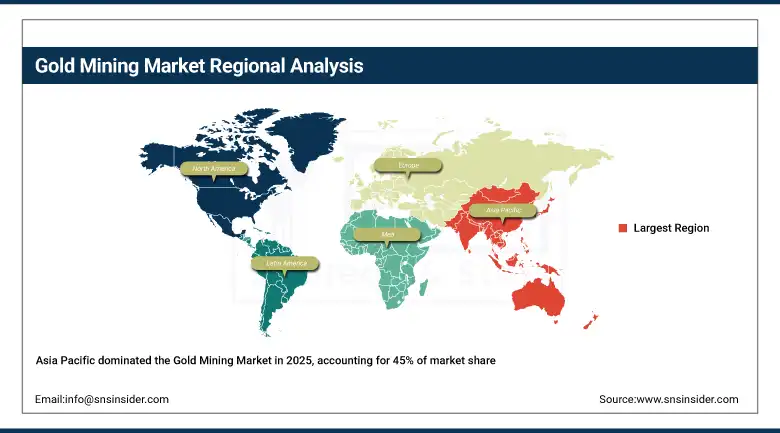

In 2025, Asia Pacific accounted for the largest revenue share in the global Gold Mining Market, with around 45%, while China was responsible for almost 50% of the regional share. It is the world’s largest gold producer which, along with the long-running mining of vast volumes across the dynamic provinces of Shandong, Henan and Inner Mongolia, gives the country its crown as the power-player of the gold world. With strong government backing, extensive development of infrastructure, technological advancements in exploration and processing, and sustained investment, regional leadership is further promoted as China turns out to be the single biggest driver of Asia Pacific's strength in this arena.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Gold Mining Market Insights

While North America still forms one of the cornerstones of global gold mining (with the U.S. making up approximately 70% of the region), it is generally the less frequent mover compared to much of the world. Very productive mining zones like Nevada are wedded to first world mining infrastructure and regulation with a continuous stream of innovation. Canada is not a small player, but the United States still leads regionally in both production and market performance..

Europe Gold Mining Market Insights

Europe’s gold mining market is led by Russia, which accounts for approximately 55% of the regional share. The country’s worldwide lead is buttressed by enormous reserves, vast-scale mining operations in Siberia and the Far East, continued investment in extraction technologies. This makes Russia the heart of gold production in Europe.

Middle East & Africa Gold Mining Market Insights

Gold Mining Market in the Middle East & Africa gradually increased growth with Ghana accounted for nearly 25% of the share of regional greatness. Across the African nations, the growth initially and foremost stems from increased mining operations supported by favourable regulatory frameworks, growing foreign investment flux and enhanced exploration activities. Although the region is only a minor producer for the Middle East, Africa still represents the heart of production in the region.

Latin America Gold Mining Market Insights

In total, Latin America is considered a key player in global gold mining, where about 35% of the Latin American regional share corresponds to Peru. Well, Peru has vast mining operations in the Andes, solid mineral deposits that continue to be attractive to foreign investors. Mexico and Brazil are also helping to bolster the region, but Peru continues to be the mainstay of Latin American gold mining together with Chile.

Gold Mining Market Growth Drivers:

-

Growing demand for gold as a strategic reserve asset and safe-haven investment driving sustained price appreciation and stimulating global exploration and production investment

As the world's most trusted monetary reserve asset, gold's structure continues to supply a robust and consistent long-term demand driver for the mining sector. With a high level of historic demand for gold coming from central banks, monetary authorities from emerging markets are currently rebalancing their reserve concentration away from the U.S. dollar and into gold — with China, India, Turkey, and Central Asian economies leading in this resurgence. Higher geopolitical risk, economic fragmentation and creeping inflation are underpinning high gold prices that significantly enhance the economics of new mining projects and incentivise expansion at existing operations. This prolonged environment of high-prices is making previously sub-economic deposits viable projects and is therefore increasing the global pipeline of investable mining opportunities.

As the World Gold Council's Gold Demand Trends data illustrates year-in, year-out, demand from central banks when considered together has held above a 1,000 tonne annual floor in recent years; emerging market central banks have placed a considerable focus on this area with reserve diversification programs that remains skewed in favour of gold accumulation — on a global scale this is a structural demand driver which directly facilitates gold mine investment and production growth over time.

Gold Mining Market Restraints:

-

Stringent environmental regulations, community opposition, and sustainability compliance requirements increasing project development timelines and operational costs across major mining jurisdictions

Among these, the one of the most influential structural constraints present on the gold mining market is environmental regulatory requirements. As a result, governments in all of the major mining jurisdictions Australia, Canada, the United States, and increasingly across Africa and Latin America are enacting regulations that require progressively stricter standards of water management, tailings storage, hazardous chemical usage, and land rehabilitation. Investment in alternative recovery technologies that are more expensive to process is being driven by bans or restrictions on cyanide-based gold extraction in certain jurisdictions. In some areas, community consultation requirements and free, prior, and informed consent (FPIC) obligations for projects impacting indigenous lands are stretching out project development schedules by years, delaying production start as well as increasing pre-development capital needs.

Gold Mining Market Opportunities:

-

Adoption of green mining technologies and expansion of gold exploration in untapped African and Asian regions creating significant new growth opportunities for the global gold mining industry

The equivalent of sustainable, technology-based gold mining is creating an extremely large opportunity set for companies best positioned to drive leadership in responsible methods of producing gold. New technologies such as bioleaching, pressure oxidation and thiosulfate leaching are providing cleaner options, allowing the leaching of previously non-leachable ore types, while still achieving regulatory thresholds that are becoming more and more stringent. The use of battery-electric underground mining equipment cuts diesel consumption, ventilation costs and greenhouse gas emissions at deep mines. As a result of the new combination of AI-powered exploration targeting, satellite geophysical surveying and geospatial data analytics, combined with the integration and delivery of research and data processing pipelines has materially improved discovery success rates and reduced time-to-production for new deposits in underexplored regions of Central Africa, the Asia Pacific, and Latin America.

Recent Developments:

-

2025: Agnico Eagle expanded gold processing capacity at its La India mine in Mexico in February 2025, targeting a 10% increase in annual output, while simultaneously launching a digital transformation program utilizing AI to optimize mining operations across its portfolio.

-

2025: Kinross Gold commissioned a high-efficiency leaching facility at its Tasiast mine in Mauritania in March 2025 to improve gold recovery rates, and acquired additional mineral rights in Chile in November 2024 to expand South American exploration exposure.

-

2025: Newmont launched a solar-powered energy project at its Boddington mine in Australia in January 2025 to reduce carbon emissions, and expanded its Peruvian gold reserves through acquisition of additional mining claims in September 2024.

-

2024: Barrick Gold advanced exploration and development activities at its Reko Diq copper-gold project in Pakistan, with initial production targeted as part of the company's portfolio diversification into high-quality, long-life assets in emerging mining jurisdictions.

Gold Mining Market Key Players

Some of the Gold Mining Market Companies

-

Newmont Corporation

-

Barrick Gold Corporation

-

Agnico Eagle Mines Ltd.

-

AngloGold Ashanti Ltd.

-

Kinross Gold Corporation

-

Gold Fields Ltd.

-

Polyus Gold International Ltd.

-

Newcrest Mining (now Newmont)

-

Northern Star Resources Ltd.

-

Evolution Mining Ltd.

-

Harmony Gold Mining Company

-

B2Gold Corp.

-

Alamos Gold Inc.

-

Coeur Mining, Inc.

-

Pan American Silver Corp.

-

OceanaGold Corporation

-

SSR Mining Inc.

-

Eldorado Gold Corporation

-

Resolute Mining Limited

-

Endeavour Mining plc

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 221.84 Billion |

| Market Size by 2035 | USD 312.94 Billion |

| CAGR | CAGR of 3.50% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Mining Type (Placer Mining, Hard Rock Mining [Underground Gold, Open-pit Gold], Hydraulic Mining, Others) •By Mining Equipment (Drills & Breakers, Excavators, Loaders, Crushers & Screens, Others) •By End-use (Investment, Jewelry, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Barrick Gold Corporation, Newmont Mining Corporation, AngloGold Ashanti Ltd, Goldcorp Inc., Kinross Gold Corporation, Newcrest Mining Ltd, Gold Fields Ltd, Polyus Gold International Ltd, Agnico Eagle Mines Ltd, Coeur Mining and other key players |

Frequently Asked Questions

Ans: Asia Pacific is the fastest-growing region in the Gold Mining Market.

Ans: North America dominated the Gold Mining Market in 2025.

Ans: The Investment segment dominated the Gold Mining Market with approximately 60% share in 2025.

Ans: The Gold Mining Market was valued at USD 221.84 billion in 2025.

Ans: The Gold Mining Market is expected to grow at a CAGR of 3.50% from 2026 to 2035.

Get in Touch