Heavy Duty Engines Market Report Scope & Overview

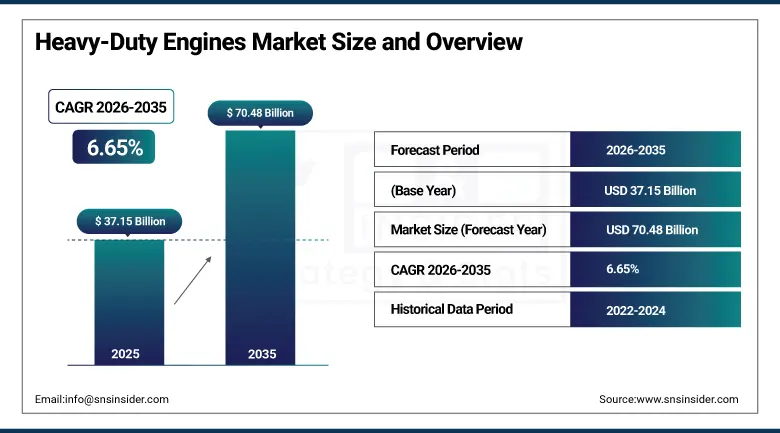

The Heavy-Duty Engines Market was valued at USD 37.15 Billion in 2025 and is expected to reach USD 70.48 Billion by 2035, growing at a CAGR of 6.65% from 2026 to 2035.

Market growth is driven by the increase in global logistics intensity, large scale infrastructure development and the continuous modernization of off-highway and on-highway fleets. Regulatory pressure on emissions is accelerating the shift to advanced diesel technologies, natural gas engines, hybrid systems and early hydrogen-based combustion platforms. OEMs are also focusing on improving engine efficiency, durability and lifecycle performance to reduce total cost of ownership for fleet operators in the transportation and industrial sectors.

Cummins has been making more investments in hydrogen and low-emissions engines in order to achieve green freight transport. On the other hand, Volvo Group is working on developing a strategy that will make use of alternative fuels for heavy duty hybrid powertrains, especially within Europe.

Market Size and Forecast

-

Market Size in 2026E: USD 39.49 Billion

-

Market Size by 2035: USD 70.48 Billion

-

CAGR: 6.65% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Heavy-Duty Engines Market - Request Free Sample Report

Market Trends

-

Increasing global freight and logistics demand is driving sustained requirement for high-torque, fuel-efficient heavy-duty engines across on-highway commercial vehicle fleets.

-

Rising infrastructure development and construction megaprojects worldwide are boosting deployment of heavy-duty engines in earthmoving, excavation, and material handling equipment.

-

Tightening emission regulations across Europe, North America, and China are accelerating demand for advanced low-emission diesel, hybrid, and alternative fuel engine technologies.

-

Expanding mining activities for critical minerals such as lithium, copper, and nickel are increasing adoption of high-horsepower heavy duty engines for haul trucks and heavy machinery.

-

Growing investments in alternative fuel technologies, including natural gas and hydrogen-based engines, are driving long-term transition opportunities in next-generation heavy-duty propulsion systems.

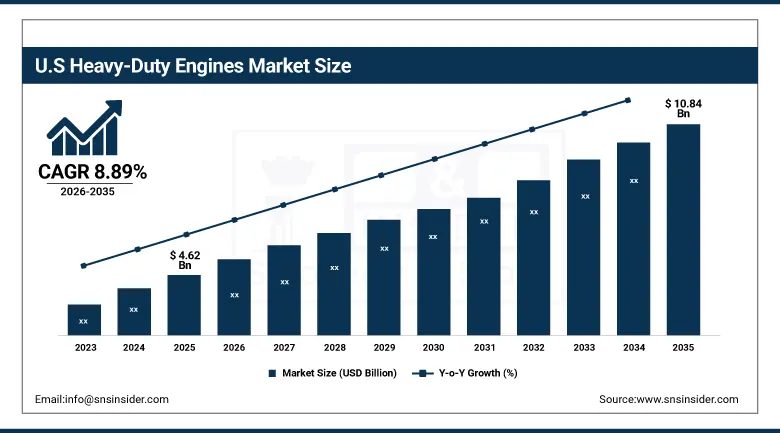

U.S. Heavy Duty Engines Market Outlook

The U.S. Heavy Duty Engines Market was valued at approximately USD 4.62 Billion in 2025 and is expected to reach approximately USD 10.84 Billion by 2035, growing at a CAGR of approximately 8.89% from 2026 to 2035.

Rising freight intensity across interstate logistics networks, the expansion of e-commerce-enabled delivery ecosystems and ongoing infrastructure investment through federal and state-level programmers are driving market growth. EPA and CARB stringent emission regulations are driving the adoption of advanced diesel engines with after-treatment systems, natural gas engines and nascent hybrid heavy-duty powertrains. Fleet owners are looking for engines that offer better fuel efficiency, lower total cost of ownership and the ability to use low carbon fuel alternatives. Furthermore, growing demand from construction and energy sectors is strengthening engine replacement cycles.

In 2025, Cummins expanded its hydrogen-ready heavy-duty engine testing programmers to major U.S. freight corridors, and PACCAR and Daimler Truck North America accelerated deployment of advanced telematics-based engine monitoring systems to increase fleet efficiency and uptime. The US remains a major player in global heavy-duty vehicle electrification and alternative fuel pilot programmers, driven by regulatory pressure from the EPA and CARB, and further cements its position as a key transition market for next-generation engine technology.

Heavy Duty Engines Market Segment Analysis

-

By Engine Type, diesel engines dominated the Heavy-Duty Engines Market with 68.00% share in 2025, while hydrogen internal combustion engines are the fastest growing segment from 2026 to 2035.

-

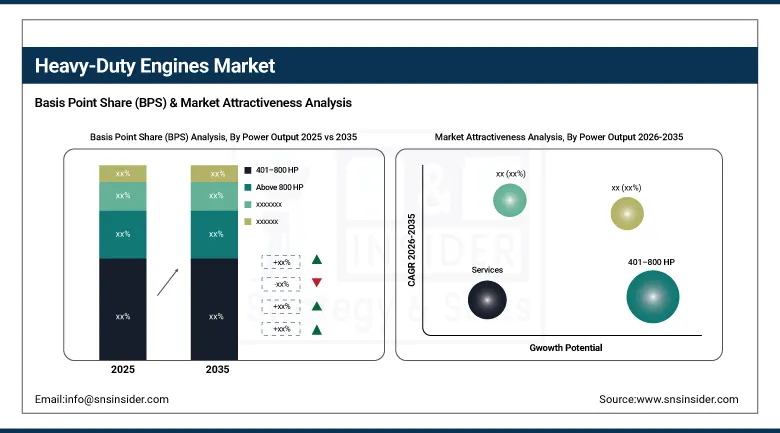

By Power Output, 401–800 HP segment dominated the Heavy-Duty Engines Market with 54.00% share in 2025, while above 800 HP segment is the fastest growing power output segment from 2026 to 2035.

-

By Application, on-highway vehicles dominated the Heavy-Duty Engines Market with 49.00% share in 2025, while mining equipment is the fastest growing application segment from 2026 to 2035.

-

By End Use Industry, transportation & logistics dominated the Heavy-Duty Engines Market with 46.00% share in 2025, while mining & infrastructure segment is the fastest growing end-use industry from 2026 to 2035.

By Engine Type, diesel engines dominate the market while hydrogen internal combustion engines are growing the fastest

Diesel engines dominated the Heavy-Duty Engines Market in 2025 and accounted for approximately 68% revenue share. This dominance is driven by high torque output, long operational durability, strong fuel efficiency under heavy loads and widespread deployment across freight trucking, construction equipment and mining machinery. The current global refueling infrastructure guarantees the leadership position of the diesel engines in mature industrial ecosystems.

The hydrogen internal combustion engine is expected to witness the fastest CAGR due to increasing decarbonization mandates and investments by the OEMs in next-generation propulsion systems. Tightening emission regulations in Europe, North America and China and increasing pilot projects in long-haul trucking and industrial applications are accelerating early-stage commercialization of hydrogen-based heavy-duty engine technologies.

By Power Output, 401–800 HP segment dominates the market while above 800 HP segment is growing the fastest

The 401–800 HP segment dominated the Heavy-Duty Engines Market in 2025 and accounted for approximately 54% revenue share. This range provides the best compromise between fuel efficiency and high torque output and is widely used in long haul trucks, construction equipment and mid-scale mining operations. Its strong OEM standardization in this power band also helps its global adoption.

The above 800 HP segment is anticipated to have the fastest CAGR owing to growing demand in large scale mining, oil & gas operations, and infrastructure megaprojects. These high load applications require high levels of torque performance and continued duty operation which in turn drives the demand for advanced high output engine systems with improved thermal efficiency and durability.

By Application, on-highway vehicles dominate the market while mining equipment is growing the fastest

On-highway vehicles dominated the Heavy-Duty Engines Market in 2025 and accounted for approximately 49% revenue share. Driving this dominance are global freight transportation, expanding logistics networks, and increasing long-haul trucking activities that support international supply chains. Continuous replacement cycles of the fleet sustain the demand across the commercial vehicle segments.

Mining equipment is anticipated to grow at the fastest CAGR due to increasing demand for critical minerals, including lithium, copper, and rare earth elements, worldwide. The large-scale mining operations in Latin America, Africa and Australia are driving the adoption of high-horsepower engines in haul trucks, drilling systems and heavy excavation machinery.

By End Use Industry, transportation & logistics dominate the market while mining & infrastructure is growing the fastest

Transportation & logistics dominated the Heavy-Duty Engines Market in 2025 and accounted for approximately 46% revenue share. The segment is being benefited by strong global trade expansion, rising demand for e-commerce logistics and high utilization of heavy-duty freight vehicles across intercity and interstate transport networks.

Mining & infrastructure is expected to have the fastest CAGR due to increasing investments in global resource extraction and large-scale infrastructure development projects. Rising demand for continuous-duty, high-performance engines operating in extreme environments is driving more adoption across mining fleets and infrastructure construction equipment.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

81.18% |

|

Europe |

Germany |

31.2% |

|

Asia Pacific |

China |

34.7% |

|

Middle East & Africa |

UAE |

24.1% |

|

Latin America |

Brazil |

45.6% |

North America Heavy Duty Engines Market Insights

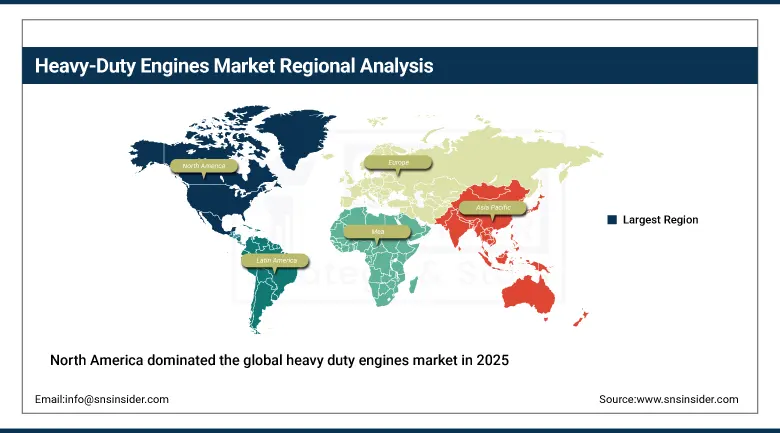

North America dominated the global heavy duty engines market in 2025 and held approximately 32.11% of global revenues. The region’s leadership is fueled by a highly developed freight transportation network, substantial penetration of Class 7-8 commercial vehicles and consistent fleet replacement cycles across the United States and Canada. High performance and durable engine systems are also required for the large-scale construction activity, logistics expansion and mining operations, which further sustains demand. Strict emission regulations from the EPA and CARB are also accelerating adoption of advanced diesel engines, natural gas engines and hybrid powertrains.

More and more commercial fleets are equipping themselves with digital engine management systems, predictive maintenance solutions and fuel optimization technologies, and this is having a positive impact on the region. Cummins continued its hydrogen-ready engine testing programmers in U.S. freight corridors in 2025. PACCAR and Daimler Truck North America expanded their deployment of connected engine diagnostics to improve fleet efficiency and uptime. Canada continues to push low-emission heavy-duty engines through clean transportation initiatives and infrastructure modernization.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Heavy Duty Engines Market Insights

Europe accounted for approximately 21.44% of global heavy duty engines market revenues in 2025. The market is driven by strict emission norms, increasing adoption of Euro VI-compliant engines and rapid transition towards hybrid and alternative fuel-based heavy-duty propulsion systems. These include Germany, France and the United Kingdom which are spearheading the demand for advanced engine technologies within freight, construction and industrial applications.

In 2025, Volvo Group continued to develop hydrogen engines, while MAN and Scania increased the use of advanced low-emission engine systems with the latest after-treatment technologies. Germany plays an important role as an innovation centre for large-scale research and development and production of industrial engines.

Asia Pacific Heavy Duty Engines Market Insights

Asia Pacific dominated the global heavy duty engines market in 2025 and held approximately 36.13% of global revenues, which makes it the largest regional market. Growth is being fueled by rapid industrialization, developing logistics networks and large-scale infrastructure development in China, India, Japan and South Korea. Regional dominance continues to be supported by strong demand from construction, mining and freight transportation sectors.

In China, Weichai Power and Yuchai increased production of high-efficiency diesel engines in 2025 while in India, Tata Motors and Ashok Leyland increased use of advanced commercial engine platforms. Japan continues to invest in OEM to innovate in fuel-efficient and low-emission engines.

Middle East & Africa & Latin America Heavy Duty Engines Market Insights

Latin America and Middle East & Africa collectively accounted for approximately 10.32% of global heavy duty engines market revenues in 2025. Factors such as increasing infrastructure development, expanding mining activities and rising oil & gas exploration projects are some of the factors fueling the growth of these regions. Heavy-duty engine usage is increasing in construction, logistics, and industrial applications in countries such as Brazil, Mexico, the UAE, and Saudi Arabia. The demand is also supported by the need for durable, high-performance engines that can operate in demanding environmental conditions.

In 2025, Brazil fortified its position in Latin America with increasing demand from mining and agricultural mechanization, while the UAE and Saudi Arabia advanced large-scale infrastructure and energy projects demanding high-output engine systems. Expansion of OEM services and aftermarket support networks are also improving market accessibility and long-term fleet efficiency in both the regions.

Market Dynamics

Growth Drivers: Rising Freight Demand and Infrastructure Expansion

The heavy-duty engines market is witnessing a strong growth due to the rising demand for global freight transportation and the expansion of logistics networks. High-torque, fuel-efficient engines are seeing a significant demand boost from increasing cross-border trade, growth in e-commerce distribution systems, and higher utilization of commercial fleets. Also, increasing deployment of construction and heavy machinery equipment due to widespread infrastructure development projects across emerging and developed economies is further strengthening engine demand across industrial applications.

Heavy-duty engines are also increasingly adopted by construction, mining and material handling sectors due to increasing urbanization and industrialization. Growing demand for efficient long-haul transportation systems and supply chain modernization is further driving demand for advanced diesel, natural gas and hybrid engine technologies across global markets.

Restraints: Stringent Emission Regulations and High Technology Compliance Costs

Engine manufacturers are facing increasing global compliance pressure due to stringent emission regulations such as Euro VI, EPA standards, and China VI norms. This is driving R&D investments in after-treatment systems, fuel efficiency improvements and alternative propulsion technologies. This results in higher production costs and longer development cycles for next generation heavy duty engines for the OEMs.

Further, the slow phase-out of traditional diesel engines is posing operational challenges to fleet operators, especially in regions where alternative fuel infrastructure is scarce. Upgrading fleets to meet regulatory standards is also costly and therefore hampering adoption in cost-sensitive markets.

Opportunities: Electrification, Hydrogen Adoption, and Alternative Fuel Transition

The heavy-duty engines market is witnessing a strong growth due to the rising demand for global freight transportation and the expansion of logistics networks. High-torque, fuel-efficient engines are seeing a significant demand boost from increasing cross-border trade, growth in e-commerce distribution systems, and higher utilization of commercial fleets. Also, increasing deployment of construction and heavy machinery equipment due to widespread infrastructure development projects across emerging and developed economies is further strengthening engine demand across industrial applications.

Increasing urbanization and industrialization are also accelerating the adoption of heavy-duty engines in construction, mining and material handling sectors. The ongoing need for efficient long-haul transportation systems and supply chain modernization is further driving demand for advanced diesel, natural gas and hybrid engine technologies across global markets

Recent Developments

-

Cummins expanded its X15N natural gas heavy-duty engine deployment in 2025 through partnerships with Daimler Truck North America, enabling production of Freightliner Cascadia trucks equipped with next-generation low-emission powertrains for long-haul freight applications.

-

Daimler Truck North America integrated Cummins’ next-generation engine portfolio into its 2027 product lineup, including updated X15 and alternative fuel engines designed to meet stricter EPA emissions standards across Freightliner and Western Star platforms.

-

Freightliner began commercial rollout of Cascadia trucks powered by Cummins X15N natural gas engines in 2025, marking a key step in scaling alternative fuel adoption for heavy-duty long-distance trucking operations.

-

Cummins strengthened its HELM engine platform strategy, expanding multi-fuel capability across diesel, natural gas, and hydrogen-ready configurations to support long-term decarbonization of heavy-duty transport fleets globally.

Key Players

-

Cummins Inc.

-

Caterpillar Inc.

-

Volvo Group

-

Daimler Truck AG

-

PACCAR Inc.

-

MAN SE

-

Scania AB

-

Weichai Power Co. Ltd.

-

Deutz AG

-

Rolls-Royce Power Systems (MTU)

-

Isuzu Motors Ltd.

-

Hino Motors Ltd.

-

Mitsubishi Heavy Industries Ltd.

-

Deere & Company

-

Kubota Corporation

-

FPT Industrial (Iveco Group)

-

Liebherr Group

-

HD Hyundai Infracore

-

Ashok Leyland Ltd.

-

Tata Motors Limited

Heavy Duty Engines Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 37.15 Billion |

| Market Size by 2035 | USD 70.48 Billion |

| CAGR | CAGR of 6.65% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Engine Type (Diesel Engines, Natural Gas Engines, Hybrid Engines, Hydrogen Internal Combustion Engines) • By Power Output (Up to 400 HP, 401–800 HP, Above 800 HP) • By Application (On-Highway Vehicles, Construction Equipment, Mining Equipment, Agricultural Machinery, Marine & Rail Applications) • By End Use Industry (Transportation & Logistics, Construction & Infrastructure, Mining, Oil & Gas, Agriculture, Marine) • By Region (North America, Europe, Asia Pacific, Latin America, Middle East & Africa) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Cummins Inc., Caterpillar Inc., Volvo Group, Daimler Truck AG, PACCAR Inc, MAN SE, Scania AB, Weichai Power Co. Ltd., Guangxi Yuchai Machinery Group Co. Ltd., Deutz AG, Rolls-Royce Power Systems (MTU), Deere & Company, Kubota Corporation, Isuzu Motors Ltd., Hino Motors Ltd., Mitsubishi Heavy Industries Ltd., FPT Industrial (Iveco Group), Liebherr Group, HD Hyundai Infracore, Ashok Leyland Ltd. |

Frequently Asked Questions

The Heavy-Duty Engines Market is expected to grow at a CAGR of approximately 6.65% during the forecast period.

The Heavy-Duty Engines Market was valued at approximately USD 37.15 Billion in 2025.

Rising global freight transportation demand, expansion of logistics networks, and increasing infrastructure development activities are major factors driving market growth globally.

Diesel engines dominated the market in 2025 due to their high torque efficiency, durability, and widespread use across long-haul trucking, construction, and mining applications globally.

Asia-Pacific dominated the Heavy-Duty Engines Market in 2025 due to strong industrialization, rapid infrastructure development, and high demand from freight, construction, and mining sectors across China and India.

Get in Touch