Helicopter Engines Market Report Scope & Overview:

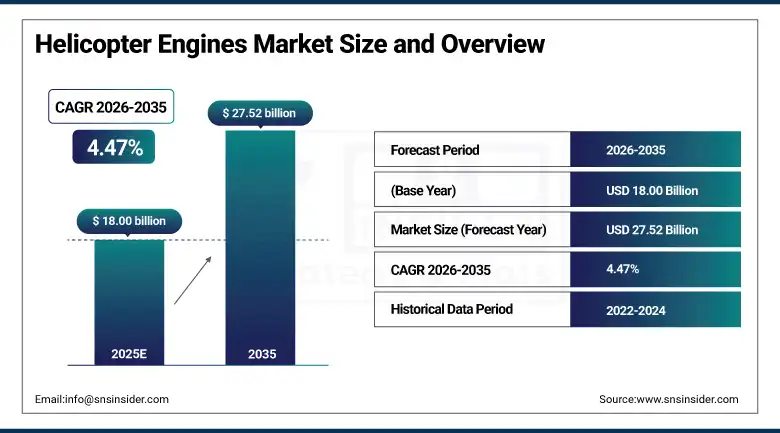

The Helicopter Engines Market was valued at USD 18.00 billion in 2025 and is expected to reach USD 27.52 billion by 2035, growing at a CAGR of 4.47% from 2026–2035.

The Helicopter Engines Market is experiencing healthy growth thanks to growing initiatives related to defense modernization across the globe, growing purchase of military and commercial helicopters, and the increasing use of emergency medical services (EMS), offshore travel, and search & rescue missions. Technology development in the form of advanced fuel-efficient turboshaft engines, FADEC, predictive maintenance, and hybrid propulsion engines is contributing to operational efficiencies and cost-effectiveness.

Supporting this trend, the U.S. Department of Defense’s proposed FY2025 budget includes significant allocations for rotorcraft modernization programs such as the UH-60 Black Hawk, AH-64 Apache, and CH-47 Chinook fleet upgrades, while global defense spending surpassed USD 2.4 trillion in 2024, according to the Stockholm International Peace Research Institute (SIPRI).

In addition, recent developments in next-generation propulsion technologies are accelerating innovation in the sector. In March 2024, Safran Helicopter Engines successfully completed the first ground test of its future hybrid-electric propulsion demonstration program, while GE Aerospace continues advancing the T901 turboshaft engine program for the U.S. Army’s Improved Turbine Engine Program (ITEP), aimed at improving power, fuel efficiency, and mission readiness for next-generation rotorcraft.

Helicopter Engines Market Size and Forecast

-

Market Size in 2025: USD 18.00 Billion

-

Market Size by 2035: USD 27.52 Billion

-

CAGR: 4.47% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Helicopter Engines Market - Request Free Sample Report

Helicopter Engines Market Trends

-

Rising adoption of fuel-efficient turboshaft engines is improving payload capacity, range, and operational efficiency across civil and military helicopter fleets.

-

Increasing integration of Full Authority Digital Engine Control (FADEC) systems is enhancing engine performance, reliability, and real-time diagnostics.

-

Rapid advancements in hybrid-electric and sustainable aviation fuel (SAF)-compatible propulsion technologies are driving next-generation helicopter engine innovation.

-

Growing demand for predictive maintenance and AI-enabled engine health monitoring systems is improving fleet uptime and reducing lifecycle costs.

-

Increasing procurement of high-power engines for military modernization and heavy-lift missions is accelerating demand for advanced propulsion systems.

-

Expanding deployment of helicopters in emergency medical services (EMS), offshore transport, and search & rescue operations is boosting engine replacement and aftermarket demand.

-

Rising use of lightweight materials and advanced turbine cooling technologies is enhancing engine durability and fuel efficiency in extreme operating environments.

U.S. Helicopter Engines Market Size Outlook:

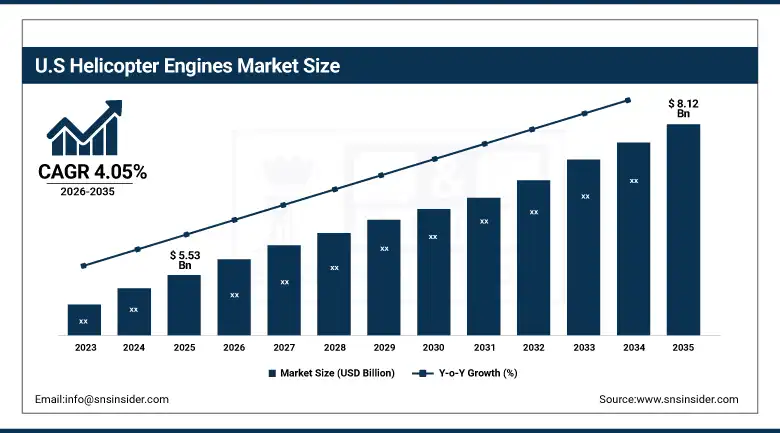

U.S. Helicopter Engines Market was valued at USD 5.53 billion in 2025 and is expected to reach USD 8.12 billion by 2035, growing at a CAGR of 4.05% from 2026–2035. U.S. Market holds the largest market share worldwide owing to high investments in defense, robust rotorcraft engine upgradation initiatives within the armed forces, and the availability of leading helicopter engines manufacturers including General Electric Company (GE Aerospace), Honeywell International Inc. (Honeywell Aerospace), and Raytheon Technologies Corporation (RTX).

In addition, recent developments such as GE Aerospace progressing the T901 engine program under the U.S. Army’s Improved Turbine Engine Program (ITEP) in 2024, and continued procurement and upgrade programs for UH-60 Black Hawk and AH-64 Apache fleets, reinforce the U.S. as a key hub for helicopter engine innovation and demand.

Helicopter Engines Market Segment Highlights

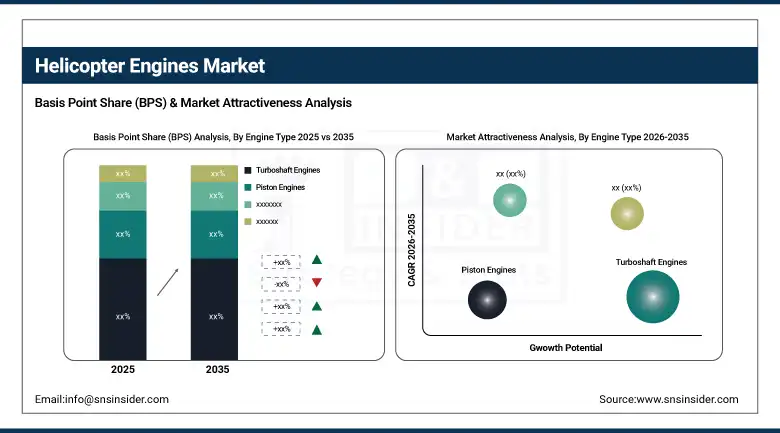

• By Engine Type, Turboshaft Engines dominated the Helicopter Engines Market with 82.36% share in 2025; Hybrid / Electric Propulsion Engines are the fastest growing in CAGR.

• By Power Output, 1,000–3,000 shp dominated the Helicopter Engines Market with 49.45% share in 2025; Above 3,000 shp is the fastest growing in CAGR.

• By Component, Turbine dominated the Helicopter Engines Market with 27.49% share in 2025; Gearbox / Transmission is the fastest growing in CAGR.

• By Application, Military Helicopters dominated the Helicopter Engines Market with 41.24% share in 2025; Utility / Cargo Helicopters is the fastest growing in CAGR.

• By End User, OEM (Original Equipment Manufacturers) dominated the Helicopter Engines Market with 36.14% share in 2025; Aftermarket / MRO Services is the fastest growing in CAGR.

• By Technology, Conventional Engines dominated the Helicopter Engines Market with 62.71% share in 2025; Hybrid-Electric Engines are the fastest growing in CAGR.

By Engine Type, Turboshaft Engines segment dominates the Helicopter Engines Market, Hybrid / Electric Propulsion Engines segment expected to grow fastest

In the Helicopter Engines Market, the Turboshaft Engines segment is Dominating in 2025, generating 82.36% of the overall market's income. Turbo shaft engines are essential components of the current helicopter engine since they possess an outstanding power-to-weight ratio, reliability, and versatility, allowing them to be used for various purposes, including military combat, lifting heavy loads, and performing emergency medical flights in offshore conditions. This segment's dominance was ensured by the extensive use of these engines in various platforms like utility, attack, and search & rescue helicopters and their continuous improvement regarding energy consumption and maintenance.

The Hybrid / Electric Propulsion Engines segment is expected to exhibit the highest CAGR of from 2026 to 2035. The development of innovative technologies aimed at decreasing emissions, fuel consumption, and noise generation attracts significant investments into this segment of the market.

By Power Output, 1,000–3,000 shp segment dominates the Helicopter Engines Market, Above 3,000 shp segment expected to grow fastest

The engine power range of 1,000–3,000 shp is projected to account for the largest market share of 49.45% in the Helicopter Engines Market in 2025 due to the wide usability of these engines on various medium-lift military helicopters, commercial cargo helicopters, and EMS aircraft. The engines of this range provide a perfect compromise between performance and economy for carrying out various helicopter missions, such as troops and goods transportation and relief flights.

The segment of Above 3,000 shp is predicted to grow at the fastest CAGR for the period from 2026 to 2035. This rapid growth can be attributed to the increasing number of orders for heavy-lift military helicopters, fire-fighting rotorcrafts, and helicopters designed for use in oil & gas industry operations.

By Component, Turbine segment dominates the Helicopter Engines Market, Gearbox / Transmission segment expected to grow fastest

The Turbine segment has consistently held the largest component market share, amounting to about 27.49%, within the Helicopter Engines Market throughout the forecast period, from 2026 to 2035. Turbines perform an essential function by enabling the transformation of combustion energy into mechanical energy, thereby playing a pivotal role in enhancing engine efficiency and performance.

The Gearbox / Transmission segment is expected to register the highest CAGR in the coming decade, between 2026 and 2035. This can be attributed to increasing demand for power optimization and effective torque management through efficient transmission technology in modern high-power and future hybrid helicopters.

By Application, Military Helicopters segment dominates the Helicopter Engines Market, Utility / Cargo Helicopters segment expected to grow fastest

Military Helicopters emerged as the largest application segment in the Helicopter Engines Market from 2018 to 2025, holding 41.24% of the market. This was attributed to growing defense budgets worldwide, rising purchases of combat and utility helicopters, and ongoing modernization initiatives for attack, transport, reconnaissance, and special mission helicopters. Military helicopters need highly efficient and robust engines that can function in harsh conditions and carry substantial loads.

Utility / Cargo Helicopters are expected to witness the highest growth rate of 7.34% in the 2026-2035 period

By End User, OEM (Original Equipment Manufacturers) segment dominates the Helicopter Engines Market, Aftermarket / MRO Services segment expected to grow fastest

The OEM (Original Equipment Manufacturers) segment maintained the highest end-user share of 36.14% in the Helicopter Engines Market till 2025. This can be attributed to large production levels of new military and civilian helicopters, increased demand for technologically sophisticated engines for new aircraft, and agreements between engine makers and helicopter original equipment manufacturers. Original equipment manufacturers continue to be the main platform for incorporating next-generation engines in new helicopter types.

The Aftermarket / MRO Services segment is projected to register the highest CAGR during the 2026–2035

By Technology, Conventional Engines segment dominates the Helicopter Engines Market, Hybrid-Electric Engines segment expected to grow fastest

The Conventional Engines segment maintained the highest technology share of approximately 62.71% in the Helicopter Engines Market till 2025. This is attributed to the extensive use of conventional turboshaft and piston engines in the present fleet of helicopters in both the civil, commercial, and military sectors owing to the high reliability, availability, maintenance structure, and ease of adoption than new engines.

The Hybrid-Electric Engines segment is projected to register the highest CAGR during the 2026–2035

Helicopter Engines Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

34.33% |

|

Europe |

Germany |

27.14% |

|

Asia Pacific |

China |

23.75% |

|

Middle East & Africa |

UAE |

6.04% |

|

Latin America |

Brazil |

8.74% |

North America Helicopter Engines Market Insights

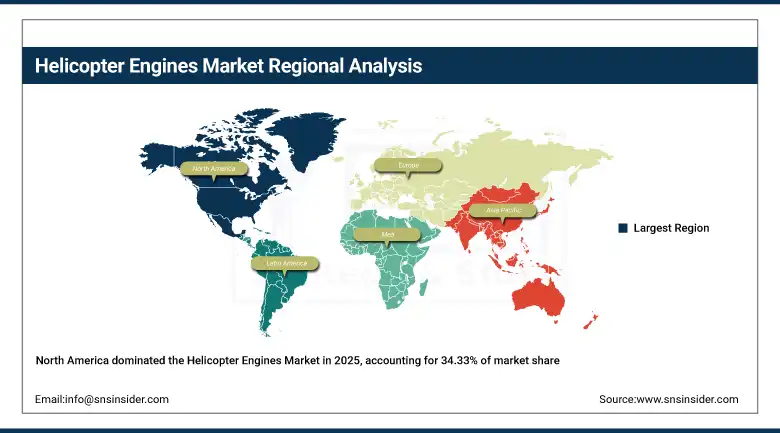

North America was the leading market for the global Helicopter Engines Market with around 34.33% share of revenues in 2025, because of the significant defense budget, large rotorcraft inventory for military applications, robust local OEM and engine industry base, and constant improvements to combat, transport, and utility helicopter fleets. In North America, the United States dominated the market, which benefited from several significant projects, including the United States Army’s Improved Turbine Engine Program (ITEP), Future Vertical Lift (FVL) programs, and existing rotorcraft fleet upgrade programs.

Get Customized Report as per Your Business Requirement - Enquiry Now

Supporting this dominance, the U.S. Department of Defense continues to increase investments in next-generation propulsion systems, engine upgrades, and sustainment programs to improve mission readiness and operational efficiency.

In addition, in 2024–2025, GE Aerospace continued advancing the T901-GE-900 engine under ITEP for the UH-60 Black Hawk and AH-64 Apache fleets, reinforcing North America’s leadership in helicopter engine innovation and military rotorcraft modernization.

Asia Pacific Helicopter Engines Market Insights

The Asia-Pacific region is forecasted to grow at a CAGR of 5.50%, and can be largely attributed to increased defense spending, increase in production of helicopters in the indigenous industry, increased civil helicopter fleet operations, and improvements in the infrastructure for emergency operations and utility aviation. Some of the main factors responsible for the growth of the market are countries such as China, India, Japan, South Korea, and Australia, among which China is the highest revenue generating country.

Additionally, China has accelerated production of indigenous military and civil helicopters, while India continues to expand domestic rotorcraft programs through Hindustan Aeronautics Limited (HAL) and related engine development initiatives.

Europe Helicopter Engines Market Insights

Europe held the second-largest revenue share in the global Helicopter Engines Market, accounting for approximately 27.20% in 2025, fueled by the substantial presence of helicopter and engine OEMs, rising demand for emergency medical services (EMS) and offshore transport helicopters, and modernization of military aircraft fleets. Nations including France, Germany, the UK, and Italy are major players, boosted by research into advanced propulsion systems and sustainable aviation programs.

Supporting this position, Safran Helicopter Engines, Rolls-Royce Holdings plc, and MTU Aero Engines AG continue to expand engine manufacturing, MRO capabilities, and hybrid-electric propulsion R&D.

In addition, in 2024, Safran Helicopter Engines advanced its hybrid-electric propulsion demonstrator programs, supporting Europe’s position as a hub for sustainable rotorcraft engine innovation.

Middle East & Africa and Latin America Helicopter Engines Market Insights

MEA & Latin America are key markets for the growth of the Helicopter Engines Market, attributed to the increasing modernization of the defense sector, the growing demand for offshore oil & gas exploration, and increasing applications of helicopters in surveillance, VIP transport, and rescue operations. Key countries driving the market growth in the MEA region are Saudi Arabia, UAE, Israel, and South Africa due to increased defense procurement.

In Latin America, countries such as Brazil, Mexico, and Colombia are driving demand due to expanding offshore operations, law enforcement aviation, and medical evacuation services. Brazil remains the largest regional contributor, supported by civil helicopter demand and military fleet sustainment programs.

Additionally, in 2024–2025, several Gulf countries increased procurement of advanced military helicopters and engine maintenance contracts, while Brazil expanded helicopter fleet modernization and support programs for offshore and security operations.

Helicopter Engines Market Growth Drivers:

-

Rising global demand for next-generation helicopter propulsion systems driven by military modernization, offshore transport expansion, and increasing adoption of advanced civil rotorcraft fleets is the primary structural growth driver of the Helicopter Engines Market

The Helicopter Engines Market is witnessing transformational changes due to increasing demands from all over the world for high-efficiency and high-performance rotorcraft that can perform their tasks under varying conditions. The armed forces of the United States, European countries, and Asia Pacific region are replacing their aging fleets of helicopters with advanced turboshaft engines capable of performing various missions ranging from transporting troops, conducting military missions, surveillance, and providing logistical support. In parallel, civil and commercial helicopter operators are increasingly adopting helicopters for offshore oil and gas drilling, emergency services, search and rescue operations, and urban transportation, all of which have greater requirements for engines in terms of efficiency and performance.

In addition, according to ICAO rotorcraft operational data trends, global helicopter utilization in offshore energy operations and emergency medical services has increased steadily over the past decade, particularly in regions such as North America, the North Sea basin, and Asia-Pacific offshore hubs. This is complemented by increasing investments from OEMs such as Safran Helicopter Engines, GE Aerospace, and Rolls-Royce in FADEC-enabled, hybrid-electric, and SAF-compatible propulsion technologies.

Helicopter Engines Market Restraints:

-

High acquisition, certification, and lifecycle maintenance costs of advanced helicopter engine systems limiting adoption among smaller operators and cost-sensitive civil aviation segments is a key restraint for the Helicopter Engines Market

The Helicopter Engines Market is severely hampered by the prohibitively high initial and operating costs related to the production of advanced turboshaft and hybrid propulsion engines. High-performance engines designed either for military purposes or high-end civilian applications such as offshore and emergency medical services have extremely high costs due to the high expense not just of procuring them but also integrating and testing them into the airframe system, including the required maintenance equipment. Original Equipment Manufacturers (OEMs) such as Safran Helicopter Engines, GE Aerospace, and Rolls-Royce utilize highly advanced FADEC-equipped engines with high power density that increase the cost per unit.

Helicopter Engines Market Opportunities:

-

Accelerating adoption of next-generation lightweight, fuel-efficient, and digitally optimized helicopter engines is creating strong growth opportunities across urban air mobility, emergency response, and next-generation rotary aviation platforms

The Helicopter Engines Market is poised to enter an era of significant opportunities fueled by the shift towards light, energy-efficient, and technologically connected engines developed for future aviation applications. With increased innovations in the development of highly efficient turboshaft engines that have superior power-to-weight performance and lower fuel consumption, it will be easier to adopt helicopter technology in urban high-frequency transportation networks, time-sensitive medevac missions, and disaster relief missions. Additionally, the advent of UAM/AAM ecosystems has presented new market opportunities for the development of small-size helicopter engines suitable for short-range and highly reliable missions.

Recent Developments:

-

2026: Safran Helicopter Engines expanded testing and early deployment of its next-generation Aneto and Arrano turboshaft engine families, focusing on improved fuel efficiency, higher power-to-weight ratios, and extended maintenance intervals.

-

2025: GE Aerospace accelerated development and validation of advanced FADEC-enhanced turboshaft engines for Future Vertical Lift (FVL) and next-generation military rotorcraft programs in collaboration with the U.S. Department of Defense.

-

2024: Rolls-Royce strengthened its helicopter propulsion portfolio by advancing its M250 and AE series engine upgrade programs, focusing on performance enhancement, reduced lifecycle costs, and improved reliability for civil and defense applications. The company also expanded hybrid-electric propulsion demonstrator testing for rotary-wing platforms, targeting future urban air mobility and next-generation light helicopter segments.

-

2024: Hindustan Aeronautics Limited (HAL) progressed indigenous helicopter engine development initiatives, including expansion of its Shakti engine program (in collaboration with Safran), supporting India’s light combat helicopter (LCH) and advanced light helicopter (ALH) platforms.

Helicopter Engines Companies are:

-

Safran Helicopter Engines

-

Pratt & Whitney Canada

-

Rolls-Royce Holdings plc

-

Honeywell Aerospace

-

Kawasaki Heavy Industries, Ltd.

-

MTU Aero Engines AG

-

ITP Aero

-

PBS Group

-

Aero Engine Corporation of China (AECC)

-

Hindustan Aeronautics Limited (HAL)

-

Klimov JSC

-

Motor Sich JSC

-

Turbomeca SA

-

Light Helicopter Turbine Engine Company (LHTEC)

-

Avio Aero

-

Turbotech SAS

-

Ivchenko-Progress

-

Kont Engine

Helicopter Engines Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 18.00 Billion |

| Market Size by 2035 | USD 27.52 Billion |

| CAGR | CAGR of 4.47% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Engine Type (Turboshaft Engines, Piston Engines, Hybrid / Electric Propulsion Engines, Others) • By Power Output (1,000–3,000 shp,Below 1,000 shp, Above 3,000 shp) • By Component (Compressor, Combustion Chamber, Turbine, Gearbox / Transmission, FADEC / Control System) • By Application (Military Helicopters,Civil & Commercial Helicopters, Emergency Medical Services (EMS) / Rescue Helicopters, Offshore Transport Helicopters, Utility / Cargo Helicopters) • By End User (OEM / Original Equipment Manufacturers, Aftermarket / MRO Services, Defense Forces, Commercial Operators) • By Technology (Conventional Engines, FADEC-Enabled Engines, Hybrid-Electric Engines, Sustainable Aviation Fuel (SAF)-Compatible Engines) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | GE Aerospace, Safran Helicopter Engines, Pratt & Whitney Canada, Rolls-Royce Holdings plc, Honeywell Aerospace, RTX Corporation, Kawasaki Heavy Industries, Ltd., MTU Aero Engines AG, ITP Aero, PBS Group, Aero Engine Corporation of China (AECC), Hindustan Aeronautics Limited (HAL), Klimov JSC, Motor Sich JSC, Turbomeca SA, Light Helicopter Turbine Engine Company (LHTEC), Avio Aero, Turbotech SAS, Ivchenko-Progress, Kont Engine |

Frequently Asked Questions

The Helicopter Engines Market is expected to grow at a CAGR of 4.47% from 2026 to 2035.

The Helicopter Engines Market was valued at USD 18.00 billion in 2025.

Rising global demand for high-performance, fuel-efficient, and mission-ready rotorcraft across defense modernization programs, offshore transport operations, and emergency medical services is the primary growth driver of the Helicopter Engines Market.

The Turboshaft Engines Type dominated the Helicopter Engines Market in 2025.

North America dominated the Helicopter Engines Market in 2025.

Get in Touch