Infrared Sensor Market Report Scope & Overview:

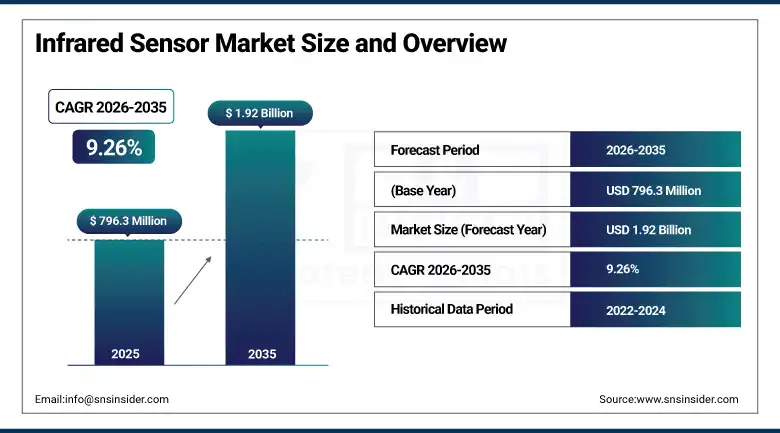

The Infrared Sensor Market was valued at USD 796.3 Million in 2025 and is expected to reach USD 1.92 Billion by 2035, growing at a CAGR of 9.26% from 2026–2035.

The global infrared sensor market is advancing as infrared radiation detection technology penetrates progressively broader application domains beyond its traditional aerospace and industrial strongholds into consumer electronics, automotive safety, smart building, healthcare diagnostics, and environmental monitoring. Infrared sensors detect electromagnetic radiation in the 0.7 to 1000 micrometre wavelength range through photodetector or thermal detection mechanisms whose selection depends on the specific wavelength, sensitivity, resolution, and temperature operating range requirements of the target application. Rising demand for contactless temperature measurement validated during COVID-19 pandemic response, autonomous vehicle ADAS thermal imaging for pedestrian detection, and smart building occupancy sensing through passive infrared motion detection are creating structural demand growth across multiple simultaneously expanding application categories.

In 2024, FLIR Systems (Teledyne Technologies) launched its Boson+ thermal imaging module for automotive ADAS applications, delivering uncooled long-wave infrared imaging at 640×512 resolution in a compact form factor compatible with automotive system-on-chip integration. The product addressed the growing demand from automotive OEMs for standardized thermal imaging sensor modules whose cost, size, and interface specifications are compatible with passenger vehicle bill-of-materials economics rather than the specialized aerospace and military thermal imager form factors whose pricing has historically restricted automotive thermal imaging to luxury vehicle categories.

Market Size and Forecast

-

Market Size in 2026E: USD 869.8 Million

-

Market Size by 2035: USD 1.92 Billion

-

CAGR: 9.26% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Infrared Sensor Market - Request Free Sample Report

Infrared Sensor Market Trends

-

Uncooled microbolometer infrared detector cost reduction is enabling mainstream automotive ADAS thermal imaging adoption in mid-range vehicle categories.

-

Low-power pyroelectric infrared sensor designs are enabling battery-powered smart building occupancy sensing and IoT presence detection deployments.

-

SWIR and MWIR sensor integration in autonomous vehicle perception systems is improving pedestrian and obstacle detection reliability in adverse weather conditions.

-

Non-dispersive infrared gas sensor adoption for indoor air quality monitoring and industrial gas leak detection is creating growing NDIR sensor procurement.

-

Infrared spectroscopy miniaturization is enabling handheld food quality assessment, pharmaceutical verification, and environmental monitoring instruments.

The U.S. Infrared Sensor Market Outlook

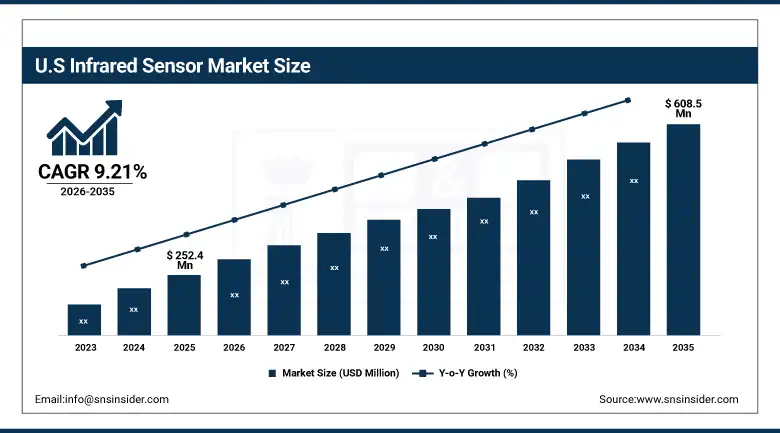

The U.S. Infrared Sensor Market was valued at approximately USD 252.4 Million in 2025 and is expected to reach approximately USD 608.5 Million by 2035, growing at a CAGR of approximately 9.21%.

The United States leads North American revenues through its dominant aerospace and defense infrared sensor procurement, the world’s most active ADAS sensor development investment at automotive and tier-1 supplier R&D centres, and NIH-funded medical infrared diagnostics research. FLIR Systems, Teledyne Technologies, and L3Harris Technologies sustain U.S. technical leadership in cooled and uncooled infrared detector technology. Department of Defense investment in next-generation thermal sighting systems, multispectral imaging, and airborne surveillance sensor modernization creates sustained government-funded infrared sensor procurement that supports the technology frontier from which commercial applications progressively derive.

In 2023, Honeywell International launched advanced non-dispersive infrared gas sensors for industrial safety applications, incorporating dual-wavelength optical bench designs that provide enhanced selectivity, reduced false alarm rates, and self-diagnostic capability for continuous unattended monitoring in petrochemical processing, offshore platforms, and confined space entry applications. The product demonstrated the growing commercial sophistication of industrial NDIR sensor specifications whose optical precision, long-term drift stability, and environmental resistance requirements substantially exceed consumer-grade infrared sensor performance.

Infrared Sensor Market Segment Analysis

-

By Type, near infrared segment dominated the infrared sensor market with approximately 34.8% share in 2025, while the far infrared segment is the fastest growing with a CAGR of approximately 11.4% driven by thermal imaging, security surveillance, and ADAS adoption.

-

By Technology, uncooled infrared sensors segment dominated the infrared sensor market with the largest share in 2025, while cooled infrared sensors retain premium positioning in high-sensitivity aerospace, defense, and scientific applications.

-

By Application, motion detection & occupancy sensing segment dominated the infrared sensor market with approximately 28.5% share in 2025, while the gas & fire detection segment is the fastest growing application with a CAGR of approximately 11.8%.

-

By End Use, aerospace & defense segment dominated the infrared sensor market with approximately 24.3% share in 2025, while the healthcare segment is the fastest growing end use with a CAGR of approximately 12.6% driven by non-contact diagnostics and patient monitoring.

By Type, near infrared dominates, far infrared grows fastest

Near infrared retained the dominant type position with approximately 34.8% of the infrared sensor market in 2025. NIR sensors’ commercial primacy reflects their wide deployment across proximity sensing in smartphones, short-range LiDAR in industrial automation, spectroscopic analysis in pharmaceutical quality control, and biometric authentication systems whose fingerprint and facial recognition functions rely on near-infrared illumination and detection. The extensive installed base of NIR photodetectors in consumer electronics, the broad material compatibility of silicon photodiodes with the 750-900nm NIR range, and the cost efficiency of silicon-based NIR detection relative to compound semiconductor alternatives for longer-wave infrared detection sustain NIR sensor specification dominance across cost-sensitive high-volume applications.

Far infrared is growing fastest at approximately 11.4% CAGR because the thermal imaging applications it enables are experiencing simultaneous demand expansion across multiple markets whose individual growth rates combine to create above-market aggregate FIR sensor demand growth. ADAS thermal imaging whose pedestrian detection in low-visibility conditions requires long-wave infrared passive sensing, industrial process temperature monitoring whose non-contact thermal measurement at elevated temperatures exceeds NIR sensor operating limits, and security surveillance whose perimeter detection requires 24-hour passive thermal imaging collectively create a growing multi-sector FIR demand base whose commercial momentum is self-reinforcing as declining uncooled FIR detector costs create adoption in previously cost-prohibitive applications.

By End Use, aerospace & defense dominates, healthcare grows fastest

Aerospace and defense retained the dominant end use position with approximately 24.3% of the infrared sensor market in 2025. The military’s operational dependence on thermal imaging for night vision, target acquisition, missile seeker heads, and intelligence, surveillance, and reconnaissance systems creates non-discretionary defense budget allocation to infrared sensor procurement whose military specification requirements, programme acquisition processes, and long operational lifetime expectations sustain the aerospace and defense segment’s revenue leadership through defense capital budget cycles whose magnitude per sensor unit substantially exceeds commercial equivalent applications. FLIR, Raytheon, and L3Harris’ defense contract backlogs create multi-year forward procurement commitments that sustain consistent revenue irrespective of short-term commercial market fluctuations.

Healthcare is growing fastest at approximately 12.6% CAGR because the expanding applications of infrared sensors in non-contact patient temperature measurement, vein imaging for venipuncture guidance, infrared spectroscopy for tissue oxygenation and glucose monitoring, and thermal imaging for inflammation and perfusion assessment create a growing clinical utility portfolio whose regulatory approval and clinical evidence accumulation is progressively supporting reimbursement and standard-of-care adoption. Each FDA-cleared infrared diagnostic device creates healthcare system procurement across the hospitals and clinics adopting the technology whose clinical workflow integration sustains recurring sensor module replacement and system upgrade procurement.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

26.8% |

|

Asia Pacific |

China |

38.5% |

|

Middle East & Africa |

Israel |

28.4% |

|

Latin America |

Brazil |

43.8% |

North America Infrared Sensor Market Insights

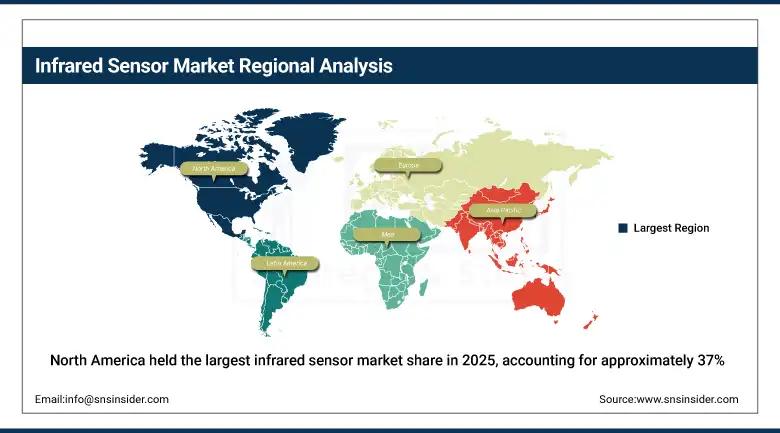

North America held the largest infrared sensor market share in 2025, accounting for approximately 37% of total market revenue. This is driven by its dominant aerospace and defense sector infrared procurement, advanced automotive ADAS technology development investment, and mature industrial and consumer electronics infrared sensor adoption. The United States accounts for approximately 82.5% of North American revenues through Department of Defense thermal imaging system programmes, FLIR Systems and Teledyne Technologies’ commercial leadership, and the automotive industry’s ADAS thermal camera development investment at Michigan and California research centres.

Canada contributes supplementary North American revenues through its growing ADAS sensor research sector, mining industry’s thermal imaging adoption for equipment monitoring and personnel safety in underground operations, and the agricultural technology sector’s infrared sensor deployment for crop health monitoring and irrigation management in precision farming applications whose thermal imaging and NDVI sensor integration is progressively becoming standard practice.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Infrared Sensor Market Insights

Europe is a technically sophisticated infrared sensor market where defense procurement, industrial process monitoring, automotive safety system development, and scientific instrumentation create diverse and high-value application demand. Germany accounts for approximately 26.8% of European revenues through its automotive industry’s leading role in ADAS thermal camera integration, the industrial automation sector’s thermal process monitoring investment, and JENOPTIK and Infratec’s domestic infrared sensor manufacturing presence that sustains European technology independence in critical sensor categories.

France’s LYNRED and Sofradir infrared detector manufacturing, the United Kingdom’s Selex ES (now Leonardo) infrared sensor production for defense applications, and Switzerland’s precision scientific instrument sector collectively sustain European infrared sensor manufacturing capability that serves both domestic and export markets. The EU’s defense technology investment under the European Defense Fund and the automotive industry’s mandatory ADAS safety feature roadmap create structured institutional procurement that sustains European market development above baseline commercial demand.

Asia Pacific Infrared Sensor Market Insights

Asia Pacific is the fastest-growing regional infrared sensor market, driven by rapid industrialization creating process monitoring demand, consumer electronics integration of infrared proximity and gesture sensing, the automotive industry’s progressive ADAS adoption, and government investment in smart city and security surveillance infrastructure. China accounts for approximately 38.5% of Asia Pacific revenues through its large manufacturing sector’s thermal process monitoring adoption, the government’s extensive security surveillance thermal camera deployment, and growing domestic ADAS sensor manufacturing capability development.

Japan’s precision infrared sensor manufacturing through Hamamatsu Photonics and Panasonic, South Korea’s Samsung and LG Electronics’ consumer electronics infrared sensor integration, and Taiwan’s advanced semiconductor-based infrared detector manufacturing collectively sustain Asia Pacific’s premium technology contribution to the regional market. India’s growing defense sector infrared procurement and industrial automation investment create an emerging secondary market whose growth rate is accelerating with domestic manufacturing investment.

MEA & Latin America Infrared Sensor Market Insights

Israel leads MEA revenues through its world-class defense infrared sensor technology base at Elbit Systems and Rafael Advanced Defense Systems, the domestic security sector’s thermal surveillance investment, and growing commercial infrared sensor manufacturing whose export-oriented production serves global aerospace and defense customers. The UAE and Saudi Arabia contribute growing civil and defense infrared sensor demand through smart city security surveillance infrastructure and military system modernization programmes.

Brazil leads Latin American revenues at approximately 43.8% through its oil and gas sector’s infrared gas detection investment, agricultural sector’s aerial thermal imaging adoption for crop monitoring and disease detection in its enormous soybean and sugarcane production area, and defense sector’s border surveillance thermal imaging procurement. Mexico and Chile contribute growing secondary demand through their mining and industrial sectors’ thermal process monitoring investment.

Market Dynamics

Growth Drivers: ADAS thermal imaging proliferation into mainstream vehicle categories and industrial IoT creating structural infrared sensor demand growth

The infrared sensor market’s most commercially significant structural growth driver is the automotive industry’s progressive adoption of ADAS thermal imaging from luxury-only to mainstream vehicle categories as uncooled micro-bolometer detector cost reductions through manufacturing scale and process improvement make thermal camera economics compatible with mid-range vehicle bill-of-materials constraints. Each percentage point increase in automotive thermal camera penetration rate across global annual vehicle production of approximately 85 million units creates millions of additional infrared sensor procurement events whose aggregate multiplies with penetration rate growth. Industrial IoT deployment of infrared temperature monitoring, gas detection, and flame sensing in manufacturing, energy, and petrochemical processing facilities creates a parallel structural demand driver whose non-discretionary safety regulation compliance motivation sustains procurement through industrial capital expenditure cycles.

Restraints: High cost of cooled infrared detectors and strategic export restrictions on advanced infrared materials limiting market access

Cooled infrared detector systems using InSb, HgCdTe, and quantum well infrared photodetector technologies whose cryogenic cooling requirements add mechanical complexity, power consumption, and maintenance burden create high total cost of ownership barriers that restrict their adoption to applications whose performance requirements for higher sensitivity, faster response, and longer-wave detection capability justify the additional system cost. The export control classification of advanced infrared detector materials and system specifications under U.S. ITAR and EAR regulations, and equivalent European and allied nation strategic export control frameworks, creates market access restrictions that limit commercial infrared sensor trade across political boundaries and increase compliance burden for international supply chains. Pyroelectric and thermopile sensor raw material supply chain concentration for lithium tantalate and PVDF pyroelectric materials creates procurement risk.

Opportunities: Consumer electronics infrared integration expansion and smart building energy management creating high-volume infrared sensor application categories

The expansion of infrared sensor integration into consumer electronics beyond smartphone proximity sensing into gesture recognition, augmented reality depth sensing, and health monitoring creates a high-volume application category whose annual device production volumes could approach MEMS microphone scale if adoption follows the trajectory of proximity sensor integration in preceding device generations. Apple’s TrueDepth camera system’s infrared dot projector and flood illuminator integration in Face ID, and the growing deployment of 3D infrared sensing in premium Android smartphones, demonstrate the commercial feasibility of sophisticated infrared sensor system integration in consumer devices at mass-market price points. Smart building energy management whose occupancy-sensing-based HVAC, lighting, and security system optimization creates commercial motivation for passive infrared sensor installation across commercial building floor areas representing billions of square metres of global commercial real estate.

Recent Developments:

-

2024: FLIR Systems (Teledyne Technologies) launched its Boson+ thermal imaging module for automotive ADAS applications, delivering uncooled LWIR imaging at 640×512 resolution in a compact automotive-compatible form factor, targeting mass-market vehicle integration at mid-range price points.

-

2023: Honeywell International launched advanced NDIR gas sensors for industrial safety applications incorporating dual-wavelength optical bench design for enhanced gas selectivity, reduced false alarms, and self-diagnostic capability for continuous unattended petrochemical and confined space monitoring.

-

2023: Hamamatsu Photonics introduced its InGaAs linear image sensor with extended SWIR response to 2600nm wavelength for food inspection, solar cell characterisation, and pharmaceutical quality control applications requiring sensitive short-wave infrared spectroscopic analysis.

Infrared Sensor Market Key Players are:

-

FLIR Systems Inc. (Teledyne Technologies)

-

Hamamatsu Photonics KK

-

Texas Instruments Incorporated

-

Honeywell International Inc.

-

Murata Manufacturing Co. Ltd.

-

Excelitas Technologies Corp.

-

InfraTec GmbH

-

JENOPTIK AG

-

Raytheon Technologies Corporation

-

L3Harris Technologies Inc.

-

Leonardo DRS (Leonardo SpA)

-

Lynred SAS

-

Vigo System SA

-

Heimann Sensor GmbH

-

Caliente LLC (Dexter Research)

-

Panasonic Holdings Corporation

-

Elbit Systems Ltd.

-

SCD (Semi Conductor Devices)

-

New Infrared Technologies SL

-

Spectrogon AB

Infrared Sensor Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 796.3 Million |

| Market Size by 2035 | USD 1.92 Billion |

| CAGR | CAGR of 9.26% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Near Infrared, Short-Wave Infrared, Mid-Wave Infrared, Far Infrared/Long-Wave Infrared) • By Technology (Cooled Infrared Sensors, Uncooled Infrared Sensors) • By Application (Motion Detection & Occupancy Sensing, Temperature Measurement, Gas & Fire Detection, Image & Vision Systems, Others) • By End Use (Aerospace & Defense, Consumer Electronics, Automotive, Industrial, Healthcare, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | FLIR Systems Inc. (Teledyne Technologies), Hamamatsu Photonics KK, Texas Instruments Incorporated, Honeywell International Inc., Murata Manufacturing Co. Ltd., Excelitas Technologies Corp., InfraTec GmbH, JENOPTIK AG, Raytheon Technologies Corporation, L3Harris Technologies Inc., Leonardo DRS (Leonardo SpA), Lynred SAS, Vigo System SA, Heimann Sensor GmbH, Caliente LLC (Dexter Research), Panasonic Holdings Corporation, Elbit Systems Ltd., SCD (Semi Conductor Devices), New Infrared Technologies SL, and Spectrogon AB |

Frequently Asked Questions

The Infrared Sensor Market is expected to grow at a CAGR of 9.26% from 2026 to 2035.

The Infrared Sensor Market was valued at USD 796.3 Million in 2025.

ADAS thermal imaging adoption in mainstream vehicle categories, industrial IoT infrared temperature and gas monitoring investment, and expanding healthcare non-contact diagnostic applications are the primary growth factors driving the Infrared Sensor Market.

Aerospace & Defense dominated the Infrared Sensor Market with approximately 24.3% share in 2025.

North America dominated the Infrared Sensor Market in 2025.

Get in Touch