Chronic Kidney Disease Market Report Scope & Overview:

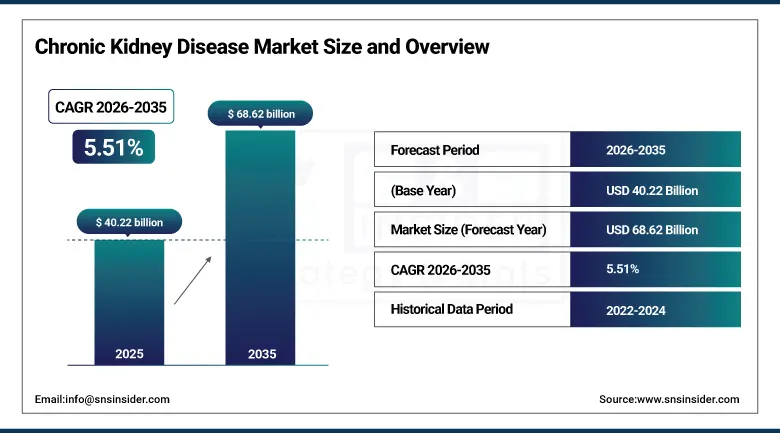

The Chronic Kidney Disease Market was estimated at USD 40.22 billion in 2025 and is expected to reach USD 68.62 billion by 2035 and grow at a CAGR of 5.51% over the forecast period of 2026-2035.

The global chronic kidney disease market is navigating a period of profound clinical and commercial transformation driven by the convergence of several distinct but reinforcing forces: the epidemiological inevitability of rising CKD prevalence as ageing populations, escalating rates of type 2 diabetes, and persistently undertreated hypertension collectively expand the diagnosed patient population across every major geography; the arrival of a genuinely transformative therapeutic class in sodium-glucose cotransporter-2 inhibitors that for the first time provide a mechanism to meaningfully slow CKD progression in diabetic and non-diabetic patients; and the growing recognition within nephrology and primary care communities that early CKD identification through expanded screening programmes can shift the clinical trajectory of the disease toward management rather than progression. The WHO’s estimate that over 850 million people globally live with some form of kidney disease, combined with the sobering statistic that fewer than 10% are diagnosed during the clinically actionable early stages when intervention can most meaningfully alter disease course, defines both the enormous unmet clinical need that underlies long-term market demand growth and the public health imperative driving national screening programme investment across high and middle-income health systems. The pharmaceutical pipeline for CKD has undergone a genuine renaissance following decades of limited therapeutic progress, with SGLT2 inhibitors like dapagliflozin and empagliflozin having demonstrated cardiovascular and renal outcome benefits in landmark trials, GLP-1 receptor agonists showing emerging nephroprotective signals, and a new generation of targeted therapies addressing the underlying inflammatory, fibrotic, and metabolic pathophysiology of CKD progression across multiple distinct mechanisms of action.

The January 2025 FDA approval of semaglutide for CKD risk reduction in type 2 diabetes patients, building on earlier approvals of dapagliflozin and empagliflozin for the same indication, marks the crystallisation of a new era in CKD pharmacotherapy where oral agents with robust cardiovascular and renal outcome evidence are becoming the foundation of multidrug regimens that can be managed in primary care settings, substantially expanding the treated patient population beyond the nephrology specialist-dependent management model that historically limited therapeutic market penetration.

Market Size and Forecast

- Market Size in 2026E: USD 42.44 Billion

- Market Size by 2035: USD 68.62 Billion

- CAGR: 5.51% from 2026 to 2035

- Fastest Growing Region: Asia Pacific

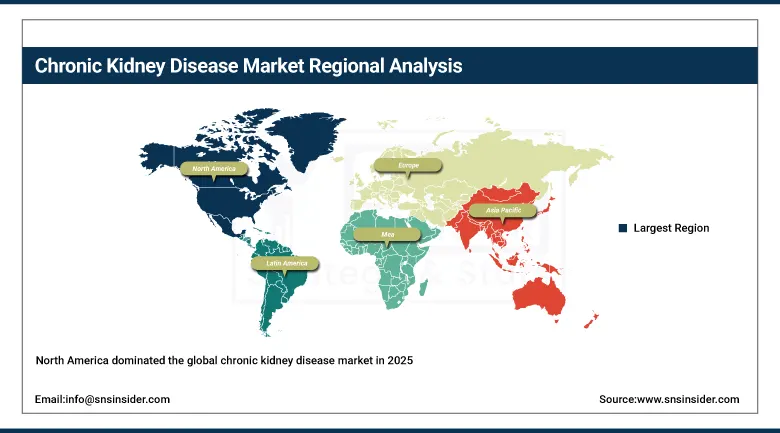

- Largest Region: North America

To Get more information on Chronic Kidney Disease Market - Request Free Sample Report

Chronic Kidney Disease Market Trends

- Rapid adoption of SGLT2 inhibitors as the new foundation of CKD pharmacotherapy across diabetic and non-diabetic patient populations, following the demonstration in landmark cardiovascular and renal outcome trials that dapagliflozin, empagliflozin, and canagliflozin significantly reduce the risk of kidney disease progression, dialysis initiation, and cardiovascular death in broad CKD patient populations beyond the type 2 diabetes indication in which the class was originally developed.

- Expanding deployment of tele-nephrology platforms and remote patient monitoring technologies that extend specialist kidney care oversight to rural and underserved patient populations who lack geographic access to nephrology centres, enabling more frequent assessment of kidney function biomarkers, blood pressure control, fluid status, and medication adherence between in-person consultations through connected monitoring devices and digital health applications integrated with electronic health record systems.

- Growing investment in home dialysis modalities including peritoneal dialysis and home haemodialysis as healthcare system payers and patients increasingly recognise the quality of life, clinical outcome, and cost advantages of home-based renal replacement therapy relative to three-times-weekly in-centre haemodialysis, with technology improvements in home dialysis machine usability, automated peritoneal dialysis cycler software, and telehealth-enabled clinical support making home dialysis an increasingly accessible and appealing option for appropriate patients.

- Increasing use of artificial intelligence and machine learning tools in CKD risk stratification, progression prediction, and care pathway optimisation, with AI-driven algorithms applied to electronic health record data identifying high-risk patients for proactive nephrology referral before creatinine-based staging criteria are met, enabling the earlier intervention that clinical evidence consistently identifies as the most impactful determinant of long-term renal outcome.

- Rising commercial interest in novel CKD therapeutic targets beyond SGLT2 inhibition, including endothelin receptor antagonists, mineralocorticoid receptor antagonists, anti-fibrotic agents, complement pathway inhibitors, and precision medicine approaches targeting the specific genetic and molecular pathophysiology of immunoglobulin A nephropathy, focal segmental glomerulosclerosis, and other primary glomerular CKD causes that have historically lacked disease-modifying pharmacotherapy.

U.S. Chronic Kidney Disease Market Outlook

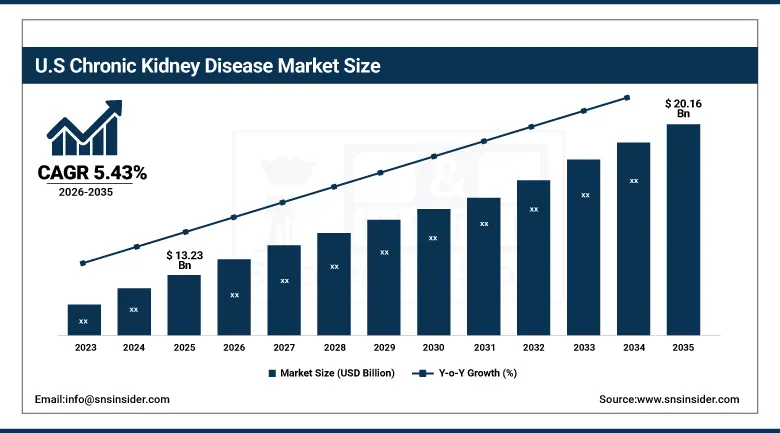

The U.S. chronic kidney disease market was valued at approximately USD 13.23 Billion in 2025 and is expected to reach approximately USD 20.16 Billion by 2035, growing at a CAGR of 5.43%, driven by the highest absolute CKD patient population in the developed world resulting from the combination of the world’s highest rates of type 2 diabetes and hypertension among a large and ageing population, the most extensively developed commercial dialysis network globally operated primarily by DaVita and Fresenius Medical Care, and a pharmaceutical market structure that rapidly adopts and remunerates innovative CKD therapies at pricing levels that reflect their outcome benefits.

The United States accounts for the dominant share of North American CKD market revenues through a treatment ecosystem that encompasses the world’s largest network of outpatient dialysis facilities, with over 7,500 freestanding dialysis centres serving approximately 550,000 end-stage renal disease patients on maintenance haemodialysis or peritoneal dialysis, alongside a rapidly growing transplant waitlist population and a far larger upstream pool of pre-dialysis CKD stages 1 through 4 patients managed across nephrology practices, endocrinology clinics, and primary care settings throughout the country. Medicare’s role as the primary payer for end-stage renal disease care through the ESRD benefit that provides coverage for dialysis and transplant services regardless of patient age creates a stable, government-backed revenue foundation for the dialysis service and CKD pharmaceutical market segments that reduces commercial exposure to insurance market volatility while creating a politically sensitive cost pressure environment where the Centers for Medicare and Medicaid Services actively monitors and regulates ESRD spending through prospective bundled payment systems and quality incentive programmes. The Kidney Health Initiative and broader policy environment supporting kidney disease prevention and transplantation access under successive administrations has elevated CKD to a national health priority with dedicated funding streams for research, screening programme expansion, and living donor kidney transplantation promotion that collectively support market development across the full CKD care continuum from prevention through end-stage treatment.

The growing recognition among U.S. healthcare payers that proactive CKD management through aggressive cardiovascular risk factor control, early SGLT2 inhibitor initiation, and regular nephrology monitoring produces dramatically lower long-term dialysis initiation costs than the standard of care reactive management approach is creating meaningful insurer-driven implementation support for CKD population health management programmes that simultaneously improve patient outcomes and reduce the projected total cost of care for high-risk diabetic and hypertensive patient populations.

Chronic Kidney Disease Market Segment Analysis

-

By Diagnosis, Blood Test led with the largest share as the primary initial screening and monitoring tool for CKD through serum creatinine measurement enabling estimated glomerular filtration rate calculation that defines CKD staging across the five clinical categories; Imaging Tests including renal ultrasound, CT scan, and MRI are growing in adoption driven by improved access to diagnostic imaging and increasing recognition of structural renal abnormalities in CKD patient assessment.

-

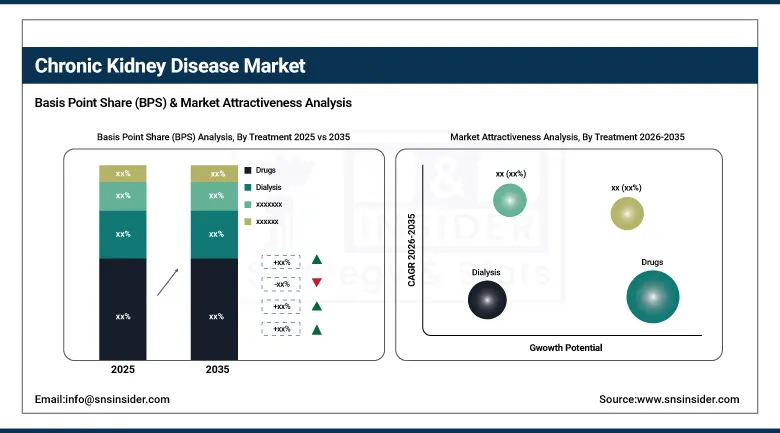

By Treatment, the Drugs segment dominated the Chronic Kidney Disease Market with approximately 44.89% revenue share in 2025 owing to the growing SGLT2 inhibitor, ACE inhibitor, ARB, and erythropoiesis-stimulating agent pharmacotherapy burden across the large pre-dialysis CKD population; Kidney Transplant segment is expected to grow fastest at a CAGR of approximately 6.22% driven by expanding living donor programmes, improved immunosuppression protocols, and growing recognition of transplant’s survival and quality of life advantages over long-term dialysis.

-

By End User, Hospitals and Clinics dominated with approximately 67.85% revenue share in 2025 as the principal sites for dialysis service delivery, kidney transplant surgery, and complex CKD complication management; Diagnostic Centers are the fastest-growing end user segment at a CAGR of approximately 5.77% driven by expanding early CKD screening programme deployment and growing demand for accessible outpatient kidney function testing in high-risk diabetic and hypertensive populations.

Drugs dominate treatment, Kidney Transplant grows fastest

The Drugs segment retained the dominant treatment position with approximately 44.89% of the chronic kidney disease market in 2025, reflecting the extraordinary expansion of the pharmacologically treated pre-dialysis CKD population driven by the commercialisation of SGLT2 inhibitors for CKD indications that has created a new and large prescription drug demand category extending well beyond the established ACE inhibitor, ARB, phosphate binder, and erythropoiesis-stimulating agent prescribing that previously defined CKD pharmacotherapy at earlier disease stages. The FDA’s landmark approvals of dapagliflozin in 2021, empagliflozin in 2023, and semaglutide in January 2025 for CKD-specific indications have collectively transformed the treatment algorithm that nephrologists and primary care physicians apply to early and moderate CKD management, creating substantial new prescription volumes as the evidence base and guideline recommendations cascade from specialist to generalist prescribing, reaching the far larger primary care prescriber community that manages the majority of stages 1 through 3 CKD patients who will form the bulk of the long-term pharmaceutical market growth opportunity. The immunosuppression drug market serving the kidney transplant patient population, including tacrolimus, mycophenolate mofetil, and newer mTOR inhibitor regimens, provides a stable long-term revenue base that grows proportionally with the transplant patient population whose cumulative size is expanding as improved graft survival rates keep more transplant recipients in stable long-term immunosuppression management.

Kidney Transplant is the fastest-growing treatment segment at a CAGR of approximately 6.22% through 2035, propelled by multiple complementary drivers including growing living donor kidney transplant programme expansion supported by policy initiatives that reduce financial and logistical barriers to living donation, improved surgical and immunosuppression protocols that are pushing one-year and five-year graft survival rates to historically high levels across experienced transplant centres, and the growing recognition among nephrologists, patients, and payers that pre-emptive kidney transplantation before dialysis initiation delivers substantially superior long-term patient survival and quality of life outcomes at lower total system cost than the standard pathway of dialysis followed by transplant waitlisting. The persistent shortage of deceased donor organs relative to the waitlisted recipient population remains the binding constraint on transplant volume growth, creating sustained research interest in xenotransplantation approaches using genetically modified porcine kidneys, bioengineered kidney scaffolds, and machine perfusion technologies that could expand the donor organ supply available to address the unmet clinical need that currently results in thousands of preventable deaths annually among patients who die on transplant waiting lists.

Hospitals and Clinics dominate, Diagnostic Centers grow fastest

Hospitals and Clinics retained the dominant end user position with approximately 67.85% of chronic kidney disease market revenues in 2025, reflecting their irreplaceable role as the primary sites for the high-acuity and technically complex CKD care modalities that generate the largest per-patient revenue streams, including in-centre haemodialysis, peritoneal dialysis initiation and training, kidney transplant surgery and peri-operative management, and the management of acute kidney injury and CKD complications including severe anaemia, hyperkalaemia, metabolic acidosis, and cardiovascular events that require hospital-level monitoring and intervention capacity. The integrated health systems operating large nephrology divisions, dedicated CKD multidisciplinary clinics, and comprehensive transplant programmes, including major academic medical centres and the large outpatient dialysis network operators including DaVita and Fresenius Medical Care that collectively manage the treatment of the majority of the U.S. end-stage renal disease population, define the institutional purchasing relationships that pharmaceutical, device, and diagnostic companies prioritise in their CKD market access strategies. Dedicated CKD multidisciplinary clinics that co-locate nephrology, dietetics, pharmacy, social work, and vascular access surgery expertise are demonstrating superior patient preparation for renal replacement therapy modality selection, lower emergency dialysis initiation rates, and higher living donor transplant rates than standard care models, creating an evidence base that is driving their expansion across major health systems in North America and Europe.

Diagnostic Centers are the fastest-growing end user segment at a CAGR of approximately 5.77% through 2035, driven by the structural expansion of early CKD detection as a public health priority that is directing investment toward accessible, community-based kidney function screening infrastructure capable of identifying the vast majority of early-stage CKD patients who are currently missed by the reactive, symptomatic presentation-driven detection model that characterises current CKD diagnosis practice in most health systems. The integration of automated eGFR calculation and UACR measurement into routine annual health check programmes for diabetic and hypertensive patients is creating a massive increase in kidney function testing volume that flows primarily through outpatient diagnostic laboratory networks rather than hospital-based testing infrastructure, expanding diagnostic centre revenues proportionally with screening programme adoption rates across primary care systems in North America, Europe, and increasingly Asia Pacific.

Regional Insights

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

61.7% |

|

Middle East & Africa |

Saudi Arabia |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Chronic Kidney Disease Market Insights

North America dominated the global chronic kidney disease market in 2025, with the United States accounting for approximately 87.4% of North American revenues, driven by the region’s combination of the world’s highest absolute CKD patient burden, the most extensively developed commercial dialysis infrastructure, the most rapid adoption of innovative CKD pharmacotherapy, and a reimbursement environment that adequately compensates the full spectrum of CKD care from early pharmacological management through end-stage renal replacement therapy. The United States CKD market benefits from the unique ESRD Medicare entitlement that provides universal payer coverage for dialysis and transplant services regardless of patient age, creating a government-backed revenue floor for the end-stage treatment market that provides extraordinary commercial stability for the dialysis service companies, transplant programme operators, and immunosuppression drug manufacturers serving this patient population. Canada contributes approximately 12.6% of North American CKD market revenues through a universal healthcare system that maintains broad access to dialysis, transplant, and CKD pharmacotherapy services subject to provincial health technology assessment frameworks that moderate innovative drug adoption speed relative to the U.S. commercial market while ensuring sustained coverage depth across the full treatment spectrum.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Chronic Kidney Disease Market Insights

Europe is a technically sophisticated and comprehensively covered CKD market where universal health coverage systems across virtually all member states ensure broad patient access to dialysis, transplant, and pharmacotherapy services subject to health technology assessment processes that evaluate the cost-effectiveness of innovative CKD treatments before authorising reimbursement at national formulary level. Germany accounts for approximately 22.3% of European CKD revenues as the region’s largest national market, with a statutory health insurance system covering over 90% of the population that provides comprehensive CKD coverage including home dialysis, transplant surgery, and innovative pharmacotherapy within a rigorous health technology assessment framework operated by the Federal Joint Committee that has been navigating the evidence base for SGLT2 inhibitors in CKD with the same rigour applied to all novel therapy classes. The European Renal Association’s clinical practice guidelines, which are progressively updated to incorporate the landmark SGLT2 inhibitor and GLP-1 trial evidence, are driving convergent prescribing pattern shifts across European nephrology practices toward earlier initiation of nephroprotective pharmacotherapy in CKD patients at highest progression risk.

Asia Pacific Chronic Kidney Disease Market Insights

Asia Pacific is the fastest-growing regional CKD market, driven by the extraordinary burden of CKD-predisposing conditions including type 2 diabetes and hypertension across China, India, Japan, South Korea, and Southeast Asian populations, combined with rapidly expanding healthcare infrastructure investment, growing insurance coverage penetration, and improving specialist nephrology capacity that is enabling earlier diagnosis and more comprehensive treatment of the enormous CKD patient population that previously went undetected or inadequately treated due to healthcare access limitations. China accounts for approximately 61.7% of Asia Pacific CKD market revenues and represents the most consequential growth opportunity in global kidney disease care, as the combination of over 130 million diabetic patients generating the world’s largest CKD risk population, rapidly expanding nephrology specialist infrastructure across tier 1 and tier 2 cities, and growing national health insurance coverage enabling pharmaceutical and dialysis service access creates a market development trajectory that international healthcare companies are prioritising with dedicated investment in local clinical evidence generation, regulatory approval strategies, and commercial infrastructure development. Japan and South Korea represent mature secondary markets where advanced dialysis technology adoption, high transplant programme quality, and sophisticated CKD pharmacotherapy prescribing create premium commercial environments for innovative CKD products despite demographic pressures and healthcare budget constraints that moderate market growth rates relative to the dynamic expansion occurring across emerging Asia Pacific markets.

Latin America and MEA Chronic Kidney Disease Market Insights

Latin America and the Middle East and Africa are growing CKD markets where expanding healthcare system coverage, rising diabetes and hypertension prevalence, and government investment in dialysis network capacity are creating sustained market development across patient populations that were previously severely underserved relative to their disease burden and the clinical and economic consequences of untreated progression to end-stage renal disease. Brazil accounts for approximately 44.2% of Latin American CKD revenues through its combination of a universal public healthcare system under the Sistema Unico de Saude that provides dialysis access to the country’s large ESRD population and a growing supplementary private insurance sector serving commercially insured patients with access to innovative pharmacotherapy and premium transplant services at rates above public system standards. Saudi Arabia leads Middle East and Africa CKD revenues at approximately 38.4% of the regional total, driven by the Kingdom’s Vision 2030 healthcare transformation programme investing in expanded dialysis capacity, transplant programme development, and innovative drug access across a patient population with extraordinarily high diabetes and hypertension prevalence generating one of the world’s highest per-capita CKD burdens relative to national population size.

Growth Drivers: Expanding CKD-predisposing disease burden from diabetes and hypertension, transformative SGLT2 inhibitor and GLP-1 pharmacotherapy adoption, and growing dialysis and transplant infrastructure investment across emerging markets

The primary structural growth drivers for the Chronic Kidney Disease Market are the epidemiologically inevitable expansion of the CKD patient population driven by the global diabetes and hypertension epidemics that are generating new CKD cases faster than existing healthcare systems can diagnose and manage them, combined with the arrival of a genuinely transformative pharmacotherapy class in SGLT2 inhibitors that has created a new and large treated patient segment extending well into the early CKD stages that were previously managed expectantly rather than pharmacologically. The International Diabetes Federation’s projection that the global diabetic population will reach 783 million by 2045, with each diabetic patient carrying a lifetime diabetic kidney disease development risk of approximately 30 to 40%, provides the most powerful long-term market demand guarantee in any therapeutic area, defining a CKD incidence pipeline whose size and geographic distribution creates sustained demand growth for diagnostic services, pharmacotherapy, dialysis, and transplant services across every region of the world. Digital health innovation is simultaneously expanding the market’s growth envelope by enabling population-level CKD risk stratification through electronic health record analytics, continuous kidney function monitoring through connected biomarker devices, and tele-nephrology consultation models that extend specialist oversight to the vast primary care-managed CKD population without proportional increases in specialist physician headcount.

Restraints: Donor organ shortage limiting kidney transplant programme growth, dialysis workforce capacity constraints, and health technology assessment barriers to innovative pharmacotherapy reimbursement in cost-constrained health systems

A significant restraint on the Chronic Kidney Disease Market is the persistent and structurally intractable shortage of donor kidneys relative to the transplant waitlist population that prevents transplantation from fully realising its clinical and economic advantages over long-term dialysis despite strong evidence that kidney transplant delivers superior patient survival, quality of life, and long-term cost-effectiveness outcomes. The U.S. kidney transplant waitlist of approximately 90,000 patients against approximately 25,000 transplants performed annually represents a structural mismatch whose resolution requires either dramatic expansion of living donation, development of functionally viable xenogeneic or bioengineered kidneys, or machine perfusion-enabled utilisation of marginal deceased donor organs that are currently declined due to preservation quality concerns, all of which are active areas of research and commercial development but none of which will resolve the gap within the 2026 to 2035 forecast period.

Opportunities: Novel therapeutic targets beyond SGLT2 inhibition expanding the CKD pharmacotherapy pipeline, AI-driven early detection reducing time to diagnosis, and home dialysis technology improvement expanding renal replacement therapy access

The CKD pharmaceutical pipeline represents one of the richest therapeutic development environments in internal medicine, with multiple novel mechanisms of action including non-steroidal mineralocorticoid receptor antagonists such as finerenone, endothelin-1 receptor antagonists, hypoxia-inducible factor prolyl hydroxylase inhibitors, anti-complement therapies for immune-mediated CKD, and precision medicine approaches targeting the specific genetic pathophysiology of IgA nephropathy and other primary glomerular diseases collectively creating the prospect of combination pharmacotherapy regimens that could substantially slow or arrest CKD progression in a far broader patient population than current standard of care pharmacotherapy achieves. Home dialysis technology improvement represents a particularly actionable market development opportunity, as the combination of simplified peritoneal dialysis cycler interfaces, remote monitoring connectivity, and telehealth-enabled clinical support programmes is reducing the practical and psychological barriers to home dialysis adoption that have historically kept home modality penetration rates well below the levels that both clinical evidence and patient preference surveys suggest are achievable in an appropriately supported home dialysis programme infrastructure.

Recent Developments:

-

2025: Novo Nordisk’s semaglutide (Ozempic) received FDA approval to reduce the risk of worsening kidney disease, kidney failure, and cardiovascular death in adults with type 2 diabetes and chronic kidney disease, marking a landmark expansion of GLP-1 receptor agonist indications into nephroprotective therapy and substantially broadening the pharmacological toolkit available for CKD management in the diabetic patient population.

-

2025: AstraZeneca advanced its ongoing clinical programme for farxiga in non-diabetic CKD populations, publishing extended follow-up data from the DAPA-CKD trial confirming durable renal and cardiovascular outcome benefits across diverse CKD patient subgroups and supporting expanded guideline recommendations for SGLT2 inhibitor use in non-diabetic CKD management.

-

2025: Fresenius Medical Care expanded its home dialysis programme infrastructure across Asia Pacific with new patient training centre developments in Australia, South Korea, and Singapore, responding to growing regional healthcare system interest in shifting dialysis modality mix toward home-based alternatives that reduce healthcare facility cost pressure while improving patient quality of life outcomes.

-

2025: DaVita introduced expanded tele-nephrology consultation services integrated into its U.S. dialysis centre network, enabling remote specialist oversight of home dialysis patients and rural CKD patients who lack convenient access to in-person nephrology consultation, improving care continuity and early complication detection for geographically dispersed patient populations.

-

2025: Arch Biopartners acquired a pre-clinical CKD drug development platform targeting interleukin-32, expanding its kidney therapeutics pipeline into next-generation anti-inflammatory CKD drug development aimed at the large non-diabetic CKD patient population underserved by current pharmacotherapy options focused predominantly on cardiometabolic risk factor modification.

Chronic Kidney Disease Market Key Players

-

Fresenius Medical Care AG & Co. KGaA

-

DaVita Inc.

-

AstraZeneca plc

-

Amgen Inc.

-

Abbott Laboratories

-

F. Hoffmann-La Roche Ltd.

-

Baxter International Inc. (Vantive)

-

B. Braun Melsungen AG

-

Medtronic plc

-

Novo Nordisk A/S

-

Boehringer Ingelheim GmbH

-

Eli Lilly and Company

-

Bayer AG

-

Otsuka Holdings Co., Ltd.

-

CSL Vifor

-

Siemens Healthineers AG

-

Beckman Coulter Inc.

-

ACON Laboratories, Inc.

-

Nova Biomedical

-

GlaxoSmithKline plc

Chronic Kidney Disease Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 40.22 Billion |

| Market Size by 2035 | USD 68.62 Billion |

| CAGR | CAGR of 5.51% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Diagnosis (Blood Test, Urine Test, Kidney Biopsy, Imaging Tests) • By Treatment (Drugs, Dialysis, Kidney Transplant) • By Indication (Type 1 CKD, Type 2 CKD, Type 3 CKD, Type 4 CKD, Type 5 CKD) • By End User (Hospitals and Clinics, Diagnostic Centers, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Fresenius Medical Care AG & Co. KGaA, DaVita Inc., AstraZeneca plc, Amgen Inc., Abbott Laboratories, F. Hoffmann-La Roche Ltd., Baxter International Inc. (Vantive), B. Braun Melsungen AG, Medtronic plc, Novo Nordisk A/S, Boehringer Ingelheim GmbH, Eli Lilly and Company, Bayer AG, Otsuka Holdings Co., Ltd., CSL Vifor, Siemens Healthineers AG, Beckman Coulter Inc., ACON Laboratories, Inc., Nova Biomedical, GlaxoSmithKline plc |

Frequently Asked Questions

The Chronic Kidney Disease Market is expected to grow at a CAGR of 5.51% from 2026 to 2035.

The Chronic Kidney Disease Market was valued at USD 40.22 Billion in 2025.

The expanding global CKD patient population driven by diabetes and hypertension epidemics, combined with the arrival of SGLT2 inhibitors and GLP-1 receptor agonists as transformative nephroprotective pharmacotherapy classes that are being adopted across broad pre-dialysis CKD patient populations, and growing healthcare infrastructure investment in dialysis and transplant services across emerging markets that is expanding treatment access for previously underserved patient populations.

Drugs dominated with approximately 44.89% revenue share in 2025.

North America dominated the Chronic Kidney Disease Market in 2025, with the United States as the leading national market within the region.

Get in Touch