Medical Equipment Market Report Scope & Overview:

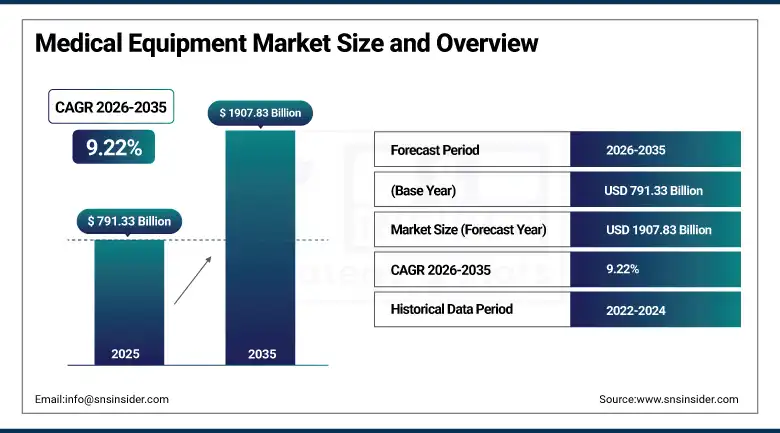

The Medical Equipment Market was valued at USD 791.33 billion in 2025 and is expected to reach USD 1907.83 billion by 2035, growing at a CAGR of 9.22% from 2026–2035.

The medical equipment market is witnessing strong growth in the global market owing to the increasing demand for advanced healthcare infrastructure, early disease diagnosis, and minimally invasive treatment solutions. The rising prevalence of chronic diseases and aging population is promoting the usage of diagnostic imaging systems, surgical instruments, and patient monitoring devices in various healthcare settings. Investments made by organizations in hospital expansion, digital health technologies, and homecare services are contributing to market growth. Increasing developments in medical technology, AI-based diagnostics, and wearable health devices are playing a major role in driving the demand for medical equipment. Growth in healthcare spending and stringent clinical performance requirements are fueling the demand for market.

According to the U.S. Food and Drug Administration Center for Devices and Radiological Health 2025, the agency received more than 21,700 medical device submissions in 2025, reflecting increasing regulatory activity in device approvals and modifications. FDA data also shows over 258 AI-enabled medical devices authorized in 2025, contributing to more than 1,300 cumulative AI medical device authorizations.

Market Size and Forecast

-

Market Size 2026E: USD 862.71 billion

-

Market Size 2035: USD 1907.83 billion

-

CAGR (2026 - 2035): 9.22%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Medical Equipment Market - Request Free Sample Report

Medical Equipment Market Trends

-

Rising adoption of home healthcare services is increasing demand for portable medical equipment and remote patient monitoring devices globally.

-

Growth of wearable health technologies is enabling continuous patient tracking and improving chronic disease management across healthcare systems.

-

Expansion of telehealth platforms is driving real time diagnosis consultation and remote monitoring across developed and emerging economies.

-

Increasing aging population is boosting demand for long term care solutions and advanced medical diagnostic and monitoring equipment.

-

Rising chronic diseases such as diabetes cardiovascular and cancer is accelerating demand for advanced imaging and surgical devices.

-

Healthcare infrastructure expansion is improving hospital capacity increasing early diagnosis adoption and strengthening preventive screening programs worldwide.

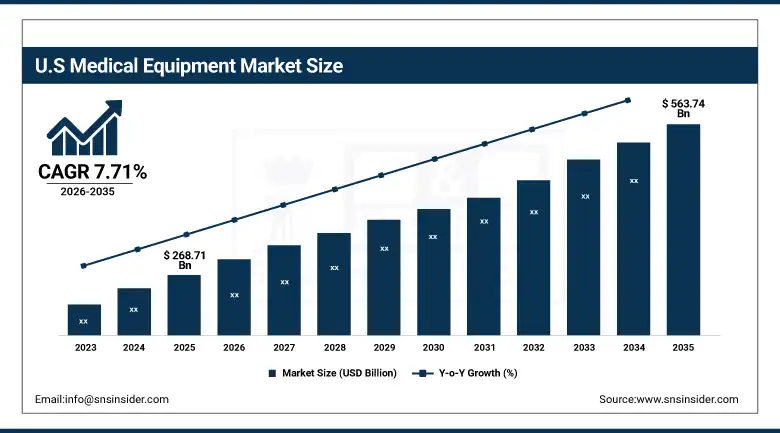

The U.S. Medical Equipment Market Size Outlook.

The U.S. Medical Equipment Market was valued at USD 268.71 billion in 2025 and is expected to reach around USD 563.74 billion by 2035, growing at a CAGR of 7.71% from 2026–2035.

The U.S. medical equipment market is growing consistently owing to increased demand for advanced healthcare infrastructure, diagnostic imaging systems, and surgical equipment. The usage of medical equipment in hospitals, clinics, and diagnostic centers has contributed to market growth in a consistent manner. Increased spending in healthcare modernization and digital health adoption has generated an increase in demand for high-precision medical devices. Development of AI-based diagnostics, minimally invasive surgeries, and wearable monitoring systems is further driving the demand for this product.

According to the U.S. FDA MDUFA performance dashboard and device authorization for Fiscal Year 2025, more than 1,200 medical devices using AI technology have been authorized for sale by the FDA, showing a rapid advancement of the use of digital technology in the medical equipment ecosystem.

According to the CDC, in the United States, there are in excess of 36 million inpatient surgical operations that take place each year, all of which require FDA-regulated medical devices.

Medical Equipment Market Segment Analysis

-

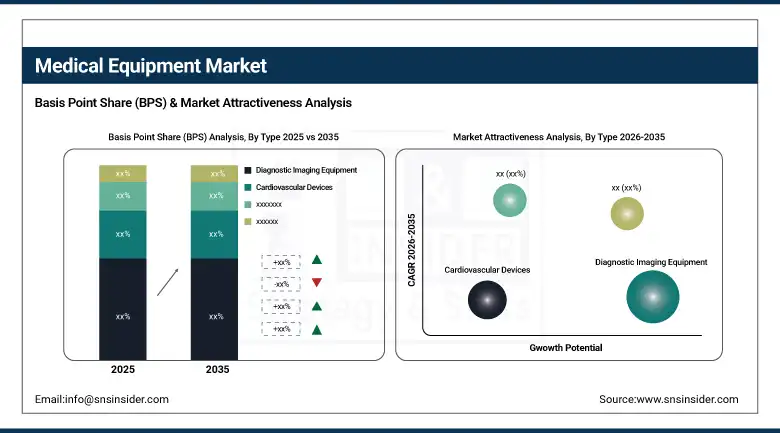

By Type, diagnostic imaging equipment dominated the market with 22.40% share in 2025; while patient monitoring devices are the fastest growing segment with CAGR of 14.67% during 2026 to 2035.

-

By Category, instruments and equipment dominated the market with 68.20% share in 2025; while disposables and consumables are the fastest growing segment with CAGR of 11.01% during 2026 to 2035.

- By Service Provider, multi-vendor OEMs dominated the market in 2025, while single-vendor OEMs are the fastest-growing segment during 2026–2035.

-

By End User, hospitals and clinics dominated the market with 61.40% share in 2025; while homecare and diagnostic centers are the fastest growing segment with CAGR of 12.04% during 2026 to 2035.

By Type, diagnostic imaging equipment dominated the medical equipment market, while patient monitoring devices are the fastest growing segment.

The diagnostic imaging equipment category emerged as a dominant segment in the market due to its largest revenue share in 2025. The growing requirement for the early diagnosis of any disease and clinical diagnosis is responsible for the dominance of this segment. The growing incidence of chronic conditions and cancer increases the usage of MRI, CT scans, and X-rays. The growing presence of hospital infrastructures along with ongoing improvements in imaging technology is fueling this trend.

The patient monitoring devices category is estimated to have the fastest CAGR in the coming years from 2026 to 2035. The growing need for remote patient monitoring and home healthcare applications has led to an increase in demand for patient monitoring devices. The growing cases of chronic conditions necessitate constant monitoring of health and data. The increasing use of wearable medical devices, telehealth services, and ICU monitoring devices is driving the adoption of this technology.

By Category, instruments and equipment dominated the medical equipment market, while disposables and consumables are the fastest growing segment.

The instruments and equipment sector was the market leader in the market by revenue share in 2025. This is attributed to the increased adoption of modern and advanced diagnostic equipment, surgical instruments, and imaging machines. The growing need for efficient diagnosis and treatment is fueling the purchase of medical equipment in large quantities. Continued innovations in technology along with the upgrade of equipment will keep driving the demand for it.

The disposables and consumables sector is estimated to exhibit the fastest CAGR during the forecast period, i.e., from 2026 to 2035. The major factors contributing to the rapid growth of this market include the increasing emphasis on controlling infections and ensuring hygiene in healthcare facilities. Moreover, the rising number of surgeries and diagnostics will keep the demand for medical devices in a steady trend.

By End User, hospitals and clinics dominated the medical equipment market, while homecare and diagnostic centers are the fastest growing segment.

The hospitals and clinics segment accounted for the dominated share of revenues in the market during the forecast period of 2025. This trend will continue due to the influx of patients and advanced healthcare setups. Hospitals and clinics carry out numerous operations, tests, and other procedures every day. The constant need for purchasing medical devices keeps the market demand high. The availability of trained personnel and reimbursement plans adds to the adoption.

The home care segment is poised to witness the fastest CAGR between 2026 and 2035. There is an increase in the adoption of remote patient monitoring solutions. The increasing cases of chronic ailments have led to the rise of homecare treatment approaches. The developments in diagnostic devices and other telemedicine techniques are accelerating the process of adoption.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025(%) |

|---|---|---|

|

North America |

United States |

88.20% |

|

Europe |

Germany |

26.80% |

|

Asia Pacific |

China |

41.50% |

|

Middle East & Africa |

UAE |

18.90% |

|

Latin America |

Brazil |

47.30% |

North America Medical Equipment Market Insights.

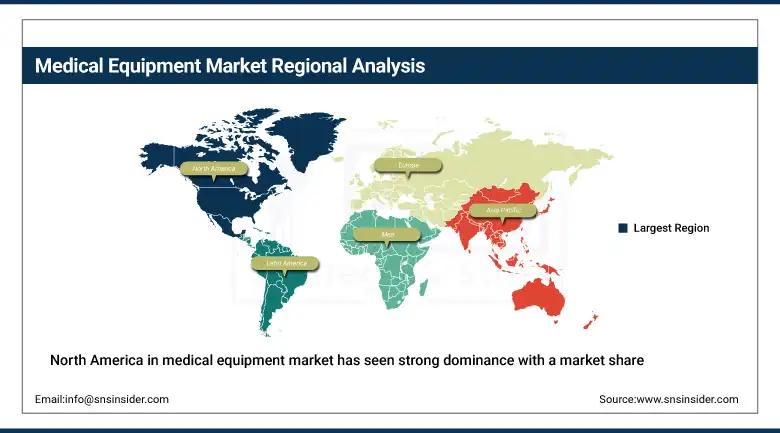

North America in medical equipment market has seen strong dominance with a market share of about 38.50% in 2025 due to advanced healthcare infrastructure and high medical technology adoption. The region benefits from strong demand in diagnostic imaging, surgical equipment, and patient monitoring systems. Increasing demand for early disease detection, chronic disease management, and advanced treatment solutions is driving market expansion across the United States and Canada. Rising adoption in digital health and homecare services is further supporting market leadership. Strong R&D investments are strengthening medical innovation capabilities.

According to the U.S. Food and Drug Administration 510(k) clearance and the U.S. Department of Commerce trade statistics found in regulatory, North America continues to be the leading continent producing medical devices globally, with the United States contributing about 85.5% of the region’s total production share in 2025. The FDA regulatory reports also show that over 6,200 medical devices have been cleared via the 510(k) and De Novo processes in the recent years.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Medical Equipment Market Insights.

The Europe medical equipment market shows strong presence in 2025 due to strict healthcare regulations and growing demand for advanced treatment solutions. Countries like Germany, France, United Kingdom, and Italy are key contributors to demand. High focus on aging population care, hospital modernization, and minimally invasive procedures is supporting steady market growth across the region. Increasing adoption in diagnostic imaging, orthopedic devices, and cardiovascular systems is further strengthening consumption. Expanding digital health frameworks are driving advanced medical equipment adoption.

According to MedTech Europe Facts & Figures 2025 and the European Commission Directorate-General for Health and Food Safety, Europe hosts over 2,000,000 medical technologies and more than 930,000 people employed in the medical technology sector in 2025. The European medical device market accounts for approximately 26.4% of the global market, making it the second-largest region after the United States

Asia Pacific Medical Equipment Market Insights.

Asia Pacific is positioned to register the fastest CAGR growth in the Medical equipment market during the forecast period with a market share of about 11.44% in 2025. Rapid healthcare infrastructure expansion and increasing medical device manufacturing are driving strong demand across China, Japan, India, South Korea, and Southeast Asia. Expanding hospital networks, rising patient population, and growing medical tourism are significantly boosting adoption. Rising demand for affordable and advanced healthcare solutions is further accelerating market growth across the region. Large scale healthcare investments support strong regional demand outlook.

According to the World Health Organization Global Health Observatory and national medical device registries, the Asia Pacific region shows wide variation in medical equipment density, including MRI availability ranging from over 50 units per million population in high-income economies to below 1 unit per million in several low-income countries as of 2025.

As stated by WHO health technology policy indicators, more than 2 million types of medical devices are globally classified, with Asia Pacific accounting for a rapidly increasing share of diagnostic imaging installations and hospital-based equipment deployment driven by rising noncommunicable disease burden and expanding healthcare infrastructure coverage across member states.

Middle East & Africa and Latin America Medical Equipment Market Insights.

The Middle East & Africa and Latin America region is witnessing steady growth due to rising healthcare infrastructure development and medical modernization. Countries like Brazil, Mexico, UAE, Saudi Arabia, and South Africa are emerging as key demand centers. Increasing investments in hospitals, diagnostic centers, and digital health systems are supporting market expansion. Growing need for efficient diagnostic and surgical equipment is further boosting product adoption. Rising healthcare access and government initiatives strengthen long term demand outlook across both regions.

As highlighted by WHO Global Health Observatory and OECD Health at a Glance 2025, Middle East and Latin America health care systems experience growing number of births taking place within institutions exceeding 90%, and growing use of diagnostic imaging equipment, which shows advancements in equipment availability towards universal health care coverage targets.

Market Dynamics

Growth Drivers: Rising prevalence of chronic diseases and aging population increasing continuous demand for advanced medical equipment globally

Increasing burden of cardiovascular diseases diabetes cancer and respiratory disorders is significantly boosting demand for diagnostic imaging surgical and monitoring equipment. Aging population across developed and emerging economies is increasing hospitalization rates and long-term care needs. Hospitals and diagnostic centers are expanding capacity to manage patient inflow. Continuous innovation in early diagnosis and treatment technologies is further supporting adoption. Growing healthcare awareness and preventive screening programs are strengthening overall market demand.

According to the World Health Organization, Global Health Estimates 2025 and UN DESA population ageing projections, the global population aged 60 years and above is projected to reach 1.4 billion by 2030, reflecting a major rise in age-related chronic disease burden. WHO reports that noncommunicable diseases account for over 74% of global deaths, with cardiovascular diseases alone contributing around 32% of total mortality. As per WHO, aging populations and multimorbidity significantly increase demand for diagnostic imaging, monitoring, and therapeutic medical equipment across healthcare systems worldwide.

Restraints: Strict regulatory approvals and complex compliance requirements delaying product launches and market expansion

Medical equipment manufacturers must comply with stringent regulatory frameworks and lengthy approval processes across different countries. Requirements for clinical trials safety validation and quality certifications increase development time and cost. Regulatory differences between regions create challenges for global market entry. Frequent updates in compliance standards demand continuous product modifications. Delays in approval impact innovation cycles and commercialization speed. Smaller companies face higher barriers due to limited regulatory expertise and resources for compliance management.

Opportunities: Expansion of home healthcare services and remote patient monitoring creating strong demand for portable medical equipment globally

Growing preference for home-based treatment and remote healthcare services is increasing demand for portable diagnostic and monitoring devices. Patients with chronic diseases are adopting wearable technologies for continuous health tracking. Healthcare systems are promoting decentralized care to reduce hospital burden. Advancements in telehealth platforms are enabling real time patient monitoring and consultation. Rising geriatric population is further supporting homecare adoption. This shift is creating significant growth opportunities for compact and user-friendly medical equipment.

As per OECD telemedicine survey indicators and WHO eHealth reports, over 58% of healthcare systems globally have implemented RPM components, while homecare-based monitoring represents 31–67% of digital health deployment share across regions in 2025. Additionally, adoption of wearable and portable medical devices exceeds 36% among adults in several high-income economies, reflecting strong expansion of home healthcare and portable diagnostics demand.

Recent Developments

-

2026: Boston Scientific announced acquisition of Penumbra, significantly expanding neurovascular and cardiovascular device portfolio and strengthening interventional treatment capabilities globally.

-

2025: Siemens Healthineers launched MAGNETOM Flow MRI platform, expanding AI-enabled imaging capabilities and improving diagnostic workflow efficiency across hospitals.

-

2025: GE HealthCare agreed acquisition of Intelerad Medical Systems, enhancing enterprise imaging workflow capabilities and strengthening radiology informatics ecosystem.

-

2024: Johnson & Johnson advanced Ottava surgical robotics program development focusing on minimally invasive surgery platforms and global clinical evaluation.

Medical Equipment Market Key Players are:

-

Johnson & Johnson

-

Medtronic

-

Siemens Healthineers

-

GE HealthCare

-

Koninklijke Philips N.V.

-

Abbott Laboratories

-

Boston Scientific Corporation

-

Stryker Corporation

-

Becton Dickinson and Company

-

Baxter International Inc.

-

Cardinal Health Inc.

-

Fresenius Medical Care AG & Co. KGaA

-

Terumo Corporation

-

Smith & Nephew plc

-

Zimmer Biomet Holdings Inc.

-

Intuitive Surgical Inc.

-

Edwards Lifesciences Corporation

-

Canon Medical Systems Corporation

-

Fujifilm Holdings Corporation

-

Olympus Corporation

Medical Equipment Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 791.33 Billion |

| Market Size by 2035 | USD 1907.83 Billion |

| CAGR | CAGR of 9.22% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Diagnostic Imaging Equipment, Cardiovascular Devices, Surgical Equipment, Patient Monitoring Devices, Others) • By Service Provider (Multi-vendor OEMs, Single-vendor OEMs, Others) • By Category (Instruments And Equipment, Disposables And Consumables) • By End User (Hospitals And Clinics, Homecare, Diagnostic Centers, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Johnson & Johnson, Medtronic, Siemens Healthineers, GE HealthCare, Koninklijke Philips N.V., Abbott Laboratories, Boston Scientific Corporation, Stryker Corporation, Becton Dickinson and Company, Baxter International Inc., Cardinal Health Inc., Fresenius Medical Care AG & Co. KGaA, Terumo Corporation, Smith & Nephew plc, Zimmer Biomet Holdings Inc., Intuitive Surgical Inc., Edwards Lifesciences Corporation, Canon Medical Systems Corporation, Fujifilm Holdings Corporation, Olympus Corporation |

Frequently Asked Questions

The medical equipment market is expected to grow at a CAGR of 9.22% from 2026 to 2035.

The medical equipment market was valued at USD 791.33 billion in 2025.

Rising chronic diseases, aging population, advanced healthcare infrastructure, early diagnosis, and minimally invasive treatments are driving global medical equipment demand.

: North America dominated the medical equipment market due to advanced healthcare infrastructure, strong R&D investment, and high technology adoption rates.

Get in Touch