Medical Plastics Market Report Scope & Overview:

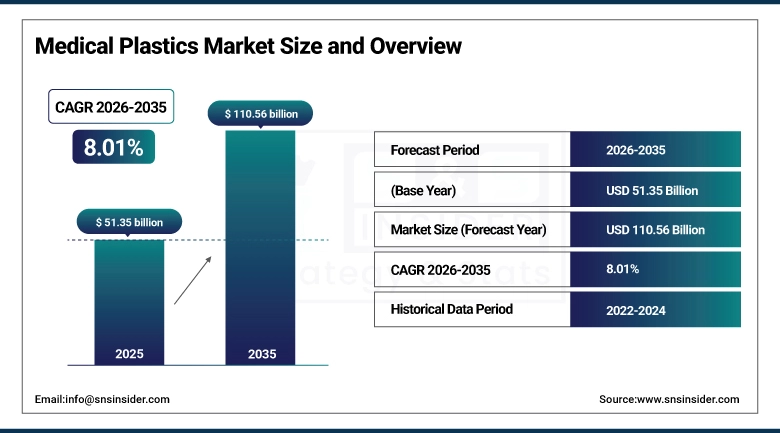

The Medical Plastics Market was valued at USD 51.35 billion in 2025 and is expected to reach USD 110.56 billion by 2035, growing at a CAGR of 8.01% from 2026-2035.

The medical device plastic market is anticipated to experience steady growth till 2035, backed by the rising demand for lightweight, durable, and economically priced plastic material that is easily sterilized. There is increasing demand for medical device plastics because they offer greater design freedom, enhanced chemical resistance, and suitability for large-scale production methods. The increasing use of minimally invasive procedures, single-use medical devices, and innovative diagnostic instruments is further driving market growth.

Rising awareness about the need for preventing infections, home healthcare devices, biopharmaceutical manufacturing equipment, and high-performing implantable devices has led companies to develop more innovative products using polymers such as polycarbonate, liquid crystal polymer, polyphenylsulfone, and polyethersulfone. Rising expenditure on healthcare services and advancements in technology in both developing and developed countries have also facilitated steady market growth.

Market Size and Forecast

-

Market Size in 2025: USD 51.35 Billion

-

Market Size by 2035: USD 110.56 Billion

-

CAGR: 8.01% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Medical Plastics Market - Request Free Sample Report

Medical Plastics Market Trends

-

Increased need for single-use and disposable medical devices is leading to the greater use of medical-grade plastic materials in healthcare institutions.

-

The usage of improved polymer materials that are resistant to heat and chemicals is on the rise within diagnostic instruments and surgical tools.

-

The manufacturing companies are making greater use of sustainable plastics materials in terms of recyclability and bio-sourced plastics.

-

The rise in minimally invasive procedures and wearable medical technology is driving the adoption of light-weighted plastics materials.

-

Furthermore, automation and precise molding technology is helping to make the manufacturing process efficient.

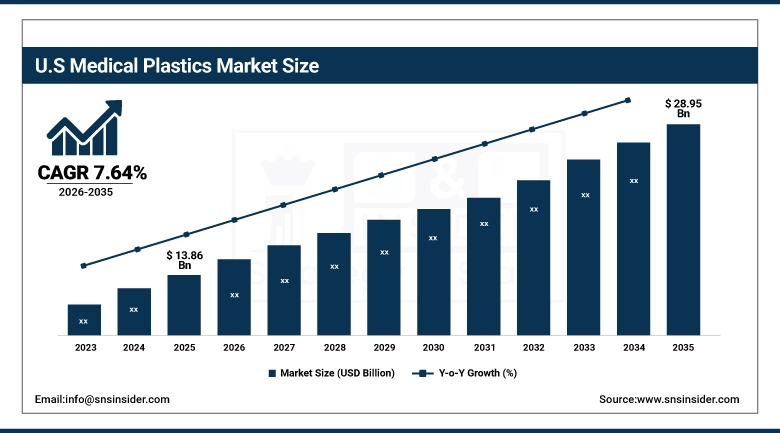

U.S. Medical Plastics Market valued at USD 13.86 billion in 2025 and will grow to reach USD 28.95 billion by 2035, registering a CAGR of 7.64% during 2026-2035.

In 2025, the United States will continue to be the dominant country in the North American medical plastics market, driven by the robust healthcare system in the country, its advanced medical devices manufacturing ecosystem, and high demand for single-use and minimally invasive medical products. Growing manufacture of diagnostic tools, surgical equipment, medicine delivery devices, IV equipment, catheters, and wearable devices will continue to fuel the rising consumption of high performance medical grade plastics such as polyethylene (PE), polypropylene (PP), polycarbonate (PC), and silicone-based materials.

The United States will benefit from the growing activities of major medical device producers and polymer companies focusing on innovative bio-compatible plastics, recyclable medical polymers, and light-weighted medical devices manufacturing techniques. Growing home care services, elderly population demographics, adoption of minimally invasive surgeries, and rising pharmaceutical packaging requirements will fuel the growth of the market over the forecast period. Regulatory focus on safety, traceability, and sustainable healthcare manufacturing practices will further fuel innovations in medical plastics applications in the United States healthcare sector.

Medical Plastics Market Segment Insights

-

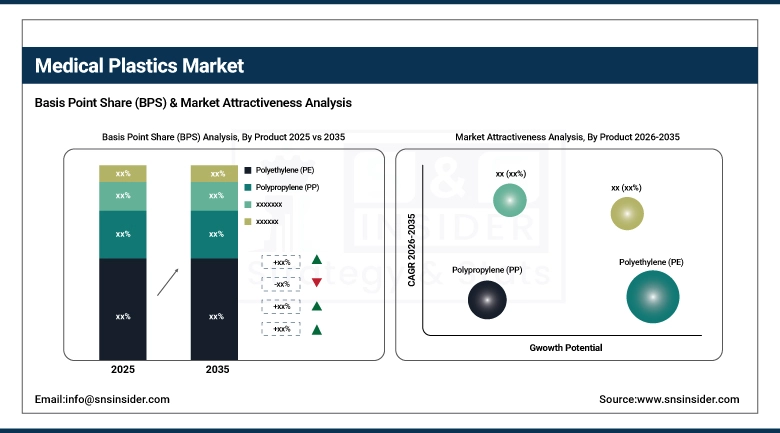

Based on Product, Polyethylene (PE) accounted for the largest market share (~24.5%) in 2025; Liquid Crystal Polymer (LCP) expected to be the fastest-growing segment (CAGR).

-

Based on Technology, Injection Molding accounted for the largest market share (~46.8%) in 2025; Injection Molding is also expected to be the fastest-growing segment (CAGR).

-

Based on Application, Medical Components accounted for the largest market share (~21.4%) in 2025; BioPharm Devices expected to be the fastest-growing segment (CAGR).

Medical Plastics Market Segment Analysis

By Product: Polyethylene (PE) dominates, Liquid Crystal Polymer (LCP) growing fastest

In 2025, Polyethylene (PE) represented the highest share in the Medical Device Plastics Market because of its wide application in disposable medical devices, tubes, packaging films, and fluid handling equipment. This material provides excellent flexibility, high chemical resistance, low-cost manufacturing process, and easy manufacturability that makes it perfect for high-demand healthcare applications. The increasing preference of hospitals and diagnostic centers for single-use devices and infection control devices is driving the usage of PE.

The Liquid Crystal Polymer (LCP) is projected to grow at the fastest pace in the forecast period. This type of material has high dimensional stability, superior heat-resistance properties, and superior electrical behavior. Increasing application of LCPs in miniaturized medical electronics, surgical instruments, and diagnostics equipment is driving the growth of this segment.

By Technology: Injection Molding dominates and records fastest growth

Injection molding emerged as the dominant technology segment for the period 2025 owing to its ability to manufacture complicated medical components with great accuracy and at low cost. It is currently employed for the fabrication of syringes, inhalers, parts of diagnostic devices, housing for implants, and surgical instruments. The adaptability of the process and applicability of the technology in large-scale production have played key roles in propelling its adoption by healthcare organizations.

The fastest-growing technology segment will also be seen in injection molding during the assessment period because healthcare providers are more focused on large-scale production, design flexibility, and automation. The increasing demand for customized medical devices, minimally invasive devices, and improved healthcare products is fostering the installation of advanced injection molding technology globally.

By Application: Medical Components dominate, BioPharm Devices growing fastest

Medical Components dominated the highest market share in 2025 because of growing production of diagnostic tools, surgical devices, catheters, connectors, and monitoring devices. The growing usage of lighter and sterilizable plastic materials in critical medical devices remains an important factor driving the growth of the segment. Moreover, the growing developments in healthcare infrastructure and patients' numbers have encouraged manufacturers to produce more medical components globally.

The fastest growth in BioPharm Devices is anticipated during the forecast period due to increasing biopharmaceutical production processes, the need for advanced drug delivery devices, and high adoption of disposable bioprocessing devices. Plastic materials remain highly sought after for biopharmaceutical products since they are resistant to contaminants and have sterilization properties.

Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

84% |

|

Europe |

Germany |

24% |

|

Asia Pacific |

China |

41% |

|

Middle East & Africa |

Saudi Arabia |

33% |

|

Latin America |

Brazil |

49% |

North America Medical Devices Market Insights

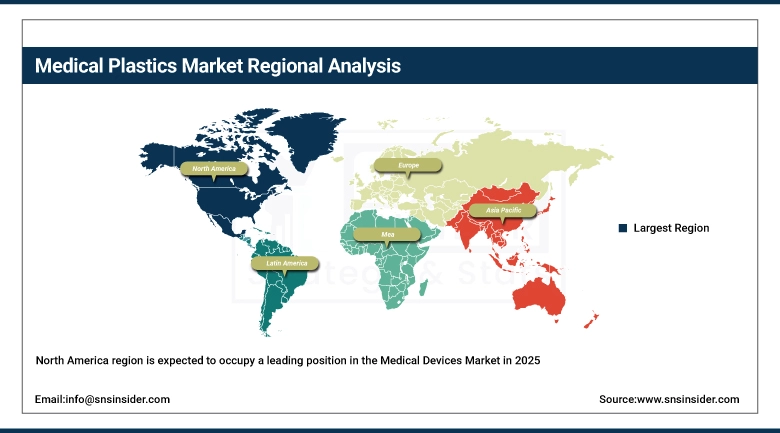

The North America region is expected to occupy a leading position in the Medical Devices Market in 2025 due to its advanced healthcare infrastructure, increased healthcare spending, and widespread adoption of technologically sophisticated medical equipment in the United States and Canada. The favorable market dynamics will be driven by the dominance of major medical device manufacturing companies, the growing need for minimally invasive surgeries, and accelerated adoption of artificial intelligence-based diagnostic tools and connected medical devices. Other factors contributing to the rapid growth of the medical devices industry in the region include rising incidence rates of chronic diseases, aging demographics, and growing home healthcare services.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Medical Devices Market Insights

The Asia-Pacific region is projected to be the highest-growing Medical Devices Market in 2025 because of the development of healthcare infrastructure, rising healthcare expenditure, and increased use of advanced diagnostics and treatments in China, India, Japan, and South Korea. China continues to dominate as the leading regional manufacturing base owing to its efficient manufacturing sector and the rising demand for cost-effective medical devices. The country of India is experiencing tremendous growth via the digitization of healthcare facilities, hospital construction, and increased medical tourism.

Europe Medical Devices Market Insights

Europe occupies a vital role in the world Medical Devices Market, with Germany, France, the UK, and Italy forming key regional markets. Europe enjoys superior healthcare systems, state-of-the-art hospitals, and the growing prevalence of precision medicine and minimally invasive surgeries. Germany stands out as the most prominent market in Europe owing to its established industry for medical equipment manufacture and robust research and development activities. The growth of geriatric populations, the escalating burden of chronic diseases, and the adoption of digital health solutions are propelling market growth. The regulatory focus on ensuring patient safety and quality products in accordance with EU Medical Device Regulation (MDR) standards is fostering innovation in the region.

Latin America Medical Devices Market Insights

There is consistent growth observed in the Medical Devices Market in Latin America, driven by developments in the country’s healthcare infrastructure, greater investments in healthcare from the private sector, and high demand for diagnostic and surgical devices in countries such as Brazil, Mexico, Argentina, and Colombia. Brazil is currently the biggest market in the region, owing to its growing number of hospitals and the adoption of cutting-edge medical technology. Factors such as higher healthcare awareness, increased medical tourism, and rising incidences of chronic diseases are expected to drive the demand for imaging, patient monitoring, and minimally invasive surgical devices.

Middle East & Africa Medical Devices Market Insights

Middle East and Africa regions have seen an increase in demand within the Medical Devices market, due to factors such as increased healthcare expenditure, hospital expansion plans, and the integration of innovative technology into healthcare practices in countries such as the United Arab Emirates, Saudi Arabia, and South Africa. These two nations have been at the forefront of market development, owing to their substantial spending on healthcare provision and technological advancements, as well as initiatives for medical tourism and digital health solutions. There is a greater incidence of chronic diseases, private sector growth within healthcare, and a growing need for advanced imaging and monitoring equipment within the region.

Market Growth Drivers: Rising demand for single-use medical devices and minimally invasive procedures

The rise in the use of disposable medical products in hospitals, diagnostic centers, and ambulatory care centers is a major factor behind the expansion of the Medical Plastics Market. Medical plastics are widely employed in syringes, catheters, IV sets, surgical instruments, diagnostic test strips, and drug delivery systems due to their lightweight nature, affordability, sterilization capabilities, and easy design. The rising number of minimally invasive procedures and preventive infections have increased the use of single-use plastic medical devices across the globe. As per WHO, health care associated infections continue to be an important issue in the world, which is why there is an emphasis on the use of disposable and resistant medical products. Aging populations, prevalence of chronic diseases, and the expansion of home care services are some other factors fueling growth in this market.

Market Restraints: Environmental concerns and stringent regulatory compliance requirements

One of the main limitations that exist within the Medical Plastics market is the rising environmental impact of plastic waste produced by disposable medical devices. Hospitals produce large amounts of single-use plastic waste, which includes packaging material, syringes, gloves, intravenous catheters, and other disposables, thereby increasing the demand for sustainable disposal solutions within the healthcare industry. Strict regulatory compliance concerning biocompatibility testing, sterilization validation, safety, and traceability for medical plastics is enforced by organizations such as the U.S. Food and Drug Administration (FDA) and the European regulatory agency. Adhering to these regulatory compliance requirements tends to increase production costs and product development time for medical plastics manufacturers. Moreover, the volatility in the prices of petrochemical feedstock and concerns surrounding the usage of non-recyclable plastic have become operational hurdles for medical plastics suppliers.

Market Opportunities: Growing adoption of bio-based polymers and advanced healthcare manufacturing technologies

Sustainability in the area of healthcare manufacturing and environmental medical materials is generating major growth opportunities in the Medical Plastics Market. Manufacturers are gradually investing in biodegradable and recyclable medical plastics as well as bio-based polymer manufacturing processes that will minimize the generation of plastic waste without compromising the efficiency and sterility of their products. Additionally, innovations in additive manufacturing techniques, precise molding, and high-end polymer design processes have made it possible for manufacturers to develop lightweight and high-performing medical devices tailored to individual patient needs. The quick adoption of advanced healthcare products including wearable health devices, remote patient monitoring devices, drug delivery systems, and minimally invasive surgery devices is widening the potential applications of advanced medical plastics. Furthermore, increased spending in healthcare infrastructure upgrade initiatives in emerging economies as well as increasing demand for home healthcare devices is driving market expansion opportunities for manufacturers.

Recent Developments:

-

2026: SABIC launched a new series of renewable medical-grade polymers for pharmaceutical packaging, drug delivery systems, and diagnostic uses, contributing to sustainable healthcare programs and lowering carbon footprints generated by traditional fossil-derived medical plastics.

-

2025: BASF increased its capacity to produce medical-grade polymers for high-end healthcare purposes such as minimally invasive surgical instruments, wearable medical equipment, and sterilizable diagnostic products due to growing worldwide demand for medical plastics.

Medical Plastics Market Key Players

-

BASF SE

-

Dow Inc.

-

DuPont

-

SABIC

-

Celanese Corporation

-

Eastman Chemical Company

-

Evonik Industries AG

-

Solvay S.A.

-

Tekni-Plex, Inc.

-

RAUMEDIC AG

-

Röchling Group

-

Saint-Gobain

-

Avient Corporation

-

Trelleborg Group

-

Freudenberg Medical

-

Viant

-

Spectrum Plastics Group

-

Orthoplastics

Medical Plastics Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 51.35 Billion |

| Market Size by 2035 | USD 110.56 Billion |

| CAGR | CAGR of 8.01% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Polyethylene (PE), Polypropylene (PP), Polycarbonate (PC), Liquid Crystal Polymer (LCP), Polyphenylsulfone (PPSU), Polyethersulfone (PES), Polyethylenimine (PEI), Polymethyl Methacrylate (PMMA), Others) • By Technology (Extrusion, Injection Molding, Blow Molding, Other) • By Application (Medical Device Packaging, Medical Components, Orthopedic Implant Packaging, Orthopedic Soft Goods, Wound Care, Cleanroom Supplies, BioPharm Devices, Mobility Aids, Sterilization and Infection Prevention, Tooth Implants, Denture Base Material, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | BASF SE, Dow Inc., DuPont, SABIC, Celanese Corporation, Covestro AG, Eastman Chemical Company, Evonik Industries AG, Solvay S.A., Tekni-Plex, Inc., RAUMEDIC AG, Röchling Group, Saint-Gobain, Avient Corporation, Trelleborg Group, Nolato AB, Freudenberg Medical, Viant, Spectrum Plastics Group, and Orthoplastics. |

Frequently Asked Questions

The Medical Plastics Market was valued at USD 51.35 billion in 2025.

The increasing demand for single-use and minimally invasive medical devices across global healthcare systems.

The Polyethylene (PE) segment dominated the Medical Plastics Market in 2025.

North America dominated the Medical Plastics Market in 2025.

The Medical Plastics Market is expected to grow at a CAGR of 8.01% from 2026 to 2035.

Get in Touch