Micro Inverter Market Report Scope & Overview:

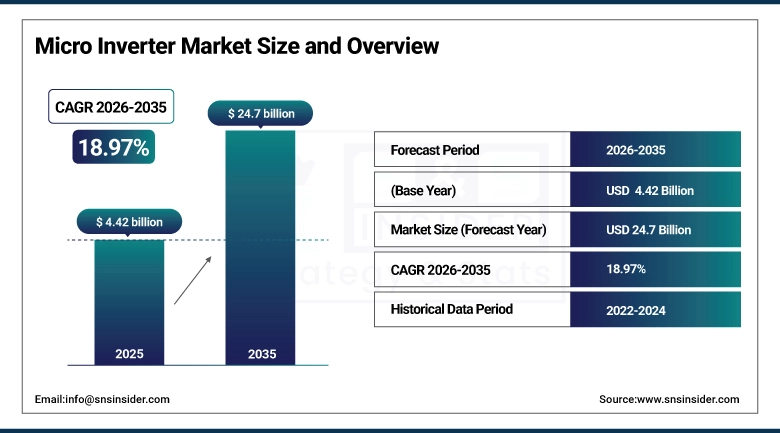

The Micro Inverter Market size was valued at USD 4.42 billion in 2025 and is expected to reach USD 24.7 billion by 2035, growing at a CAGR of 18.97% from 2026–2035.

The Micro Inverter Market is booming at an unprecedented rate and sustained growth this is because all over the world the trend of rooftop solar photovoltaic (PV) adoption has witnessed rapid acceleration in residential, commercial and industrial applications. Micro inverters, which operate at the module-level, are different to traditional string inverters that manage an entire solar array from a central unit and do not perform as efficiently due to system-wide losses caused by panel mismatch, shading and soiling. This has been translating into widespread adoption by homeowners and large commercial building owners seeking to maximize the energy yield of their solar installations. The value proposition of micro inverters moves beyond just DC to AC conversion with the integration of these devices with energy storage systems, smart home platforms and grid management technologies.

Data from the industry consistently shows that installed solar systems with micro inverters produce 5-25% more energy than similar string inverter systems when real world conditions cause partial shading or panel mismatch, delivering a quantifiable and compelling performance advantage for residential and commercial installations looking to optimize their solar ROI, enough to justify their incremental cost premium.

Growth in the number of electric vehicle charging points being deployed at residential properties is supporting rapidly growing demand for micro inverter-based solar-plus-storage systems, as homeowners consolidate their investment decisions around integrated energy management platforms that drive value by concurrently optimizing solar generation, battery storage and EV charging based on time-of-use electricity pricing and prevailing grid conditions.

Micro Inverter Market Size and Forecast

-

Market Size in 2025: USD 4.42 Billion

-

Market Size by 2035: USD 24.7 Billion

-

CAGR: 18.97% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Micro Inverter Market - Request Free Sample Report

Micro Inverter Market Trends

-

Growing adoption of grid-forming micro inverter technology enabling resilient solar operation during grid outages without requiring a separate battery system.

-

Increasing integration of micro inverters with home energy management systems enabling AI-optimized solar, storage, and load management.

-

Rising deployment of three-phase micro inverter systems in commercial solar installations addressing demand for scalable, modular rooftop solar solutions.

-

Expanding adoption in emerging solar markets as declining system costs make rooftop solar economically viable for a broader range of property types.

-

Growing demand for micro inverter systems with integrated rapid shutdown compliance for fire safety and first-responder protection.

-

Increasing use of wireless monitoring and remote diagnostics capabilities enabling proactive maintenance and performance optimization across solar portfolios.

-

Rising demand for micro inverter-battery storage integration enabling residential energy independence and backup power during grid outages.

U.S. Micro Inverter Market Size Outlook:

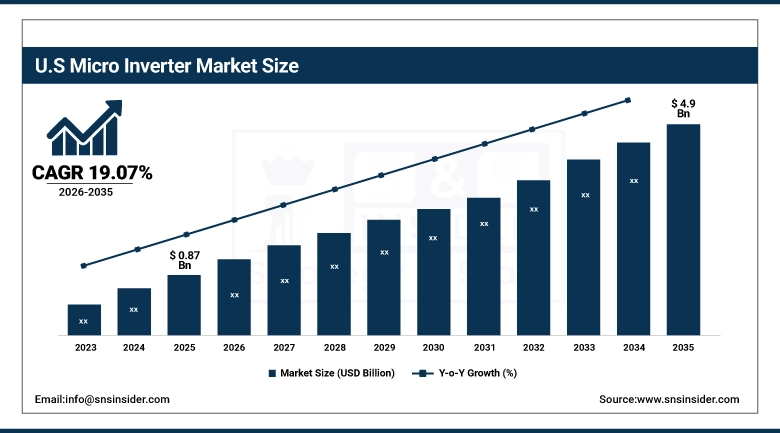

The U.S. Micro Inverter Market was valued at USD 0.87 billion in 2025 and is expected to reach USD 4.9 billion by 2035, registering a CAGR of 19.07% during 2026–2035. The market is the most mature in the world, driven by Enphase Energy's global technology leadership and supported at home by a large residential solar installation base with favorable federal Investment Tax Credit (ITC) terms; abundant net metering policies; and numerous strong state-level solar incentives. Conditional on data as far advanced as October of 2023, micro inverters are securing larger shares of the U.S. residential solar market amid wide-ranging shifts to clean energy tax credits (and attendant ill end up reflationary booms) detailed under the Inflation Reduction Act, and turning in pacing oriented final credit work therein.

Growing enthusiasm for community solar programs, new virtual power plant initiatives and services and utility-managed residential energy programs across U.S. states are now generating higher demand for micro inverter-based solar installations in which two-way communication capability with advanced monitoring will soon become a prerequisite for grid-interactive generation units as utilities increasingly embrace distributed solar generation asset classes as desirable grid resources requiring intelligent communications on an individual basis via a networked connectivity architecture.

Micro Inverter Market Segment Insights

-

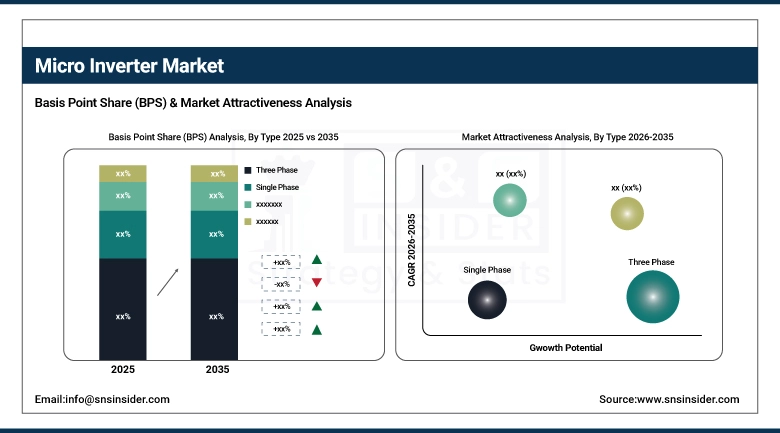

Based on Type, Three-Phase segment accounted for the largest market share in 2025; Single-Phase segment expected to be the fastest-growing segment (CAGR) driven by residential solar expansion.

-

Based on Power Rating, Above 500 W segment accounted for the largest market share (45%) in 2025; 250–500 W segment expected to be the fastest-growing segment (CAGR).

-

Based on End User, Residential segment accounted for the largest market share in 2025; Commercial segment expected to be the fastest-growing segment (CAGR).

By Type, Three-Phase dominates, Single-Phase expected to grow fastest

The Three-Phase segment represented more than 99% of market share in 2025. Due to their improved performance at imbalanced load conditions and better compatibility with the electrical systems of most commercial buildings, three-phase micro inverters have become the de-facto technology for larger scale solar installations due to their superior power balancing and higher efficiency.

Single-Phase is expected to witness the fastest CAGR from 2023 to 2035 as a result of rapid adoption of rooftop solar in residential. Single-phase micro inverters are the usual technology used for residential solar systems as they avoid increase installation costs while still being relatively cheaper for the average home with single phase electrical service. The continuing cost reduction of single-phase micro inverter systems and the expanding universe of residential solar incentive programs, coupled with increased homeowner awareness of solar economics, is encouraging solid volume growth in this segment.

By Power Rating, Above 500 W dominates, 250–500 W expected to grow fastest

The Above 500 W segment had the highest micro inverter market and held ~45% of this clients in 2025, as a result of their beneficial traits and advantages that emerge from included high-power apparatuses that are generally utilized for high-limit private, business and little mechanical sun oriented establishments. These micro inverters are higher powered and can therefore accommodate the growing high wattage solar panels, improve energy conversion efficiency to system output and mitigate the total units needed for each roof/ground mount installation which makes these devices highly compelling for larger rooftop and distributed solar projects. Increasing deployment of systems above 500 W across the globe was additionally supported by rising demand for more efficient generation of energy and growing commercial solar infrastructure.

The 250–500 W segment is expected to register the fastest CAGR through 2035, primarily owing to rapid installation of medium capacity solar photovoltaic modules at residential rooftop. This power range provides the best balance between affordability, efficiency and flexibility, perfect for small to medium home systems. This segment is expected to witness growth during the forecast period due to growing government incentives for residential solar deployment, advancement in compact inverter designs, and increasing consumer preference for modular solar solutions.

By End User, Residential leads, Commercial expected to grow fastest

The Residential Application segment commanded a major share of the application market due to consumers favoring micro inverters for home solar systems with module-level optimization, shade tolerance and integrated monitoring capabilities. On a global macro level, the massive adoption of residential solar, thanks to millions of new home installations completed annually in North America, Europe, Asia Pacific and emerging markets posturing to fuel sustained strong volume demand for residential micro inverter systems.

The Commercial segment is expected to witness the fastest growth (CAGR) in the past and future forecast years 2026-2035 as falling costs lead to accelerating adoption of rooftop solar power in commerce buildings striving for sustainable strategies and looking to offset utility costs. Businesses across the spectrum — from retail stores to warehouses, office buildings and manufacturing plants — are increasingly turning to rooftop solar as a means of cutting energy costs, achieving corporate sustainability goals and demonstrating environmental leadership. Micro inverter scalability, reliability and panel-level monitoring have a distinct advantage in commercial installations with complex roofs and partial shading.

Micro Inverter Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

76% |

|

Europe |

Germany |

28% |

|

Asia Pacific |

China |

48% |

|

Middle East & Africa |

UAE |

36% |

|

Latin America |

Brazil |

50% |

Asia Pacific Micro Inverter Market Insights

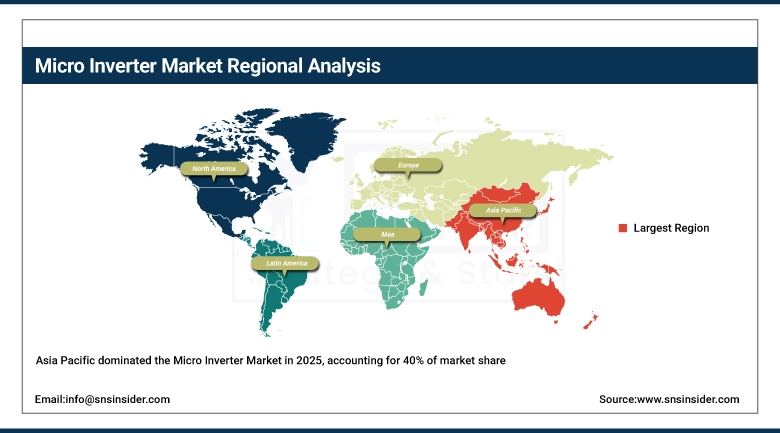

The Asia Pacific-region has generated the largest share in global micro inverter market of 40% with respect to revenue in 2025 on account of government support for deployment of residential solar in nations including China, Japan, Australia and South Korea; rapid urbanization opening doors for rooftop solar installations and presence of major micro inverter manufacturers. A large-scale solar manufacturing ecosystem in China underpins competitively-priced micro inverter production — while the world-leading per-capita residential solar take-up in Australia creates ongoing replacement and upgrade demand for superior micro inverter systems.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Micro Inverter Market Insights

North America is projected to grow at the highest rate over the forecast period, supported by accelerating adoption of U.S. residential solar under IRA incentives, Enphase Energy decisively leading U.S. tech and brand market share, & Canadian solar traction through recently renewed provincial incentive programs. Cumulative residential solar growth continues, driven by U.S. federal Investment Tax Credit at 30 percent, and strong state-level solar programs in California, New York, Texas and Florida that provide sustained multi-year residential solar installations which correspondingly drives demand for micro inverters directly.

Europe Micro Inverter Market Insights

Europe remained the second larger market for micro inverter in 2025, with Germany, Netherlands and France was major market of the country. The pace of rooftop solar deployment on the backs of national feed-in premium schemes and urgent energy independence imperatives, given Russian natural gas supply disruptions in Europe, is quickening in line with European Union set to aggressive 2030 600 GW PV targets under the REPowerEU initiative. The demand for sophisticated micro inverter platforms of solar-plus-storage systems with capability of grid resiliency is rising among several European homeowner.

Middle East & Africa and Latin America Micro Inverter Market Insights

The Micro Inverter Market in the Middle East & Africa and Latin America are high-growth segments supported by very good solar irradiance resources, fast-rising electricity costs motivating integration of solar energy systems and dynamic government programs for renewable energy. Residential and commercial solar installations are being made at increasing rates across Gulf nations as part of diversification measures, with Saudi Arabia and UAE governments also taking a lead in promoting rooftop solar. Rooftop solar growth in Latin America, spearheaded by Brazil, Chile and Mexico, is benefitting from favorable net metering policies and falling system costs..

Micro Inverter Market Growth Drivers: Accelerating global solar PV deployment and superior module-level energy optimization performance

The major growth driver for the Micro Inverterl Market is the increasing implementation of solar photovoltaic across residential and commercial applications worldwide, which is further coupled with rising individual & installer awareness regarding considerable performance benefits over traditional string inverter counterparts Its economic benefit, especially in practical environments with shading, soiling or variation in panel orientation – also called energy yield advantages of module-level optimization – appeals more and more to highlight a brilliant micro inverter adoption argument as electricity prices globally increase. Strong multi-year installation volumes that translate directly into demand for micro inverters are being supported by governmental renewable energy mandates, tax incentives, and net metering policies in the largest solar markets.

A new wave of next-gen “grid-forming” micro inverter technology from Enphase Energy and others is opening up entirely new value propositions for residential and commercial customers seeking energy resilience without batteries, especially in regions experiencing increasing grid reliability challenges stemming from extreme weather events and aging electrical infrastructure.

Micro Inverter Market Restraints: Higher per-watt cost compared to string inverters and dependence on third-party installation networks

Higher upfront cost per watt of installed capacity to string systems and power optimizer Systems can potentially inhibit Micro Inverter Market growth as price-sensitive installers and customers in cost-competitive solar markets may avoid micro inverter solutions. The total cost of ownership case for micro inverters is definitely a good one owing to energy yield gains, longer warranties and maintenance savings but no-one has to deploy the initial capital needed which still locks budget constrained residential customers as well some commercial buyers with shorter payback period appetites out.

Micro Inverter Market Opportunities: Solar-plus-storage integrated platforms and virtual power plant aggregation enabling new revenue streams

The micro inverter market is poised for transformational growth as this technology converges with residential battery storage, electric vehicle charging and smart home energy management platforms. Premium pricing un comes next-generation whole-home energy platforms that integrate intelligent management of solar generation, battery charging, EV charging, and grid interaction into distinctive value propositions well beyond the conversion of sunlight to electrical energy alone. At the same time, the advent of utility-sponsored virtual power plant programs that aggregate tens of thousands of individual residential solar-plus-storage systems into grid batteries commoditized as dispatchable grid resources that get paid for their grid services is creating enticing new financial incentives for homeowners to invest in next-gen micro inverter-based energy systems with advanced grid-interactive functionality.

Recent Developments:

-

2026: Enphase Energy expanded its IQ System Controller platform globally with enhanced grid-forming capabilities and vehicle-to-home (V2H) charging integration, enabling homeowners to use EV batteries as home backup power through the micro inverter system. Multiple new entrants launched competitive micro inverter platforms targeting commercial rooftop applications with improved three-phase power densities and wireless monitoring capabilities.

-

2025 (April): Enphase Energy launched the IQ System Controller in France and the Netherlands, offering homeowners grid-tariff resilience through integrated energy management combining microinverters, energy storage, and monitoring, providing dependable backup power during grid outages and enabling automated optimization of electricity consumption based on dynamic grid pricing.

-

2024 (June): Hoymiles introduced the MIT-5000-8T, a 5 kW microinverter for three-phase applications representing the manufacturer’s largest and most efficient unit. The system targets commercial rooftop installations requiring high power output per installation point, reducing balance-of-system costs and installation complexity for large commercial solar projects.

Micro Inverter Companies are:

-

Enphase Energy, Inc.

-

Hoymiles Power Electronics Inc.

-

APsystems

-

SMA Solar Technology AG

-

Chilicon Power LLC

-

ABB Ltd. (Fimer)

-

Darfon Electronics Corp

-

Altenergy Power System Inc. (APS)

-

Siemens Energy AG

-

Delta Electronics Inc.

-

GreenBrilliance USA

-

Yotta Energy

-

Birdview Solar

-

Tigo Energy Inc.

-

Northern Electric Power

-

AEconversion GmbH & Co. KG

-

Zhejiang Envertech Corp.

-

Sensata Technologies Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.42 Billion |

| Market Size by 2035 | USD 24.7 Billion |

| CAGR | CAGR of 18.97% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Single Phase, Three Phase) • By Power Rating (Below 250 W, Between 250 to 500 W, Above 500 W) • By End-User (Residential, Commercial, Industrial and Electric Utility) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Enphase Energy, Inc.; SolarEdge Technologies Inc.; Hoymiles Power Electronics Inc.; APsystems; SMA Solar Technology AG; Chilicon Power LLC; ABB Ltd. (Fimer); Darfon Electronics Corp.; Sparq Systems Inc.; Altenergy Power System Inc. (APS); Siemens Energy AG; Delta Electronics Inc.; GreenBrilliance USA; Yotta Energy; Birdview Solar; Tigo Energy Inc.; Northern Electric Power; AEconversion GmbH & Co. KG; Zhejiang Envertech Corp.; Sensata Technologies Inc. |

Frequently Asked Questions

North America is expected to register the fastest CAGR during the forecast period of 2026–2035, driven by accelerating U.S. residential solar adoption and Enphase Energy’s technology leadership.

The Three-Phase segment dominated the Micro Inverter Market in 2025, while the Single-Phase segment is expected to grow at the fastest CAGR driven by residential solar expansion.

Accelerating global solar PV adoption, superior module-level energy yield optimization compared to string inverter alternatives, and growing integration with energy storage and home energy management platforms.

The Micro Inverter Market was valued at USD 4.42 billion in 2025.

The Micro Inverter Market is expected to grow at a CAGR of 18.97% from 2026 to 2035.

Get in Touch