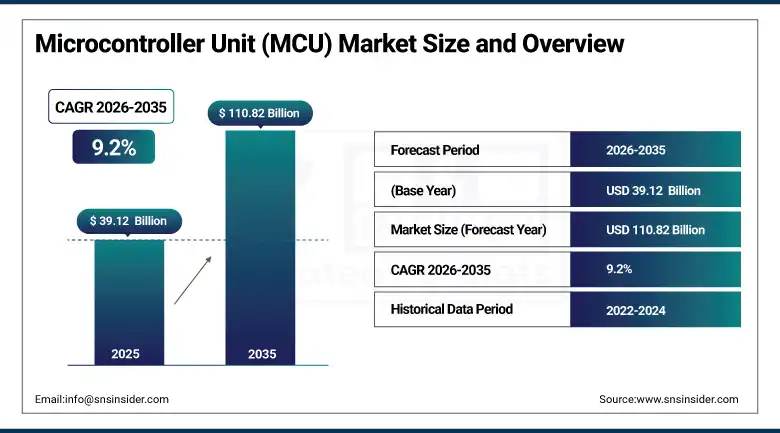

Microcontroller Unit (MCU) Market Report Scope & Overview:

The Microcontroller Unit (MCU) Market was valued at USD 39.12 Billion in 2025 and is expected to reach USD 110.82 Billion by 2035, growing at a CAGR of 9.2% from 2026–2035.

The global MCU market is growing at an exceptional pace. MCUs are compact integrated circuits combining a processor core, memory, and programmable input-output peripherals that provide processing power and control for embedded systems across automotive, consumer electronics, industrial automation, healthcare, and IoT applications. Rising adoption of automation and IoT technologies across industries is the primary growth driver. The market is experiencing rapid evolution as MCUs integrate wireless communication, security enclaves, and AI inference capability into increasingly power-efficient form factors.

STMicroelectronics launched the STM32U5 series of ARM-based MCUs designed for ultra-low-power applications in 2023, targeting IoT edge devices and wearables requiring extended battery life without compromising processing performance. The STM32U5 achieves 36 μA/MHz active current and 300 nA standby current through advanced power management architecture, demonstrating the commercial direction of MCU innovation toward energy efficiency optimisation whose performance improvement sustains adoption in battery-powered embedded applications across the rapidly expanding IoT device ecosystem.

Market Size and Forecast

-

Market Size in 2026E: USD 42.72 Billion

-

Market Size by 2035: USD 110.82 Billion

-

CAGR: 9.2% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get more information On Microcontroller Unit (MCU) Market - Request Free Sample Report

Microcontroller Unit (MCU) Market Trends

-

IoT device proliferation is driving MCU volume growth as each connected sensor, smart home device, and industrial IoT endpoint requires at least one MCU for local processing, peripheral control, and wireless connectivity management.

-

EV adoption is creating above-average automotive MCU demand as each battery electric vehicle requires 50-100 or more MCUs for battery management, and body electronics compared with 20-30 in conventional vehicles.

-

Edge AI integration in MCUs is enabling local machine learning inference for always-on voice recognition, anomaly detection, and predictive maintenance without cloud connectivity.

-

Wireless MCU development combining microcontroller cores with Bluetooth LE, Wi-Fi, Zigbee, or proprietary RF transceivers is enabling single-chip connected device design.

-

32-bit MCU adoption is progressively displacing 8-bit and 16-bit alternatives as processing complexity of IoT security and connectivity stack management exceeds 8-bit capability at competitive pricing.

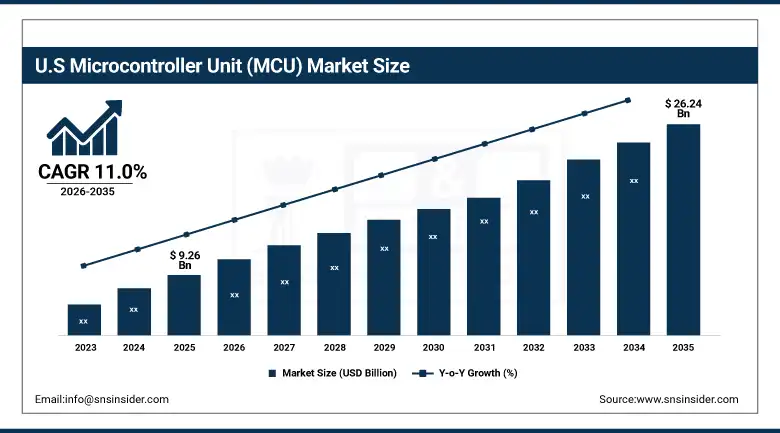

U.S. Microcontroller Unit (MCU) Market Outlook

The U.S. Microcontroller Unit (MCU) Market was valued at approximately USD 9.26 Billion in 2025 and is expected to reach approximately USD 26.24 Billion by 2035, growing at a CAGR of approximately 11.0%.

The U.S. is the world's most commercially sophisticated MCU market within the fastest-growing North American region. The automotive sector's ADAS and EV investment, the industrial automation market's programmable controller modernisation, and the IoT device development ecosystem centred in Silicon Valley collectively create above-average MCU demand per dollar of GDP. Texas Instruments, Microchip Technology, and NXP Semiconductors' U.S. operations define the commercial frontier of MCU product development whose innovation sustains competitive advantage in global OEM procurement.

NXP Semiconductors launched its S32K automotive MCU series in 2023, incorporating enhanced safety features and connectivity for automotive safety and electrification applications. The S32K3 family targets functional safety applications at ASIL-D level with integrated hardware security module and CAN-FD connectivity supporting next-generation vehicle architectures whose increasing electronic content per vehicle creates above-average MCU procurement growth independent of overall automotive production volume variation.

Microcontroller Unit (MCU) Market Segment Analysis

-

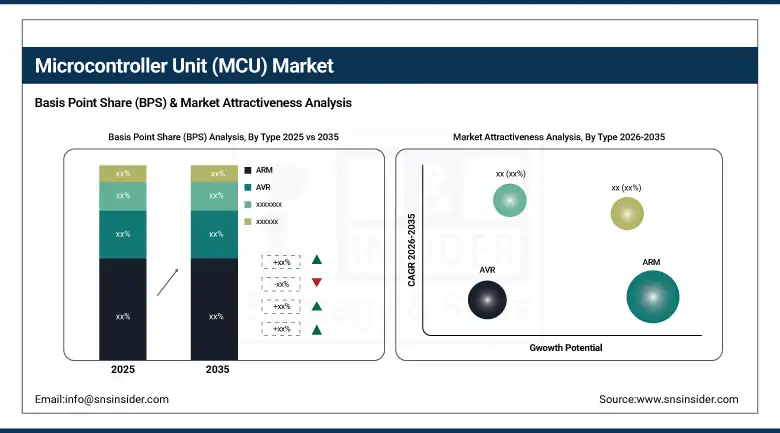

By Type, the ARM segment dominated the Microcontroller Unit (MCU) Market with 46.00% share in 2025, while the TriCore segment is the fastest growing with a CAGR of 11.56% during 2026–2035.

-

By Instruction Set, the RISC segment dominated the Microcontroller Unit (MCU) Market with approximately 70% share in 2025, while the CISC segment is the fastest growing with a CAGR of 10.03%.

-

By Application, the Consumer Electronics & Telecom segment dominated the Microcontroller Unit (MCU) Market with 24%, while the Automotive segment is the fastest growing with a CAGR of 12.73%.

-

By Bit Size, the 32-bit segment dominated the Microcontroller Unit (MCU) Market with approximately 46% share in 2025, while the 32-bit segment is also the fastest growing.

By Type, ARM dominates, TriCore grows fastest

ARM retained the dominant type position with 46.00% of the MCU market in 2025. ARM's commercial primacy reflects decades of ecosystem investment by MCU manufacturers whose ARM Cortex-M series architecture has become the de facto standard for embedded systems from simple 8-bit equivalent Cortex-M0 through high-performance Cortex-M7 and Cortex-M33 cores with TrustZone security. The ARM ecosystem's software compatibility across millions of libraries, RTOS implementations, and development tools reduces firmware development cost and time that creates structural preference in OEM procurement decisions.

TriCore is the fastest-growing MCU type at 11.56% CAGR because the automotive industry's transition toward electric vehicles and advanced driver assistance requires the performance, functional safety, and real-time determinism that Infineon's AURIX TriCore architecture provides at specifications that ARM Cortex-M cannot match in the most demanding automotive safety-critical applications. Each new ADAS domain controller, EV battery management system, and automotive power conversion unit that specifies AURIX creates MCU procurement whose per-unit value substantially exceeds consumer electronics or industrial MCU economics.

By Instruction Set, RISC dominates, CISC grows fastest

RISC retained the dominant instruction set position with approximately 70% of the MCU market in 2025. RISC architecture's commercial leadership reflects its fundamental advantage in the power-constrained embedded application contexts that define the majority of MCU use cases. RISC's fixed instruction width, load-store memory access model, and simplified decode pipeline create implementations whose silicon area efficiency and power consumption per instruction executed enable the combination of performance and battery life that IoT, wearable, and automotive MCU applications require. The RISC-V open instruction set architecture's commercial emergence as a royalty-free alternative to ARM is simultaneously creating new RISC MCU market participants whose competitive pricing sustains RISC's aggregate market share growth.

CISC is the fastest-growing instruction set at 10.03% CAGR because industrial automation, high-performance embedded computing, and applications requiring compatibility with complex instruction set software ecosystems are creating structured demand for CISC MCUs whose per-instruction capability reduces code density requirements and simplifies complex algorithm implementation. Microchip Technology's PIC32 and microchip's dsPIC families demonstrate the commercial viability of CISC-adjacent MCU architectures in industrial and motor control applications whose algorithm complexity favours CISC instruction density over RISC code volume.

By Application, consumer electronics dominates, automotive grows fastest

Consumer Electronics and Telecom retained the dominant application position with 24% of the MCU market in 2025. The extraordinary production scale of smartphones, tablets, smart home devices, wireless earbuds, wearables, and 5G infrastructure equipment creates aggregate MCU procurement whose unit volume substantially exceeds any other single application category. Each consumer electronics product generation that adds features including touch interfaces, wireless connectivity, biometric sensing, and voice control creates additional MCU procurement requirements whose commercial scale compounds with the global consumer electronics market's continuing volume expansion. 5G infrastructure deployment's radio unit and baseband processing requirements create institutional-scale MCU procurement that complements consumer device volume.

Automotive is the fastest-growing application at 12.73% CAGR because the convergence of vehicle electrification and autonomy is creating the most commercially transformative embedded electronics adoption wave in the automotive industry's history. Each EV requires battery management MCUs, powertrain control MCUs, thermal management MCUs, and charging system MCUs that collectively represent 2-4 times the MCU count of equivalent ICE vehicle powertrains. ADAS systems' camera, radar, and LiDAR processing, vehicle-to-everything communication, and over-the-air update management each add MCU requirements that create growing per-vehicle electronics content independent of overall production volume.

By Bit Size, 32-bit dominates and grows fastest

32-bit MCUs retained the dominant bit size position with approximately 46% of the MCU market in 2025, and are simultaneously the fastest-growing bit size category. Their dual leadership reflects the progressive displacement of 8-bit and 16-bit MCUs as the processing requirements of modern embedded applications including IoT security, RTOS execution, wireless protocol stack management, and sensor fusion exceed 8-bit capability at price points where 32-bit alternatives have become cost-competitive. ARM Cortex-M0 at commodity pricing has created a 32-bit MCU accessible at cost structures previously associated with 8-bit alternatives, accelerating the migration of 8-bit designed applications toward 32-bit replacements.

The 32-bit segment's fastest-growing status reflects the structural migration of the MCU market's installed base from legacy 8-bit and 16-bit architectures toward 32-bit replacements in each product generation refresh. IoT device connectivity requirements, automotive functional safety standards, and industrial automation real-time performance specifications each create design requirements that 8-bit MCUs cannot satisfy, creating systematic 32-bit adoption across successive product development cycles whose aggregate commercial impact is progressively concentrating MCU market revenue in the 32-bit category.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

54.6% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

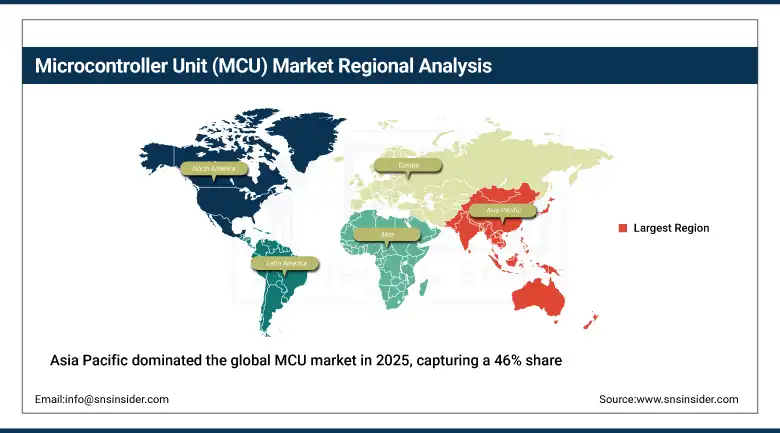

Asia Pacific Microcontroller Unit (MCU) Market Insights

Asia Pacific dominated the global MCU market in 2025, capturing a 46% share. The region's dominance reflects its status as the world's largest consumer electronics manufacturing hub, the most concentrated automotive electronics production base, and the home of major MCU manufacturers including Renesas Electronics, Toshiba, and Nuvoton Technology. China accounts for approximately 54.6% of Asia Pacific revenues through its extraordinary consumer electronics manufacturing scale, the government's semiconductor investment programme, and the rapidly growing EV industry's automotive MCU demand. Japan and South Korea's advanced semiconductor manufacturing and automotive electronics sectors represent significant secondary markets within Asia Pacific.

India and Southeast Asia are the most commercially dynamic emerging markets within Asia Pacific where the electronics manufacturing sector's expansion, the automotive industry's electrification investment, and the government's semiconductor self-sufficiency programmes are collectively creating above-average MCU demand growth whose commercial momentum attracts increasing international MCU manufacturer attention.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Microcontroller Unit (MCU) Market Insights

North America is the fastest-growing regional MCU market, driven by U.S. semiconductor investment under the CHIPS Act, the automotive industry's EV and ADAS investment, and the industrial automation sector's programmable controller modernisation. The United States accounts for approximately 87.4% of North American revenues through Texas Instruments, Microchip Technology, and NXP Semiconductors' product development and commercial operations whose combined portfolio breadth defines the global MCU market's technical frontier.

Canada contributes approximately 12.6% of North American revenues through its automotive electronics supply chain investment, the technology sector's IoT device development, and the industrial automation sector's MCU procurement whose combined demand creates consistent commercial engagement with leading MCU suppliers.

Europe Microcontroller Unit (MCU) Market Insights

Europe is a technically sophisticated MCU market where the automotive industry's EV transition, industrial automation's Industry 4.0 investment, and the medical device sector's regulated electronics procurement create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through Infineon Technologies' AURIX TriCore automotive MCU leadership, the automotive OEM sector's electronic content investment, and the industrial automation sector's Siemens and ABB programmable controller MCU procurement.

The United Kingdom, France, and Sweden are significant secondary European markets where the automotive supply chain, aerospace electronics, and medical device manufacturing create consistent MCU procurement. STMicroelectronics' European headquarters and Renesas's European automotive MCU operations sustain European market supply from established regional commercial presences.

MEA & Latin America Microcontroller Unit (MCU) Market Insights

The Middle East and Africa and Latin America are growing MCU markets where electronics manufacturing development, automotive sector electrification, and industrial automation investment are creating structured demand. UAE leads MEA revenues at approximately 38.4% through its electronics sector, smart city infrastructure investment, and the growing manufacturing sector whose automation investment creates MCU procurement demand.

Brazil leads Latin American revenues at approximately 44.2% through its large automotive manufacturing sector's increasing electronic content, the consumer electronics market's MCU procurement, and the industrial automation sector's growing investment in programmable control systems whose MCU-based architecture sustains consistent procurement.

Market Dynamics

Growth Drivers: IoT proliferation creating volume demand and EV adoption creating premium automotive MCU procurement

IoT device proliferation is the MCU market's most commercially certain volume growth driver. Each connected sensor, smart home device, industrial monitor, and wearable requires at least one MCU for local processing, peripheral control, and wireless connectivity management. The IoT device population is projected to surpass 29 billion by 2030, creating proportional MCU demand whose volume scale compounds with each percentage point increase in IoT device connectivity penetration across industrial, commercial, and consumer application domains. Each new IoT use case that achieves commercial scale creates a new MCU demand category whose aggregate impact on market volume substantially exceeds individual application category analysis suggests.

EV adoption creates a premium MCU demand category whose per-vehicle procurement value substantially exceeds conventional automotive or consumer electronics applications. The transition from ICE vehicles averaging 20-30 MCUs to BEVs requiring 50-100+ MCUs creates a structural demand increase that compounds with EV market share growth. Each percentage point increase in global EV market penetration creates proportional above-average automotive MCU demand whose commercial value per unit, reflecting automotive grade qualification, functional safety certification, and extended operational lifetime requirements, substantially exceeds commodity MCU pricing.

Restraints: Global semiconductor supply chain cyclicality and MCU design-in cycle complexity limiting rapid adoption

Semiconductor supply chain cyclicality creates procurement volatility whose impact on MCU market revenue growth is visible in the 2022-2023 inventory correction that followed the 2020-2021 shortage cycle. OEM customers who accumulated excess MCU inventory during the shortage period reduced procurement in subsequent quarters whose correction impact created temporary market revenue decline that obscured the underlying demand growth trend. Supply chain management complexity sustained by geopolitical semiconductor trade restrictions and geographic concentration of manufacturing capacity creates ongoing commercial risk for MCU market growth trajectory.

MCU design-in cycle complexity creates adoption lag that limits the pace at which new MCU generations penetrate the installed OEM design base. Embedded system product lifecycles of 5-10 years in industrial and automotive applications mean that MCU procurement for new designs represents a fraction of total OEM production volume in any given year, with legacy designs consuming established MCU part numbers whose replacement requires re-qualification investment that OEMs defer until necessary product transitions justify the engineering cost.

Opportunities: Edge AI MCU development and RISC-V open architecture creating new competitive MCU market entrants

Edge AI MCU development represents the most commercially premium near-term MCU innovation direction. MCUs integrating neural processing units for local machine learning inference without cloud connectivity create qualitatively new embedded system capabilities whose commercial differentiation sustains pricing premiums above commodity MCU alternatives. Always-on voice recognition, industrial anomaly detection, predictive maintenance sensor processing, and gesture control are each edge AI applications whose MCU intelligence requirements create new procurement categories in OEM embedded system designs.

RISC-V open instruction set architecture is creating new commercial MCU market entrants whose royalty-free architecture eliminates the ARM licensing cost that represents a meaningful input cost for high-volume MCU production. GigaDevice, WinChipHead, and multiple Chinese MCU manufacturers are commercialising RISC-V MCUs whose competitive pricing is creating market share opportunities in cost-sensitive consumer IoT and industrial applications where ARM alternatives previously held structural cost advantages.

Recent Developments:

-

2023: STMicroelectronics launched the STM32U5 series of ARM-based MCUs for ultra-low-power IoT applications in 2023, achieving 36 μA/MHz active current enabling extended battery life in wearables, industrial sensors, and smart home devices without compromising processing performance.

-

2023: NXP Semiconductors launched its S32K automotive MCU series in 2023 incorporating functional safety at ASIL-D level with integrated hardware security module and CAN-FD connectivity, targeting next-generation vehicle architectures whose increasing electrification and ADAS content creates above-average automotive MCU demand.

-

2024: Renesas Electronics released its RX72N MCU in 2024 offering 50% performance improvement over its predecessor for industrial automation applications, targeting the industrial control market's requirement for higher processing throughput as Industry 4.0 automation complexity increases MCU computational demand per controller.

Microcontroller Unit (MCU) Market Key Players

-

STMicroelectronics

-

NXP Semiconductors

-

Renesas Electronics

-

Microchip Technology

-

Infineon Technologies

-

Texas Instruments

-

Silicon Laboratories

-

Espressif Systems

-

Nordic Semiconductor

-

Nuvoton Technology

-

Holtek Semiconductor

-

Toshiba Corporation

-

Cypress Semiconductor (Infineon)

-

Samsung Electronics

-

Qualcomm

-

MediaTek

-

GigaDevice Semiconductor

-

WinChipHead (WCH)

-

RIOS Lab (SiFive)

-

Ambiq Micro

Microcontroller Unit (MCU) Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 39.12 Billion |

| Market Size by 2035 | USD 110.82 Billion |

| CAGR | CAGR of 9.2% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Type (ARM, AVR, PIC, TriCore, Others) • by Instruction Set (RISC, CISC) • by Application (Consumer Electronics & Telecom, Automotive, Industrial Automation, Healthcare, Others) • by Bit Size (8-bit, 16-bit, 32-bit) • by End User (Automotive OEMs, Consumer Electronics, Industrial, Healthcare, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | STMicroelectronics, NXP Semiconductors, Renesas Electronics, Microchip Technology, Infineon Technologies, Texas Instruments, Silicon Laboratories, Espressif Systems, Nordic Semiconductor, Nuvoton Technology, Holtek Semiconductor, Toshiba Corporation, Cypress Semiconductor (Infineon), Samsung Electronics, Qualcomm, MediaTek, GigaDevice Semiconductor, WinChipHead (WCH), RIOS Lab (SiFive), Ambiq Micro |

Frequently Asked Questions

The Microcontroller Unit (MCU) Market is expected to grow at a CAGR of 9.2% from 2026 to 2035.

The Microcontroller Unit (MCU) Market was valued at USD 39.12 Billion in 2025.

IoT device proliferation creating volume MCU demand across billions of connected endpoints, and EV adoption creating premium automotive MCU procurement as battery electric vehicles require 2-4 times the MCU count of conventional internal combustion engine vehicles.

Asia Pacific dominated the Microcontroller Unit (MCU) Market in 2025 with approximately 46% share, with China accounting for approximately 54.6% of Asia Pacific revenues.

Get in Touch