Microcontroller Socket Market Report Scope & Overview:

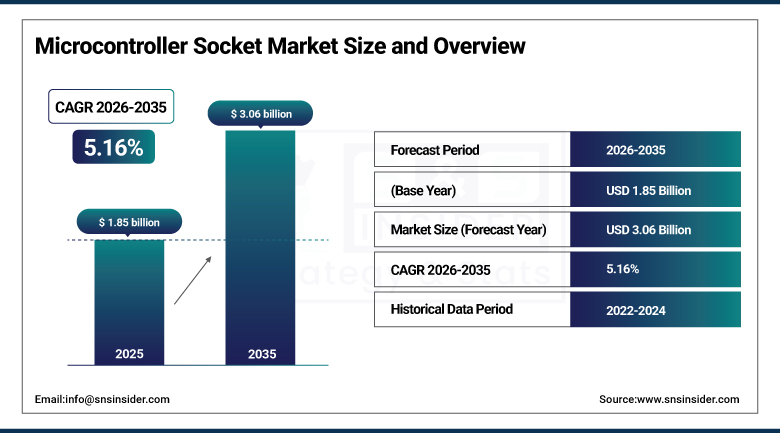

The Microcontroller Socket Market was valued at USD 1.85 Billion in 2025 and is expected to reach USD 3.06 Billion by 2035, growing at a CAGR of 5.16% from 2026 to 2035.

Microcontroller sockets are electromechanical interconnect components that provide a removable, socketed interface between a microcontroller unit and the printed circuit board into which it is installed, enabling the microcontroller to be inserted, removed, tested, reprogrammed, and replaced without soldering or de-soldering operations that would otherwise damage the board, the component, or both. The socket's defining commercial value proposition rests on three interconnected capabilities. First, it enables in-circuit programming and debugging during product development by allowing engineers to rapidly swap microcontroller variants, firmware versions, and test configurations without solder work whose time and labor cost would prohibit iterative development workflows at the pace modern embedded systems design requires.

Yamaichi Electronics, a leading Japanese precision socket manufacturer, launched its IC Test Socket series for advanced BGA microcontrollers in 2025 with enhanced kelvin contact structures enabling four-wire resistance measurement accuracy required for AEC-Q100 automotive qualification testing, zero-insertion-force mechanisms rated for 100,000 insertion cycles without contact resistance degradation, and temperature cycling capability across the minus 55 to plus 175 degree Celsius range demanded by automotive electronics reliability qualification programmes. The product's compliance with JEDEC and IPC socket standards and its compatibility with standard test handler interfaces made it the preferred socket solution for automotive microcontroller manufacturers expanding production capacity for electric vehicle control unit and battery management system applications across Asian and North American test operations.

Market Size and Forecast

-

Market Size in 2026E: USD 1.94 Billion

-

Market Size by 2035: USD 3.06 Billion

-

CAGR: 5.16% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Microcontroller Socket Market - Request Free Sample Report

Microcontroller Socket Market Trends

-

BGA socket adoption is increasing as advanced microcontrollers migrate to high-density packaging that requires superior thermal performance and signal integrity.

-

Zero insertion force (ZIF) and low insertion force (LIF) socket designs are gaining preference for reliable testing of high-pin-count and fine-pitch microcontroller packages.

-

High-temperature socket materials are witnessing greater adoption in automotive and aerospace applications requiring enhanced durability and reliability under extreme operating conditions.

-

Semiconductor manufacturing expansion and reshoring initiatives are driving demand for microcontroller test sockets across newly established fabrication and testing facilities.

-

IoT device miniaturization is fueling the development of ultra-compact socket solutions for fine-pitch QFN and WLCSP microcontroller packages.

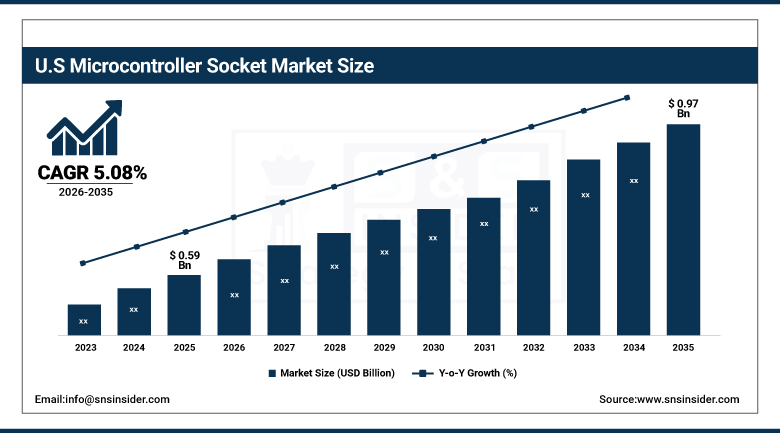

The U.S. Microcontroller Socket Market Outlook

The U.S. Microcontroller Socket Market was valued at approximately USD 0.59 Billion in 2025 and is expected to reach approximately USD 0.97 Billion by 2035, growing at a CAGR of approximately 5.08%.

The United States is the dominant national market within North America's leading regional position, driven by the concentration of major microcontroller manufacturers including Texas Instruments, Microchip Technology, and NXP Semiconductors whose domestic production and test operations sustain large-volume socket procurement demand, the presence of aerospace and defense electronics manufacturers whose high-reliability socket requirements command premium pricing, and the growing domestic semiconductor manufacturing capacity enabled by CHIPS Act investment that is creating new test socket demand at greenfield and expanding wafer fabrication and back-end testing facilities. The automotive electronics supply chain expanding in response to domestic EV production growth at Tesla, GM, Ford, and Stellantis facilities is creating growing demand for automotive-grade microcontroller test and burn-in sockets.

Enplas Corporation expanded its North American automotive test socket production capacity in 2025 in response to growing demand from automotive microcontroller manufacturers whose EV production programmes required AEC-Q100 qualified test sockets for battery management system and motor control microcontroller production testing at scale. The company's proprietary spring-loaded kelvin contact design enabled the four-wire low-resistance measurement accuracy required for automotive power management circuit qualification testing, while the socket housing's injection-moulded PEEK structure provided the thermal stability required for extended burn-in testing at temperatures above 125 degrees Celsius that automotive reliability standards mandate. The North American capacity expansion positioned Enplas to serve growing domestic automotive microcontroller test socket demand generated by CHIPS Act-stimulated semiconductor investment and the reshoring of EV electronics production.

Microcontroller Socket Market Segment Analysis

-

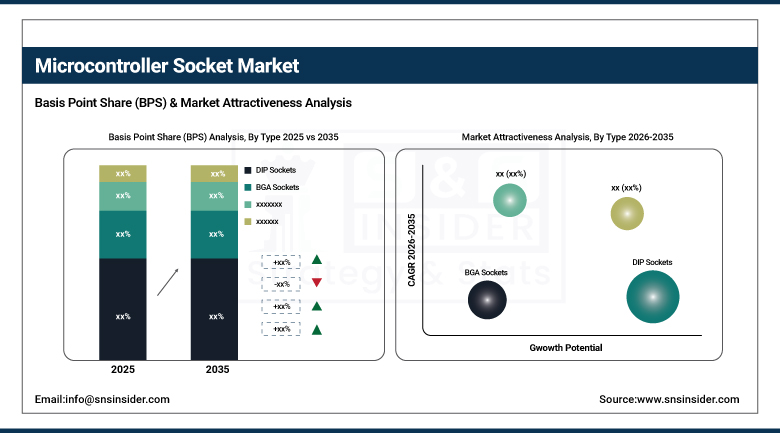

By Type, the DIP socket segment dominated the microcontroller socket market with 35.10% share in 2025, while the BGA socket segment is the fastest growing type during 2026 to 2035 at a CAGR of 6.95%.

-

By Mount Type, the surface mount segment dominated the microcontroller socket market in 2025, while the surface mount segment also represents the fastest growing mount type during 2026 to 2035.

-

By Application, the automotive segment dominated the microcontroller socket market in 2025, while the consumer electronics segment is the fastest growing application during 2026 to 2035.

-

By Contact Material, the gold-plated contact segment dominated the microcontroller socket market in 2025, while the palladium-plated segment is the fastest growing material during 2026 to 2035.

By Type, DIP dominates, BGA grows fastest

DIP sockets retained the dominant market position with 35.10% of revenue in 2025, reflecting the large installed base of 8-bit and 16-bit microcontroller applications across industrial control, consumer appliances, and legacy embedded systems where through-hole DIP package microcontrollers remain the most cost-effective and application-appropriate design choice. DIP socket robustness, low cost, ease of field replacement, and the enormous existing inventory of DIP-format microcontrollers in commercial production sustain the segment's market leadership even as newer microcontroller designs progressively adopt surface mount packages.

BGA sockets are growing fastest at a CAGR of 6.95% through 2035 as 32-bit microcontrollers with advanced peripherals, high memory, and high operating frequencies progressively adopt BGA packaging formats whose superior thermal management and signal integrity characteristics enable performance levels that leaded packages cannot achieve, creating corresponding demand for BGA-compatible socket designs capable of making reliable, low-resistance electrical contact with area array solder ball patterns at the precision tolerances that BGA package geometry requires.

By Application, automotive dominates, consumer electronics grows fastest

The automotive segment generated the largest share of microcontroller socket market revenue in 2025, driven by the growing volume and functional complexity of microcontrollers deployed in vehicle ECUs, battery management systems, ADAS sensors, and body control modules whose production testing, functional verification, and reliability qualification requirements create sustained demand for automotive-grade test sockets whose AEC-Q100 qualification status, extended temperature range performance, and high-cycle-count durability specifications command significant premiums over standard commercial socket alternatives.

Consumer electronics is growing fastest as the miniaturization and functional complexity growth of smart home devices, wearable electronics, wireless audio products, and portable consumer gadgets is driving adoption of increasingly sophisticated QFN and WLCSP microcontrollers whose development and production test requirements demand compatible precision socket solutions. The rapid development cycles of consumer electronics products, where time to market pressures require frequent firmware iterations and hardware revisions during development, create strong demand for development sockets that enable rapid microcontroller swapping without board rework.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.73% |

|

Europe |

Germany |

32.84% |

|

Asia Pacific |

China |

43.84% |

|

Middle East & Africa |

Israel |

22.84% |

|

Latin America |

Mexico |

38.47% |

North America Microcontroller Socket Market Insights

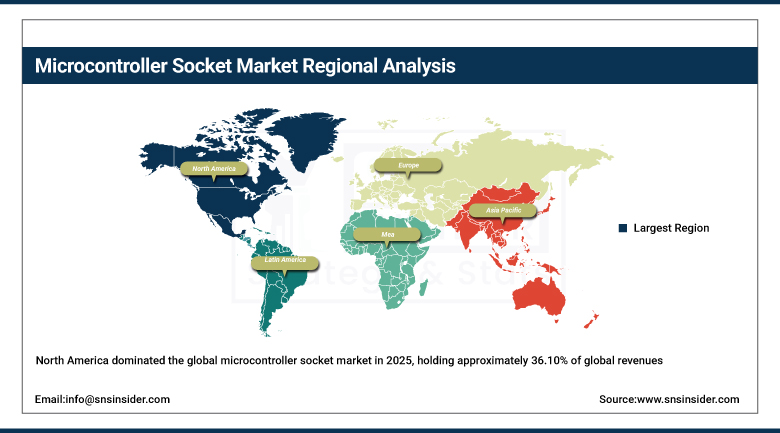

North America dominated the global microcontroller socket market in 2025, holding approximately 36.10% of global revenues. The United States accounts for approximately 84.73% of regional revenue through its combination of major microcontroller manufacturer domestic operations creating large-volume test socket procurement, aerospace and defense electronics manufacturers whose high-reliability socket requirements support premium pricing segments, and the growing domestic semiconductor capacity enabled by CHIPS Act investment creating new test socket demand. The CHIPS Act's USD 52 billion investment programme is stimulating both new wafer fabrication and back-end test infrastructure whose commissioning creates concentrated equipment and consumables procurement cycles including significant test socket volumes at each new facility.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Microcontroller Socket Market Insights

Europe is also a major region in global microcontroller socket revenues in 2025. Germany accounts for approximately 32.84% of European revenues through its automotive electronics manufacturing ecosystem whose Bosch, Continental, Infineon, and STMicroelectronics operations create substantial microcontroller test socket demand both for automotive-grade component qualification testing and for production programming socket applications at automotive ECU assembly facilities. The EU Chips Act's EUR 43 billion investment programme for European semiconductor manufacturing capacity is creating new test infrastructure investment across the continent that will incrementally expand European socket procurement volumes. The United Kingdom, France, and the Netherlands contribute secondary European demand through their industrial electronics, semiconductor research, and telecommunications equipment manufacturing activities.

Asia Pacific Microcontroller Socket Market Insights

Asia Pacific is the fastest-growing regional microcontroller socket market, projected to expand at a CAGR of approximately 5.80% through 2035. China accounts for approximately 43.84% of Asia Pacific revenues through its dominant position in consumer electronics contract manufacturing, its growing domestic microcontroller and semiconductor industry, and the large-scale back-end semiconductor test operations serving global fabless MCU companies at OSAT facilities in Shanghai, Shenzhen, and Chengdu. Japan contributes precision test socket manufacturing capability through companies including Yamaichi Electronics, Enplas, and Sensata whose high-precision socket designs for automotive and industrial applications are globally distributed. South Korea, Taiwan, and India each contribute growing regional demand through their semiconductor manufacturing and electronics assembly industries.

MEA & Latin America Microcontroller Socket Market Insights

Middle East and Latin America represent smaller but developing Microcontroller Socket markets where electronics manufacturing investment and domestic industrial and automotive production growth are creating incremental demand. Israel leads MEA revenues at approximately 22.84% of the regional total through its semiconductor design and test industry, military electronics manufacturing, and the presence of chip development centres for global technology companies whose design activity requires development socket procurement. Mexico leads Latin American revenues at approximately 38.47% of the regional total through its automotive electronics manufacturing ecosystem serving U.S. OEMs, where growing electronics content per vehicle and expanding EV platform assembly at Mexican facilities is creating incremental demand for automotive-grade microcontroller sockets in both production and service applications.

Market Dynamics

Growth Drivers: Microcontroller market expansion driven by IoT, automotive electrification, and industrial automation and increasing BGA package adoption creating premium socket demand

The global microcontroller market sustained growth, driven by the explosion of IoT device production, the electrification of automotive vehicle architectures that is multiplying per-vehicle MCU content, and the progressive automation of industrial manufacturing operations that requires embedded control intelligence at every machine and process node, creates a proportional expansion in the addressable market for microcontroller sockets at development, production test, and service application stages. The progressive transition of high-performance microcontroller designs to BGA and advanced surface mount package formats whose precision contact requirements and higher per-socket complexity create premium pricing opportunities for specialized socket manufacturers is shifting market revenue mix toward higher average selling price products that sustain revenue growth rates above the underlying microcontroller unit volume growth rate.

Restraints: Soldering technology improvements that reduce the need for socketed microcontroller installations in production applications and the price sensitivity of socket procurement decisions in cost-competitive consumer electronics manufacturing

Advances in automated soldering technology, reflow process control, and selective soldering accuracy have progressively reduced the error rates and rework costs associated with directly soldering surface mount microcontrollers in production assembly, reducing the economic justification for socket-based installation in applications where the ability to remove and replace the microcontroller was the primary reason for socket adoption. This trend is particularly evident in high-volume consumer electronics assembly where the combination of lean manufacturing philosophy, increasingly reliable soldering processes, and the dominant motivation to minimize BOM cost pushes manufacturers toward direct solder mounting of MCUs whose replacement economics are addressed through whole-board replacement rather than component-level field service.

Opportunities: CHIPS Act and EU Chips Act investment creating new domestic semiconductor test infrastructure and automotive EV platform microcontroller qualification requirements represent high-value near-term demand

The CHIPS Act's USD 52 billion U.S. investment programme and the EU Chips Act's EUR 43 billion European investment are collectively creating the largest single expansion of domestic semiconductor manufacturing and test capacity in both regions since the 1990s. Each new fab commissioning event requires procurement of test socket inventories for the specific microcontroller packages produced at that facility, creating concentrated demand events whose timing is predictable from public facility commissioning announcements and whose geographic concentration in the United States and Europe provides socket manufacturers with focused sales channel opportunities. The automotive EV transition's requirement for AEC-Q100 qualified sockets for high-reliability battery management, power conversion, and motor control microcontrollers creates a premium market segment whose growth trajectory is aligned with global EV production volume expansion forecasts.

Recent Developments:

-

2025: Yamaichi Electronics launched its IC Test Socket series for advanced BGA microcontrollers with enhanced kelvin contact structures, zero-insertion-force mechanisms rated for 100,000 insertion cycles, and temperature cycling capability across minus 55 to plus 175 degrees Celsius, meeting AEC-Q100 automotive qualification testing requirements at automotive microcontroller manufacturers expanding EV control unit production capacity.

-

2025: Enplas Corporation expanded its North American automotive test socket production capacity to serve growing EV programme microcontroller testing demand, with its proprietary spring-loaded kelvin contact design enabling four-wire low-resistance measurement required for automotive power management circuit qualification and PEEK housing structure providing extended burn-in thermal stability.

-

2024: Samtec Inc. released its DMM series high-density surface mount microcontroller development sockets with 0.5 millimetre pitch contact capability targeting QFN and WLCSP package formats used in IoT, wearable, and portable consumer electronics microcontroller applications, enabling reliable contact engagement at package pitches that previous-generation development socket designs could not accommodate without contact or package damage risk.

Microcontroller Socket Market Key Players are:

-

Texas Instruments Incorporated

-

Microchip Technology Inc.

-

NXP Semiconductors NV

-

STMicroelectronics NV

-

Renesas Electronics Corporation

-

Infineon Technologies AG

-

Yamaichi Electronics Co. Ltd.

-

Enplas Corporation

-

Mill-Max Manufacturing Corporation

-

Aries Electronics Inc.

-

Sensata Technologies Inc.

-

Samtec Inc.

-

Amphenol Corporation

-

Molex LLC

-

TE Connectivity Ltd.

-

3M Company

-

Plastronics Socket Company

-

Johnstech International Corporation

-

Advanced Interconnections Corporation

-

Ironwood Electronics Inc.

Microcontroller Socket Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.85 Billion |

| Market Size by 2035 | USD 3.06 Billion |

| CAGR | CAGR of 5.16% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (DIP Sockets, BGA Sockets, QFP Sockets, SOP Sockets, SOIC Sockets, QFN Sockets) • By Contact Material (Tin-Plated, Gold-Plated, Palladium-Plated) • By Mount Type (Through-Hole, Surface Mount) • By Application (Automotive, Industrial Automation, Consumer Electronics, Medical Devices, Aerospace & Defense, Telecommunications, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Texas Instruments Incorporated, Microchip Technology Inc., NXP Semiconductors NV, STMicroelectronics NV, Renesas Electronics Corporation, Infineon Technologies AG, Yamaichi Electronics Co. Ltd., Enplas Corporation, Mill-Max Manufacturing Corporation, Aries Electronics Inc., Sensata Technologies Inc., Samtec Inc., Amphenol Corporation, Molex LLC, TE Connectivity Ltd., 3M Company, Plastronics Socket Company, Johnstech International Corporation, Advanced Interconnections Corporation, and Ironwood Electronics Inc. |

Frequently Asked Questions

The primary growth factors are the expanding global microcontroller market driven by IoT device proliferation, automotive electrification increasing per-vehicle MCU content, industrial automation investment.

The DIP socket segment dominated the Microcontroller Socket Market with 35.10% share in 2025.

North America dominated the Microcontroller Socket Market in 2025, holding approximately 36.10% of global revenues.

The Microcontroller Socket Market was valued at USD 1.85 Billion in 2025.

Get in Touch