Off-Highway Brake Oil Aftermarket Market Report Scope & Overview:

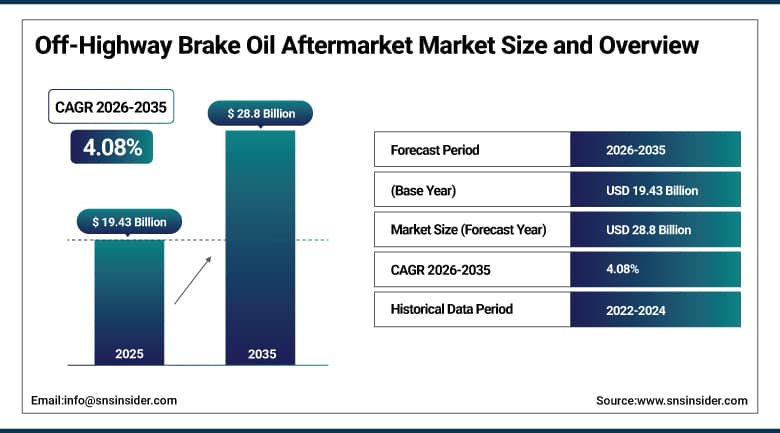

The Off-Highway Brake Oil Aftermarket Market was valued at USD 19.43 Billion in 2025 and is expected to reach USD 28.8 Billion by 2035, growing at a CAGR of 4.08% from 2026–2035.

Off-highway vehicles including construction equipment, agricultural machinery, and mining vehicles operate under conditions that place extraordinary demands on braking systems. The hydraulic brake systems that control these machines depend on brake fluid, referred to commercially as brake oil in this segment, to transmit the force from operator control inputs through hydraulic circuits to the mechanical braking elements at each axle. The aftermarket provides replacement brake oil and maintenance services to the large installed global fleet of off-highway vehicles once they leave original equipment manufacturer warranty periods. Given that off-highway vehicles total close to 5 million in sales around the world just in 2023, this provides a structurally significant aftermarket customer base for all of the off-highway segments combined. As opposed to passenger cars' braking fluid, whose replacement is scheduled less frequently under controlled circumstances, the maintenance of off-highway braking fluid takes place more often since the working environment is more severe, leading to increased contamination levels and hydraulic pressure on the equipment. When compared to passenger car brake fluids, this means that there is higher earnings potential than average when it comes to sales of the off-highway brake oil aftermarket per unit.

Over 5 million units of off-highway vehicles have been sold across the world during 2023, which contributes to a total installed fleet in construction, agricultural, and mining industries that constitutes demand for off-highway brake oil aftermarket products. The higher number of hours and harsher conditions than the on-road vehicles result in high brake oil consumption per vehicle.

Market Size and Forecast

-

Market Size in 2026E: USD 20.23 Billion

-

Market Size by 2035: USD 28.8 Billion

-

CAGR: 4.08% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get More Information On Off-Highway Brake Oil Aftermarket Market - Request Free Sample Report

Off-Highway Brake Oil Aftermarket Trends

-

Environmentally safer synthetic brake fluid formulations are gaining adoption due to stricter occupational safety and environmental regulations globally.

-

Products designed for long-lasting brake oil application are minimizing maintenance intervals and downtime in massive construction/mining machinery.

-

Development of infrastructure in developing countries is leading to an increased use of off-highway vehicles, including aftermarket brake oils.

-

Fleet management software is enabling condition-based brake fluid replacement with help of modern brake system health monitoring solutions.

-

Hybrid and electric off-highway vehicles are creating demand for brake fluid used in regenerative braking systems.

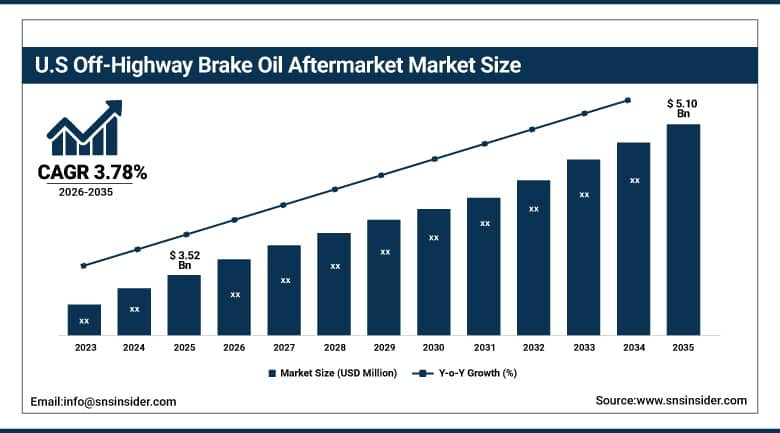

The U.S. Off-Highway Brake Oil Aftermarket Market Outlook

The U.S. Off-Highway Brake Oil Aftermarket Market was valued at approximately USD 3.52 Billion in 2025 and is expected to reach approximately USD 5.10 Billion by 2035, growing at a CAGR of 3.78%.

The United States maintains a large and well-established off-highway brake oil aftermarket through its extensive fleets of agricultural, construction, and mining equipment operating across the country's major production regions. American agricultural equipment fleets operated by Deere, CNH Industrial, and AGCO dealers cover millions of acres of crop production requiring extensive maintenance support including brake fluid replacement across seasonal maintenance cycles. The U.S. Occupational Safety and Health Administration regulations governing safe brake system operation on construction and mining equipment create regulatory-backed demand for regular brake fluid inspection and replacement. OSHA standards mandate that equipment operators maintain braking systems in safe working condition, providing compliance-driven motivation for brake oil replacement that does not depend solely on equipment operator cost-benefit analysis. The U.S. mining sector operating in Nevada, Wyoming, Montana, and Western states uses large fleets of haul trucks, excavators, and processing equipment whose heavy-duty braking demands require the most robust brake fluid specifications available commercially.

OSHA standards for construction and mining equipment require documented brake system maintenance as part of mandatory pre-operation inspection procedures. These regulatory requirements create compliance-driven brake oil aftermarket demand that is relatively insensitive to economic cycle fluctuations as equipment operators cannot legally defer brake system maintenance below the safety standards that federal and state occupational safety regulations mandate.

Off-Highway Brake Oil Aftermarket Segment Analysis

-

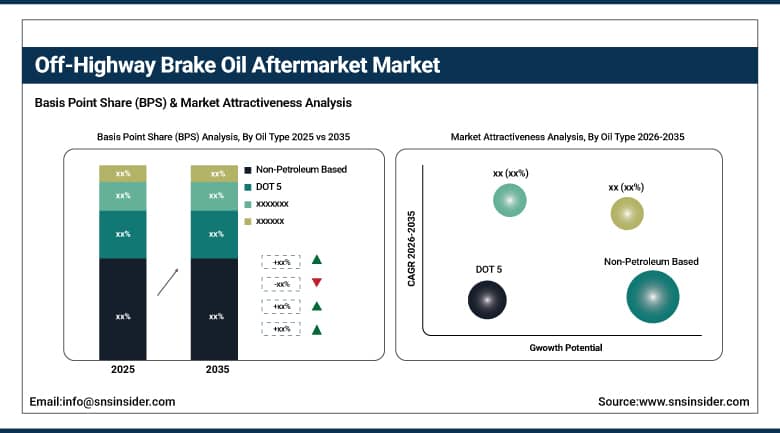

By Oil Type, non-petroleum and DOT 5 formulations dominated the market with the largest combined share in 2025; DOT 4 is growing.

-

By Application, construction held the largest share of approximately 38% in 2025; mining is growing through the extraordinary brake demands of large haul truck operations.

-

By Vehicle Type, construction equipment held the largest share in 2025; agricultural equipment is a significant and stable volume segment.

-

By Distribution Channel, independent aftermarket distributors held the largest share in 2025; online is the fastest-growing channel.

By Oil Type, non-petroleum and DOT 5 dominate, DOT 4 grow fastest

The formulations of brake oil, which do not contain petroleum or have been formulated using silicone DOT 5 type, accounted for the lion's share of the off-highway brake oil aftermarket in 2025. DOT 5 silicone-type brake fluid boasts of a dry boiling point of 260 degrees Celsius against 230 degrees Celsius that DOT 4 can offer. The extra thermal safety cushion provided by DOT 5 makes it a better choice for severe brake heat-generating environments, which occur in the mining and heavy construction sectors. The other unique characteristic of silicone DOT 5 is that it does not absorb any water vapor. This means that even after long periods of use, the fluid maintains its boiling point, unlike glycol types, whose boiling point falls due to moisture absorption.

DOT 4 brake oil has shown immense growth in the off-highway brake oil aftermarket owing to its efficiency, versatility, and excellent boiling point characteristics in comparison to regular DOT 3 oils. The use of DOT 4 oils has increased amongst fleets owing to the high temperatures involved while performing braking functions in newer agricultural and construction equipment. With new projects being undertaken along with the use of off-highway vehicles in various emerging markets, the demand is likely to continue growing while new DOT 4 oils are developed.

By Application, construction dominates, mining grows fastest

Construction held approximately 38% of the off-highway brake oil aftermarket in 2025. Construction equipment operates in environments that place extreme and variable demands on braking systems. Urban construction sites require frequent starts and stop as equipment manoeuvres in confined spaces with pedestrians, other equipment, and infrastructure in close proximity. Infrastructure construction on steep gradients and at high speeds places the most demanding thermal loads on hydraulic brake circuits. The global construction boom in Asia Pacific, Africa, and Latin America is expanding the total construction equipment fleet at rates that outpace fleet retirements, creating net installed base growth that drives aftermarket demand expansion. Global construction output is forecast to grow at above-average rates through 2035 in markets where infrastructure investment plans are most ambitious.

Mining is a high-value and growing application for off-highway brake oil. Large open-pit mining operations use haul trucks whose gross vehicle weights can exceed 400 tones fully loaded. The brake demands on these vehicles descending loaded from pit benches create heat generation in brake circuits that is unlike anything encountered in other off-highway or on-road vehicle categories. Brake fluid in mining haul trucks operates at temperatures and pressures that require the most thermally stable and highest boiling point formulations commercially available. The expansion of global mining activity driven by demand for copper, lithium, nickel, and iron ore for energy transition infrastructure and electric vehicle production is expanding the haul truck fleet and the associated brake oil aftermarket.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

76.4% |

|

Europe |

Germany |

27.8% |

|

Asia Pacific |

China |

42.3% |

|

Middle East & Africa |

South Africa |

29.4% |

|

Latin America |

Brazil |

43.8% |

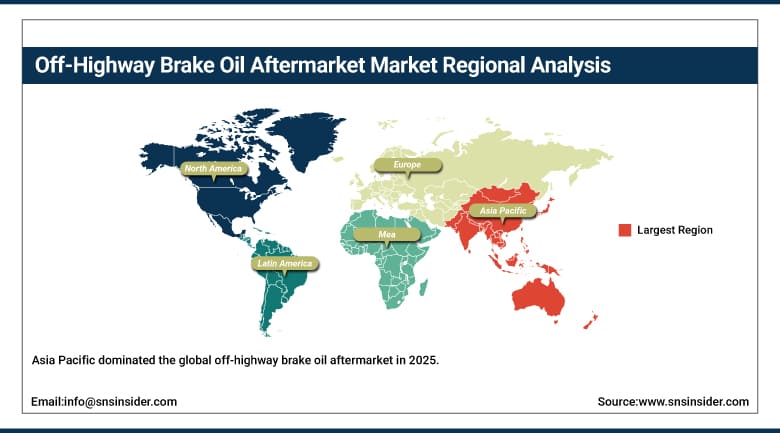

Asia Pacific Off-Highway Brake Oil Aftermarket Insights

Asia Pacific dominated the global off-highway brake oil aftermarket in 2025 through its extraordinary concentration of construction activity, the world's largest agricultural equipment fleets in China and India, and significant mining operations across Australia, Indonesia, and Southeast Asia. China accounts for approximately 42.3% of Asia Pacific revenues as the world's largest construction and agricultural equipment market whose massive domestic infrastructure investment programme sustains extraordinary off-highway vehicle fleet utilization rates and aftermarket service demand. India's construction equipment market is growing rapidly as its infrastructure investment programme accelerates, adding new vehicles to the aftermarket demand base at an above-average rate relative to other global regions.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Off-Highway Brake Oil Aftermarket Insights

North America maintains a large and established off-highway brake oil aftermarket supported by extensive agricultural, construction, and mining equipment fleets operating across the continent. The United States accounts for approximately 76.4% of North American revenues as the most commercially developed off-highway equipment aftermarket globally. North American equipment dealers operating John Deere, CNH Industrial, Caterpillar, and Komatsu service networks provide the primary distribution pathway for brake oil to the professional equipment operator segment. Canadian mining operations in Alberta's oil sands, Ontario's nickel belt, and British Columbia's coal and copper mining regions sustain significant brake oil demand from heavy mining equipment fleets operating under severe cold climate conditions. U.S. and Canadian agricultural equipment fleets represent one of the most predictable and stable off-highway brake oil demand segments globally. Precision agriculture technology adoption is enabling more condition-based brake fluid management among sophisticated farm operators who use telematics data to optimize maintenance scheduling.

Europe Off-Highway Brake Oil Aftermarket Insights

Europe is a mature off-highway brake oil market with well-established distribution networks, stringent product quality standards, and growing regulatory pressure on brake fluid chemistry and disposal. Germany accounts for approximately 27.8% of European revenues through its strong construction machinery industry presence, extensive agricultural sector, and the headquarters of major brake fluid manufacturers and distributors. EU chemical regulations including REACH are progressively reviewing the environmental and health classifications of glycol-based brake fluid components, creating regulatory-driven interest in alternative formulations among European equipment operators and fleet managers. European construction activity is expanding in Central and Eastern European markets receiving EU infrastructure funding through cohesion policy programmes. European agricultural equipment operators benefit from advanced precision farming infrastructure and telematics adoption that enables condition-based maintenance scheduling, potentially moderating the frequency of preventive brake fluid changes while ensuring replacement before degradation causes system problems.

MEA & Latin America Off-Highway Brake Oil Aftermarket Insights

The Middle East and Africa and Latin America are growing off-highway brake oil markets where infrastructure investment, agricultural development, and mining expansion are driving equipment fleet growth and associated aftermarket demand. South Africa leads MEA revenues at approximately 29.4% of the regional share through its established mining industry serving gold, platinum, coal, and iron ore production that maintains large haul truck and underground mining equipment fleets with intensive brake maintenance requirements. Brazil leads Latin American revenues at approximately 43.8% through its large agricultural equipment fleet serving soybean, sugarcane, and corn production, its growing construction equipment sector, and active mining operations across its iron ore, copper, and gold producing regions.

Market Dynamics

Growth Drivers: Expanding global off-highway vehicle fleet from construction and infrastructure investment in emerging markets are driving off-highway brake oil aftermarket growth.

Global construction and infrastructure investment is the most powerful structural driver of off-highway brake oil aftermarket growth. Government-funded infrastructure programmes in India, Southeast Asia, Africa, and Latin America are adding new construction equipment to operating fleets at above-average rates. Each new excavator, loader, bulldozer, and motor grader added to an operating fleet becomes a recurring aftermarket customer for brake oil throughout its service life. The scale of infrastructure investment commitments under programmes including India's National Infrastructure Pipeline, China's Belt and Road construction activity in developing markets, and African Development Bank infrastructure funding creates multi-year demand visibility for the off-highway brake oil market.

Energy transition metals demand is driving mining activity expansion that directly increases haul truck and mining equipment fleet sizes at operating mines and at newly permitted mine developments. Copper, lithium, nickel, cobalt, and manganese are all critical inputs for electric vehicles, grid storage batteries, and renewable energy infrastructure whose deployment rates are growing rapidly. Mine operators responding to strong long-term demand visibility for these metals are investing in fleet expansion that creates new brake oil aftermarket customers at mines whose operating profiles impose the most demanding brake fluid specifications of any off-highway application segment.

Restraints: Electric and hybrid off-highway vehicle adoption reducing conventional brake oil consumption are restraining off-highway brake oil aftermarket growth.

Electric and hybrid off-highway vehicle adoption represents a long-term structural threat to conventional brake oil demand in this market. Electric construction equipment and agricultural machinery using regenerative braking reduces the heat load on conventional hydraulic brake circuits, extending brake fluid service life and potentially enabling longer replacement intervals or reformulated lower-specification fluids at lower cost per vehicle per year. While the electric off-highway vehicle transition is much slower than the on-road passenger vehicle transition due to payload, range, and charging infrastructure requirements, it creates a medium-term demand moderation concern for conventional brake oil suppliers in markets where EV adoption is advancing fastest.

Intense price competition from low-cost brake oil manufacturers in Asia, particularly China, is compressing margins for established Western aftermarket brands in price-sensitive emerging market segments. Chinese-manufactured brake oil products meeting basic DOT specifications at prices significantly below Western branded equivalents are gaining market share among independent aftermarket distributors and fleet operators whose purchasing decisions are primarily price-driven in commodity brake fluid categories. Established brands compete through technical performance claims, extended service life, and distribution network relationships that do not transfer easily to lower-cost alternatives.

Opportunities: Synthetic extended-life formulation development for severe-duty applications and electric and hybrid off-highway vehicle specific fluid development represent the strongest off-highway brake oil aftermarket growth opportunities.

Synthetic extended-life brake oil formulations represent a premium growth opportunity in the off-highway aftermarket. Large mining and construction fleet operators with intensive equipment utilization and significant maintenance labor costs have a clear commercial incentive for brake fluids that require less frequent replacement without compromising braking system performance or reliability. A brake oil product that provides twice the service life of conventional alternatives at 1.5 times the per-litre cost delivers significant net cost savings to high-utilization fleet operators while simultaneously reducing maintenance downtime. Developing, validating, and commercially positioning extended-life formulations is therefore one of the most commercially attractive product development investments available to established aftermarket brake oil suppliers.

Digital fleet telematics integration with brake system monitoring creates a service model opportunity for brake oil suppliers who can move beyond product sales toward condition-based maintenance service agreements. Fleet management platforms that monitor brake system fluid condition through onboard sensors can trigger replenishment alerts and automated service scheduling when brake fluid condition deteriorates below defined thresholds. Brake oil suppliers who integrate with these platforms create procurement preference by connecting their products to the operational intelligence that fleet managers are increasingly relying on for maintenance scheduling decisions.

Recent Developments:

-

2025: Shell Lubricants expanded its Spirax range of off-highway brake and transmission fluids with new extended-life formulations targeting mining haul truck operators seeking longer change intervals and reduced maintenance downtime across large equipment fleets.

-

2025: Fuchs Petrolub introduced new synthetic brake fluid products specifically formulated for electric and hybrid construction equipment, addressing the different thermal and hydraulic profiles of brake systems in electrified off-highway vehicles entering commercial production.

-

2025: Castrol expanded its distribution network for off-highway maintenance products in Southeast Asian markets through new partnerships with Caterpillar and Komatsu dealer networks in Indonesia, Vietnam, and the Philippines serving rapidly growing construction equipment fleets.

Off-Highway Brake Oil Aftermarket Market Key Players are:

-

Shell plc

-

BP plc

-

TotalEnergies SE

-

Chevron Corporation

-

ExxonMobil Corporation

-

Fuchs Petrolub SE

-

Phillips 66 Lubricants

-

Lukoil Lubricants

-

Indian Oil Corporation Ltd.

-

BRB International BV

-

Halron Lubricants

-

Topaz Energy Group

-

Idemitsu Kosan Co. Ltd.

-

Morris Lubricants

-

Millers Oils Ltd.

-

Eurol BV

-

Repsol SA

-

Motul SA

-

Comma Oil & Chemicals Ltd.

-

Penrite Oil Company

Off-Highway Brake Oil Aftermarket Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 19.43 Billion |

| Market Size by 2035 | USD 28.8 Billion |

| CAGR | CAGR of 4.08% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Oil Type (DOT 3, DOT 4, DOT 5, DOT 5.1, Non-Petroleum Based) • By Application (Mining, Construction, Agriculture, Others) • By Vehicle Type (Agricultural Equipment, Construction Equipment, Mining Equipment, Others) • By Distribution Channel (OEM, Independent Aftermarket Distributors, Online) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Shell plc (Shell Lubricants), BP plc (Castrol), TotalEnergies SE, Chevron Corporation, ExxonMobil Corporation, Fuchs Petrolub SE, Phillips 66 Lubricants, Lukoil Lubricants, Indian Oil Corporation Ltd., BRB International BV, Halron Lubricants, Topaz Energy Group, Idemitsu Kosan Co. Ltd., Morris Lubricants, Millers Oils Ltd., Eurol BV, Repsol SA, Motul SA, Comma Oil & Chemicals Ltd., Penrite Oil Company |

Frequently Asked Questions

Asia Pacific dominated the off-highway brake oil aftermarket Market in 2025.

Construction dominated with approximately 38% of revenues in 2025.

Expanding global off-highway vehicle fleet from construction and infrastructure investment in emerging markets is the primary driver.

The off-highway brake oil aftermarket Market was valued at USD 19.43 Billion in 2025.

The off-highway brake oil aftermarket market is expected to grow at a CAGR of 4.08% from 2026 to 2035.

Get in Touch