-

Rising prevalence of diabetes is driving demand for pen needles, with over 540 million adults globally affected, supporting consistent consumption growth.

-

Increasing adoption of insulin pens over syringes is boosting pen needle usage, accounting for over 65% of insulin delivery methods in developed markets.

-

Demand for shorter and finer needles (4mm–6mm) is rising due to improved patient comfort, with over 70% patient preference for minimally painful options.

-

Growth in home healthcare and self-administration is expanding the market, with more than 60% of insulin users managing injections outside clinical settings.

-

Technological advancements such as safety pen needles are gaining traction, reducing needlestick injuries by up to 80% and increasing adoption in hospitals and clinics.

Pen Needles Market Size Analysis:

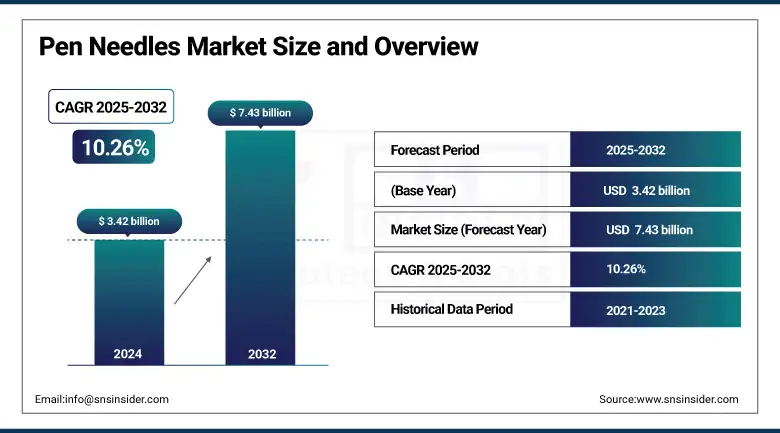

The Pen Needles Market size was USD 3.42 billion in 2024 and is expected to reach USD 7.43 billion by 2032, growing at a CAGR of 10.26% over the forecast period of 2025-2032.

The global pen needles market is experiencing strong growth, driven by the rising prevalence of diabetes and increased adoption of self-injection devices. Advancements in needle technology, including ultra-fine and safety-engineered designs, are enhancing patient comfort and compliance. Growing awareness about insulin delivery and expanding healthcare access, especially in emerging economies, further support market expansion. Additionally, the shift toward home-based care and the availability of pen needles through retail and online channels are contributing significantly to the market's upward trajectory.

Pen Needles Market Size and Forecast

-

Market Size in 2024: USD 3.42 Billion

-

Market Size by 2032: USD 7.43 Billion

-

CAGR: 10.26% from 2025 to 2032

-

Base Year: 2024

-

Forecast Period: 2025–2032

-

Historical Data: 2022–2024

To Get more information On Pen Needles Market - Request Free Sample Report

Pen Needles Market Trends:

U.S. pen needle market size outlook:

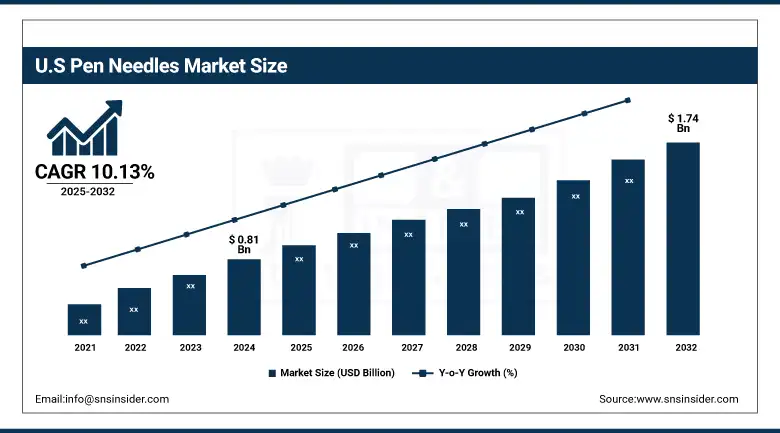

The U.S. pen needle market size was valued at USD 0.81 billion in 2024 and is expected to reach USD 1.74 billion by 2032, growing at a CAGR of 10.13% over the forecast period of 2025-2032. The U.S. dominates the North American pen needle market due to its high prevalence of diabetes, well-established healthcare infrastructure, and widespread adoption of advanced self-injection technologies. Strong insurance coverage and a growing preference for home-based care further reinforce the country's leading position.

Droplet Micron has launched a 34-gauge, 3.5mm pen needle in the U.S., available over the counter following FDA approval in April 2024, claimed as the world's thinnest and shortest needle.

Pen Needles Market Dynamics:

Drivers:

-

Rising Prevalence of Diabetes is Driving the Market Growth

Diabetes is one of the biggest global burdens, with behavioural risk factors such as unhealthy diet, physical inactivity, and increasing prevalence of obesity as the major contributors to new diabetes cases. As per the International Diabetes Federation, more than 530 million adults were living with diabetes in 2023, and this number is expected to rise sharply by 2030. This increase directly fuels the growth of insulin therapy, especially for Type 1 diabetes and also advanced Type 2 diabetes. As an essential part of insulin delivery through an injection pen, pen needles are widely used in daily self-management for diabetes, which is one of the main driving factors of the pen needles market growth.

According to a new high-profile international study published in the journal. The Lancet showed that the prevalence of adult diabetes has more than doubled globally, from 7% in 1990 to about 14% by 2022, affecting more than 800 million people globally.

Such an increase is driven by the epidemic of obesity, inactivity, and poor dietary habits. In the U.S. alone, an estimated 38 million diabetics with 2022 health care expenditures of more than USD 412.9 billion. The growing disease burden has led to a greater use of insulin therapies and the rise in demand for pen needles.

-

Advancements in Needle Technology are Propelling the Market Growth

Continuous innovations in technology, novel design, and functionality of pen needles increase patient comfort by making pen injections less painful. New and improved pen needles come in ultra-fine gauges (down to 32-gauge), shorter lengths, and can significantly decrease injection pain and limit the chance for intramuscular delivery (crucial for lean or pediatric patients). New needle designs minimize the chance of an unintentional needlestick injury, providing additional protection for both patients and caregivers. Such innovations have greatly enhanced user trust and therapy compliance, further promoting wider adoption and supporting market growth.

Roche Diabetes Care India launched the ACCU‑FINE range in May 2022, including ultra-soft coatings and 33-gauge, 4mm tips to offer comfort to the patient.

Restraints:

-

Cost Sensitivity in Low-Income Regions is Restraining the Market from Growing

One of the major restraints in the pen needle market analysis is the high cost of advanced products, such as ultra-fine, short, or safety-engineered needles, which are often priced significantly higher than standard variants. In low- and middle-income countries, where healthcare infrastructure is limited and insurance coverage is minimal or non-existent, patients frequently rely on out-of-pocket expenses for diabetes care. As a result, many individuals opt for more affordable but less safe or less comfortable alternatives, or in some cases, avoid treatment altogether due to cost concerns. This economic barrier restricts the widespread adoption of pen needles in these regions, despite the rising need for diabetes management tools.

Pen Needles Market Segmentation Analysis:

By Product

In 2024, the standard pen needles segment dominated the pen needles market with an 84.26% market share due to high availability and low cost, as these are widely used by diabetic patients for taking insulin externally. These needles are fully established, not only in clinical but also in home care settings in developing and price-sensitive markets where affordability is crucial. They remain prevalent, particularly amongst the patient population that is most used to traditional injection techniques, due to their compatibility with the vast majority of pen injectors and ease of use.

The safety pen needles segment is projected to gain significant market share over the next few years, owing to a rise in the number of needlestick injuries and needlestick injuries an emphasis on the safety of healthcare workers and patients. Safety-engineered devices are increasingly regulated in North America and Europe, leading to their higher adoption for use in hospital and clinical settings. Additionally, the rising number of self-injections at home and the enhancement in the incidence of the need for infection management devices is further expected to support the growth of tech-advanced, protection devices, and tools covered under this segment.

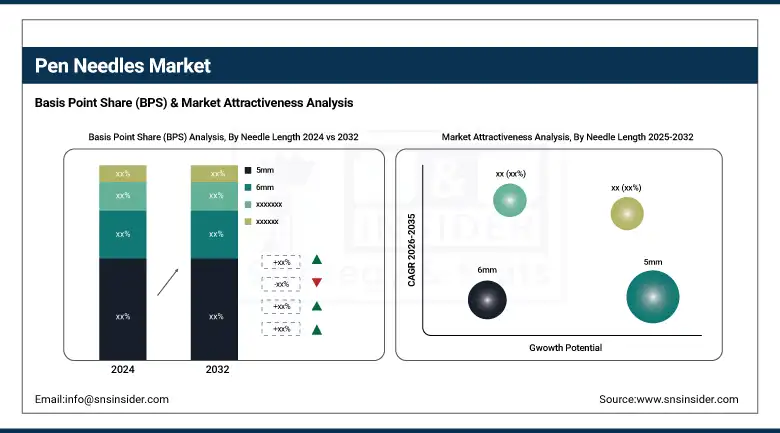

By Needle Length

The 5mm needle length segment accounted for 31.25% market share in the pen needles market in 2024, as it has a good balance of effectiveness and comfort, and it is preferred by most healthcare professionals and patients. Over the years, it has been a staple offering, delivering the right amount of insulin, preferably subcutaneously, but never penetrating too deeply. The majority of patients are familiar with this size, especially among adults, and due to its compatibility with many pen injectors, it is well established in both clinical and home care settings.

The 4 mm needle segment is expected to be the fastest-growing segment in the forecast period, owing to the demand for shorter needles to reduce intramuscular injection and less invasive needles (less anxiety to the patients). Ultra-short needles such as these are ideal for giving fast-acting insulin to small or thin patients (children, the elderly), but can be used by anyone who prefers less pain with their injections. The increasing focus on patient-centered care, improved needle quality, and an increasing preference for pain-free self-administration is moving the trend towards shorter needles, particularly 4mm.

By Therapy

The insulin segment led the pen needles market share in 2024 with an 86.15%, which is attributed to the higher global patient population for the diabetes condition and preference of insulin therapy as the mainstay treatment for both Type 1 and Type 2 diabetic patients. Tens of millions of diabetic patients rely on daily injections of insulin, most commonly delivered through pen devices combined with pen needles. The established clinical history of everyone using insulin pens provides a steady inflow of shoppers, and solid backing from healthcare providers makes this the most established and best-selling therapy category in the marketplace.

Glucagon-like-peptide-1 (GLP-1) segment is expected to grow fastest in the forecast years due to the increasing use of GLP-1 receptor agonists for the treatment of Type 2 diabetes and obesity. These non-insulin injectable therapies offer extra advantages- weight loss, cardiovascular safety, and reduced risk of hypoglycemia, and these advantages are driving the use of these agents. Once-weekly GLP-1 injections are increasingly being clinically endorsed, and as indications expand, patient preference for once-weekly GLP-1 injections will ultimately drive a rapid uptake of pen needles compatible with these therapies.

By Distribution Channel

In 2024, the pen needles market was dominated by the retail pharmacies segment with a 68.08% market share, as it provides wide accessibility to direct patients and an increased level of trust among patients while also providing company products on a wider scale, thus providing product availability on a stagnant note. Retail pharmacies, such as local pharmacy, are an important purchasing channel for diabetic products including pen needles, as chronic disease patients are inclined to seek in-person purchase and fast refill availability; Moreover, these pharmacies tend to have excellent ties with healthcare providers and insurance networks that ensure repeat prescription sales and improve patient productivity.

The online channels segment is expected to grow at the fastest pace over the years, owing to the increasing transition to digital healthcare and e-commerce platforms. The convenience of discreet purchasing, competitive pricing, and home delivery options is attracting more patients towards the online channels, especially among the patients treated for diabetes self-therapy. As such, increasing penetration of telehealth services and advancing internet penetration in emerging economies is allowing for pen needles to be distributed online, thereby aiding the fast growth of this distribution segment in the market.

By End-use

The home care settings segment dominated the pen needles market with a 58.22% market share due to an increase in self-administration of injectable therapies in this segment in 2024. Factors, such as convenience, cost-effectiveness, and improved quality of life have led to a rise in patients with chronic illnesses, such as diabetes embracing home-based management of their treatment. The emergence of handy pen needles, along with educating patients for home use, has also helped to enable patients to self-inject. This is especially notable amidst the aging population and among those who prefer to take control of their health.

During the forecast period, the hospitals and clinics segment is estimated to witness the fastest growth, due to the increasing number of hospital admissions arising from complications of diabetes and the need for professional monitoring of administered injectable therapies. Healthcare sites are placed into opting for high-performance safety pen needles owing to the rising safety issues associated with issues, such as needlestick injuries. Adoption is further accelerated in clinical practice by the continued proliferation of outpatient and specialty diabetes clinics, together with better reimbursement and the incorporation of pen-based therapies into institutional protocols.

Pen Needles Market Regional Insights:

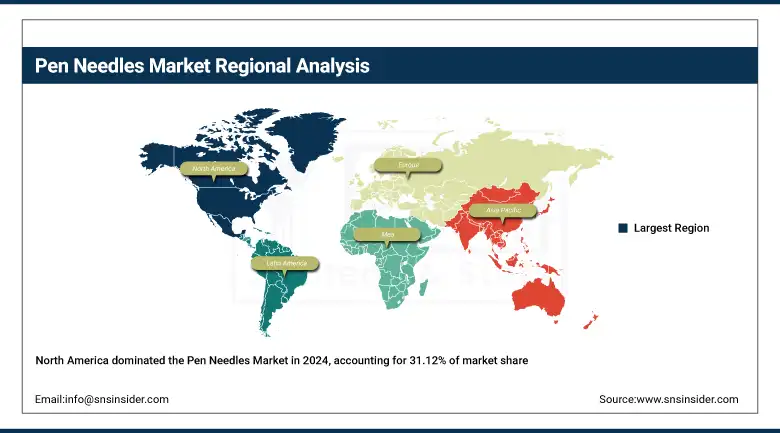

The pen needles market is dominated by North America with a 31.12% market share in 2024 due to excellent advanced health care facilities, the prevalence of diabetes, and the high use of self-injection devices for chronic disease management. Robust reimbursement structures, appealing regulations, and a well-educated patient population mean the region will continue to see steady, repeat use of pen needles for insulin and other therapies. Moreover, continuous innovations in needle technology (safety needles/ultra-fine needles) and high adoption of home care settings backed by the presence of major market players, enhance the regional leadership.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific is the fastest-growing pen needle market with a 10.93% CAGR over the forecast period, owing to the rapidly increasing number of diabetic patients in the region, mainly in China and India. The increasing prevalence of healthcare awareness among the population, the increasing geriatric population, and access to healthcare facilities in urban and rural places will boost the growth of easy-to-use and cost-effective injection devices are the major driving factors for the market. Additionally, the growing government initiatives for diabetes care, the increasing healthcare infrastructure, coupled with the increasing affordability of diabetes treatment options, are further supporting the market growth. In addition, increasing home-based treatment and increasing penetration of e-commerce platforms are allowing pen needles to be more available and accessible in this region.

The pen needle market trends are expanding across Europe substantially, due to the increasing diabetes prevalence, the rise in the geriatric population, and the growing obesity prevalence. Robust healthcare infrastructure in this region, along with growing awareness regarding diabetes treatment and the introduction of advanced pen needle technologies (particularly safety-engineered and ultra-fine needles), is expected to drive the market growth shortly. The growth of the market on the continent is attributed to the regulatory support and focus on patient safety.

Similarly, other nations, such as Germany, the U.K., and France are leading this augmentation due to established reimbursement scenarios along with government-backed efforts promoting self-care and diabetes education. Increasingly, pen needles are also being integrated into diabetes care regimes, particularly for home use, by public health systems and healthcare providers alike. Furthermore, the remarked large number of key market players, and the constant development of new design needles, lead to almost no barriers in consuming and adopting the products throughout the region.

The pen needle market is moderately growing in Latin America, primarily due to the increasing prevalence of diabetes and enhanced awareness towards self-injection. The country is seeing rising needs for safe and simple injection devices as public healthcare is slowly improving. The availability of pen needles in urban and semi-urban areas is driven by government-led health campaigns in addition to the growing presence of local distributors and international manufacturers.

The moderate growth in the Middle East & Africa (MEA) region is attributed to the rising geriatric population, rising prevalence of lifestyle-related diseases including diabetes, and improved access to healthcare. Countries such as Saudi Arabia, the UAE, South Africa, and Egypt are investing in improved chronic disease management solutions, including pen needles. Even though affordability and low awareness still plague several emerging economies, persistent health care reforms and a rise in the number of private health care providers are paving ways for the way for a thriving landscape for the pen needle market in the foreseeable future.

Key Players in the Pen Needles Market:

The major pen needle market companies, BD (Becton, Dickinson and Company), Novo Nordisk A/S, Terumo Corporation, Owen Mumford Ltd., Ypsomed Holding AG, Allison Medical, Inc., HTL-Strefa S.A. (a MTD Group company), Artsana S.p.A. (Pic Solution), Arkray, Inc., UltiMed, Inc., and other players.

Recent Developments in the Pen Needles Market:

-

April 2025 – Owen Mumford launches UnifineOTC, a new line of over-the-counter pen needles to assist pharmacies in the improved care of patients living with diabetes. As a response to increasing out-of-pocket healthcare expenses, UnifineOTC merges the trusted quality of Unifine with a low MSRP from the manufacturer.

-

March 2024 – Ypsomed entered into a deal with Medical Technology and Devices S.p.A. (MTD) for the sale of its pen needle and blood glucose monitoring system (BGM) businesses. The deal will see MTD ensure a long-term supply of Ypsomed's proprietary pen needle products under its guidance.

-

September 2022 – Terumo India, the Indian arm of Terumo Corporation, has introduced FineGlide, a sterile pen needle suitable for patients needing frequent insulin injections or self-injections. FineGlide is usable with most commonly used pen devices across India and is designed to promote patient comfort, thus enhancing treatment compliance and overall drug compliance.

Pen Needles Market Report Scope:

Report Attributes Details Market Size in 2024 USD 3.42 Billion Market Size by 2032 USD 7.43 Billion CAGR CAGR of 10.26% From 2025 to 2032 Base Year 2024 Forecast Period 2025-2032 Historical Data 2021-2023 Report Scope & Coverage Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook Key Segments • By Product (Standard Pen Needles, Safety Pen Needles)

• By Needle Length (4mm, 5mm, 6mm, 8mm, 10mm, 12mm)

• By Therapy (Insulin, Glucagon-like-peptide-1, Growth Hormone)

• By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Channels)

• By End-Use (Hospitals and Clinics, Home Care Settings, Other End-Users)

Regional Analysis/Coverage North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) Company Profiles BD (Becton, Dickinson and Company), Novo Nordisk A/S, Terumo Corporation, Owen Mumford Ltd., Ypsomed Holding AG, Allison Medical, Inc., HTL-Strefa S.A. (a MTD Group company), Artsana S.p.A. (Pic Solution), Arkray, Inc., UltiMed, Inc., and other players.

Get in Touch