Permanent Magnet Motor Market Report Scope & Overview:

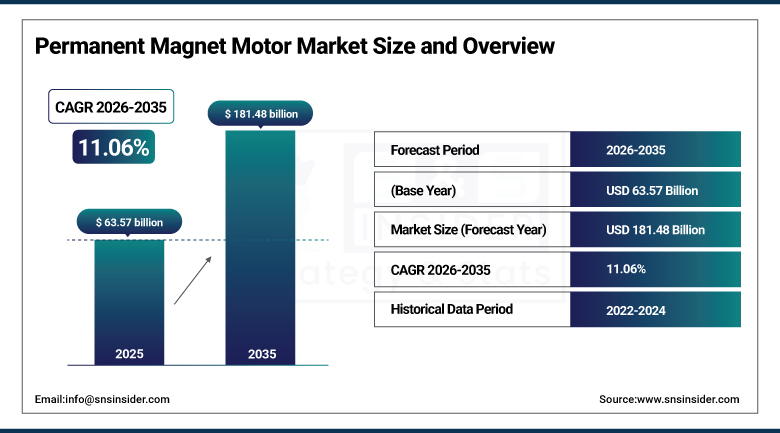

The Permanent Magnet Motor Market was valued at USD 63.57 billion in 2025 and is expected to reach USD 181.48 billion by 2035, growing at a CAGR of 11.06% from 2026-2035.

The Permanent Magnet Motor market has been propelled by factors such as rise in the usage of electric vehicles, rising demand for energy-efficient motors, and fast-paced industrial automation. The focus on cutting down carbon footprint and improving efficiency has helped drive its adoption in the automobile industry, manufacturing industry, and renewable energy sector. Furthermore, technological advancements in the field of motor, coupled with the rise in robotics and smart manufacturing, have also been responsible for pushing its demand.

For instance, over 70% of modern electric vehicles now incorporate permanent magnet motors due to their high torque density and compact size.

Market Size and Forecast

-

Market Size in 2025: USD 63.57 Billion

-

Market Size by 2035: USD 181.48 Billion

-

CAGR: 11.06% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Permanent Magnet Motor Market - Request Free Sample Report

Permanent Magnet Motor Market Trends

-

Rising demand for energy-efficient and high-performance electric motors is driving the permanent magnet motor market.

-

Growing adoption across electric vehicles, industrial automation, HVAC systems, and renewable energy applications is boosting market growth.

-

Expansion of electrification trends in transportation and manufacturing is fueling motor deployment.

-

Increasing focus on reducing energy consumption, improving torque density, and enhancing operational efficiency is shaping adoption trends.

-

Advancements in rare-earth magnet materials, motor design, and power electronics integration are enhancing performance.

-

Rising investments in clean energy transition and sustainable mobility are supporting market expansion.

-

Collaborations between motor manufacturers, automotive OEMs, and industrial equipment providers are accelerating innovation and global adoption.

U.S. Permanent Magnet Motor Market Size Outlook:

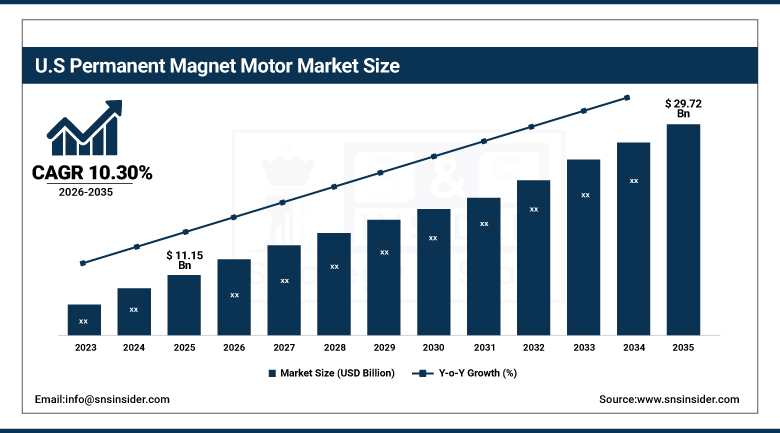

The U.S. Permanent Magnet Motor Market was valued at USD 11.15 billion in 2025 and is expected to reach USD 29.72 billion by 2035, growing at a CAGR of 10.30% from 2026-2035. Growth in U.S. Permanent Magnet Motor Industry is fueled by increased penetration of electric cars, robust industrial automation, and escalating demand for efficient energy use. Renewable energy initiatives, enhanced manufacturing facilities, and ongoing advancements in technology associated with motor design are also playing a pivotal role in market expansion.

Permanent Magnet Motor Market Segment Highlights

-

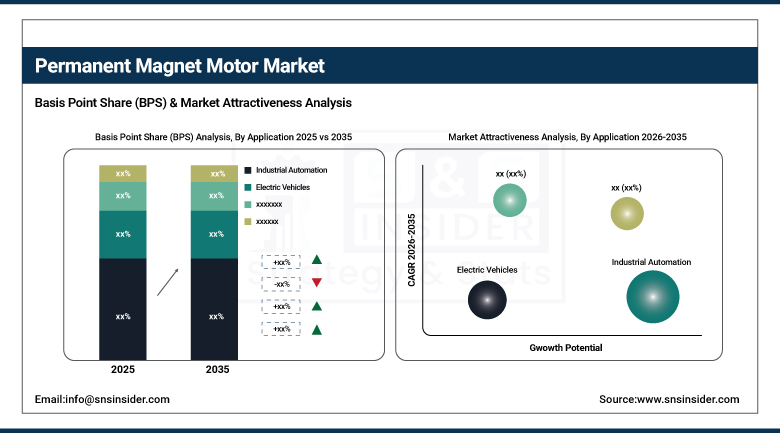

By Application, Industrial Automation segment dominated the Permanent Magnet Motor Market in 2025 with approximately 34% share; Electric Vehicles segment fastest growing.

-

By Type, Brushless DC Motors segment dominated the Permanent Magnet Motor Market in 2025 with approximately 38% share; Synchronous Motors segment fastest growing.

-

By End-User, Manufacturing segment dominated the Permanent Magnet Motor Market in 2025 with approximately 36% share; Transportation segment fastest growing.

-

By Cooling Method, Air-Cooled segment dominated the Permanent Magnet Motor Market in 2025 with approximately 58% share; Liquid-Cooled segment fastest growing.

By Application, Industrial Automation segment dominates the Permanent Magnet Motor Market, Electric Vehicles segment expected to grow fastest

The Industrial Automation segment had the largest share in the Permanent Magnet Motor Market in 2025 because of extensive use of efficient motors in robotic applications, conveyors, and other manufacturing machines. Increased usage of energy-saving motors and automation devices in the production processes was another reason for this trend. Digital transformation and productivity enhancement in industries also contributed to its growth and made permanent magnet motors more popular due to their consistency, reliability, and efficiency.

The Electric Vehicles segment is the fastest-growing owing to the rapid electrification trend worldwide and aggressive emission reduction goals set by nations. Electric vehicles commonly use permanent magnets in motors owing to their high efficiency, compactness, and excellent torque characteristics. The growing network of electric vehicles, declining costs of batteries, and increased consumer acceptance of electric vehicles are contributing to increased demand.

By Type, Brushless DC Motors segment dominates the Permanent Magnet Motor Market, Synchronous Motors segment expected to grow fastest

The Brushless DC Motors segment occupied the largest share in the Permanent Magnet Motor Market in 2025 owing to their high efficiency, maintenance-free nature, and excellent speed control. They are widely utilized in various industries in order to ensure reliable operations as well as better performance. The higher operating life of brushless DC motors makes them an extremely popular choice among consumers. Moreover, technological advancements in motor technologies are driving their wide usage.

The Synchronous Motors segment accounted for the fastest-growing segment owing to their increasing demand for efficient and precise motor systems. They provide high efficiency and stability along with a better power factor, which makes them preferable for industrial as well as EV purposes. Increased emphasis on electrification and renewable energy sources along with advancements in motor control systems technology is expected to drive its growth.

By End-User, Manufacturing segment dominates the Permanent Magnet Motor Market, Transportation segment expected to grow fastest

The manufacturing segment had the largest market share in the Permanent Magnet Motor Market in 2025. This was attributed to the widespread usage of motors in machines, assembly lines, and automated manufacturing plants. The need for reliable, durable, and efficient motors in continuous operations in industries results in high demand. The trend is expected to continue due to the growth in industrialization, smart factory development, and automation technology adoption.

The transportation segment is projected to have the highest growth rate among all segments. The rise in electrification of automobiles, trains, and ships is fueling the segment's growth rate. Motors are popular because of their superior torque density, compact size, and efficiency. In addition, favorable government policies, growing investments in electric vehicle charging infrastructure, and innovations in electric propulsion technology are expected to drive the market.

By Cooling Method, Air-Cooled segment dominates the Permanent Magnet Motor Market, Liquid-Cooled segment expected to grow fastest

Air-Cooled segment had the largest market share in the Permanent Magnet Motor market in 2025 owing to the simplicity in design, low costs, and easy maintenance features of this type. Air-cooling systems are extensively used in typical applications in industries that have moderate heat production levels. The reliable nature and ease of installation associated with this segment contribute to their dominance across different industry segments. Adoption of air-cooled motors in the manufacturing and automation segments also drives dominance, given that air-cooled motors have adequate capacity for use in such applications.

The Liquid-Cooled segment is the fastest-growing because of rising demand for high-performing motors used in electric cars and industrial processes. The use of liquid cooling technology ensures effective temperature regulation and, thus, allows motors to work optimally under harsh conditions. Increased use of electric cars and automation systems is expected to increase the demand for motors that are small yet have high power density.

Market Regional Insights

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

90.8% |

|

Europe |

United Kingdom |

22.3% |

|

Asia Pacific |

Australia |

8.9% |

|

Middle East & Africa |

UAE |

13.5% |

|

Latin America |

Brazil |

48.2% |

Asia Pacific Permanent Magnet Motor Market Insights

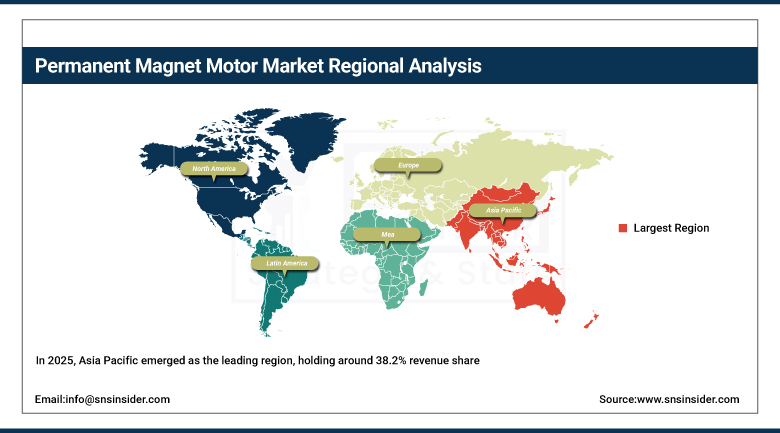

In 2025, Asia Pacific emerged as the leading region, holding around 38.2% revenue share in the Permanent Magnet Motor Market. The supremacy of the region is backed by the presence of an extensive industrial manufacturing ecosystem, widespread electrification of transportation, and extensive usage of automation technology. Growing production of electric vehicles, increasing installation of renewable energy sources, and increased need for energy-efficient motors played a significant role in establishing the region's stronghold.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Permanent Magnet Motor Market Insights

The North American region possesses a notable presence in the Permanent Magnet Motor Market owing to the increased utilization of electric cars, industrial automation, and advanced manufacturing processes. Such a scenario is supported by the presence of a strong automotive and aerospace industry base, investments made in the development of clean energy products, and the quick adoption of energy-efficient motor systems. The emphasis on the reduction of carbon emissions and improved efficiency will boost the market's growth.

Europe Permanent Magnet Motor Market Insights

Europe represents a strong market for permanent magnet motors due to stringent environmental policies, rising popularity of electric vehicles, and advanced industrial automation processes. There is an increased utilization of energy-saving technologies in the automobile industry, renewable energy, and manufacturing industries. The focus on sustainability and carbon neutral goals promotes the application of highly efficient motor systems. Innovations, research and development activities, and prominent industrial manufacturers contribute to market growth in major European countries.

Middle East & Africa and Latin America Permanent Magnet Motor Market Insights

Middle East & Africa and Latin America can be considered as developing markets for permanent magnet motors owing to ongoing industrialization and infrastructure developments. Increasing investments in renewable energy initiatives and modernizing efforts in the transportation industry have been promoting the use of energy-efficient motors. Increased manufacturing operations and growing attention towards automation will serve as other factors propelling the market forward. Even though there are no notable adoption rates yet, positive economic scenarios and governmental efforts towards industrial diversification should facilitate future growth potential.

Market Dynamics

Market Growth Drivers: Rapid electrification of vehicles and growing adoption of energy efficient motor systems across automotive and transportation industries worldwide

The increasing demand for electric automobiles, hybrid vehicles, and transportation systems electrification has significantly contributed to encouraging the widespread adoption of permanent magnet motors globally. The benefits offered by these motors consist of high efficiency, compact design, and excellent torque performance, making them essential components of electric automobile propulsion systems. In addition, as automobile manufacturers develop a greater interest in integrating the latest technologies in motors, they will be able to adhere to environmental regulations and fuel consumption standards. Thanks to the evolution in charging stations and government incentives, the production of electric automobiles is escalating.

Market Restraints: High manufacturing and maintenance costs restricting wider adoption in cost-sensitive industrial and commercial applications

The use of permanent magnet motors is associated with relatively high initial manufacturing expenses in contrast to traditional motor manufacturing because of the need for special materials and accurate production processes. The presence of expensive rare earth magnets and complicated design leads to the increase in the final price of the motor. Moreover, maintenance and part replacements add to operational expenses. Sectors, where cost effectiveness is an important factor, remain cautious about implementing these types of motors, even when considering their advantages. Small companies lack resources needed for the implementation of this innovation.

Market Opportunities: Rising investments in renewable energy and industrial electrification projects supporting long-term demand for high efficiency motor solutions

The growing number of renewable energy sources like wind turbines and solar power plants leads to the rising use of permanent magnet motors in energy generation. Electrification in industry promotes the transition from old systems to motorized energy-saving solutions. The heightened attention to energy savings and efficiency contributes to the adoption of these devices in the industrial and utility sectors. State programs for the implementation of clean energy sources and carbon emissions reduction stimulate investments in these motors. Innovative technology development and integration with intelligent control systems create new application fields, thus ensuring growth prospects worldwide.

Recent Developments:

-

2026: ABB launched next-generation permanent magnet motor series with water-jacket cooling and high-efficiency IE5 performance, designed for marine, HVAC, and industrial variable-speed drive applications requiring compact, high-torque solutions.

-

2026: Siemens expanded SIMOTICS permanent magnet motor platforms for EV, industrial automation, and renewable energy systems, focusing on higher torque density and improved energy efficiency for next-generation electrified systems.

-

2025: Yaskawa expanded Sigma-X servo motor systems using high-efficiency permanent magnet designs, improving torque density and precision control for robotics and semiconductor manufacturing equipment.

-

2024: Rockwell released firmware and drive enhancements for PowerFlex 6000T medium-voltage drives, improving control performance for permanent magnet motors in high-speed industrial applications such as compressors and pumps.

Permanent Magnet Motor Companies are:

-

ABB Ltd

-

Siemens AG

-

Mitsubishi Electric Corporation

-

Toshiba Corporation

-

WEG S.A.

-

Wolong Electric Group

-

Rockwell Automation

-

TECO Electric & Machinery

-

Johnson Electric Holdings Limited

-

Yaskawa Electric Corporation

-

Hitachi Ltd

-

Schneider Electric

-

Danfoss

-

Parker Hannifin

-

Ametek Inc.

-

Emerson Electric Co.

-

Baldor Electric Company

-

Franklin Electric

Permanent Magnet Motor Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 63.57 Billion |

| Market Size by 2035 | USD 181.48 Billion |

| CAGR | CAGR of 11.06% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Application (Electric Vehicles, Industrial Automation, Home Appliances, Renewable Energy and Robotics) • By Type (Synchronous Motors, Brushless DC Motors, Stepper Motors and Switched Reluctance Motors) • By End-User (Transportation, Manufacturing, Residential and Commercial) • By Cooling Method (Air-Cooled and Liquid-Cooled) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | ABB Ltd, Siemens AG, Nidec Corporation, Mitsubishi Electric Corporation, Toshiba Corporation, WEG S.A., Wolong Electric Group, Rockwell Automation, Regal Rexnord Corporation, TECO Electric & Machinery, Johnson Electric Holdings Limited, Yaskawa Electric Corporation, Hitachi Ltd, Schneider Electric, Danfoss, Parker Hannifin, Ametek Inc., Emerson Electric Co., Baldor Electric Company, Franklin Electric. |

Frequently Asked Questions

Answer: Asia Pacific dominated the Permanent Magnet Motor Market in 2025.

Answer: The Industrial Automation segment dominated the Permanent Magnet Motor Market in 2025.

Answer: Rapid electrification of vehicles and growing adoption of energy efficient motor systems across automotive and transportation industries worldwide.

Answer: The Permanent Magnet Motor Market was valued at USD 63.57 billion in 2025.

Answer: The Permanent Magnet Motor Market is expected to grow at a CAGR of 11.06% from 2026 to 2035.

Get in Touch