Whole Slide Imaging Market Report Scope & Overview:

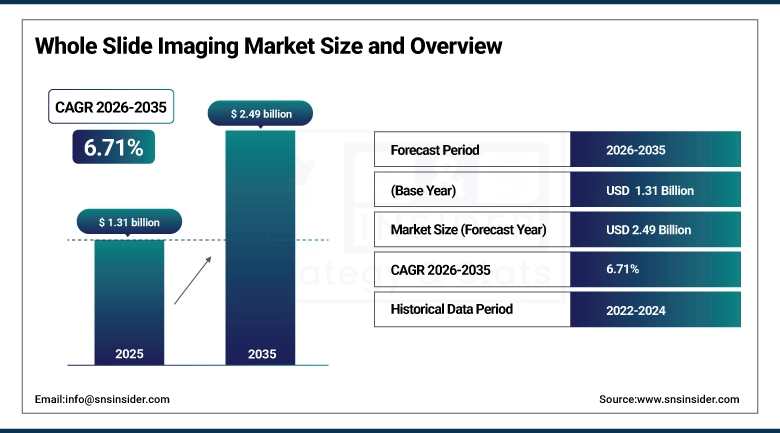

The Whole Slide Imaging Market was valued at USD 1.31 Billion in 2025 and is expected to reach USD 2.49 Billion by 2035, growing at a CAGR of 6.71% from 2026-2035.

The Whole Slide Imaging (WSI) Market is witnessing strong growth fueled by rising demands for digital pathology systems which facilitate fast and accurate diagnosis, collaborative efforts, and efficient processes. Innovations in high-resolution scanning, fluorescence and bright-field imaging techniques, AI-assisted image analysis software, and advanced IT solutions have widened the scope of clinical and experimental studies in numerous fields ranging from telepathology, immunohistochemistry, cytopathology, to hematopathology. The growing prevalence of chronic illnesses, including cancer, heart diseases, and various infections, drives continued interest in digital pathology, alongside the trends towards personalized treatments and drug development.

Supporting this trend, the World Health Organization (WHO) reported that cancer accounted for 9.7 million deaths globally in 2022, with projections of more than 20 million new cases annually by 2030, underscoring the urgent need for advanced diagnostic technologies.

Furthermore, in 2025, Leica Biosystems announced the launch of its next-generation Aperio GT 450 DX scanner, capable of scanning over 450 slides per day, exemplifying how technological innovation is accelerating adoption of WSI across hospitals, research institutes, and pharmaceutical companies worldwide.

Market Size and Forecast:

-

Market Size in 2025: USD 1.31 Billion

-

Market Size by 2035: USD 2.49 Billion

-

CAGR: 6.71% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Whole Slide Imaging Market - Request Free Sample Report

Whole Slide Imaging Market Trends:

-

Rapid digital pathology adoption as hospitals and labs transition from glass slides to digital workflows.

-

AI and machine learning integration enhancing diagnostic accuracy, especially in oncology and complex disease detection.

-

Telepathology expansion enabling remote consultations and collaboration across geographies.

-

Regulatory approvals (e.g., FDA clearance for primary diagnosis) accelerating clinical adoption of WSI systems.

-

Advances in scanner technology with higher resolution, faster throughput, and fluorescence imaging capabilities.

-

Cloud-based image management supporting large-scale storage, sharing, and analysis of pathology data.

-

Growing use in pharmaceutical R&D for drug discovery, biomarker analysis, and clinical trials.

-

Personalized medicine demand fueling adoption of WSI for precision diagnostics and targeted therapies.

-

Cost efficiency and workflow optimization making WSI attractive for hospitals, research institutes, and biotech companies.

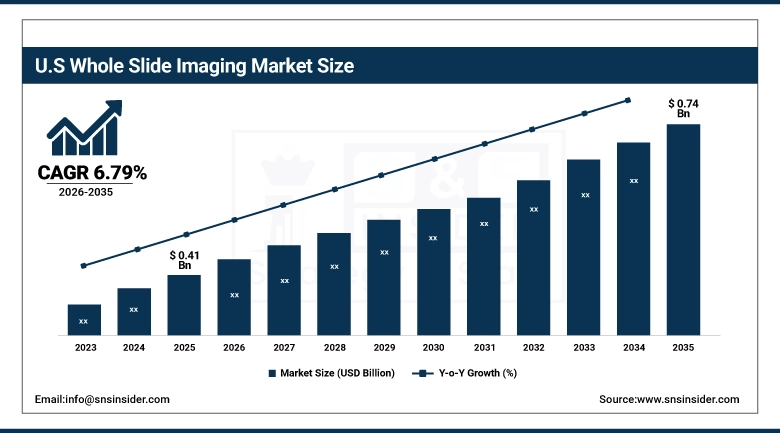

U.S. Whole Slide Imaging Market was valued at USD 0.41 Billion in 2025 and is expected to reach USD 0.74 Billion by 2035, growing at a CAGR of 6.79% from 2026-2035.

The U.S. WSI Market is considered to be the largest globally owing to the superior health care infrastructure, well-established reimbursement policies, and availability of prominent digital pathology vendors like Philips, Leica Biosystems, Roche, and Hamamatsu Photonics. Reimbursement Policies of CMS for digital pathology and diagnostic imaging have been favorable and have been promoting the use of digital pathology.

Supporting this trend, the U.S. Centers for Disease Control and Prevention (CDC) reported that cancer remains the second leading cause of death in the country, with approximately 1.9 million new cancer cases diagnosed in 2024, underscoring the urgent need for advanced diagnostic technologies such as Whole Slide Imaging.

In addition, the U.S. Food and Drug Administration (FDA) has expanded approvals for digital pathology systems, including the clearance of the Philips IntelliSite Pathology Solution for primary diagnosis, marking a pivotal milestone in enabling WSI for routine clinical use.

Whole Slide Imaging Market Segment Highlights:

-

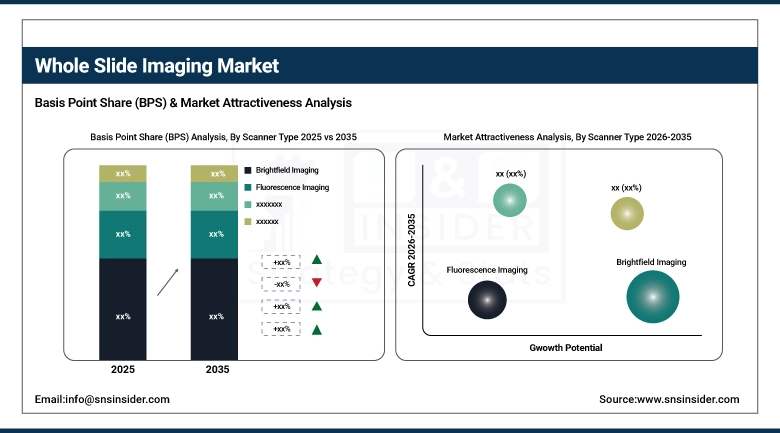

By Scanner Type, Brightfield Imaging dominated the Whole Slide Imaging Market with 50.54% share in 2025; Fluorescence Imaging fastest growing (CAGR).

-

By Technology, Scanners dominated the Whole Slide Imaging Market with 41.32% share in 2025; Image Management Systems Centers fastest growing (CAGR).

-

By Application, Telepathology dominated the Whole Slide Imaging Market with 37.38% share in 2025; Immunohistochemistry fastest growing (CAGR).

-

By End User, Hospitals & Clinical Labs dominated the Whole Slide Imaging Market with 46.47% share in 2025; Pharmaceutical & Biotech Companies fastest growing (CAGR).

Whole Slide Imaging Market Segment Analysis:

By Scanner Type, Brightfield Imaging segment dominates the Whole Slide Imaging Market, Fluorescence Imaging segment expected to grow fastest

In 2025, the Brightfield Imaging division retained its leadership position in the Whole Slide Imaging market with a market share of around 50.54%. The brightfield imaging division comprises advanced whole slide imaging scanners used for the acquisition of images from H&E-stained slides in routine histopathological applications. The dominance of this division can be attributed to the high usage rates of these systems in diagnostic applications owing to their ability to provide gold-standard imaging.

Between 2026 and 2035, the Fluorescence Imaging segment is expected to register the highest CAGR in the Whole Slide Imaging market. Advanced fluorescence imaging systems, which are capable of providing multi-multiplex staining, fluorescent imaging, and cellular imaging, are included in this segment.

By Technology, Scanners segment dominates the Whole Slide Imaging Market, Image Management Systems segment expected to grow fastest

In 2025, the Scanners category retained its dominant share in the Whole Slide Imaging Market, capturing about 41.32% of total market revenue. This category comprises high-throughput, mid-throughput, and low-throughput whole slide imaging scanners that provide the foundation for digital pathology processes by helping to capture the images from physical glass slides.

Between 2026 and 2035, the Image Management Systems (IMS) category is expected to demonstrate the highest CAGR in the whole slide imaging market. The segment represents software solutions that help manage the digital pathology image data, including storage, organization, retrieval, and sharing.

By Application, Telepathology segment dominates the Whole Slide Imaging Market, Immunohistochemistry segment expected to grow fastest

Telepathology was the dominating market segment in the Whole Slide Imaging Market during 2025, contributing nearly 37.38% to the overall market share. The telepathology market segment covers services like primary diagnosis, secondary opinion consultation, and slide viewing via different geographic locations. The telepathology market segment is driven by the rising need for remote diagnostics in regions that lack the expertise of qualified pathologists.

During 2026-2035, the Immunohistochemistry (IHC) market segment is anticipated to witness the fastest growth rate (CAGR). The IHC market segment comprises the use of whole slide imaging technology for assessing the methods involved in detecting specific antigens in tissue samples with the help of antibodies. Increasing incidence of cancer and personalized medicine are among the key factors driving the IHC market segment.

By End User, Hospitals & Clinical Labs segment dominates the Whole Slide Imaging Market, Pharmaceutical & Biotech Companies segment expected to grow fastest

The Hospitals & Clinical Labs segment was the most dominant one in the Whole Slide Imaging Market during 2025, contributing about 46.47% to the market's total revenue. The Hospitals & Clinical Labs segment is comprised of medical facilities that employ WSI equipment in clinical diagnosis. This segment is expected to dominate the market as more healthcare facilities adopt digital pathology technology over conventional microscopic pathology methods.

The Pharmaceutical & Biotech Companies segment is predicted to experience the highest compound annual growth rate from 2026 to 2035. The Pharmaceuticals & Biotech Companies segment incorporates organizations that heavily rely on Whole Slide Imaging techniques in their drug discovery processes, preclinical research, and clinical trials.

Regional Analysis:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

40.36% |

|

Europe |

Germany |

26.85% |

|

Asia Pacific |

China |

21.66% |

|

Middle East & Africa |

UAE |

4.39% |

|

Latin America |

Brazil |

6.74% |

North America Whole Slide Imaging Market Insights

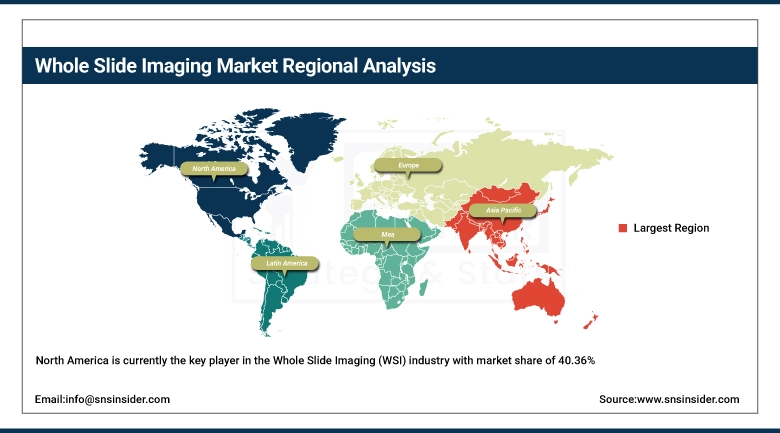

North America is currently the key player in the Whole Slide Imaging (WSI) industry with market share of 40.36%, owing to the advanced healthcare infrastructure, supportive reimbursement policies, and rapid adoption of digital pathology technology in the region. From 2025 to 2035, North America will continue to be the top region. The major factors driving growth in the region include increasing incidences of cancer and other chronic ailments, FDA clearance of WSI devices for use in primary diagnosis, and presence of top companies, including Philips, Leica Biosystems, Roche, and Hamamatsu Photonics.

Supporting this dominance, the U.S. Food and Drug Administration has enabled the clinical adoption of whole slide imaging through multiple regulatory clearances for primary diagnosis, beginning with the first approval in 2017. This regulatory momentum has contributed to widespread institutional uptake, with the United States accounting for approximately 82.1% of the North American Whole Slide Imaging market share in 2025, reflecting its strong leadership in digital pathology implementation and infrastructure.

According to insights from the American Society for Clinical Pathology, over 60% of pathology laboratories in the U.S. are actively using or piloting digital pathology workflows by 2025, highlighting the rapid transition from conventional microscopy to digital platforms.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Whole Slide Imaging Market Insights

The Asia Pacific is expected to see the highest CAGR of 8.12% through 2026-2035, owing to the confluence of fast-growing healthcare infrastructure, growing use of digital pathology, and robust investments from the government to upgrade hospitals. Some of the major economies in the region include China, Japan, India, South Korea, and Australia. Amongst these, China contributes significantly to the revenue of this market. Population growth, prevalence of cancer cases, and pharmaceutical industry growth are some other key factors driving the growth of the market.

Supporting this growth, China’s National Health Commission (NHC) announced in 2025 a nationwide initiative to accelerate adoption of digital pathology and Whole Slide Imaging systems, allocating significant funding for hospital modernization and AI‑enabled diagnostic platforms.

In parallel, the Japanese Ministry of Health, Labour and Welfare (MHLW) expanded reimbursement coverage for digital pathology services, including WSI‑based cancer diagnostics, reinforcing Japan’s leadership in advanced healthcare technology. Furthermore, in 2025, Hamamatsu Photonics unveiled its latest fluorescence WSI scanner designed for high‑throughput cancer research, exemplifying Asia Pacific’s rapid progress in digital pathology innovation.

Europe Whole Slide Imaging Market Insights

The European continent is one of the vital regions in the Whole Slide Imaging (WSI) market because of the presence of efficient healthcare systems, high use of digital pathology, and favorable regulatory policies. The WSI market is expected to grow from 2026 to 2035 owing to rising cases of cancers and advanced diagnostic needs. The German nation is considered the leader among other nations in Europe since it generates massive amounts of revenue in the market.

Supporting this position, the European Commission’s Horizon Europe program has allocated substantial funding toward digital pathology, AI‑enhanced imaging, and advanced diagnostic platforms, reinforcing the EU’s commitment to next‑generation healthcare technologies.

In addition, the EU Medical Device Regulation (MDR 2017/745), fully implemented in 2021, has elevated quality and safety standards for digital pathology systems, strengthening trust in certified WSI technologies and accelerating adoption across Europe.

Middle East & Africa and Latin America Whole Slide Imaging Market Insights

The Middle East and Africa (MEA) and Latin America regions have been witnessing consistent market growth for Whole Slide Imaging (WSI). Factors such as increased investment in health care, development of health care infrastructure, and enhanced awareness about the advantages of digital pathology are some of the reasons behind this market growth in these regions. Within the MEA region, UAE, Saudi Arabia, and South Africa have been the most prominent countries using WSI systems, owing to their national visions that include health care modernization, such as the vision 2030 of Saudi Arabia and the National Agenda of UAE.

Supporting this development, Saudi Arabia’s Ministry of Health has launched nationwide digital pathology initiatives as part of the Kingdom’s health sector transformation agenda, including procurement of advanced Whole Slide Imaging systems to modernize hospitals and strengthen cancer diagnostics.

In Latin America, the national health authority ANVISA (Agência Nacional de Vigilância Sanitária) in Brazil has streamlined regulatory approvals for innovative diagnostic technologies, reducing time‑to‑market for WSI platforms and facilitating broader adoption across the country’s extensive public and private healthcare networks.

Whole Slide Imaging Market Growth Drivers:

-

Rising demand for faster, more accurate, and remote diagnostic capabilities is driving global adoption of Whole Slide Imaging (WSI).

The structural change in the field of pathology where the use of glass slides has transitioned to digital technology is one of the strongest factors behind the development of the WSI market. The demand for systems that can facilitate high-resolution image scanning, AI-assisted diagnosis, and telepathology collaboration has grown. Consequently, health care organizations have begun making investments in WSI systems for improved accuracy, faster processing, expert consultation opportunities, and differentiation.

Supporting this growth, the U.S. Agency for Healthcare Research and Quality (AHRQ), through its Healthcare Cost and Utilization Project (HCUP) databases, has documented a long‑term trend of rising Whole Slide Imaging utilization across both inpatient and outpatient diagnostic settings, with digital pathology now increasingly replacing traditional glass slide workflows nationwide.

The World Health Organization (WHO) emphasizes that non‑communicable diseases such as cancer, cardiovascular disease, diabetes, and chronic respiratory illness collectively account for nearly 74% of global deaths annually, underscoring the massive and growing diagnostic demand that WSI technologies are uniquely positioned to address through enhanced accuracy, scalability, and remote collaboration.

Whole Slide Imaging Market Restraints:

-

High capital investment requirements for advanced Whole Slide Imaging (WSI) scanners and digital pathology infrastructure are creating adoption barriers, particularly for smaller healthcare facilities and institutions in emerging economies.

The financial difficulties related to the purchase, installation, and maintenance of WSI systems constitute one of the main constraints limiting market expansion, particularly within community hospitals and regional laboratories. The advanced scanning technology of vendors like Philips, Leica Biosystems, and Hamamatsu Photonics is costly to acquire and maintain due to software licensing fees, cloud storage costs, AI capabilities, and yearly service agreements. Moreover, such advanced equipment demands a specific technical setup, including high-capacity servers, dedicated IT infrastructure, and data security.

Whole Slide Imaging Market Opportunities:

-

Accelerating development of compact, cost‑effective Whole Slide Imaging (WSI) scanners and AI‑enabled digital pathology platforms is creating new growth pathways for market expansion into community hospitals, regional labs, and emerging healthcare systems.

Opportunities for WSI growth lie ahead as technology shrinks and becomes more affordable, as well as more intelligent and automated. Firms are working on scanners that will be smaller and less expensive so that they may better serve mid-sized institutions. This new development promises to open the door for the use of WSI in a much larger segment of healthcare that has been previously under-serviced. With the use of cloud-based telepathology and AI image analysis programs, WSI usage has expanded past academic settings.

Recent Developments:

-

2026: Philips advanced its IntelliSite Pathology Solution with expanded AI integration through partnerships with Ibex Medical Analytics, enhancing cancer detection accuracy and workflow efficiency. The company also reported growing adoption across major U.S. and European hospital networks, supported by interoperability with DICOM standards for seamless integration into digital health ecosystems.

-

2025: Leica Biosystems launched the Aperio GT Elite scanner in North America and Europe, delivering ultra‑fast scanning speeds and AI‑driven quality control features. The platform was adopted by leading cancer research institutes, reinforcing Leica’s position as a global leader in digital pathology innovation.

-

2025: Roche expanded its NAVIFY Digital Pathology portfolio, integrating advanced AI algorithms for breast and lung cancer diagnostics. The company strengthened collaborations with academic medical centers in Germany and the U.S., supporting precision oncology initiatives and accelerating the clinical adoption of WSI technologies.

-

2025: 3DHISTECH introduced the PANNORAMIC 1000 scanner, capable of processing up to 1,000 slides per day, targeting high‑volume pathology labs and research centers. The company also expanded its footprint in Asia Pacific, with installations in China and Japan, underscoring its role in scaling digital pathology solutions for large healthcare systems.

Whole Slide Imaging Market Key Players:

-

Leica Biosystems

-

3DHISTECH

-

Hamamatsu Photonics

-

Ventana Medical Systems

-

Olympus Corporation

-

Fujifilm Holdings

-

Siemens Healthineers

-

GE Healthcare

-

Agfa-Gevaert N.V.

-

Hologic Inc.

-

Digirad Corporation

-

Gamma Medica Inc.

-

Positron Corporation

-

CardiArc Ltd.

-

Indica Labs

-

Sectra AB

-

Inspirata Inc.

Whole Slide Imaging Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.31 Billion |

| Market Size by 2035 | USD 2.49 Billion |

| CAGR | CAGR of 6.71% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Scanner Type (Brightfield Imaging, Fluorescence Imaging, Others), • By Technology (Scanners, IT Infrastructure, Image Management Systems, Viewing Software, Others), • By Application (Telepathology, Immunohistochemistry, Cytopathology, Hematopathology, Others), • By End User (Hospitals & Clinical Labs, Pharmaceutical & Biotech Companies, Academic & Research Institutes, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Philips, Leica Biosystems, Roche, 3DHISTECH, Hamamatsu Photonics, PerkinElmer, Ventana Medical Systems, Olympus Corporation, Fujifilm Holdings, Siemens Healthineers, GE Healthcare, Agfa-Gevaert N.V., Hologic Inc., Digirad Corporation, Gamma Medica Inc., Positron Corporation, CardiArc Ltd., Indica Labs, Sectra AB, , Inspirata Inc. |

Frequently Asked Questions

North America dominated the Whole Slide Imaging Market in 2025.

The Brightfield Imaging segment dominated the Whole Slide Imaging Market in 2025.

The major growth factor is the rapid adoption of digital pathology solutions powered by advanced scanners, IT infrastructure, and AI-driven image analysis.

The Whole Slide Imaging Market was valued at USD 1.31 billion in 2025.

The Whole Slide Imaging Market is expected to grow at a CAGR of 6.71% from 2026 to 2035.

Get in Touch