Rubber Compound Market Report Scope and Overview:

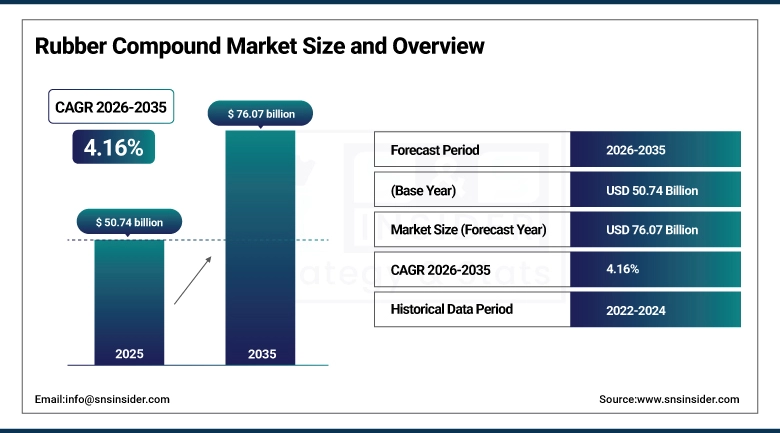

The Rubber Compound Market was valued at USD 50.74 billion in 2025 and is expected to reach USD 76.07 billion by 2035, growing at a CAGR of 4.16% from 2026-2035.

The Rubber Compounds Market is experiencing robust growth due to the rise in demand from various application industries like the automobile industry, construction sector, and manufacturing of industrial machinery. Rubber compounds are produced through the mixing of base rubber, either natural or synthetic, with other ingredients like vulcanizing agents, fillers, plasticizers, and antioxidants to act as basic raw materials for several products like seals, gaskets, hoses, tires, vibration dampening equipment, and protective paints. This market is affected by the increasing pace of industrialization in the Asia-Pacific region, rise in vehicle manufacturing, and investments made in infrastructural projects.

Increasing demand for rubber compounds that can withstand adverse environmental conditions of high temperatures, harsh chemicals, and extreme pressure is fueling research and development activities in silicone compounds, fluoroelastomer compounds, and ethylene propylene diene monomer (EPDM) compounds. Companies are developing innovative rubber compounds that cater to the specific needs of the electric vehicle transmission system, health care devices, and green buildings.

Market Size and Forecast

-

Market Size in 2025: USD 50.74 Billion

-

Market Size by 2035: USD 76.07 Billion

-

CAGR: 4.16% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Rubber Compound Market - Request Free Sample Report

Rubber Compound Market Trends

-

The rapid shift towards electric vehicle technology on a global scale is affecting the direction of focus when considering compound formulation in terms of the unique characteristics required by an EV powertrain system architecture, which includes improved thermal stability, electrical insulating capabilities, and the ability to resist corrosive attack from battery cooling fluids.

-

The demand for rubber compound formulations in liquid form is increasing at a greater rate than that for solid or powder versions, due to the increased applicability of such formulations for use in sealant, adhesives, and coating products for use in construction, electronics, and medical devices industries.

-

The use of silicone rubber compound formulations is increasing in applications where biocompatibility, wide temperature ranges of operation from -60 degrees Celsius up to 230 degrees Celsius, and protection from ozone and ultraviolet exposure make it preferable over general-purpose rubber compound formulations.

-

Sustainability-based compound formulation strategies, including the use of biodegradable processing oils, devulcanization techniques to reuse reclaimed rubber, and low-hazard additive formulas, have emerged in response to new environmental regulations regarding rubber compound manufacturing processes and the fate of end-of-use materials in Europe and North America.

-

Asia Pacific manufacturers, particularly in China, India, and South Korea, are investing in compounding capacity expansion and formulation capability development to serve both domestic demand growth and export markets, with regional compounders increasingly competing on technical compound quality alongside traditional cost-per-kilogram value propositions in automotive and industrial segments.

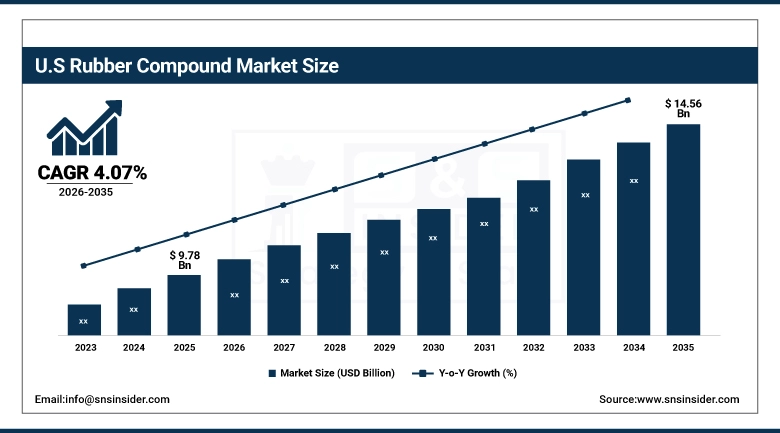

U.S. Rubber Compound Market was valued at USD 9.78 billion in 2025 and is expected to reach USD 14.56 billion by 2035, growing at a CAGR of 4.07%.

The US Rubber Compound Market has established dominance in the North American continent based on strong downstream manufacturing capacity for automobile components, aircraft parts, construction materials, and industrial machinery in the country, which ensures continuous usage levels for rubber compounds. The domestic demand for compounds is driven by a dynamic vehicle manufacturing industry, infrastructure modernization projects, and a developing segment of manufacturers for industrial equipment in the Midwest and Southeast industrial belts of the United States. U.S. compound producers cater to captive production needs for fully integrated manufacturers as well as converters supplying molded, extruded, and calendered rubber products to various application segments.

The rising demand for specialty compounds, like EPDM compounds for use in weather stripping and roofing sheets, silicone compounds for medical and food packaging uses, and fluoropolymer compounds in aerospace and chemical process equipment sealing applications, has added to the value of domestic compound purchases vis-à-vis regular commodity compound usage in terms of volume. Automotive components suppliers have been shifting to domestic production lines, thus driving up the local demand for automotive grade rubber compounds as well.

Rubber Compound Market Segment Analysis

-

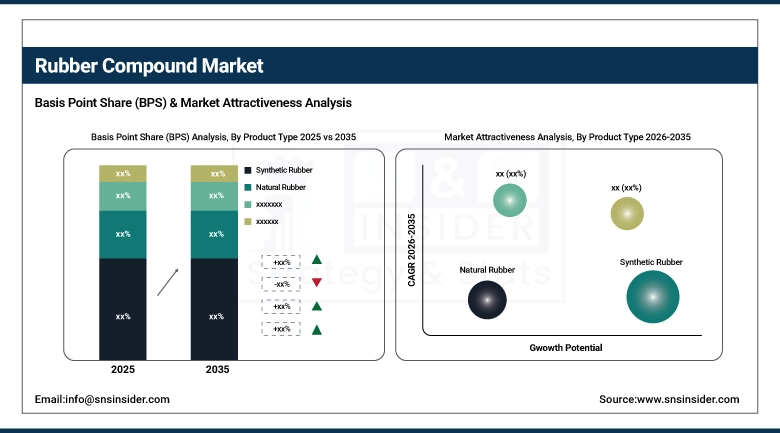

By Product Type, Synthetic Rubber dominated with ~71.80% share in 2025; Synthetic Rubber is also the fastest-growing product type segment.

-

By Product Form, Solid Rubber dominated with ~63.40% share in 2025; Liquid Rubber is the fastest-growing product form segment with a CAGR of 6.40%.

-

By Rubber Type, Silicone Rubber dominated with ~31.60% share in 2025; Silicone Rubber is also the fastest-growing rubber type with a CAGR of 6.50%.

-

By End-User, Automotive & Transportation dominated with ~46.30% share in 2025; Automotive & Transportation is also the fastest-growing end-user segment with a CAGR of 5.90%.

By Product Type: Synthetic Rubber dominates, Natural Rubber maintaining stable demand

Synthetic Rubber accounted for around 71.80% market share of the Rubber Compound Market with revenues reaching approximately USD 36.43 billion in 2025. The strong preference for synthetic rubbers in applications such as automotive, industrial, and construction due to the critical importance of the consistent nature of the raw material quality, tailored engineering for performance properties, and reliability in procurement are expected to drive market growth over the forecast period. Synthetic rubber varieties including SBR, NBR, EPDM, silicone, and fluoroelastomers possess superior performance capabilities to natural rubbers in extreme temperatures, chemical resistance, and weathering. Synthetic rubber compound formulation standards have become more common in the design specifications of automotive OEM applications, while EV platform development is boosting demands in powertrain sealing and insulation.

Natural Rubber will continue to secure a steady demand base in tire manufacture, heavy duty conveyor belt compound, and vibration isolation because of natural rubber's unmatched durability and tensile strength and tear resistance qualities. Factors associated with the supply of natural rubber including plantation-based production in countries like Thailand, Indonesia, and Malaysia which provide the bulk of worldwide natural rubber supplies are contributing to price fluctuations that result in substitute pressures for synthetic rubber compounds.

By Product Form: Solid Rubber dominates, Liquid Rubber fastest growing

The share of Solid Rubber in the global Rubber Compound market was around 63.41% in 2025 because it has been widely used as the leading compound form in manufacturing processes such as compression molding, injection molding, extrusion, and calendering for rubber products made for use in the automotive industry, building, and other industries. The capability of solid compounds to be processable using ordinary rubber manufacturing machines, flexibility in their formulations, and established infrastructure in manufacturers of the compounds contribute to their domination by volume in both commodity and specialty compounds. Use of solid EPDM, NBR, and silicone rubber compounds for seals, hoses, and vibration dampening in the automotive industry constitutes the largest volume application among all applications of solid rubber compounds.

Liquid Rubber emerged as the fastest-growing segment in terms of product form, growing at a CAGR of 6.40%. Liquid rubber compounds have been increasingly adopted for applications in glazing sealants, protective coatings, potting compounds for electrical components, and liquid silicone injection molding. The ease of shaping complex geometry parts with liquid rubber compounds and achieving full mold filling without high pressure make them preferable to solid compounds for some specific uses, especially in precision manufacturing operations.

By Rubber Type: Silicone Rubber dominates specialty segment, EPDM strong in weathering applications

The share of Silicone Rubber in the Rubber Compound market stood at 31.60% in 2025 and is expected to have a growth CAGR of 6.50% in comparison to other rubbers. Silicone rubbers compounds provide unique functionality such as thermal tolerance from low temperatures to high temperatures, chemically resistant, biocompatible, electrical insulation properties, and resistance to ozone, UV, and moisture, which make them essential ingredients in medical devices, food processing equipment, aerospace materials, and insulation of high voltage electricity. The increased use of LSR injection process, demand for medical-grade silicone compounds, and the requirement for silicone-based compounds in automotive high-temperature seals drive the growth in the silicone compound market.

Among other rubbers, EPDM rubbers hold the position of the second largest compound used in the manufacturing of building envelopes. They are used for applications like roofing membranes, automotive weather stripping, windows sealing, and HVAC equipment. Because of their great tolerance of heat, sunlight, and UV radiation, they are preferred compounds for construction activities that involve sealing roofs, windows, and weatherproofing infrastructures as well as automotive OEMs for door seals and glass encapsulations.

By End-User: Automotive dominates, Building & Construction second largest

Segment-wise analysis indicates that the Automotive & Transportation application accounted for the largest market share of nearly 46.30% of the total rubber compounds market share in 2025. This segment is also estimated to register a faster growth rate than any other end-use segment of around 5.90%. The use of rubber compounds is seen in various functional aspects of vehicles such as door seals, under-hood hoses and coolants, vibration isolation mounts and bushes, fuel system components, and brake systems. The shift towards electric platform technology has increased the demand for rubber compounds to meet specific application requirements for EVs, such as battery thermal management system seals, high-voltage insulation compound cables, and seals for charging interfaces which was not necessary in conventional ICE vehicles.

Building & Construction application emerged as the second-largest end-user category after automotive applications due to constant demand for rubber compounds from commercial roofing membranes, architectural glazing seals, pipe joints, and expansion joints. Commercial roofing membrane applications and silicone architectural glazing compounds emerged as valuable products within construction compound consumption and are associated with commercial constructions, green buildings' refurbishments, and maintenance of infrastructures which creates sustained demand irrespective of changes in construction activity levels.

Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

81% |

|

Europe |

Germany |

27% |

|

Asia Pacific |

China |

46% |

|

Middle East & Africa |

Saudi Arabia |

31% |

|

Latin America |

Brazil |

51% |

North America Rubber Compound Market Insights

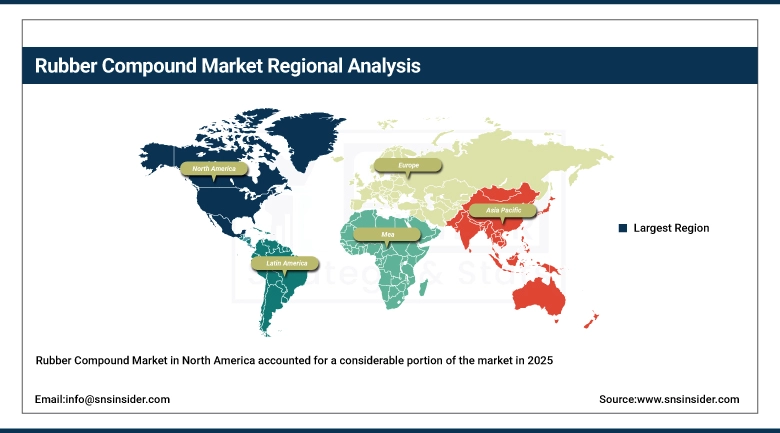

The Rubber Compound Market in North America accounted for a considerable portion of the market in 2025, registering a CAGR of 4.50%. The primary driving force behind the demand for compounds in the region is the significant presence of an automotive industry based on the Great Lakes and southeastern parts of the country. Other sectors that contribute to compound consumption in the region include commercial building construction and a highly advanced manufacturing sector for industrial machinery and aircraft components. In North America, compound manufacturers like Lanxess, ExxonMobil Chemical, and Shin-Etsu Silicones supply compound material directly to OEMs and also indirectly through distributors to converters.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Rubber Compound Market Insights

APAC is currently the biggest and fastest-growing regional market for Rubber Compounds, which is set to register a CAGR of 6.80% up to 2035 – the highest growth of any region. The biggest national market for Rubbers Compound is that of China, buoyed by the largest vehicle production in the world, the presence of strong industrial manufacturing capabilities, and construction on a significant scale to maintain its compounded demand despite any economic cycles worldwide. As far as national markets go, APAC's second-largest market is India, spurred on by fast vehicle production expansion and infrastructural developments as per the country's national development programs.

Southeast Asian compounding markets, especially in Thailand, Indonesia, and Malaysia, have a clear advantage in having access to sources of natural rubber feedstock and facilities for compound production geared towards both internal consumption and exports. Infrastructure development by Southeast Asian governments in rail transport, highways, ports, and intra-city transit networks is creating pipeline opportunities for demand in construction sealants and rubber products for civil engineering applications that will run for several years into the future. Proximity to the natural rubber production centers in the Asia Pacific region confers a significant raw material cost advantage for compounders.

Europe Rubber Compound Market Insights

Europe Rubber Compound Market experiencing a CAGR growth of 4.20%, with Germany, France, UK, and Italy being the primary national markets. The dominant position held by Germany as Europe's largest automotive production economy provides continuous demand for automobile-grade EPDM, NBR, silicone, and fluoroelastomer compound products due to its extensive network of tier one and tier two suppliers for the automobile industry. European rubber compound suppliers are under regulatory pressure owing to regulations under the REACH act on some of the accelerator and plasticizer used in their compound products, which leads to investment in the reformulation of the compounds. The EU green deal, and the circular economy action plan has led to sustainable compound development through investments in bio-process oils and reclaim rubber.

Latin America Rubber Compound Market Insights

Latin America Rubber Compound Market with CAGR Expected to grow at a Rate of 4.90%, led mainly by Brazil, Mexico, and Argentina. Brazil stands out as the largest market for rubber compounds in Latin America due to its strong automotive manufacturing industry, robust infrastructure development projects, and active industrial equipment manufacturing industry that drives steady compound purchase rates. Increasing presence of auto assembly and component manufacturers in Mexico, especially as part of the USMCA integrated supply chain for North American OEM products, is driving rising demand for rubber compounds from the automotive components manufacturers. Growth in construction compound purchases in Colombia, Peru, and Chile is being witnessed due to investments in road and urban transport infrastructure projects.

Middle East & Africa Rubber Compound Market Insights

Middle East & Africa Rubber Compound Demand is influenced by spending on infrastructure development in GCC nations, South Africa, and other important sub-Saharan African regions. Road construction, office building projects, and factory projects have led to consistent demand for rubber sealants and building compounds in such nations. There is regional compound demand generated from vehicle assembly facilities located in South Africa, Morocco, and Egypt. Investment in synthetic rubber monomers in GCC countries has increased compound manufacturing investments in the United Arab Emirates and Saudi Arabia.

Market Growth Drivers: Sustained automotive production volumes and accelerating electric vehicle platform adoption driving compound demand expansion

The use of rubber compounds in automobiles is the highest contributor to end-user demand within the compound market, with automobile production figures from Asia Pacific, North America, and Europe ensuring that there will be continuous demand for compounds for sealing, vibration dampening, fluid transfer, and heat dissipation needs. The shift towards electric vehicle models has created additional demand for compounds through the introduction of seals for battery systems, heat dissipation compounds, and insulation requirements for electrical components, thereby helping somewhat mitigate demand losses due to elimination of ICE-specific needs. Expected vehicle production levels in the global market have been kept at around 90-95 million units annually until 2030.

Market Restraints: Raw material price volatility and synthetic rubber feedstock dependency on petroleum market conditions constraining margin stability

Rubber compound producers find themselves highly vulnerable to input costs for both commodity rubber and petrochemical feedstocks such as butadiene, isoprene, ethylene, and propylene used in their synthetic rubber products. Commodity natural rubber prices are prone to supply fluctuations related to weather conditions and diseased crops in Southeast Asian plantations, as well as volatile speculation which makes the purchasing environment unpredictable for compound producers and prevents passing increased costs on to their customers due to short-term contracts. Costs for synthetic rubber input feedstocks follow the price movements in oil markets and in petrochemical manufacturing, putting pressure on rubber compound margins at times of rising energy prices.

Market Opportunities: Electric vehicle component specification growth and sustainable compound formulation development creating new market opportunities

Electric vehicle powertrains generate a need for new rubber compound developments in applications for battery thermal management systems, high voltage cables, and charging port sealants, offering compound development opportunities not available in previous generation vehicle programs. Compound producers that have successfully qualified their materials according to EV OEM and battery maker specifications are entering into premium pricing sourcing programs with long-term supply contracts for revenues beyond the basic compound business. Sustainable formulation advances incorporating bio-based oils as plasticizers, devulcanized reclaim rubber use, and low-VOC vulcanizing systems will enable compounders to satisfy the increasing demands from EV OEMs and contractors for sustainable sourced materials at different prices than traditional compound formulations in Europe and North America.

Recent Developments:

-

2025: Lanxess AG introduced the Levapren EVM compounds range, developed for use in EV battery module sealing applications, designed to provide reliable compression set properties under -40°C to 175°C temperature cycling conditions found in thermal management systems of battery packs, and received qualification from three European EV OEM battery assembly manufacturers within one year after its market introduction.

-

2025: Shin-Etsu Chemical increased production capacity of liquid silicone rubber compounding materials at its plant in Naoetsu, Japan, by 15,000 metric tons per annum to meet increasing demand from medical devices and LSR injection molding industries in Asia Pacific and North America, and utilized the additional capacity for production of healthcare, automotive high-temperature sealing, and electronics potting compounds ranges.

Rubber Compound Market Key Players

-

Lanxess AG

-

ExxonMobil Chemical Company

-

Shin-Etsu Chemical Co., Ltd.

-

Dow Inc.

-

Momentive Performance Materials Inc.

-

Trelleborg AB

-

Zeon Corporation

-

Arlanxeo (Saudi Aramco / LANXESS JV)

-

Mitsui Chemicals, Inc.

-

TSRC Corporation

-

Kumho Petrochemical Co., Ltd.

-

JSR Corporation

-

Denka Company Limited

-

Versalis S.p.A. (Eni Group)

-

Kraiburg TPE GmbH & Co. KG

-

Robinson Rubber Products Company

-

Elkem ASA

-

Nok Corporation

Rubber Compound Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 51.35 Billion |

| Market Size by 2035 | USD 110.56 Billion |

| CAGR | CAGR of 8.01% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Synthetic Rubber, Natural Rubber) • By Product Form (Solid Rubber, Liquid Rubber, Powdered Rubber) • By Rubber Type (Silicone Rubber, Fluoro Rubber, Butyronitrile Rubber, EPDM Rubber, Others) • By End-User (Automotive & Transportation, Building & Construction, Industrial Machinery & Equipment, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Lanxess AG, ExxonMobil Chemical Company, Shin-Etsu Chemical Co. Ltd., Wacker Chemie AG, Dow Inc., Momentive Performance Materials Inc., Trelleborg AB, Zeon Corporation, Arlanxeo, Mitsui Chemicals Inc., TSRC Corporation, Kumho Petrochemical Co. Ltd., JSR Corporation, Denka Company Limited, Versalis S.p.A., Kraiburg TPE GmbH & Co. KG, Hexpol AB, Robinson Rubber Products Company, Elkem ASA, Nok Corporation. |

Frequently Asked Questions

Automotive & Transportation dominated with approximately 46.30% share in 2025.

Asia Pacific is expected to grow at the fastest CAGR of 6.80% in the Rubber Compound Market.

Synthetic Rubber dominated with approximately 71.80% share in 2025.

The Rubber Compound Market was valued at USD 50.74 Billion in 2025.

The Rubber Compound Market is expected to grow at a CAGR of 4.16% from 2026 to 2035.

Get in Touch