Semiconductor Equipment Market Report Scope & Overview:

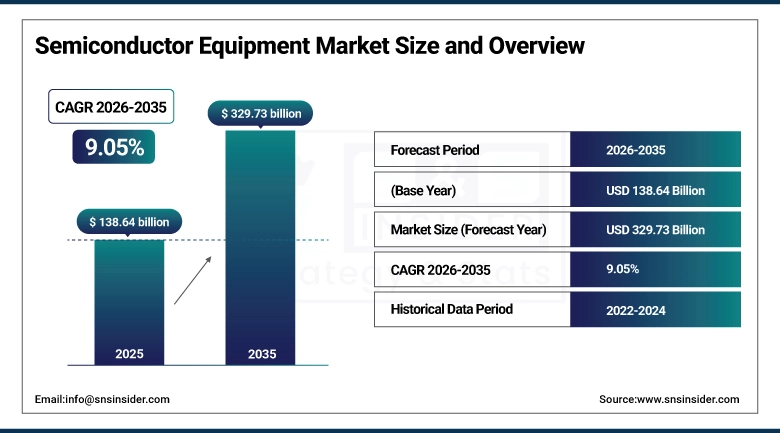

The Semiconductor Equipment Market Size was valued at USD 138.64 Billion in 2025 and is projected to reach USD 329.73 Billion by 2035, growing at a CAGR of 9.05% during 2026–2035.

Semiconductor Equipment Market has observed a high growth in demand for these advanced chips and is mainly used in consumer electronic, automotive and telecommunications activities. The surge in demand for AI, 5G, IoT, and high-performance computing is contributing to the need for advanced fabrication technologies. Furthermore, a trend towards smaller node sizes and complex chip architectures is raising the need for advanced equipment. The global market is also gaining from government investments for setting up new semiconductor manufacturing facilities, with new foundries following up, and an increased emphasis on maintaining supply chain resilience.

Semiconductor Equipment Market Size and Growth Forecast:

-

Market Size in 2025: USD 138.64 Billion

-

Market Size by 2035: USD 329.73 Billion

-

CAGR: 9.05% during 2026–2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Semiconductor Equipment Market - Request Free Sample Report

Semiconductor Equipment Market Key Trends:

-

There is a growing demand for advanced semiconductor chips across industries; hence, there is a higher demand for semiconductor manufacturing equipment globally.

-

A growing trend toward miniaturization and advanced node technologies is increasing the adoption of cutting-edge fabrication equipment in the long term.

-

A growing number of innovations in AI, IoT, and 5G technologies is improving the complexity of chip manufacturing, thereby driving demand for advanced equipment.

-

Technological advancements in lithography, etching, and deposition processes are improving the efficiency and precision of semiconductor equipment.

-

A growing number of semiconductor fabrication plants and foundry expansions is improving the demand for semiconductor equipment.

-

A growing number of strategic collaborations between chip manufacturers and equipment providers is improving innovation and accelerating production capabilities.

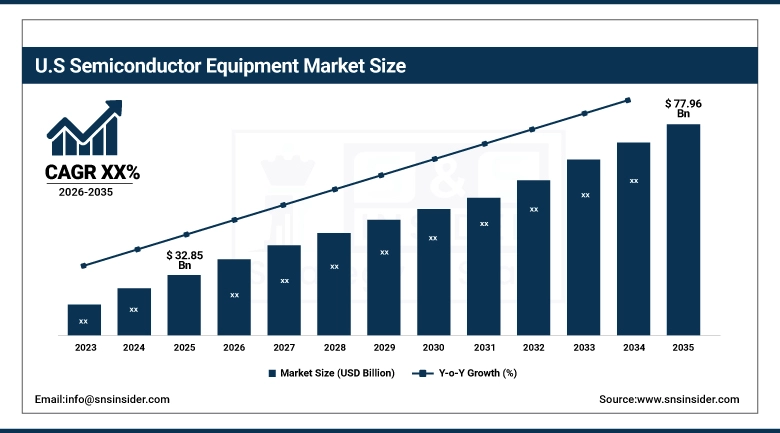

U.S. Semiconductor Equipment Market Size Outlook:

The U.S. Semiconductor Equipment Market size was valued at approximately USD 32.85 Billion in 2025 and is projected to reach USD 77.96 Billion by 2035. Growth in the U.S. Semiconductor Equipment Market is driven by strong government support, rising investments in domestic chip manufacturing, increasing demand for advanced semiconductors, rapid adoption of AI and 5G technologies, and expansion of leading semiconductor foundries and fabrication facilities.

Semiconductor Equipment Market Key Drivers:

-

Rising demand for advanced semiconductor chips and increasing investments in fabrication facilities.

Massive semiconductor demand growth across consumer electronics, automotive and telecommunications, are the main drivers of the Semiconductor Equipment Market. There is an individual expansion requirement for new-age chip manufacturing gear largely powered by using the multiplication of AI, IoT, and 5G technologies. The investment in new fabs, the expansion of foundries, and local government or supply chain initiatives to build domestic semiconductor production capacity are also leading to market growth.

Semiconductor Equipment Market Key Restraints:

-

High capital investment and supply chain complexities are some of the restraints for market growth.

The cost of semiconductor manufacturing equipment is very high, so it is a big barrier to entry for new comers. Moreover, supply chain issues and reliance on specific parts can affect how quickly things are produced. High skilled labor requirement and complexity of advanced manufacturing processes further limits market growth. Meeting these challenges is necessary for the market to continue to grow steadily.

Semiconductor Equipment Market Key Opportunities:

-

Growing adoption of advanced node technologies and expansion of semiconductor manufacturing offer significant growth opportunities.

Emergence of new markets due to semiconductor fabrication technologies like EUV lithography, 3D chip architectures, etc. The global semiconductor market also has substantial growth opportunities due to the rise of multi-national investments in local chip development across the world as well as the increases in demand for cutting-edge chips in emerging industries. In addition, growing demand for AI, electric vehicles and HPC will provide, fertile opportunities for the players operating in the market.

Semiconductor Equipment Market Segments:

-

By Component Type: In 2025, Wafer Fabrication Equipment dominated with 48% share; Testing Equipment fastest growing segment during 2026–2035

-

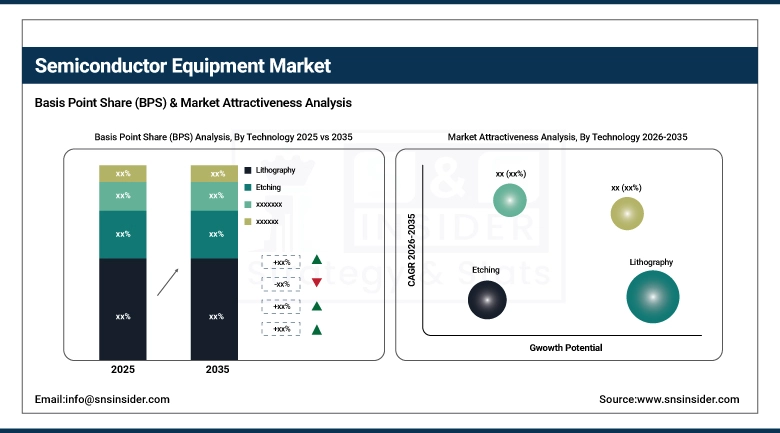

By Technology: In 2025, Lithography dominated with 36% share; Inspection & Metrology fastest growing segment during 2026–2035

-

By Application: In 2025, Foundry dominated with 40% share; Memory fastest growing segment during 2026–2035

-

By End User: In 2025, Integrated Device Manufacturers (IDMs) dominated with 46% share; Foundries fastest growing segment during 2026–2035

By Component Type, Wafer Fabrication Equipment Dominates While Testing Equipment Grows Rapidly:

In terms of technology, Wafer Fabrication Equipment held the largest market share since it is used in several front-end semiconductor manufacturing processes such as lithography, deposition, and etching. This segment contributed prominent revenue in 2025, owing to an increase in demand for advanced node chips and the rise of fabrication facilities worldwide.

Testing Equipment is the fastest-growing type in the market as from the increasing requirement of the high performance and stable semiconductor systems. As the complexity in chip designs is rising and factories are dependent on quality assurance, this part is driving a growth in this segment.

By Technology, Lithography Dominates While Inspection & Metrology Witness Fastest Growth:

Segmental coverage of the report based on type of product scope shows Lithography segment outperformed the market owing to its leading position in patterning of circuits on a semiconductor wafer. This segment accounted for considerable demand in 2025 propelled by the development of extreme ultraviolet (EUV) lithography technologies.

The Inspection and Metrology segment is projected to have the fastest growth due to growing needs for accuracy and defect identification in next-generation semiconductor manufacturing. The increasing complexity of chip designs is also driving up the need for these technologies.

By Application, Foundry Segment Dominates While Memory Segment Records Fastest Growth:

Market dominance of the foundry segment attributed to outsourcing of semiconductor manufacturing and the leading foundries expansion across the globe. That segment brought in sizable revenue in 2025 owing to its high-volume chip manufacturing.

The Memory segment achieved the largest growth rate owing to growing data storage demand supported by cloud computing, AI, and data center. This segment is being fueled by the increasing requirement for high-speed and high-capacity memory devices.

By End User, Integrated Device Manufacturers (IDMs) Dominate While Foundries Record Fastest Growth:

The IDMs Segment Held the Largest Share of the Semiconductor Packaging Market. The segment featured a notable share in 2025, powered by constant supply and innovation production.

The fastest growing segment is the Foundries, which is driven by the increasing demand for outsourced semiconductor manufacturing services. Demand for foundry services is increasing due to new fabless companies that have emerged on the scene in recent years, and the increasing complexity of producing chips.

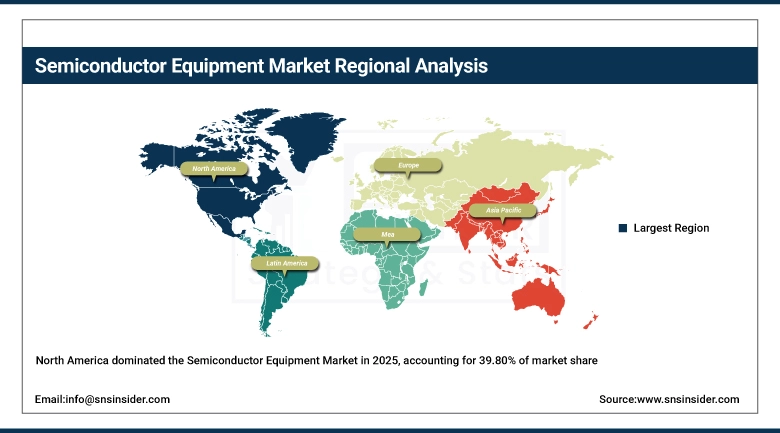

Semiconductor Equipment Market Regional Analysis:

North America Semiconductor Equipment Market Insights:

North America region holds a significant share of 39.80% of North America Semiconductor Equipment Market in 2025. This is because well-known semiconductor manufacturers and equipment vendors in the U.S. and Canada. The high investment in advanced chip technologies and support by the government for domestic production of semiconductors and capabilities in R&D all boost up the growth of the market. The high demand for AI, 5g, and high-performance computing is also fueling the market across this region.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia-Pacific Semiconductor Equipment Market Insights:

Region-wise, the Asia-Pacific Semiconductor Equipment Market is the fastest-growing region, and, the fastest-growing region, which is expected to garner a CAGR Between 2026 and 2035 is 10.20%. Semiconductor manufacturing activities in the region including China, Taiwan, Korea, Japan, and India are driving growth into this region. The growing demand for consumer electronics, a large number of foundry players, and increasing investments in fabrication plants are driving the growth of the Asia-Pacific market.

Europe Semiconductor Equipment Market Insights:

Factors such as investment in semiconductor manufacturing, high demand in automotive and industrial sectors, etc. are the basis for the growth of the Europe Semiconductor Equipment Market. From the geographical perspective, the European market is driven by countries, including Germany, France, and the UK, as the rising adoption of semiconductor technologies for electric vehicles, industrial automation, and smart manufacturing are supporting the market growth in this region. Furthermore, government in this region is taking supportive initiatives to fuel the market growth by funding in research & development activities.

Latin America Semiconductor Equipment Market Insights:

Growing digitalization, expansion in electronics manufacturing are some of the factors which are contributing to the growth of Latin America Semiconductor Equipment Market. This is complemented by increasing spending on technology infrastructure and high demand for consumer electronics, especially across nations such as Brazil and Mexico. Apart from this, growing regional players in the market are also benefitting the market by improvement in industrial abilities.

Middle East & Africa (MEA) Semiconductor Equipment Market Insights:

Growth in the Middle East & Africa Semiconductor Equipment Market is primarily driven by increasing technology infrastructure investments, as well as the adoption of digital technologies. Furthermore, participants in the market are benefitting from rising incorporation of electronics and promising setup of smart city projects proliferating in nations such as UAE, Saudi Arabia, and South Africa. In addition, higher government avenues towards diversification and technology development is helping to drive the semiconductor equipment market in the region.

Semiconductor Equipment Market Competitive Landscape:

ASML is a dominant player in semiconductor equipment focusing on high-end lithography systems used for chip making. You will not only get exposure to your daily grocery items and food, but also a critical supply chain company that you may not think of too often — semiconductor – production company with its extreme ultraviolet ((EUV) lithography technology enabling next-generation semiconductor production. That revolves around nonstop innovation, high-precision manufacturing, as well as deep partnerships with the biggest semiconductor makers.

-

In October 2025, ASML expanded its EUV lithography system capabilities to support advanced node semiconductor manufacturing, enhancing chip performance and production efficiency.

Tokyo Electron is a key player in the semiconductor equipment market, offering a wide range of solutions including deposition, etching, and cleaning systems. The company supports semiconductor manufacturing across various stages of chip fabrication and serves major global foundries and integrated device manufacturers. Tokyo Electron focuses on technological innovation, process optimization, and strong customer partnerships to strengthen its market position.

-

In August 2025, Tokyo Electron introduced advanced etching and deposition equipment designed to improve precision and efficiency in next-generation semiconductor manufacturing processes.

Semiconductor Equipment Companies are:

-

ASML

-

Tokyo Electron

-

Applied Materials

-

KLA Corporation

-

SCREEN Holdings

-

Nikon

-

Canon

-

Advantest

-

Teradyne

-

ASM International

-

Veeco Instruments

-

Rudolph Technologies

-

Onto Innovation

-

CyberOptics Corporation

-

Kulicke & Soffa

-

MKS Instruments

-

Disco Corporation

-

Cohu Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 138.64 Billion |

| Market Size by 2035 | USD 329.73 Billion |

| CAGR | CAGR of 9.05 % From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component Type: (Wafer Fabrication Equipment, Assembly & Packaging Equipment, Testing Equipment) • By Technology: (Lithography, Etching, Deposition, Cleaning, Inspection & Metrology) • By Application: (Foundry, Memory, Logic, Discrete & Others) • By End User: (Integrated Device Manufacturers (IDMs), Foundries, Outsourced Semiconductor Assembly and Test (OSAT) Providers) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | ASML, Tokyo Electron, Lam Research, Applied Materials, KLA Corporation, SCREEN Holdings, Nikon, Canon, Hitachi High-Technologies, Advantest, Teradyne, ASMI (ASM International), Veeco Instruments, Rudolph Technologies, Onto Innovation, CyberOptics Corporation, Kulicke & Soffa, MKS Instruments, Disco Corporation, Cohu, Inc. |

Frequently Asked Questions

The Semiconductor Equipment Market is expected to grow at a CAGR of 9.05 % during 2026–2035.

The Semiconductor Equipment Market size was valued at USD 138.64 Billion in 2025 and is projected to reach USD 329.73 Billion by 2035.

The key drivers of the Semiconductor Equipment Market include increasing demand for advanced semiconductor chips, rising adoption of AI, IoT, and 5G technologies, growing investments in semiconductor fabrication plants.

The Wafer Fabrication Equipment segment dominated the Semiconductor Equipment Market during the projected period.

North America dominated the Semiconductor Equipment Market in 2025.

Get in Touch