Silicone Surfactants Market Report Scope & Overview

Get E-PDF Sample Report on Silicone Surfactants Market - Request Sample Report

The Silicone Surfactants Market size was valued at USD 1.9 Billion in 2023. It is expected to grow to USD 2.8 Billion by 2032 and grow at a CAGR of 4.5% over the forecast period of 2024-2032.

Silicone surfactants are essential components in the usability of household cleaners, a sector that is fast growing due to the increased consumer preference for cleaning agents that are more effective and efficient. The trend is generally explained by rising awareness on issues of hygiene and cleanliness, a move that has been necessitated by the challenges experienced across the globe on matters of health. The surfactants aid in proper utilization of household cleaning agents by wetting services, emulsification, and stabilization of foam. In the final cleaning products, frequent users have reported improved user experience due to the improved feel and texture.

According to a report from the U.S. Bureau of Labor Statistics, the home cleaning products market is projected to grow at an annual rate of 4.1% from upcoming year, highlighting the increasing demand for innovative cleaning solutions. This growth, coupled with the unique benefits offered by silicone surfactants, positions them as a vital component in the formulation of modern household cleaning products, thereby contributing to the overall expansion of the silicone surfactants market.

The increase in consumption of sustainable and eco-friendly products has significantly heightened interest in silicone surfactants, as they are generally more environmentally friendly than conventional surfactants. Currently, manufacturers are productizing different versions of biodegradable silicone surfactants to meet these increasing demands.

Moreover, in 2022 when Wacker Chemie AG introduced a biodegradable silicone surfactant range intended for use in personal care and household cleaning applications. The move ensured a reduction of the environmental footprint as they are highly efficient. This new product not only aligns with changing market needs but provides a harmonious way forward in the industry.

Silicone Surfactants Market Dynamics

Drivers

-

Growing demand for construction materials drive the market growth.

-

Raising demand for personal care products drives the market growth.

The global silicone surfactants market is majorly growing due to the rising demand for personal care products. With increasing concern about grooming and skincare, demand for personal care products like shampoos, conditioners, lotions, and cosmetics has soared. Silicone surfactants have proven to be exceptional ingredients that can address specific needs, such as superior conditioning, shine, and softening. Specifically, their distinctive spread ability, texture modification, and excellent humidity retention have enabled these surfactants to formulate luxuriously-feeling and high-performing products. Moreover, the inclination toward more premium and specialized personal care products has compelled manufacturers to seek effective and innovative materials that can deliver superior sensory performance for their intended applications. According to data from the U.S. Bureau of Labor Statistics, the consumer price index for personal care products increased by 2.9% from 2021 to 2022. This rise indicates growing consumer investment in personal care items, reflecting an increased focus on grooming and skincare.

Restraint

-

Harmful emissions released in manufacturing processes hamper the market growth.

-

Availability of alternatives of silicone surfactants hamper the market growth.

There are several alternatives to ethoxylated surfactants, such as alkyl polyglucosides and sorbitan esters. These alternatives have similar qualities to silicone surfactants, but they are frequently less expensive and more environmentally friendly. As a result, they are gaining popularity, placing pressure on the silicone surfactants industry. The emissions can include volatile organic compounds (VOCs), which are harmful to human health and the environment. They can also include greenhouse gases, which contribute to climate change.

Opportunities

-

Growing demand for sustainable products

-

Rising demand for surfactants from end-user

Silicone surfactants are used to improve the performance and longevity of water-based paints and coatings. They can aid in making the paint more water-resistant, easier to apply, and fade-resistant. also, they are found in a variety of textile care products, including softeners and antistatic agents. They can aid to make materials softer, smoother, and static cling. Other than that silicone surfactants find application in a variety of industrial applications, construction, agriculture, refrigerator, etc.

Moreover, silicone surfactants are broadly applied in textile care commodities, such as softeners and antistatic. Silicone surfactants make the textiles softer, smoother, and with less static. In addition, silicone surfactants are used in numerous industrial areas, such as building, where they provide better performance to sealants and adhesives, agriculture, where they better the formulation of pesticides for covering the larger territories and proper action, refrigeration, where they serve in the development of efficient cooling fluids.

Silicone Surfactants Market Segmentation Outlook

By Type

In 2023, the water-soluble category held the largest market share around 42% in 2023. The increasing use of the product in fertilizer formulations in the agricultural industry is expected to drive the expansion of water-soluble surfactants. Also, the oil-soluble sector is expected to develop at a steady rate. Because of its ability to improve viscosity, the oil-soluble type is becoming more prevalent in drilling fluids. The drilling fluid industry is heavily reliant on the oil soluble variety since it provides for high surface tension and stability.

By Application

In 2023, the emulsifiers category owned the market with a share of revenue of more than 31.0%. This is due to the growing usage of silicone surfactants in cosmetics, personal care, and home care products. The wetting agent segment is expected to grow significantly in the future. The agricultural business is heavily reliant on wetting agents because they allow water to spread evenly on the surface and penetrate more deeply.

Dispersants category is also growing and in high demand because they provide stability, UV protection, and coating strength. It aids in the improvement of fluid workability. Because of these characteristics, it is widely utilized in the paints and coatings market, which is expected to drive the market. Furthermore, the emulsifying and foaming capabilities of silicone surfactants have resulted in a global increase in demand for these surfactants.

By End-User

Personal care held the largest market share around 36% in 2023. The segment of personal care is the main market driver as customers become more interested in high quality grooming and skincare. The rising demand for cosmetics, shampoos, conditioners, lotions, and other beauty products has been observed as personal hygiene and grooming take on more importance in the average customers’ life. To meet the requirements of this market, silicone surfactants are greatly appreciated for the ability to make the product more efficient. Specifically, the enhancement of conditioning, moisture savings, and improved feel draws personal care customers looking for not only superior feeling but actual premiumization, i.e. high-quality products that are more efficient overall and are often on the more expensive side traced.

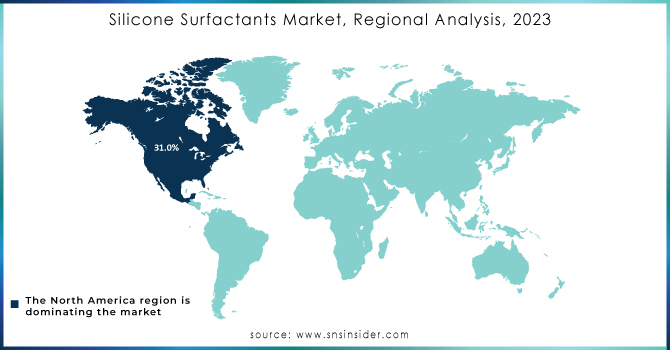

Silicone Surfactants Market Regional Analysis

The North American region led the market with a revenue share of nearly 31.0% in 2023. This increase can be attributed to the area's adoption of natural cosmetics, construction, and personal care goods, as well as increased R&D activities to develop distinctive personal care products. Furthermore, the existence of important end-use producers in the area is expected to improve product demand in the near term. North America's market is developing as a consequence of the existence of important players such as Key Performance Materials Inc., Elkem Silicones, and Shin-Etsu Chemical Co., Ltd.

According to the U.S. Environmental Protection Agency, 2022 report highlights that 30% of U.S. consumers actively seek environmentally friendly products, including personal care items. This trend aligns with the adoption of natural and sustainable ingredients, contributing to the growing demand for silicone surfactants that enhance product performance while meeting consumer preferences for eco-friendly solutions.

Asia Pacific is expected to increase at a CAGR of 4.5% during forecast period from 2024 to 2032. Furthermore, developing nations such as China, India, and Japan are boosting their need for silicone surfactants in cosmetics, textiles, construction, soap, and personal care goods, resulting in market expansion. China is one of the major Asian countries with a lot of construction going on, with the industrial use and construction industries accounting for roughly half of the GDP.

The European region is expected to increase significantly during the predicted period. This is due to increased demand for construction, household, toiletries, and other items, as Europe is an important region for the production of luxurious cosmetics and personal care products. The use of silicone surfactants in the region's paints and coatings sector is expected to drive market expansion.

Get Customized Report as Per Your Business Requirement - Request For Customized Report

Key Players in Silicone Surfactants Market

-

Momentive (Silicone Antifoam Agents)

-

DOW Inc. (DOWSIL 4200 Silicone Fluid)

-

Elkem Silicones (Silcolease)

-

Innospec (SILICONE 720)

-

Evonik Industries AG (TEGO Wet 270)

-

Andisil (Andisil 1200 Series)

-

Supreme Silicones (Supreme 1061)

-

Shin-Etsu Chemical Co., Ltd. (KEM-030)

-

Wacker Chemie AG (WACKER SILICONE EMULSION)

-

Siltech Corporation (Siltech 7400)

-

Kraton Corporation (Kraton G Series)

-

Huangshan Huasu New Material Science & Technology Co., Ltd. (Huasu Silicone Surfactants)

-

Wynca (Wynca Silicone Surfactants)

-

Mitsui Chemicals, Inc. (Mitsui Silicone Surfactants)

-

KCC Corporation (KCC Silicone Surfactants)

-

NuSil Technology (NuSil Silicone Gel)

-

Hubei Yihua Chemical Industry Co., Ltd. (Yihua Silicone Surfactants)

-

Dapeng Chemical (Dapeng Silicone Surfactants)

-

Zhejiang Yonghe Silicone Co., Ltd. (Yonghe Silicone Surfactants)

-

Trelleborg AB (Trelleborg Silicone Solutions)

Recent Development:

-

In 2023 Momentive Performance Materials, Inc. a global specialty solutions and high-performance silicones firm, has introduced HARMONIE, a cutting-edge line of high-performance derived natural and natural ingredients for the beauty and personal care industries.

-

In 2023 Shin-Etsu announced a fresh $100 billion investment in its silicone portfolio, one of the key sections of its Operational Materials business sector, to strengthen its high-performance silicone goods and expand its line-up of eco-friendly products.

-

In 2022 Siltech Corporation, a global manufacturer of specialties of organic functional silicone announced that they are expanding their manufacturing facilities. A new, cutting-edge grassroots manufacturing plant is nearing completion in terms of engineering design and approval.

| Report Attributes | Details |

| Market Size in 2023 | USD 1.9 Billion |

| Market Size by 2032 | USD 2.8 Billion |

| CAGR | CAGR of 4.5% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Water-soluble, Oil-soluble) • By Application (Emulsifiers, Defoaming Agents, Foaming Agents, Wetting Agents, Dispersants, and Others) • By End-user (Agriculture, Building & Construction, Textile, Personal Care, and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe [Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia Rest of Latin America) |

| Company Profiles | Momentive, DOW Inc., Elkem Silicones, Innospec, Evonik Industries AG, Andisil, Supreme Silicones, Shin-Etsu Chemical Co. Ltd, Wacker Chemie AG, Siltech Corporation |

| Key Drivers | • Growing demand for construction materials • Raising demand for personal care products |

| Market Opportunity | • Growing demand for sustainable products • Rising demand for surfactants from end-user |

Frequently Asked Questions

Ans. Restraints are Harmful emissions released in manufacturing processes and the availability of alternatives to silicone surfactants.

Ans. Drivers are Growing demand for construction materials and personal care products of Silicone Surfactants.

Ans. The CAGR of the Silicone Surfactants Market over the forecast period is 4.5%.

Ans. USD 2.8 billion is the projected Silicone Surfactants Market size of the market by 2032.

Ans. USD 1.9 billion is the market size for Silicone Surfactants Market in 2023.

Get in Touch