Smart Greenhouse Market Report Scope & Overview:

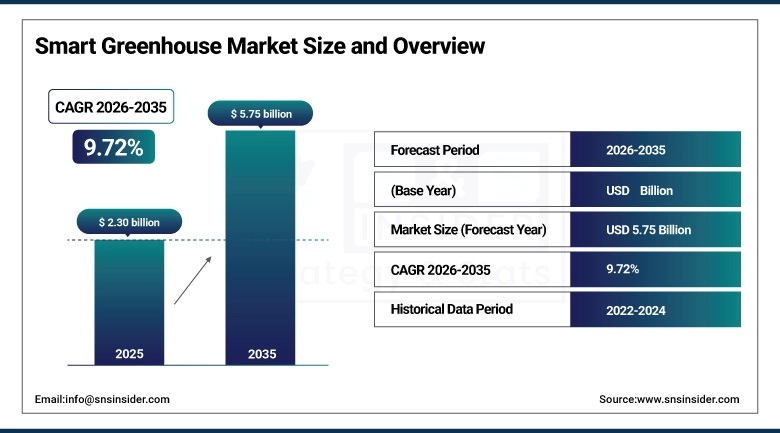

The Smart Greenhouse Market size was valued at USD 2.30 billion in 2025 and is expected to reach USD 5.75 billion by 2035, growing at a CAGR of 9.72% from 2026-2035.

Market growth of Smart Greenhouses is fueled by factors such as rising demand for sustainable agriculture, optimizing agricultural yields, and managing resources efficiently. Advancements in technology such as Internet of Things (IoT), artificial intelligence (AI), climate control, and irrigation systems have enhanced production efficiency and minimized water and energy use.

The Food and Agriculture Organization's 2024 World Food and Agriculture Statistical Yearbook documents that global greenhouse growing area exceeded 5 million hectares with Asia accounting for over 90% but the majority of this area is low-technology film greenhouse that does not qualify as smart greenhouse.

Market Size and Forecast

-

Market Size in 2025: USD 2.30 Billion

-

Market Size by 2035: USD 5.75 Billion

-

CAGR: 9.72% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Smart Greenhouse Market - Request Free Sample Report

Smart Greenhouse Market Trends

-

AI-powered crop growth optimization where machine learning models analyze sensor data streams and adjust climate, lighting, and nutrition parameters in real time to maximize crop development velocity toward target harvest specifications is transforming greenhouse management from periodic human adjustment to continuous algorithmic optimization.

-

Vertical farming integration where smart greenhouse technology is applied to multi-layer indoor growing systems stacked vertically in converted warehouses and purpose-built facilities is creating ultra-high-density growing that achieves 100x land area productivity of open-field growing in urban locations that eliminate food miles.

-

Water recycling and zero-discharge systems where greenhouse irrigation water and nutrient runoff is captured, treated, and recirculated with zero discharge to the surrounding environment are enabling greenhouse construction in water-stressed regions where external environmental discharge regulations would otherwise prohibit intensive cultivation.

-

Renewable energy integration with smart greenhouse climate control where solar panels, wind turbines, and heat pumps provide the substantial energy required for LED lighting and climate control at carbon-neutral cost is enabling sustainable smart greenhouse operations whose energy cost advantages over grid-dependent facilities grow with each renewable energy price improvement.

U.S. Smart Greenhouse Market Size Outlook:

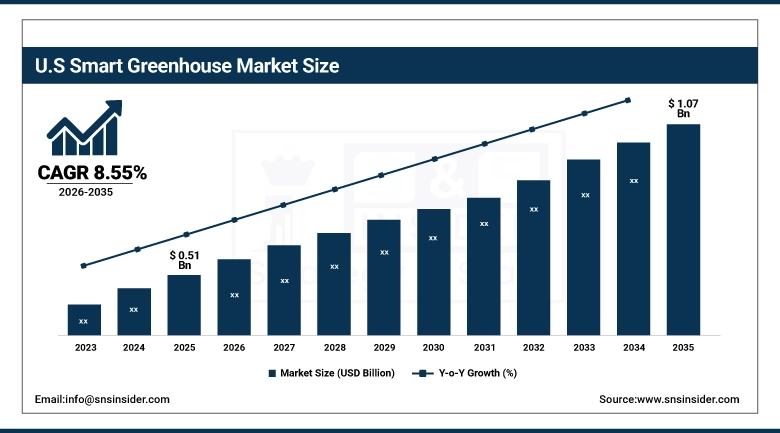

The U.S. Smart Greenhouse Market was valued at USD 0.51 billion in 2025 and is expected to reach USD 1.07 billion by 2035, growing at a CAGR of 8.55% from 2026-2035. Drivers of growth in the U.S. Smart Greenhouses Industry include increased usage of precision farming practices, the need for round-the-year crop cultivation, and labor issues faced by the agricultural industry. Increased spending on climate-controlled systems, IoT-based monitoring, and water-saving cultivation technology are additional factors driving the adoption of smart greenhouses.

The Controlled Environment Agriculture Center at Cornell University's 2024 market assessment documents that U.S. controlled environment agriculture production revenues exceeded USD 4 billion annually with tomatoes, cucumbers, leafy greens, and herbs as the four largest revenue categories sustained by retail premium pricing that compensates for CEA's higher production costs relative to field growing in optimal climates.

Smart Greenhouse Market Segment Analysis

-

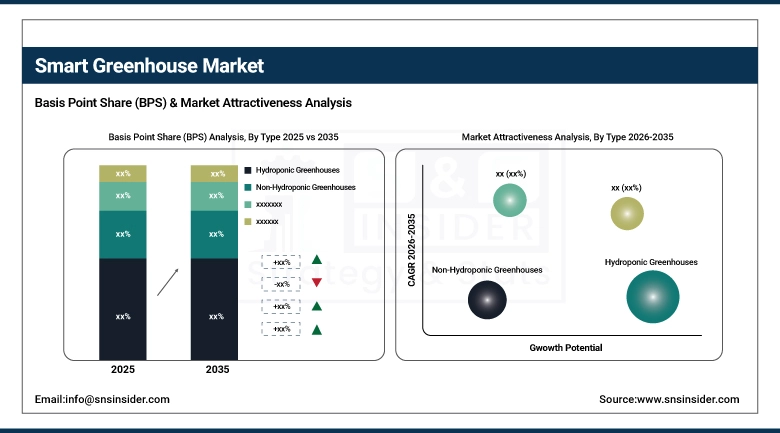

By Type, Hydroponics dominant; Non-Hydroponic growing at fastest CAGR driven by accessibility for traditional growers.

-

By Component, HVAC Systems dominated with ~42.9% share in 2025; LED Grow Lights growing at fastest CAGR.

-

By Material, Polyethylene dominated with ~61.8% share in 2025; Polycarbonate growing fastest for durability.

-

By End User, Commercial Growers dominated with ~57.3% share in 2025; Research Institutions fastest CAGR.

By Type: Hydroponics dominant, Non-Hydroponic growing fastest

Hydroponic greenhouses where plants grow in nutrient-rich water solutions without soil represent the majority of smart greenhouse installations and revenue, reflecting hydroponics' superior water efficiency, nutrient delivery precision, and disease management advantages that justify the higher system complexity relative to soil-based growing. Hydroponic systems encompass multiple sub-types nutrient film technique (NFT) for leafy greens, deep water culture (DWC) for lettuce and herbs, drip irrigation systems for vine crops, and Dutch bucket systems for tomatoes and cucumbers each optimized for specific crop types and whose automation integration creates the smart greenhouse capability that drives market growth.

Non-Hydroponic greenhouses are expected to grow at the fastest CAGR from 2026-2035, reflecting the broader addressable market that soil-based smart greenhouse technology serves. Soil-based growing remains the foundation of greenhouse cultivation for crops where hydroponic alternatives have not been commercially proven cannabis, specialty herbs, ornamentals, and certain fruit crops and for growers whose existing greenhouse infrastructure uses soil-based cultivation methods whose replacement with hydroponic systems would require substantial capital reinvestment.

By Component: HVAC dominates at 42.9%, LED Grow Lights fastest CAGR

HVAC Systems held approximately 42.9% of the Smart Greenhouse Market in 2025, reflecting both climate control's fundamental role in creating the controlled environment that defines greenhouse cultivation's advantage over field growing and the capital cost of industrial-scale heating, ventilation, and cooling systems. A commercial greenhouse's HVAC system encompassing boilers or heat pumps for winter heating, evaporative cooling or refrigerated cooling for summer temperature management, CO2 enrichment systems, and humidity management infrastructure represents 30-40% of total greenhouse construction cost in northern climate operations where heating requirements are substantial. The smart greenhouse's HVAC intelligence where AI-controlled climate management continuously optimizes temperature, humidity, and CO2 toward crop-specific targets while minimizing energy consumption creates the value that transforms conventional greenhouses into smart greenhouses whose technology premium is justified by energy savings and yield improvement.

LED Grow Lights are growing at the fastest component CAGR, driven by the rapid cost reduction that LED technology improvements have delivered LED fixture costs have fallen 70% since 2018, and LED efficacy (lumens per watt) has improved 50% making LED supplemental lighting economically viable for a broader range of crops and geographic locations than the high-pressure sodium and metal halide lighting that LED is progressively replacing. LED grow lights' spectral tunability the ability to adjust the ratio of red, blue, far-red, and white light output enables crop-specific lighting recipes whose photomorphogenic benefits (plant architecture control, flowering stimulation, yield optimization) go beyond simple light quantity to address the light quality dimension of plant growth that conventional lighting cannot achieve.

By End User: Commercial Growers dominate, Research fastest

Commercial Growers held approximately 57.3% of the Smart Greenhouse Industry in 2025, reflecting their large-scale capital investment in smart greenhouse technology whose ROI depends on the yield improvement, resource efficiency, and labor savings that automation and data analytics deliver at commercial production scale. Large commercial greenhouse operations including Dalsem greenhouse projects in Europe, Gotham Greens in the U.S., and Jiangsu Academy of Agricultural Sciences in China invest in sophisticated climate control, automated growing systems, and AI-powered management platforms that smaller operations cannot justify. Research Institutions are growing at the fastest end-user CAGR, driven by university, government, and private research programs investigating controlled environment agriculture for food security, plant science, and sustainable agriculture applications.

Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

85% |

|

Europe |

Netherlands |

35% |

|

Asia Pacific |

China |

52% |

|

Middle East & Africa |

UAE |

40% |

|

Latin America |

Brazil |

48% |

North America Smart Greenhouse Market Insights

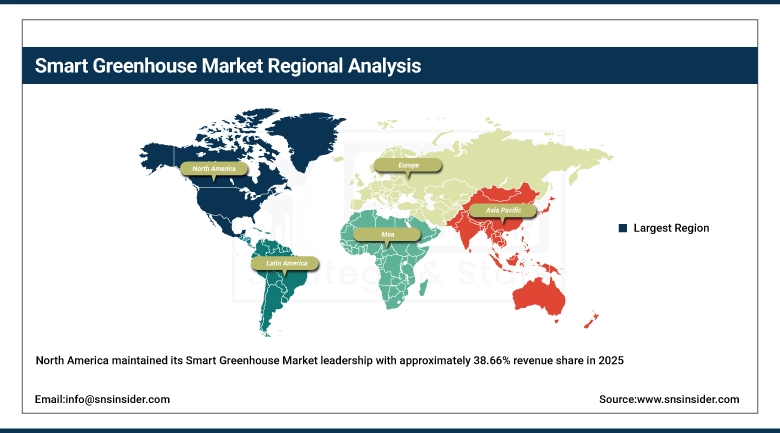

North America maintained its Smart Greenhouse Market leadership with approximately 38.66% revenue share in 2025, sustaining dominance through the U.S.'s large commercial greenhouse sector, strong venture capital investment in CEA technology companies, and the retail premium environment that makes premium-priced greenhouse produce commercially viable at scale. The consolidation of U.S. retail grocery into large national chains whose centralized buying creates nationwide distribution opportunities for domestic greenhouse produce reducing food miles and providing year-round supply consistency sustains the commercial incentive for U.S. greenhouse expansion investment.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Smart Greenhouse Market Insights

Asia Pacific is the fastest-growing regional Smart Greenhouse Industry, driven by China's massive existing greenhouse sector over 4 million hectares of greenhouse area whose technology upgrade toward smart systems represents an enormous addressable market Japan's sophisticated precision agriculture culture whose farmers have among the world's highest per-unit greenhouse technology investment, and India's rapidly growing controlled environment agriculture adoption driven by population growth and food security investment. China's government agricultural modernization programs funding smart greenhouse technology deployment in the rural vitalization initiative are accelerating technology upgrade rates that pure commercial ROI timelines would extend. South Korea's vertical farming industry represented by companies including Smart Farm Korea and Seoul National University's greenhouse technology programs is creating Asia Pacific's most technically advanced controlled environment agriculture ecosystem.

China's Ministry of Agriculture and Rural Affairs reports that government subsidies for greenhouse modernization technology reached CNY 4.2 billion in 2024 the largest annual government smart greenhouse investment globally accelerating technology adoption at the millions of Chinese greenhouse operations whose average technology level remains below global best practice despite the sector's enormous aggregate scale.

Europe Smart Greenhouse Market Insights

Europe's Smart Greenhouse Market is characterized by the world's most sophisticated commercial greenhouse sector concentrated in the Netherlands, which produces 25% of European fresh tomatoes from approximately 9,000 hectares of advanced greenhouse cultivation and the EU's strong policy support for sustainable agriculture through the Farm to Fork strategy and its controlled environment agriculture investment components. Dutch greenhouse technology companies including Priva, Ridder, and Royal Brinkman sustain a globally dominant greenhouse technology supply ecosystem whose products and expertise are exported worldwide as the reference standard for advanced greenhouse management.

MEA and Latin America Smart Greenhouse Market Insights

The Middle East's Smart Greenhouse Industry is growing with the Gulf states' food security investment driven by the recognition that domestic fresh produce production in desert climates requires controlled environment agriculture creating government-funded smart greenhouse programs in Saudi Arabia, UAE, and Qatar. Emirates Hydroponics Farms and Pure Harvest Smart Farms in UAE represent commercially operating smart greenhouse companies demonstrating the viability of high-technology year-round vegetable production in extreme climates. Latin America's market is growing in Brazil, Chile, and Mexico, where premium produce markets, expanding export opportunities for off-season vegetables, and the availability of agricultural technology financing are sustaining smart greenhouse adoption.

Growth Drivers: Food security urgency and climate-resilient agriculture demand driving sustained smart greenhouse market growth globally

The Smart Greenhouse Industry is growing at a fast pace owing to growing food security threats and higher demands for agriculture methods that adapt well to changes in the climate. The use of smart greenhouses allows controlled agriculture practices, thus ensuring better crop yields with reduced reliance on climatic conditions. The growing use of IoT devices, artificial intelligence for monitoring processes within the farm, automatic irrigation systems, and climate control equipment allows for improved water, energy, and fertilizer utilization. Moreover, factors such as urbanization and reduced arable land are contributing to the growth of the smart greenhouse market.

Restraints: High capital costs and energy intensity creating smart greenhouse market adoption barriers in cost-sensitive markets globally

Smart greenhouse construction costs ranging from USD 200/m² for basic smart film greenhouses to USD 2,000/m² for full-technology glass greenhouse with LED supplemental lighting and full automation create capital investment barriers that restrict adoption to well-capitalized commercial operators and government-funded programs whose access to affordable long-term capital accommodates the 8-15 year payback periods that smart greenhouse economics sustain in most crop and market combinations. Energy intensity is the smart greenhouse market's most persistent operational challenge: LED lighting, climate control, and water treatment collectively represent 30-50% of production costs in northern-climate smart greenhouse operations where extended lighting periods and heating requirements create continuous large energy loads whose cost directly determines the economic viability of smart greenhouse production relative to field or import alternatives.

Opportunities: Urban vertical farming expansion and AI-powered yield optimization creating significant smart greenhouse industry growth opportunities

Urban farming's expansion where controlled environment agriculture facilities are developed within or immediately adjacent to major urban population centers whose fresh produce consumption and premium willingness-to-pay create favorable unit economics represents the smart greenhouse market highest-growth commercial opportunity. Proximity to urban consumers enables direct-to-retail and direct-to-consumer supply chain models that eliminate the 2-4 day post-harvest transit that long-distance produce distribution imposes, delivering fresher produce with measurably better nutritional content and shelf life that premium urban grocery retail is willing to pay substantial premiums to source. AI-powered yield optimization whose documented performance improvements 25-40% yield increase through algorithmic climate management versus human-judgment-based greenhouse management provide the ROI justification that persuades conservative growers to invest in smart greenhouse technology upgrades.

Recent Developments:

-

2026: Signify (Philips Horticulture LED) launched GreenPower LED toplight Gen5 with 3.8 µmol/J efficacy the highest commercially available LED fixture efficiency globally enabling smart greenhouse operators to achieve equivalent Daily Light Integral targets with 15% less energy than Gen4 fixtures, reducing lighting energy cost by an estimated USD 12 per m² annually at European electricity tariffs and creating an accelerated payback period for LED fixture replacement at existing smart greenhouse installations.

-

2025: Priva launched its Priva Compass greenhouse management platform — an AI-powered greenhouse operating system integrating climate control, irrigation management, crop registration, and predictive analytics in a single cloud-native platform achieving integration with over 200 greenhouse hardware brands through standardized communication protocols, enabling existing greenhouse technology investments to connect to a unified intelligence layer without requiring hardware replacement.

Smart Greenhouse Companies are:

-

Priva BV

-

Ridder Group

-

Argus Control Systems Ltd.

-

Signify NV (Philips Horticulture)

-

Netafim Ltd.

-

Motorleaf Inc.

-

Dalsem Greenhouse Projects

-

Iron Ox Inc.

-

Gotham Greens LLC

-

Little Leaf Farms LLC

-

AppHarvest Inc.

-

Spread Co. Ltd.

-

SananBio Inc.

-

Logiqs BV

-

Van der Hoeven Horticultural Projects

-

Gakon Horticultural Projects BV

-

Certhon Build BV

-

Pure Harvest Smart Farms

Smart Greenhouse Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.30 Billion |

| Market Size by 2035 | USD 5.75 Billion |

| CAGR | CAGR of 9.72% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Hydroponic Greenhouses, Non-Hydroponic Greenhouses) • By Component (HVAC Systems, LED Grow Lights, Sensors, Control Systems, Others) • By Material (Polyethylene, Polycarbonate, Glass, Others) • By End User (Commercial Growers, Research Institutions, Residential, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Royal Brinkman, Priva BV, Ridder Group, Argus Control Systems Ltd., Signify NV, Heliospectra AB, Netafim Ltd., Motorleaf Inc., Dalsem Greenhouse Projects, Iron Ox Inc., Gotham Greens LLC, Little Leaf Farms LLC, AppHarvest Inc., Spread Co. Ltd., SananBio Inc., Logiqs BV, Van der Hoeven Horticultural Projects, Gakon Horticultural Projects BV, Certhon Build BV, Pure Harvest Smart Farms. |

Frequently Asked Questions

The Smart Greenhouse Market was valued at USD 2.30 billion in 2025.

North America dominated with approximately 38.66% share; Asia Pacific is the fastest growing.

Polyethylene dominated with approximately 61.8% share; Polycarbonate is growing fastest.

HVAC Systems dominated with approximately 42.9% share; LED Grow Lights are growing fastest.

The Smart Greenhouse Market is expected to grow at a CAGR of 9.72% from 2026 to 2035.

Get in Touch