Vertical Farming Market Size & Trends:

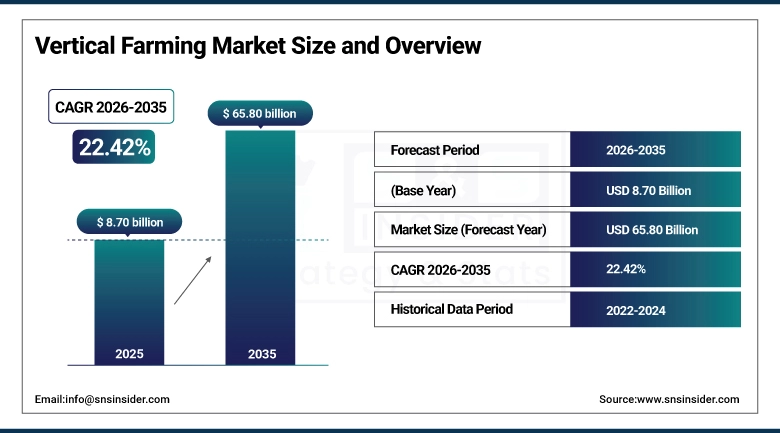

The Vertical Farming Market was valued at USD 8.70 Billion in 2025 and is projected to reach USD 65.80 Billion by 2035, growing at a CAGR of 22.42% during the forecast period 2026–2035.

The case for vertical farming has been building for years, but the conditions that turn a compelling concept into a fast-growing commercial sector are now firmly in place. Cities are getting denser, arable land at the urban fringe is shrinking, and the supply chain disruptions of recent years made the long logistics tail of conventional agriculture harder to defend. Vertical farms sit inside or at the edge of the populations they feed. That proximity alone cuts transport emissions substantially, but the resource efficiency numbers are what tend to resonate most with serious investors and policymakers. Water consumption in a well-run vertical facility runs around 90% lower than field agriculture because systems are closed-loop water is captured, treated, and cycled back rather than lost to runoff and evaporation. Yield per square foot can run ten times what an equivalent outdoor plot produces, which changes the math on urban land value in ways that make city real estate viable as a production asset rather than simply a cost.

A growing number of commercial-scale operations have worked through the early-stage economics and are expanding. LED lighting now delivers the specific spectral outputs plants need at a fraction of the energy draw of earlier systems, climate control has become more precise, and software-driven crop management tools are reducing the dependence on experienced growers that made early vertical farms difficult to replicate at scale.

Vertical Farming Market Size and Growth Forecast:

-

Market Size in 2025: USD 8.70 Billion

-

Market Size by 2035: USD 65.80 Billion

-

CAGR: 22.42% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Vertical Farming Market - Request Free Sample Report

Key Vertical Farming Market Trends:

-

Vertical farming is finding new commercial ground in pharmaceutical and cosmetic applications, where producers grow medicinal plants and botanical ingredients under controlled conditions that deliver consistency in potency and purity that outdoor or greenhouse sourcing cannot reliably match.

-

Sustainability commitments from food retailers and restaurant groups are creating demand pull for vertical farm output, as consumer-facing brands seek supply chain decisions that support their environmental claims with locally grown, low-pesticide, reduced-emission sourcing.

-

LED lighting, precision climate control, and sensor-integrated crop analytics have matured to a point where the operational economics of vertical farming are substantially stronger than they were three years ago, narrowing the energy cost gap with conventional agriculture while extending capability on crop consistency and quality.

-

Consumer health awareness is shaping retail purchasing behavior in ways that favor vertical farm produce buyers are demonstrably willing to pay premiums for fresh, traceable, chemical-free food, and vertical farm operators have been effective at communicating those attributes through both retail and direct-to-consumer channels.

-

Energy sourcing has become the defining variable for vertical farm sustainability credentials. Facilities drawing from coal-heavy grid power face legitimate environmental scrutiny, while operations integrating solar or wind generation, or securing clean power through long-term offtake agreements, are building a meaningfully differentiated position on climate performance.

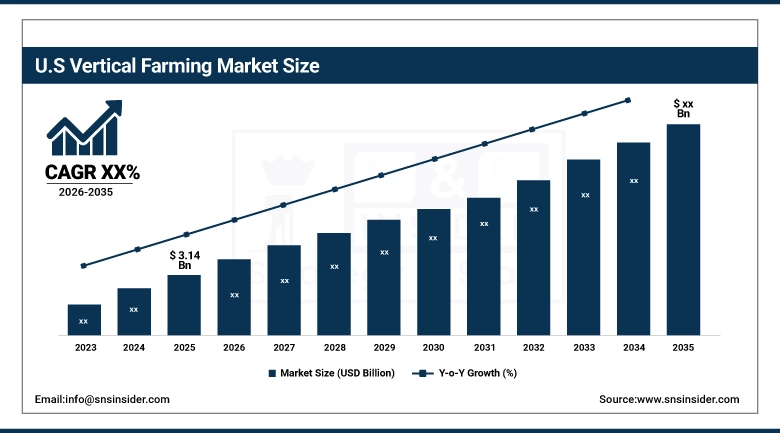

U.S. Vertical Farming Market Size Outlook:

The U.S. Vertical Farming Market was valued at USD 3.14 Billion in 2025, driven by rising urban agriculture adoption, technology investment, and consumer demand for local, sustainably produced food. Smart farming solutions, hydroponics, and controlled-environment agriculture have seen significant deployment across coastal metros and inland distribution-focused production hubs throughout the country.

Vertical Farming Market Growth Drivers:

-

Sustainability Pressures on Conventional Agriculture Are Accelerating the Shift Toward Controlled-Environment Food Production

The environmental cost of conventional agriculture has become difficult to ignore. Soil degradation, aquifer depletion, synthetic fertilizer runoff, and pesticide contamination are each well-documented, individually serious, and collectively unsustainable at the scale required by a global population approaching 10 billion. Vertical farming addresses most of these problems within a single production model. The 90% water reduction reflects the fundamental difference between open-field irrigation where a large fraction of applied water never reaches the plant root zone and closed-loop hydroponic and aeroponic systems where every litter is tracked and recovered. The absence of soil removes most of the pest and disease vectors that make pesticide application routine in field crops, cutting chemical inputs without the yield penalties that complicate organic field production at commercial scale. Proximity to urban markets is not just a logistics advantage; it is a carbon accounting one.

Vertical Farming Market Restraints:

-

Energy Consumption and Power Source Dependencies Constrain the Environmental and Economic Case for Vertical Farming at Scale

The energy intensity of vertical farming is not a secondary concern it is the central operational challenge the industry needs to resolve to fully deliver on its sustainability premise. Plants in an enclosed facility receive no natural light. Every unit of photosynthetically active energy comes from electrical systems running continuously across the growing cycle. LED technology has reduced per-unit energy draw substantially, but the aggregate demand across a production-scale installation is still significant. Electricity costs that are competitive with field agriculture in low-tariff markets become a genuine margin problem as energy prices rise, which they have done across most developed markets in recent years. The carbon implications depend entirely on grid mix. A vertical farm drawing from a coal-heavy grid can carry a worse carbon footprint than a well-managed field operation with efficient logistics. This is not a reason to dismiss the technology, but it is why the industry's sustainability credentials are contingent on the pace at which operators shift to dedicated renewable generation or credibly source clean power through long-term procurement agreements.

Vertical Farming Market Segment Analysis:

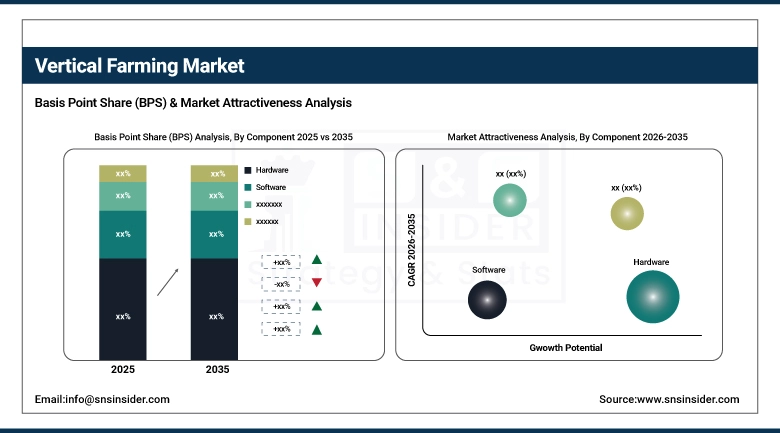

By Component

Hardware dominated with a 45% market share in 2025. The capital intensity of building a vertical farm sits primarily in its physical systems: LED lighting arrays, hydroponic or aeroponic delivery infrastructure, environmental control systems, and irrigation networks that define what the farm can grow, how consistently, and at what operating cost. These are not commodity purchases they require specification, installation, commissioning, and maintenance, which explains why hardware accounts for such a large share of both initial investment and ongoing procurement. Companies like Lettuce Grow have built product lines around modular, scalable hardware configurations that lower the barrier for smaller operations. Software is expected to record the fastest CAGR during 2026–2035. The shift mirrors what has happened across precision agriculture: physical infrastructure is increasingly managed through software, and the value of sensor data from hundreds of monitoring points per growing zone is becoming the real operational differentiator.

By Structure

Shipping containers dominated with a 58% market share in 2025. The appeal is practical: containers are prefabricated, structurally sound, weatherproof, and available globally at prices that make them far more accessible than purpose-built growing structures for early-stage and mid-scale operators. They can be placed in parking lots, on industrial rooftops, at institutional food buyers, or in underserved urban communities where food access is a genuine challenge. Companies including Freight Farms and Container Farm have built commercially viable businesses around the format, proving that a standardized container-based system can produce meaningful volumes of leafy greens and herbs at unit economics that work without requiring the capital outlay of a full building-based facility. Building-based vertical farming is expected to record the fastest growth rate during 2026–2035. As the industry matures and capital becomes more available at favorable terms, the economics of purpose-built or converted large-format facilities with their larger footprints, superior climate control integration, and lower per-square-foot cost at scale become increasingly compelling.

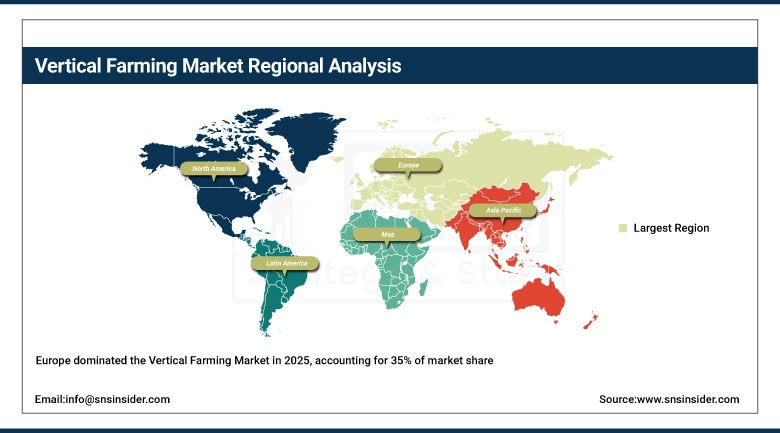

Vertical Farming Market Regional Analysis:

Europe Vertical Farming Market Trends

Europe held a 35% market share in 2025 and is expected to be among the fastest-growing regions during 2026–2035. The Netherlands, Germany, and the UK have built meaningful vertical farming sectors underpinned by strong agricultural research, high consumer willingness to pay for locally produced food, and regulatory frameworks that reward sustainable production practices. Food security concerns sharpened by supply chain disruptions in 2020–2022 and energy market volatility have given vertical farming policy support that translated into capital availability and retail procurement commitments. Infarm, based in Berlin, and Agricool in France represent the regional approach of placing modular growing systems directly inside urban retail supply chains, reducing the logistics gap between farm and store to a minimum.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Vertical Farming Market Trends

North America held significant market share in 2025, backed by venture capital investment, established technology infrastructure, and a consumer market that has consistently supported local and sustainable food brands. The United States leads regional adoption, with AeroFarms, Bowery Farming, and BrightFarms each having built commercial-scale operations supplying major retail accounts. Canada has invested in controlled-environment agriculture as a hedge against climate vulnerability in its domestic food supply.

Asia-Pacific Vertical Farming Market Trends

Asia-Pacific is the fastest-growing region during 2026–2035. Japan, Singapore, and parts of China face a combination of land scarcity, dense urban populations, and consumer preference for food safety and traceability that makes vertical farming an economically rational response rather than an aspirational one. Japan has operated sophisticated plant factory systems for decades through companies like Mirai Co., Ltd., and the technology has moved from high-cost specialty production to competitive commercial scale. Singapore's Sky Greens has built a globally recognized example of tower farming adapted to tropical conditions, and China is deploying vertical farming at a scale consistent with its broader food security strategy.

Latin America Vertical Farming Market Trends

Latin America is at an earlier adoption stage, but improving. Brazil and Mexico are the primary markets, supported by government agricultural modernization programs providing some structural backing for controlled-environment production. Food security pressures, supply chain inefficiency in reaching remote urban populations, and climate vulnerability of traditional growing regions in both countries make the case for vertical farming investment that domestic and international operators are increasingly acting on. Kalera and Altius Farms are among the commercial operators with active or announced presence in the region.

Middle East & Africa Vertical Farming Market Trends

The Middle East presents a straightforward structural case for vertical farming: extreme heat, severely limited arable land, and a political imperative to reduce food import dependency have pushed Gulf state governments and private investors toward controlled-environment agriculture for years. The UAE and Israel are the most advanced markets, with Israel bringing deep precision irrigation and agricultural technology expertise to indoor growing applications. South Africa leads the African continent's early adoption. Operators including Square Roots and Plantagon are active across the region, and sovereign investment in food security infrastructure has funded facility development at a scale that reflects how seriously Gulf states regard their import dependency as a strategic vulnerability.

Competitive Landscape for Vertical Farming Market:

AeroFarms is a U.S. vertical farming leader specializing in aeroponic indoor cultivation of microgreens, commanding over 70% of the U.S. retail microgreens market and pioneering sustainable, climate‑agnostic food production using 90% less water and no pesticides. It aims to expand globally while advancing high‑efficiency vertical agriculture technologies

-

August, 2025: AeroFarms raised equity financing and refinanced debt to support expansion and pre‑construction for a second vertical farm in Danville, Virginia.

Plenty Unlimited Inc. is a U.S. vertical farming innovator using advanced indoor 3D vertical farm technology to grow produce year‑round with high yields and minimal water. Founded in 2014, it operates farms and R&D facilities focused on scalable fresh produce production, supported by major investors and patented automation systems.

-

March, 2025: Plenty opened the world’s first indoor vertical farm dedicated to berries, producing over 4 million pounds of strawberries annually in Richmond, Virginia, powered by its vertical towers and tech platform.

Leading Vertical Farming Companies are:

-

AeroFarms (Model X, Dream Greens)

-

Plenty (Farm Stack, Lettuce Mix)

-

Bowery Farming (Bowery Arugula, Bowery Kale)

-

Infarm (Infarm Grow Platform, Infarm Salad Greens)

-

BrightFarms (Sunny Crunch, BrightBerry)

-

Gotham Greens (Gotham Butterhead Lettuce, Gotham Pesto Basil)

-

Freight Farms (Greenery S, Leafy Green Machine)

-

Vertical Harvest (Microgreen Mix, Leafy Blend)

-

Spread Co., Ltd. (Techno Farm Keihanna, Green Leaf)

-

Agricool (Coolberry, Coolgreens)

-

Urban Crop Solutions (Plant Factory, Cropbox)

-

Sky Greens (Sky Urban Systems, Vertical Farming Towers)

-

Kalera (Kale Microgreens, Butterhead Lettuce)

-

Altius Farms (Living Butter Lettuce, Living Basil)

-

Square Roots (Herb Gardens, Square Roots Salad Mix)

-

JungleBox (Modular Farm System, JungleBox Greens)

-

Sky Vegetables (Sky Romaine, Sky Basil)

-

Plantagon (Plantagon CityFarm, Vertical Greenhouse)

-

iFarm (iFarm Growtune, iFarm Leafy Greens)

-

Mirai Co., Ltd. (Mirai Leafy Green, Mirai Romaine)

|

Report Attributes |

Details |

|---|---|

| Market Size in 2025 | USD 8.70 Billion |

| Market Size by 2035 | USD 65.80 Billion |

| CAGR | CAGR of 22.42% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

|

Report Scope & Coverage |

Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

|

Key Segments |

• By Structure (Shipping Container, Building-based) |

|

Regional Analysis/Coverage |

North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

|

Company Profiles |

AeroFarms, Plenty, Bowery Farming, Infarm, BrightFarms, Gotham Greens, Freight Farms, Vertical Harvest, Spread Co., Ltd., Agricool, Urban Crop Solutions, Sky Greens, Kalera, Altius Farms, Square Roots, JungleBox, Sky Vegetables, Plantagon, iFarm, Mirai Co., Ltd. |

Frequently Asked Questions

Ans: The Hardware segment dominated the Vertical Farming Market.

Ans: The Vertical Farming Market is expected to grow at a CAGR of 22.42% during 2026-2035.

Ans: Europe dominated the Vertical Farming Market in 2025.

Ans: The Vertical Farming Market Size was valued at USD 8.70 Billion in 2025. It is estimated to reach USD 65.80 Billion by 2035, growing at a CAGR of 22.42% during 2026-2035.

Ans: The rising awareness of health and nutrition is significantly influencing the vertical farming market.

Get in Touch