Substrate-Like PCB Market Report Scope and Overview:

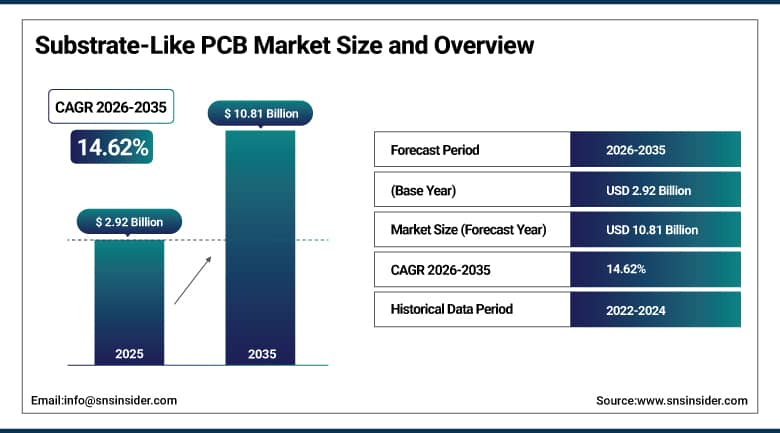

The Substrate-Like PCB Market was valued at USD 2.92 billion in 2025 and is expected to reach USD 10.81 billion by 2035, growing at a CAGR of 14.62% from 2026-2035.

Substrate-Like PCB market has seen tremendous growth because of the increasing requirement for smaller and more efficient electronic devices in the consumer electronics market, the automotive industry, the telecommunication industry, and the computing market. The substrate-like PCB provides ultra-fine circuitry, high-quality signal performance, efficient heat dissipation, and high-density interconnects; therefore, it is ideal for future semiconductor packaging.

Because of investments in AI technology, cloud computing, 5G networks, high-performance CPU technology, and ADAS technology, there is an increase in demand for better PCB architectures. There have been large-scale investments in technologies such as modified semi-additive process technology, lithographic equipment technology, laser drilling technology, and inspection technology.

Substrate-Like PCB Market Size and Forecast

-

Market Size in 2025: USD 2.92 Billion

-

Market Size by 2035: USD 10.81 Billion

-

CAGR: 14.62% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get More Information On Substrate-Like PCB Market - Request Free Sample Report

Substrate-Like PCB Market Trends

-

Increased usage of ultra-fine line space technology below 25/25 µm for future electronic devices.

-

The use of substrate-like PCBs for AI-enabled servers and high-performance computing machines.

-

An increase in investment in advanced package and substrate technologies.

-

Increased consumer interest in compact consumer electronic goods and wearables leading to the rise of SLPs.

-

Quick developments in the field of electric cars and automobiles, resulting in the requirement for advanced PCBs.

-

Adoption of automated optical inspection and AI-based defect detection systems.

-

Increased partnership between semiconductor packaging companies and PCB producers.

-

Advanced thermal management solutions and low loss material usage.

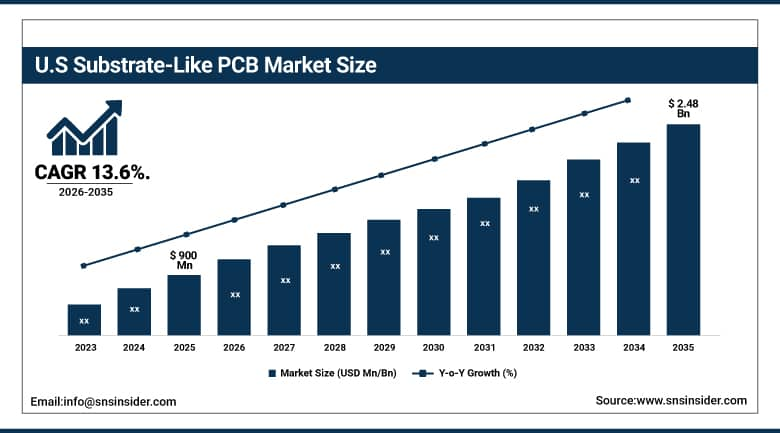

U.S. Substrate-Like PCB Market Size Outlook:

The U.S. Substrate-Like PCB Market was valued at USD 900 million in 2025 and is expected to reach USD 2.48 billion by 2035, growing at a CAGR of 13.6%.

There is a rise in the demand for high-performance computing infrastructure, accelerators for AI, advanced telecommunication infrastructure, and military electronic equipment in the US market. The rising demand for high-density packaging solutions and resilient semiconductor manufacturing in the region is propelling the growth of the market.

Cloud computing infrastructure and advanced AI-based data center technology developments have created ample opportunities for the production of substrate-like PCBs in the US.

Substrate-Like PCB Market Segment Analysis

-

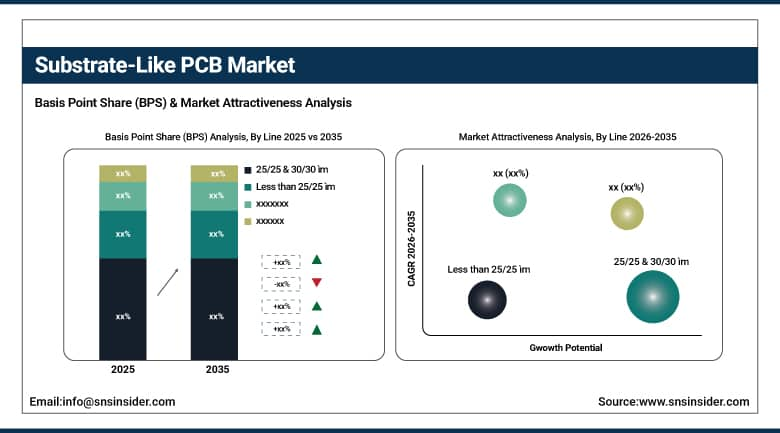

Based on Line, 25/25 & 30/30 µm segment led in the Substrate-Like PCB (SLP) share at 66.3% globally.

-

Based on Inspection Technology, Automated Optical Inspection (AOI) had the largest share, accounting for 53.3%

-

Based on Application, Consumer Electronics held the highest share 56.3%.

-

Based on End-User, industrial dominated the market with 52.79% share in 2025; while commercial are the fastest growing segment with CAGR of 17.29% during 2026 to 2035.

By Line Width, 25/25 & 30/30 µm Segment Dominated While Finer Line SLP Designs Continue Expanding

The 25/25 µm and 30/30 µm line width segment led the global Substrate-Like PCB (SLP) market in 2025, contributing more than 66.3% of the overall revenue share. The prominence of this segment is mainly because of its extensive application in mobile phones, tablets, wearable, and other consumer electronic equipment that necessitates small circuit density along with better electrical performance. This type of line width offers a good balance of miniaturization capability, scalability in manufacturing, effective signal transmission capability, and cost-effectiveness in the production of electronic goods. Most leading OEMs and semiconductor packaging manufacturers are employing 25/25 µm and 30/30 µm SLP technology because of the suitability of these types of boards to advanced HDI boards and multilayer substrates. The rising demand for thin, lightweight, and functional consumer products will drive the use of these line widths on a larger scale.

By Inspection Technology, Automated Optical Inspection (AOI) Accounted for the Largest Share

In 2025, the share held by Automated Optical Inspection (AOI) accounted for about 53.3% of the Substrate-Like PCB market owing to the increasing need for complex ultra-fine circuit designs and defect detection techniques for advanced PCB manufacturing. The use of AOI has become common while examining misalignments, micro-cracks, short circuits, open circuits, and surface defects in the fabrication of high-density PCBs. There will be an upsurge in the need for AOI as the demand for smaller electronic parts and substrate structures requires advanced automated optical inspection technologies, which provide effective results with fewer defects during production. AI-driven Automated Optical Inspection tools are slowly gaining popularity to allow faster inspections and reduce any possible manufacturing defects. Higher production volumes for smartphones, semiconductor substrates, and automotive electronics drive the use of AOI technology among advanced PCB manufacturing plants.

By Application, Consumer Electronics Held the Highest Share

The Consumer Electronics Vertical was the leading segment in the Substrate-Like PCB Market in 2025, generating around 56.3% of the market share in terms of revenue generation. The rising global consumption of smart phones, laptops, tablets, wearables, gaming consoles, and various other small smart electronics has mainly propelled the growth of the consumer electronics vertical. Substrate-like printed circuit boards offer superior wiring density, better signal integrity, thin package height, and excellent thermal management features. These attributes make substrate-like printed circuit boards the most suitable choice for upcoming portable electronics. Top electronics companies are opting for substrate-like printed circuit board technology in their products, as it allows them to incorporate thinner device profiles, enhanced processing speed, and the integration of AI and 5G features into small form factors.

Substrate-Like PCB Market Regional Analysis:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

~83% |

|

Europe |

United Kingdom |

~28% |

|

Asia Pacific |

China |

~49% |

|

Middle East and Africa |

UAE |

~32% |

|

Latin America |

Brazil |

~47% |

North America Substrate-Like PCB Market Insights

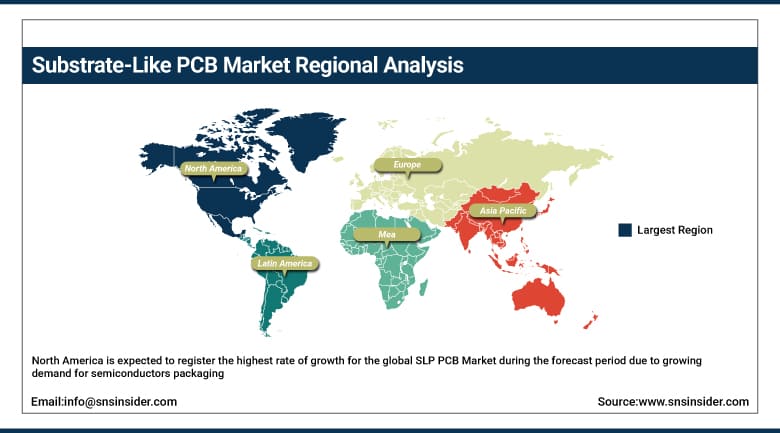

North America is expected to register the highest rate of growth for the global SLP PCB Market during the forecast period due to growing demand for semiconductors packaging, AI-driven computing systems, data centers, and highly sophisticated consumer electronics in the US and Canada. Growing application of 5G smartphones, cloud computing components, automotive electronics, and network devices is boosting the adoption of PCBs having ultra-fine lines in the region. Significant investments made in the semiconductor manufacturing sector, the expansion of the electronics supply chain in the region, and advancements in electronics packaging technologies are some of the other factors expected to drive market growth in North America. The adoption of AI-powered processors, edge computing solutions, and high-density electronics architectures will help boost the adoption of SLP PCBs in next-gen electronic devices.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Substrate-Like PCB Market Insights

Europe represents an important market share in the international Substrate-Like PCB (SLP) Market owing to the rising need for enhanced electronics products in automotive applications, automation processes, and communications networks in countries like Germany, UK, France, Italy, and the Netherlands. Manufacturers in the region have been increasingly using substrate-like PCBs for electric vehicles, advanced driver assistance systems, robotic automation solutions, and aerospace electronics, which require efficient circuitry and improved thermal properties. The regional governments' push toward semiconductor development, digital infrastructure growth, and industry 4.0 transition programs has fueled the demand for innovative PCB solutions in the region. Germany still dominates the market owing to its thriving automotive electronics segment and growing emphasis on EV production and intelligent transportation solutions.

Asia Pacific Substrate-Like PCB Market Insights

Asia-Pacific took the lead in the global SLP PCB market in 2025 due to its well-developed electronics manufacturing industry, substantial semiconductor manufacturing capacities, and consumer electronics consumption needs in China, Taiwan, South Korea, Japan, and Southeast Asia. China continues taking the top position in the region due to massive output volumes in smartphones, rapid roll-out of 5G infrastructure, and semiconductor packaging applications. The regions of Taiwan and South Korea maintain their dominant positions due to highly developed PCB fabrication technology and active presence of semiconductor fabrication plants and electronics manufacturing original equipment manufacturers (OEMs). Increasing consumer demands for small-sized electronic gadgets, wearable devices, AI-powered consumer electronics, and automotive electronics are driving the demand for highly dense SLP PCBs.

Latin America Substrate-Like PCB Market Insights

A steady rise in the demand for substrate-like PCBs can be witnessed in Latin America because of increased assembly work in the electronics industry, growth in telecommunication networks, and an increasing need for consumer electronic goods in Brazil, Mexico, Argentina, and Chile. Brazil leads the pack when it comes to the number of markets in Latin America because of the growth in the electronics manufacturing industry along with the increasing use of industrial automation technology. Mexico stands out because of its expanding electronics supply chain integrated with manufacturing ecosystems within North America. The adoption of smartphones and automotive electronics is adding up to gradual demand in the region.

Middle East & Africa Substrate-Like PCB Market Insights

Middle East and Africa is experiencing emerging growth in the Substrate-Like PCB (SLP) Market due to increasing digital infrastructure investments, expansion of telecommunications networks, and growing adoption of smart technologies across the United Arab Emirates, Saudi Arabia, South Africa, and Israel. Governments across the region are investing heavily in smart city development, data centers, AI infrastructure, and advanced communication technologies, creating growing demand for high-performance electronic components and advanced PCB solutions. The UAE and Saudi Arabia remain key regional markets due to expanding 5G deployment, digital transformation programs, and increasing investments in semiconductor and electronics ecosystems. Rising adoption of connected devices, industrial automation systems, and intelligent infrastructure solutions is expected to further accelerate substrate-like PCB demand across the region.Bottom of Form

Market Growth Drivers:

-

Rising demand for miniaturized high-performance electronic devices and advanced semiconductor packaging

The rising global requirement for small-sized consumer electronics, fast computing equipment, AI-based products, and 5G communication solutions is greatly contributing to the popularity of Substrate-Like PCB (SLP) products. The SLP technology allows for extremely narrow circuit lines, better signal transfer, improved heat dissipation, and increased electronic component densities, which make it ideal for smartphones, wearable gadgets, computers, servers, and automotive electronics. The rapid developments in semiconductor packaging technology, edge computing, and high-performance processors are motivating the electronics companies to incorporate SLP designs in their new products. The growing applications of AI processors, IoT devices, cloud computing systems, and high-density interconnects in Asia Pacific, North America, and Europe regions are further boosting the global demand for SLP PCBs.

Market Restraints:

-

High manufacturing complexity and elevated production costs limiting adoption

The manufacturing of substrate like PCBs needs some of the most sophisticated production technologies that include precision laser drilling technology, fine line etching technology, as well as inspection technology; thus, making production difficult and costly. Ensuring very fine circuitry with high production yields is a problem for many PCB manufacturers. The increasing cost of raw materials, expensive investments for building semiconductor packaging facilities, as well as lack of highly skilled personnel, are also restricting the expansion of the market. Small PCB companies also find it difficult to produce SLP due to high initial investments.

Market Opportunities:

-

Expanding adoption of AI, automotive electronics, and 5G infrastructure creating new growth opportunities

The quick adoption of AI computing, self-driving cars, EVs, fast networking, and electronic devices enabled by 5G technology is providing numerous opportunities for the global Substrate-Like PCB Market. The SLP technology is gaining prominence in applications such as ADAS, AI accelerators, cloud servers, data centers, and communication devices that need excellent signal performance and compact boards. Increased spending on semiconductor localization, packaging innovations, and integration of high-density electronic components is anticipated to drive growth in the market. Innovation in ultra-thin PCB substrate, flexible electronics, and thermal management solutions is expected to create opportunities across several growth electronics segments.

Recent Developments:

-

2026: Ibiden Co., Ltd. increased their production capability for substrates like PCBs due to an increase in demand for the product due to AI server usage, HPC applications, and semiconductor packaging applications.

-

2025: Unimicron Technology unveiled their innovative next-generation ultra-fine line substrate-like PCBs intended for use in AI smartphones, 5G communication products, and wearables.

Substrate-Like PCB Market Key Players

-

Ibiden Co., Ltd.

-

Unimicron Technology Corporation

-

Zhen Ding Technology Holding Limited

-

AT&S Austria Technologie & Systemtechnik AG

-

TTM Technologies, Inc.

-

Samsung Electro-Mechanics Co., Ltd.

-

Compeq Manufacturing Co., Ltd.

-

Tripod Technology Corporation

-

Shennan Circuits Co., Ltd.

-

Nippon Mektron, Ltd.

-

Daeduck Electronics Co., Ltd.

-

Kinsus Interconnect Technology Corp.

-

Nan Ya PCB Corporation

-

Meiko Electronics Co., Ltd.

-

Career Technology (Mfg.) Co., Ltd.

-

Kinwong Electronic Co., Ltd.

-

Unitech Printed Circuit Board Corp.

-

LG Innotek Co., Ltd.

-

CMK Corporation

-

Toppan Inc.

Substrate-Like PCB Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.92 Billion |

| Market Size by 2035 | USD 10.81 Billion |

| CAGR | CAGR of 14.62% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments |

• By Line (25/25 & 30/30 ìm, Less than 25/25 ìm) • By End USe (Industrial, Commercial, Residential) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Ibiden Co., Ltd., Unimicron Technology Corporation, Zhen Ding Technology Holding Limited, AT&S Austria Technologie & Systemtechnik AG, TTM Technologies, Inc., Samsung Electro-Mechanics Co., Ltd., Compeq Manufacturing Co., Ltd., Tripod Technology Corporation, Shennan Circuits Co., Ltd., Nippon Mektron, Ltd., Daeduck Electronics Co., Ltd., Kinsus Interconnect Technology Corp., Nan Ya PCB Corporation, Meiko Electronics Co., Ltd., Career Technology (Mfg.) Co., Ltd., Kinwong Electronic Co., Ltd., Unitech Printed Circuit Board Corp., LG Innotek Co., Ltd., CMK Corporation, and Toppan Inc. |

Frequently Asked Questions

The Substrate-Like PCB Market is expected to grow at a CAGR of 14.62% from 2026 to 2035.

The Substrate-Like PCB Market was valued at USD 2.92 Billion in 2025.

25/25 & 30/30 µm held approximately 66.3% share in 2025.

Automated Optical Inspection (AOI) dominated with approximately 53.3% share in 2025.

North America is expected to grow at the fastest CAGR of 9.8% in the Substrate-Like PCB Market.

Get in Touch