Tank Level Monitoring System Market Report Scope & Overview:

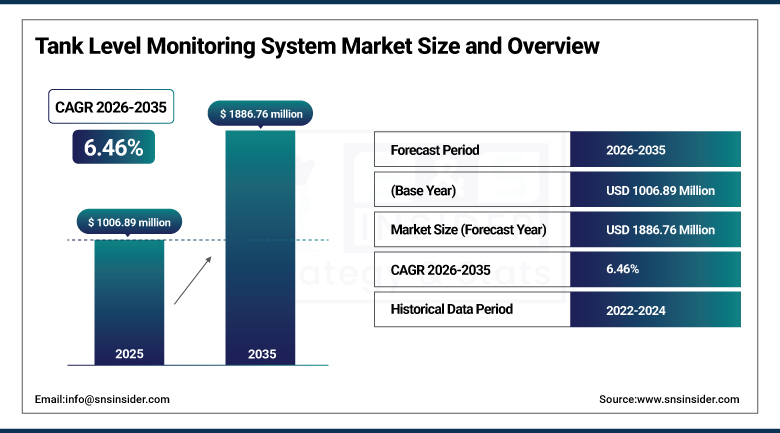

The Tank Level Monitoring System Market was valued at USD 1,006.89 Million in 2025 and is expected to reach USD 1,886.76 Million by 2035, growing at a CAGR of 6.46% from 2026–2035.

The tank level monitoring system market is exhibiting strong growth at a sustainable commercial rate. The tank level monitoring system is the type of instrument which monitors or tracks the levels of liquid, slurry, or bulk materials stored within a storage or processing tank, ensuring timely information regarding inventory levels for remote monitoring, process control, safety management, and adherence to rules and regulations. This market is witnessing expansion based on the requirement for real-time inventory tracking and safety and automation within sectors such as oil & gas, water, and chemicals. Moreover, the use of IoT and cloud computing technologies, which provide for real-time remote monitoring at many locations, is contributing to its growth.

In April 2023, Emerson Electric upgraded its tank level monitoring systems with IoT-enabled remote access, enabling real-time monitoring, predictive maintenance, and enhanced operational safety across distributed tank farms and remote storage facilities. The upgrade’s wireless connectivity eliminates manual gauge reading rounds whose labour cost and measurement frequency limitation create operational inefficiency, while predictive maintenance analytics reduce unplanned measurement system downtime whose impact on tank inventory accuracy creates operational and regulatory compliance risk.

Market Size and Forecast

-

Market Size in 2026E: USD 1,072.00 Million

-

Market Size by 2035: USD 1,886.76 Million

-

CAGR: 6.46% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

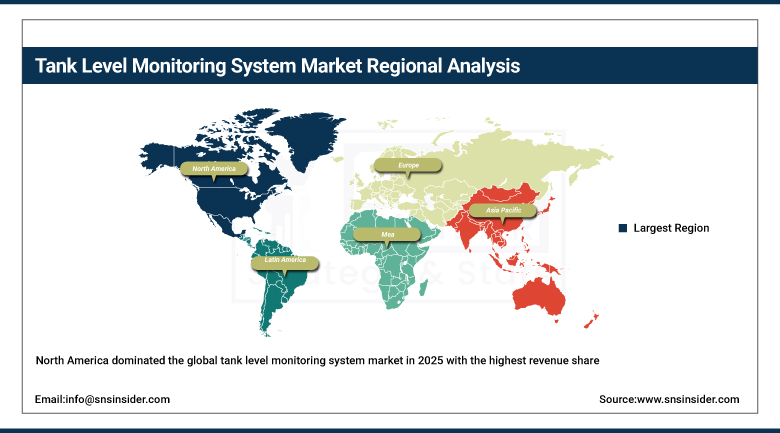

Largest Region: North America

To Get more information on Tank Level Monitoring System Market - Request Free Sample Report

Tank Level Monitoring System Market Trends

-

IoT-enabled tank monitoring platforms provide real-time inventory visibility across sites, reducing manual inspections and improving operational efficiency.

-

Falling radar sensor costs are expanding adoption across water, agriculture, food processing, and lower-value storage applications.

-

Wireless LoRaWAN and NB-IoT connectivity enable remote tank monitoring without extensive wired communication infrastructure investments.

-

Stricter environmental regulations are increasing demand for tank monitoring systems supporting leak detection and overflow prevention compliance.

-

Digital twin integration enhances tank farm management through inventory optimization, refill planning, and capacity utilization improvements.

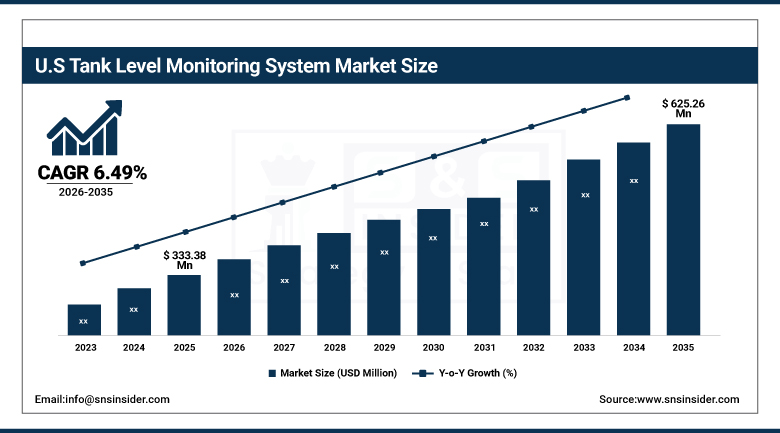

The U.S. Tank Level Monitoring System Market Outlook

The U.S. Tank Level Monitoring System Market was valued at approximately USD 333.38 Million in 2025 and is expected to reach approximately USD 625.26 Million by 2035, growing at a CAGR of approximately 6.49%.

The U.S. is the most commercially significant tank level monitoring system market within North America’s dominant revenue position. Emerson Electric’s Rosemount tank gauging division, Honeywell Enraf, Endress+Hauser’s U.S. operations, and VEGA Americas collectively serve the domestic oil and gas, chemical, and water utility markets. EPA’s underground storage tank regulation under 40 CFR Part 280, OSHA’s process safety management standard for highly hazardous chemical tanks, and the Clean Water Act’s chemical tank secondary containment requirements create regulatory compliance procurement motivation that sustains consistent domestic demand independent of oil and gas price cycle variation.

Rochester Sensors acquired Tekelek in Ireland in May 2023 as part of its multi-year strategy to expand its global liquid level sensor portfolio for fuel retail, utilities, and industrial tank monitoring applications. The acquisition reflects the commercial recognition that remote fuel tank monitoring for petrol station, bulk fuel distribution, and commercial heating oil delivery route optimization creates above-average IoT-connected tank level monitoring demand whose recurring data subscription revenue sustains above-hardware commercial value.

Tank Level Monitoring System Market Segment Analysis

-

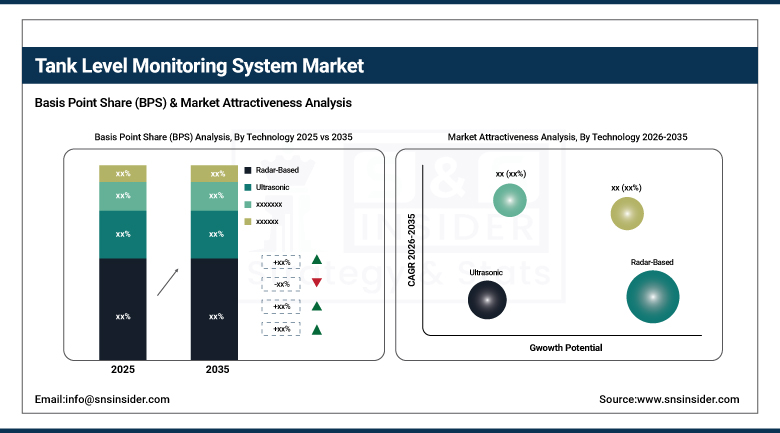

By Technology, the radar-based segment dominated the tank level monitoring system market in 2025 and is expected to witness the fastest growth.

-

By Product Type, the invasive/contact tank level monitoring systems segment dominated the tank level monitoring system market with approximately 58% share in 2025, while the non-invasive/non-contact segment is the fastest growing.

-

By Application, the oil & fuel segment dominated the tank level monitoring system market with approximately 35% share in 2025, while the chemical segment is the fastest growing.

-

By End User, the oil & gas segment dominated the tank level monitoring system market with approximately 38% share in 2025, while the water & wastewater utilities segment is the fastest growing.

By Technology, radar dominates and is expected to grows fastest

Radar-based tank level monitoring retained the dominant technology position in the tank level monitoring system market in 2025. Radar’s dual commercial primacy reflects its position as the most technically capable and commercially mature non-contact tank level measurement technology whose frequency-modulated continuous wave (FMCW) and guided wave radar (GWR) variants collectively serve the broadest range of liquid, slurry, and solid bulk material measurement applications. Each oil terminal’s high-accuracy custody transfer tank gauging, each chemical storage facility’s corrosive liquid non-contact measurement, and each offshore platform’s high-pressure process tank level monitoring creates radar technology procurement whose performance specification reflects the application’s measurement accuracy, reliability, and safety requirements.

The radar-based segment is expected to witness the fastest growth during the forecast period. Growth is driven by declining radar sensor costs, increasing adoption of IoT-enabled monitoring platforms, and rising demand for real-time inventory visibility across industries. Expanding use in water and wastewater management, agriculture, food processing, and remote storage facilities is further supporting adoption. In addition, integration with cloud analytics, wireless communication technologies, and predictive maintenance platforms is enhancing the value proposition of radar-based systems, making them increasingly attractive for both new installations and modernization projects.

By Application, oil & fuel dominates, chemical grows fastest

Oil and fuel retained the dominant application position with approximately 35% of the tank level monitoring system market in 2025. The petroleum storage industry’s tank gauging requirement encompasses API-standard custody transfer measurement at terminals, refineries, and fuel distribution depots whose inventory accuracy directly impacts product transfer value. Each petroleum storage tank whose API 2350 overfill prevention standard requires automatic tank gauging creates regulatory compliance procurement. The global petroleum logistics infrastructure’s tank network, encompassing upstream storage, pipeline terminals, refinery tankage, and retail fuel storage, creates commercial scale whose aggregate procurement defines the oil and fuel application’s dominant market position.

Chemical is the fastest-growing application because specialty chemical storage’s corrosive material handling, extreme temperature requirements, and hazardous substance monitoring create above-average demand for precision radar measurement whose non-contact specification eliminates sensor corrosion risk that invasive alternatives cannot avoid. Each new chemical storage facility whose material properties create invasive sensor specification challenge creates radar non-contact procurement motivation whose technical advantage sustains above-alternative premium specification. The specialty chemical market’s geographic expansion in Asia Pacific creates growing first-time installation demand that compounds with existing facility upgrade investment.

By Product Type, invasive dominates, non-invasive grows fastest

Invasive and contact tank level monitoring systems retained the dominant product position with approximately 58% of the tank level monitoring system market in 2025. The invasive product’s commercial primacy reflects the lower per-system cost and wide application familiarity of float gauging, tape and float tank gauging, capacitance probes, and submersible pressure transmitters whose established installation practice creates specification accessibility for the broadest range of tank monitoring budget contexts. Each water utility, agricultural storage, and commercial fuel storage whose tank monitoring requirement does not demand non-contact measurement creates invasive product specification preference whose lower system cost sustains volume commercial dominance.

Non-invasive products are the fastest-growing category because the progressive democratization of radar and ultrasonic sensor costs is expanding non-contact specification from premium industrial applications into water, food, and commercial fuel monitoring whose measurement quality and maintenance-free operation justify the premium above invasive alternatives. Each non-contact sensor that eliminates probe replacement, cleaning, and calibration cost creates lifecycle cost ROI whose measurement sustains specification preference in high-maintenance invasive alternative contexts.

By End User, oil & gas dominates, water & wastewater grows fastest

Oil and gas retained the dominant end-user position with approximately 38% of the tank level monitoring system market in 2025. The petroleum industry’s extraordinary tank inventory creates the most commercially concentrated tank level monitoring procurement category whose custody transfer accuracy, overfill prevention compliance, and inventory management value create consistent commercial demand. Each oil terminal expansion, each new petroleum storage facility, and each existing tank gauging system upgrade creates procurement whose commercial relationships sustain long-term service and maintenance revenue that sustains above-hardware commercial value.

Water and wastewater utilities are the fastest-growing end user because global water infrastructure investment, smart water grid adoption, and environmental discharge compliance create structured above-average utility sector procurement. Each new water treatment plant, wastewater facility, and potable water storage installation creates tank level monitoring procurement whose utility sector’s government capital programme sustains consistent investment independent of commodity price cycles. The progressive smart water grid adoption, whose real-time tank level monitoring creates distribution network optimization capability, sustains above-average water utility procurement.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Tank Level Monitoring System Market Insights

North America dominated the global tank level monitoring system market in 2025 with the highest revenue share, driven by the strong presence of key end-user industries including oil and gas, chemicals, and power generation. The United States accounts for approximately 87.4% of North American revenues through Emerson Electric’s Rosemount, Honeywell Enraf, Endress+Hauser, and VEGA’s commercial operations, sustained by EPA, OSHA, and industry standard compliance requirements that create non-discretionary tank monitoring investment.

Canada contributes approximately 12.6% of North American revenues through its oil sands storage infrastructure, the pipeline terminal’s custody transfer gauging, and the water utility’s infrastructure investment programme.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Tank Level Monitoring System Market Insights

Europe is a technically sophisticated tank level monitoring system market where ATEX hazardous area standards, REACH chemical regulation’s secondary containment monitoring requirement, and Endress+Hauser’s and VEGA’s European commercial leadership create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its chemical industry’s precision tank measurement requirement, BASF’s and Bayer’s tank farm management, and Endress+Hauser’s Reinach Swiss Headquarters’ European market proximity.

France, the United Kingdom, and the Netherlands are significant secondary markets where petroleum refinery tank gauging, chemical storage monitoring, and water utility infrastructure investment create consistent demand.

Asia Pacific Tank Level Monitoring System Market Insights

Asia Pacific is the fastest-growing regional tank level monitoring system market, driven by China’s extraordinary petrochemical and chemical industry expansion, India’s oil refining and water infrastructure investment, Japan’s advanced process industry’s precision measurement adoption, and Southeast Asia’s rapid industrialization. China accounts for approximately 44.8% of Asia Pacific revenues through its petroleum storage terminal expansion, the chemical industry’s tank monitoring investment, and the water utility’s smart infrastructure programme.

India’s refinery capacity expansion, South Korea’s petrochemical industry, and Australia’s mining and resource sector’s bulk material tank monitoring create significant secondary markets whose combined procurement sustains Asia Pacific’s fastest-growing regional status.

MEA & Latin America Tank Level Monitoring System Market Insights

The MEA and Latin America Tank Level Monitoring System markets are growing steadily due to increasing investments in industrial storage infrastructure and digital monitoring technologies. In the Middle East & Africa, Saudi Arabia accounts for approximately 31.2% of regional revenues, supported by extensive petroleum storage facilities, large petrochemical tank farms, and ongoing investments in oil and gas inventory management systems.

In Latin America, Brazil leads with around 44.2% share, driven by refinery and terminal tank monitoring requirements, expanding chemical industry operations, and modernization of water utility infrastructure. Growing emphasis on operational efficiency, safety, and regulatory compliance continues to support market expansion.

Market Dynamics

Growth Drivers: IoT and automation adoption for real-time inventory management and regulatory compliance driving non-contact monitoring investment

Increasing adoption of IoT and cloud-based solutions enabling real-time remote monitoring is the tank level monitoring system market’s most commercially transformative growth driver. Each industrial operator whose distributed tank farm creates manual gauge reading rounds whose labor cost and measurement frequency limitation creates IoT monitoring investment motivation sustains connected tank monitoring adoption. The cloud platform’s multi-site tank inventory dashboard, refill scheduling algorithm, and API integration with ERP systems creates operational intelligence value that sustains above-hardware commercial relationships whose recurring subscription revenue compounds with the connected sensor installed base.

Regulatory compliance requirements including EPA’s 40 CFR Part 280 underground storage tank regulation, OSHA’s process safety management standard, and API 2350 overfill prevention standard create non-discretionary tank monitoring investment motivation whose compliance character sustains procurement independent of operational ROI alone. Each regulatory tightening that creates new measurement accuracy, data logging, or alarm management requirement creates system upgrade procurement whose compliance deadline creates commercial urgency.

Restraints: High installation cost for precision radar systems and wireless connectivity limitations in remote industrial environments

Precision radar tank level monitoring system’s premium cost relative to float and tape gauging alternatives creates adoption barriers for small storage tank operators and cost-sensitive applications whose measurement accuracy requirement does not justify premium radar investment. Each small fuel oil, agricultural, and commercial storage tank whose simple inventory awareness creates specification preference for lower-cost alternatives that moderates precision radar adoption across the addressable market’s entire population.

Wireless connectivity reliability in remote industrial environments whose thick metal tank walls, electromagnetic interference from industrial equipment, and geographic remoteness create wireless signal attenuation moderates IoT-connected monitoring adoption in technically constrained deployment contexts.

Opportunities: Smart water grid tank monitoring and oil and gas digital twin integration

Smart water grid’s progressive adoption of connected storage tank level monitoring creates above-average utility sector procurement whose government infrastructure investment programme sustains commercial scale. Each new smart water management programme that integrates real-time tank level data with distribution network control creates system procurement whose aggregate across progressive global water utility modernization creates commercial momentum.

Oil and gas digital twin integration connecting tank level monitoring data with virtual refinery and terminal models creates above-average premium system procurement whose operational optimization value sustains investment beyond standard measurement replacement.

Recent Developments:

-

2026: Endress+Hauser launched upgraded digital tank monitoring solutions in 2026 integrating advanced analytics, predictive diagnostics, and IIoT connectivity, helping operators optimize inventory control.

-

2025: Emerson Electric Co. expanded its Rosemount Tank Gauging portfolio with enhanced wireless monitoring and cloud-connected inventory management capabilities, improving real-time tank visibility, operational efficiency, and regulatory compliance.

-

2025: VEGA Grieshaber KG introduced next-generation radar level sensors featuring improved measurement accuracy and extended remote monitoring functionality.

Tank Level Monitoring System Market key players are:

-

Emerson Electric Co. (Rosemount Tank Gauging)

-

Honeywell International Inc. (Enraf)

-

Endress+Hauser Group Services AG

-

VEGA Grieshaber KG (VEGA Americas)

-

Siemens AG (SITRANS LT)

-

ABB Ltd. (Level & Flow)

-

Schneider Electric SE

-

Yokogawa Electric Corporation

-

KROHNE Group

-

Magnetrol International

-

Rochester Sensors LLC

-

Gems Sensors & Controls (Fortive)

-

APG Sensors (Automation Products Group)

-

BinMaster Level Controls

-

Pepperl+Fuchs SE

-

Banner Engineering Corp.

-

Tekelek Europe Ltd. (Rochester Sensors)

-

WIKA Alexander Wiegand SE & Co. KG

-

Piusi S.p.A.

-

SICK AG

Tank Level Monitoring System Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1,006.89 Million |

| Market Size by 2035 | USD 1,886.76 Million |

| CAGR | CAGR of 6.46% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (Radar-Based/FMCW & Guided Wave Radar, Ultrasonic, Float & Tape Gauging, Capacitance Level Monitoring, Conductivity Level Monitoring, Data Transmission/Wireless IoT, Others) • By Product Type (Invasive/Contact Tank Level Monitoring Systems, Non-Invasive/Non-Contact Systems) • By Application (Oil & Fuel, Power Plants, Mining, Chemical, Automotive, Agriculture & Husbandry, Water & Wastewater, Others) • By End User (Oil & Gas, Water & Wastewater Utilities, Chemical & Petrochemical, Food & Beverage, Power Generation, Mining & Minerals, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Emerson Electric Co. (Rosemount Tank Gauging), Honeywell International Inc. (Enraf), Endress+Hauser Group Services AG, VEGA Grieshaber KG (VEGA Americas), Siemens AG (SITRANS LT), ABB Ltd. (Level & Flow), Schneider Electric SE, Yokogawa Electric Corporation, KROHNE Group, Magnetrol International, Rochester Sensors LLC, Gems Sensors & Controls (Fortive), APG Sensors (Automation Products Group), BinMaster Level Controls, Pepperl+Fuchs SE, Banner Engineering Corp., Tekelek Europe Ltd. (Rochester Sensors), WIKA Alexander Wiegand SE & Co. KG, Piusi S.p.A., SICK AG |

Frequently Asked Questions

The Tank Level Monitoring System Market is expected to grow at a CAGR of 6.46% from 2026 to 2035.

The Tank Level Monitoring System Market was valued at USD 1,006.89 Million in 2025.

The need for real-time inventory management, safety, and automation in industries like oil and gas, water, and chemicals, and increasing adoption of IoT and cloud-based solutions.

Radar-based technology dominated the Tank Level Monitoring System Market in 2025 and is also set to grow at the fastest CAGR through 2035.

North America dominated the Tank Level Monitoring System Market in 2025 with the highest revenue share.

Get in Touch