Transfection Reagents and Equipment Market Report Scope & Overview:

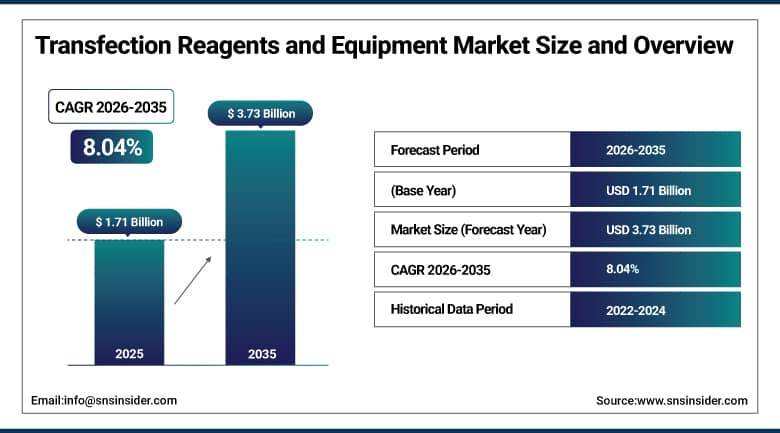

The Transfection Reagents and Equipment Market was valued at USD 1.71 Billion in 2025 and is expected to reach USD 3.73 Billion by 2035, growing at a CAGR of 8.04% from 2026–2035.

The global transfection reagents and equipment market is growing at an exceptional pace. Transfection is the process of introducing nucleic acids including DNA, RNA, siRNA, and mRNA into eukaryotic cells for gene expression, silencing, editing, or therapeutic delivery research. The market is driven by rising R&D expenditure by pharmaceutical and biotechnology companies, technological advancements in transfection methodology, growing demand for synthetic genes and mRNA-based therapies, and the extraordinary expansion of cell and gene therapy clinical programmes. FDA approval of multiple gene therapies has created commercial momentum whose downstream reagent and equipment demand compounds with the growing clinical pipeline.

In April 2023, Sartorius and its subsidiary Sartorius Stedim Biotech acquired Polyplus for approximately USD 2.6 billion from private investors. Polyplus is a French company providing cutting-edge upstream technologies for cell and gene therapies including transfection, high-quality GMP-grade DNA and RNA delivery reagents, and plasmid DNA. The acquisition reflects the commercial recognition that proprietary transfection reagent technology is a high-value strategic asset in the cell and gene therapy manufacturing value chain whose control creates commercial advantage in the fastest-growing biopharmaceutical manufacturing segment.

Market Size and Forecast

-

Market Size in 2026E: USD 1.85 Billion

-

Market Size by 2035: USD 3.73 Billion

-

CAGR: 8.04% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Transfection Reagents and Equipment Market - Request Free Sample Report

Transfection Reagents and Equipment Market Trends

-

Demand for mRNA transfection reagents is increasing as applications expand beyond vaccines into gene editing, therapeutic mRNA, and personalized cancer treatment programs

-

Growth in CRISPR-based gene editing is driving the need for advanced transfection reagents capable of efficiently delivering genetic material into complex cell types

-

Adoption of electroporation technologies is accelerating in cell therapy manufacturing as companies seek effective non-viral methods for genetic modification of immune cells

-

Development of GMP-grade transfection reagents is creating a high-value market segment supported by stringent quality requirements in clinical and commercial biopharmaceutical production

-

AI-driven optimization tools are improving transfection efficiency by identifying ideal reagent formulations and delivery conditions more rapidly than traditional experimental methods

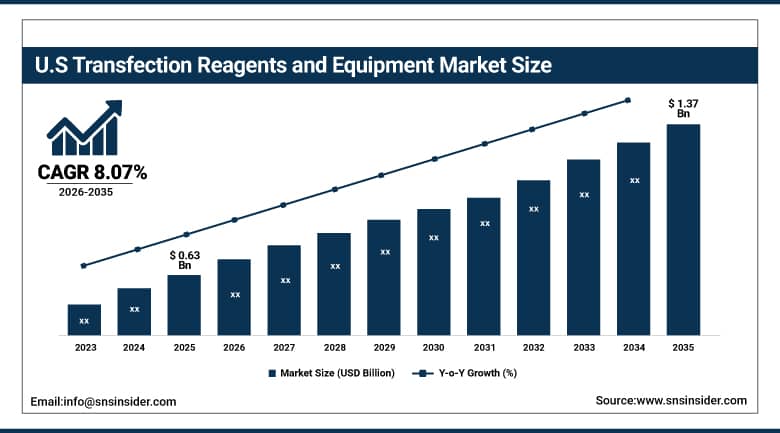

U.S. Transfection Reagents and Equipment Market Outlook

The U.S. Transfection Reagents and Equipment Market was valued at approximately USD 0.63 Billion in 2025 and is expected to reach approximately USD 1.37 Billion by 2035, growing at a CAGR of approximately 8.07%.

The U.S. is the world's most commercially sophisticated transfection reagents and equipment market within North America's dominant revenue position. Thermo Fisher Scientific, Promega, Mirus Bio, and MaxCyte are U.S.-headquartered transfection market leaders whose combined portfolio defines the commercial and technology frontier. The extraordinary U.S. gene therapy clinical pipeline, with hundreds of active IND applications at FDA, creates the most commercially concentrated cell and gene therapy transfection reagent demand globally..

In 2024, MaxCyte Inc. expanded its ExPERT electroporation platform with new high-throughput configurations for clinical and commercial CAR-T cell manufacturing, enabling cell therapy manufacturers to scale ex vivo T-cell transfection from research to GMP clinical production without changing the fundamental electroporation parameters that determine therapeutic product consistency. The expansion reflects the commercial demand for scalable non-viral transfection technology in CAR-T manufacturing whose regulatory preference for non-viral delivery over viral vectors creates structured electroporation equipment procurement from cell therapy developers.

Transfection Reagents and Equipment Market Segment Analysis

-

By Product, the Transfection Reagents segment dominated the Transfection Reagents and Equipment Market with approximately 74% share in 2025, while the Transfection Equipment segment is the fastest growing segment.

-

By Transfection Method, the Lipid-Mediated/Chemical Transfection segment dominated the Transfection Reagents and Equipment Market with approximately 45% share in 2025, while the Electroporation segment is the fastest growing segment.

-

By Application, the Basic Research segment dominated the Transfection Reagents and Equipment Market with approximately 38% share in 2025, while the Gene Therapy segment is the fastest growing segment.

-

By End User, the Pharmaceutical & Biotechnology Companies segment dominated the Transfection Reagents and Equipment Market with approximately 42% share in 2025, while the Contract Research Organizations (CROs) segment is the fastest growing segment.

By Product, reagents dominate, equipment grows fastest

Transfection reagents retained the dominant product position with approximately 74% of the transfection reagents and equipment market in 2025. Reagents’ commercial primacy reflects the recurring consumption model whose laboratory and manufacturing use creates continuous procurement independent of capital equipment replacement cycles. Lipid-based transfection reagents including Lipofectamine, FuGENE, and Lipofection formulations create the most commercially established procurement category whose long history of laboratory use, broad cell type compatibility, and established safety profile sustain consistent academic and industrial procurement.

Transfection equipment is the fastest-growing product because electroporation systems, acoustic liquid handler integration, and automated transfection workstations are replacing manual reagent-based transfection in clinical-scale cell therapy manufacturing whose output quality consistency requirements demand the precision and reproducibility that automated equipment provides. Each new CAR-T manufacturing facility and each gene therapy CDMO capacity expansion creates electroporation equipment procurement whose clinical-grade specification and GMP compliance requirements create above-commodity pricing that sustains above-average equipment segment revenue growth.

By Method, lipid-mediated dominates, electroporation grows fastest

Lipid-mediated and chemical transfection retained the dominant method position with approximately 45% of the transfection reagents and equipment market in 2025. Chemical transfection’s commercial primacy reflects its ease of use, broad cell type compatibility, and established laboratory protocol infrastructure that create the lowest barrier to transfection adoption for researchers transitioning from untransfected controls toward gene expression and silencing experimental designs. Each new research laboratory that establishes transfection capability specifies lipid-based or polymer-based chemical reagents as the starting protocol whose familiarity and published optimisation data create specification continuity.

Electroporation is the fastest-growing transfection method because its ability to deliver nucleic acids into difficult-to-transfect primary cells including T-cells, natural killer cells, haematopoietic stem cells, and iPSCs that lipofection cannot efficiently transfect creates a technically non-substitutable method for the fastest-growing application categories. CAR-T cell manufacturing’s systematic adoption of electroporation for ex vivo T-cell modification, CRISPR gene editing’s requirement for simultaneous delivery of guide RNA and Cas9 protein into primary cells, and stem cell reprogramming’s electroporation protocol adoption collectively create electroporation equipment and consumable procurement that compounds with the cell and gene therapy industry’s commercial expansion.

By Application, basic research dominates, gene therapy grows fastest

Basic research retained the dominant application position with approximately 38% of the transfection reagents and equipment market in 2025. The global academic and institutional biomedical research community’s transfection use across gene function characterisation, protein expression, reporter assay, RNA interference, and CRISPR gene editing experimental designs creates the broadest application base and highest participant count of any transfection application category. NIH, MRC, DFG, and equivalent national research funding whose life sciences allocation sustains university and research institute transfection reagent procurement creates consistent commercial demand that is less sensitive to commercial cycle variation than the biopharmaceutical industry’s product development-linked procurement.

Gene therapy is the fastest-growing application because the extraordinary clinical programme expansion of cell and gene therapies, including FDA-approved gene therapies for haemophilia, SMA, ADA-SCID, and multiple rare diseases, is creating GMP-grade transfection reagent and equipment procurement whose clinical and commercial manufacturing quality standards create premium pricing above research-grade equivalents. Each new gene therapy IND application creates clinical-stage transfection reagent procurement that compounds with the growing programme, and each commercial approval creates manufacturing-scale procurement that sustains above-average segment revenue growth independently of research-grade market dynamics.

By End User, pharma & biotech dominate, CROs grow fastest

Pharmaceutical and biotechnology companies retained the dominant end-user position with approximately 42% of the transfection reagents and equipment market in 2025. The biopharmaceutical industry’s cell and gene therapy pipeline investment, the pharmaceutical R&D sector’s drug discovery transfection requirement, and the biotech industry’s protein production and cell line development transfection use collectively create the most commercially concentrated and highest-value transfection procurement category. Each major cell therapy programme creates manufacturing-scale transfection procurement whose GMP reagent and validated equipment specification creates above-research-grade commercial relationships whose per-unit value substantially exceeds academic procurement.

Contract research and development and manufacturing organisations are the fastest-growing end user because the biopharmaceutical industry’s progressive outsourcing of cell and gene therapy development and manufacturing to specialist CDMOs creates concentrated transfection procurement at organisations whose multiple programme service contracts create transfection reagent and equipment demand that compounds with the number of concurrent client programmes.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Transfection Reagents and Equipment Market Insights

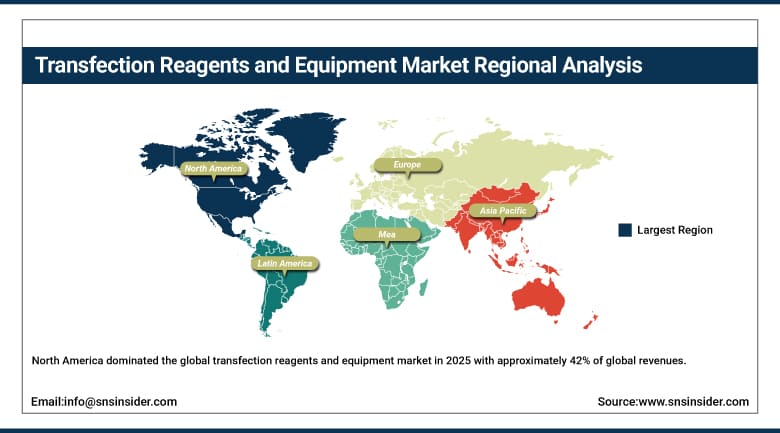

North America dominated the global transfection reagents and equipment market in 2025 with approximately 42% of global revenues. The United States accounts for approximately 87.4% of North American revenues through its extraordinary cell and gene therapy clinical pipeline, NIH-funded academic research infrastructure, Thermo Fisher Scientific, MaxCyte, Mirus Bio, and Promega’s commercial presence, and the CDMO sector’s cell therapy manufacturing capacity expansion.

Canada contributes approximately 12.6% of North American revenues through its active university biomedical research community, the National Research Council’s life sciences investment, and the growing Canadian biotech sector’s transfection reagent procurement for gene therapy and cell biology research programmes.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Transfection Reagents and Equipment Market Insights

Europe is a technically sophisticated transfection reagents and equipment market where the EMA’s gene therapy regulatory framework, Sartorius-Polyplus’ French commercial presence, Lonza’s Swiss cell therapy CDMO leadership, and EU Horizon research funding create a complete transfection technology ecosystem. Germany accounts for approximately 22.3% of European revenues through its strong pharmaceutical industry’s cell biology research, Max Planck and Helmholtz Institute academic research programmes, and the growing cell therapy CDMO sector’s manufacturing expansion.

The United Kingdom and France are significant secondary markets where the Francis Crick Institute, Institut Pasteur, and prominent gene therapy clinical programme development create consistent academic and clinical research transfection procurement. The UK’s Cell and Gene Therapy Catapult sustains structured transfection technology development and clinical-scale manufacturing investment.

Asia Pacific Transfection Reagents and Equipment Market Insights

Asia Pacific is the fastest-growing regional transfection reagents and equipment market, driven by China’s extraordinary cell therapy clinical programme expansion, Japan’s regenerative medicine regulatory framework enabling iPSC-based therapy development, South Korea’s biotech investment, and India’s rapidly growing pharmaceutical R&D sector. China accounts for approximately 44.8% of Asia Pacific revenues through its hundreds of registered CAR-T clinical trials, government biotech investment, and the domestic transfection reagent manufacturer development.

Japan’s iPSC research programme, whose Shinya Yamanaka’s Nobel Prize-winning technology creates consistent stem cell transfection demand, and South Korea’s Samsung Biologics and Celltrion’s cell therapy investment create significant secondary markets whose transfection procurement reflects the region’s advanced biotechnology capability.

MEA & Latin America Transfection Reagents and Equipment Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through its King Abdullah University of Science and Technology’s biomedical research investment, Vision 2030’s healthcare and biotech development, and the growing pharmaceutical manufacturing sector’s cell biology research. Brazil leads Latin American revenues at approximately 44.2% through its university biomedical research network, FAPESP and CNPq research funding, and the growing pharmaceutical and biotech industry’s transfection reagent procurement.

UAE’s biomedical research investment and South Africa’s academic research community represent significant MEA secondary markets whose transfection reagent procurement reflects growing life sciences research investment across the region.

Market Dynamics:

Growth Drivers: Gene therapy clinical programme expansion and mRNA therapeutic platform creating premium transfection reagent demand

Gene therapy clinical programme expansion is the transfection reagents and equipment market’s most commercially transformative growth driver. FDA approvals of Zolgensma for SMA, Hemgenix for haemophilia B, Casgevy for sickle cell disease and beta-thalassaemia, and multiple additional gene therapies in advanced clinical development collectively validate the commercial pathway whose downstream manufacturing scale-up creates GMP-grade transfection reagent and equipment procurement. Each new gene therapy IND application creates clinical-stage procurement that compounds with the growing programme portfolio, and each commercial approval creates manufacturing-scale demand whose recurring nature sustains long-duration supply relationships.

mRNA therapeutic platform expansion following COVID-19 mRNA vaccine’s commercial validation is creating the most commercially dynamic new transfection reagent demand category. Personalised cancer vaccines, therapeutic mRNA for protein replacement, and mRNA-based gene editing each require lipid nanoparticle transfection chemistry whose formulation is proprietary to specific mRNA therapeutic programmes creating commercially exclusive supply relationships. Each mRNA therapeutic that progresses from preclinical to clinical development creates transfection reagent procurement that grows proportionally with the programme’s clinical scale.

Restraints: High cost of GMP-grade reagents and transfection efficiency limitations for difficult cell types

GMP-grade transfection reagent cost creates procurement barriers for early-stage cell therapy developers whose clinical-stage budget constraints create motivation to delay GMP reagent transition until later-stage manufacturing requirements mandate it. Each GMP reagent qualification process that requires analytical testing, validation study investment, and regulatory documentation creates cost and timeline that research-grade reagent alternatives defer. The cost differential between research-grade and GMP-grade transfection reagents of 5-10 times creates procurement resistance that extends the research-grade market’s dominance over clinical-grade alternatives.

Transfection efficiency limitations for specific difficult-to-transfect cell types including primary neurons, haematopoietic stem cells, and certain T-cell subsets create application gaps whose resolution requires method optimisation investment that not all research programmes can allocate. Each cell type whose transfection efficiency with available reagents is inadequate for experimental or manufacturing requirements creates demand for novel reagent formulations or alternative physical delivery methods whose development investment adds cost and timeline to research programmes.

Opportunities: CAR-T electroporation scale-up and CRISPR therapeutic transfection platform development

CAR-T cell therapy manufacturing’s electroporation scale-up represents the most commercially certain near-term equipment growth opportunity whose clinical programme expansion creates defined manufacturing-scale electroporation procurement timelines. Each CAR-T therapy that advances from Phase I to Phase II clinical manufacturing creates electroporation equipment procurement whose scale increases proportionally with the manufacturing batch size required for trial patient enrolment. Each commercial CAR-T approval creates long-duration GMP electroporation equipment and consumable supply relationships whose multi-year operational commitment creates commercially predictable revenue.

CRISPR therapeutic transfection platform development represents the most commercially premium emerging opportunity whose high-efficiency nucleic acid delivery requirements for simultaneous guide RNA and Cas9 cargo create demand for next-generation transfection solutions beyond current lipofection and electroporation performance levels. Each new CRISPR therapeutic programme that achieves clinical proof of concept creates validation of its specific transfection platform whose commercial partnership with the programme’s developer creates above-research-grade commercial relationships whose premium reflects the therapeutic programme’s value.

Recent Developments:

-

2023: Sartorius acquired Polyplus for approximately USD 2.6 billion in April 2023, obtaining cutting-edge upstream technologies for cell and gene therapies including transfection, GMP-grade DNA and RNA delivery reagents, and plasmid DNA, reflecting the strategic value of proprietary transfection reagent technology in cell and gene therapy manufacturing.

-

2024: MaxCyte expanded its ExPERT electroporation platform in 2024 with new high-throughput configurations for clinical and commercial CAR-T cell manufacturing, enabling scalable ex vivo T-cell transfection from research to GMP clinical production without changing fundamental electroporation parameters.

-

2024: Thermo Fisher Scientific launched new Lipofectamine CRISPRMAX Plus reagent formulations in 2024, optimised for high-efficiency CRISPR-Cas9 ribonucleoprotein and mRNA delivery in difficult-to-transfect primary cells including haematopoietic progenitors and T-lymphocytes targeting the fastest-growing gene editing application segment.

Transfection Reagents and Equipment Market Key Players

-

Thermo Fisher Scientific Inc.

-

Promega Corporation

-

Qiagen N.V.

-

Bio-Rad Laboratories Inc.

-

MaxCyte Inc.

-

Lonza Group AG

-

Merck KGaA (Sigma-Aldrich)

-

Mirus Bio LLC

-

Polyplus (Sartorius)

-

OriGene Technologies Inc.

-

PerkinElmer Inc.

-

PromoCell GmbH

-

BTX Instruments

-

Agilent Technologies

-

Takara Bio Inc.

-

Eppendorf AG

-

Inovio Pharmaceuticals

-

OZ Biosciences

-

SignaGen Laboratories

-

Altogen Biosystems

Transfection Reagents and Equipment Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.71 Billion |

| Market Size by 2035 | USD 3.73 Billion |

| CAGR | CAGR of 8.04% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Product (Transfection Reagents, Transfection Equipment) • by Transfection Method (Lipid-Mediated/Chemical Transfection, Electroporation, Viral Transduction, Calcium Phosphate, Polymer-Based, Microinjection, Others) • by Application (Basic Research, Gene Therapy, Drug Discovery & Development, Protein Production, Cell Line Development, Vaccine Development, Others) • by End User (Pharmaceutical & Biotechnology Companies, Academic & Research Institutes, Contract Research Organizations/CROs, Hospitals & Clinical Laboratories, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Thermo Fisher Scientific Inc., Promega Corporation, Qiagen N.V., Bio-Rad Laboratories Inc., MaxCyte Inc., Lonza Group AG, Merck KGaA (Sigma-Aldrich), Mirus Bio LLC, Polyplus (Sartorius), OriGene Technologies Inc., PerkinElmer Inc., PromoCell GmbH, BTX Instruments, Agilent Technologies, Takara Bio Inc., Eppendorf AG, Inovio Pharmaceuticals, OZ Biosciences, SignaGen Laboratories, Altogen Biosystems |

Frequently Asked Questions

The Transfection Reagents and Equipment Market is expected to grow at a CAGR of 8.04% from 2026 to 2035.

The Transfection Reagents and Equipment Market was valued at USD 1.71 Billion in 2025.

Rising R&D expenditure by pharmaceutical and biotechnology companies in gene therapy clinical programmes requiring GMP-grade transfection reagents and equipment, and mRNA therapeutic platform expansion creating premium lipid nanoparticle transfection reagent demand from personalised medicine and RNA therapy programmes.

Transfection Reagents dominated the market with approximately 74% share in 2025, while the Transfection Equipment segment is the fastest growing.

North America dominated the Transfection Reagents and Equipment Market in 2025 with approximately 42% of global revenues, with the United States accounting for approximately 87.4% of North American revenues.

Get in Touch