Von Willebrand Disease Treatment Market Report Scope & Overview:

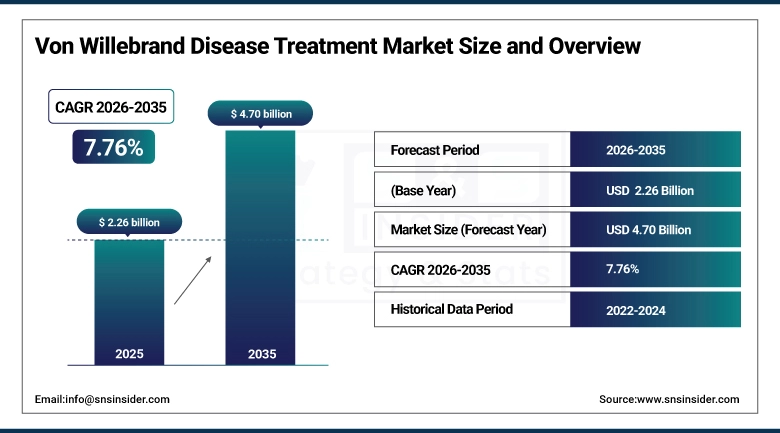

The Von Willebrand Disease Treatment Market was valued at USD 2.26 billion in 2025 and is expected to reach USD 4.70 billion by 2035, growing at a CAGR of 7.76% from 2026–2035.

The Von Willebrand Disease Treatment Market is witnessing steady growth driven by increasing diagnosis rates of hereditary bleeding disorders, expanding awareness programs, and improved access to specialized hematology care. Rising adoption of prophylactic treatment approaches and the shift toward targeted biologics are significantly enhancing patient outcomes. Advancements in recombinant von Willebrand factor (rVWF) therapies, improved plasma fractionation technologies, and extended half-life products are strengthening treatment efficacy while reducing dosing frequency.

Supporting this trend, the Centers for Disease Control and Prevention estimates that von Willebrand disease affects up to 1% of the global population, although only a fraction of cases are clinically diagnosed, indicating a substantial underdiagnosed patient pool

In addition, regulatory agencies such as the U.S. Food and Drug Administration continue to support innovation in rare bleeding disorder treatments. For instance, recombinant von Willebrand factor therapies like Vonvendi (developed by Takeda) have gained regulatory approvals and expanded indications in recent years, offering plasma-free alternatives with improved safety profiles

Von Willebrand Disease Treatment Market Size and Forecast

-

Market Size in 2025: USD 2.26 Billion

-

Market Size by 2035: USD 4.70 Billion

-

CAGR: 7.76% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Von Willebrand Disease Treatment Market - Request Free Sample Report

Von Willebrand Disease Treatment Market Trends

-

Increasing adoption of recombinant von Willebrand factor (rVWF) therapies is improving treatment safety, consistency, and reducing reliance on plasma-derived products.

-

Rising emphasis on early diagnosis and screening programs is expanding the identified patient population and accelerating treatment initiation rates.

-

Growing shift toward prophylactic treatment regimens is enhancing long-term bleeding control and reducing hospitalization rates.

-

Advancements in long-acting biologics and extended half-life therapies are improving dosing convenience and patient adherence.

-

Expanding adoption of home-based care and self-administration models is improving patient convenience and reducing healthcare system burden.

-

Increasing investment in rare disease research and orphan drug development is accelerating innovation in targeted treatment solutions.

-

Integration of digital health tools for bleeding episode tracking and therapy management is enhancing patient monitoring and treatment optimization.

-

Rising demand for personalized treatment approaches based on disease severity and patient profile is improving clinical outcomes.

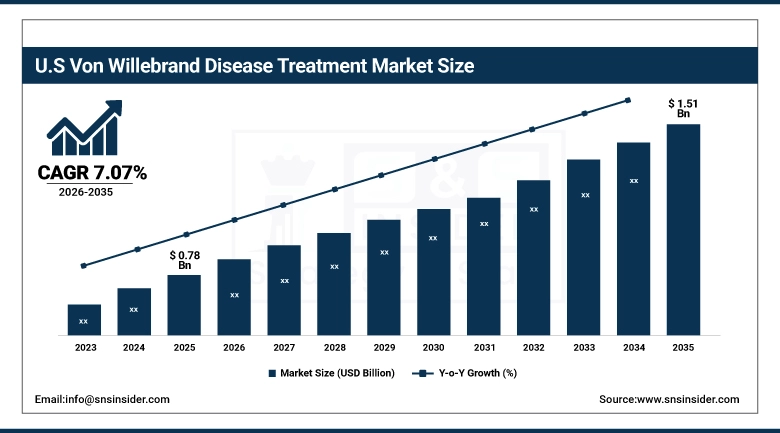

U.S. Von Willebrand Disease Treatment Market was valued at USD 0.78 billion in 2025 and is expected to reach USD 1.51 billion by 2035, growing at a CAGR of 7.07% from 2026–2035.

The U.S. Von Willebrand Disease Treatment Market leads globally, driven by advanced hematology care infrastructure, strong reimbursement support, and presence of key players such as Takeda Pharmaceutical Company, CSL Behring, and Grifols. Favorable policies from the Centers for Medicare & Medicaid Services continue to support access to high-cost biologics and prophylactic therapies.

Supporting this trend, the Centers for Disease Control and Prevention estimates that VWD affects up to 1% of the population, with increasing diagnosis rates expanding the treated patient base across the country.

In addition, the U.S. Food and Drug Administration continues to advance rare disease therapies; recombinant VWF products such as Vonvendi have seen continued clinical adoption and label expansions in recent years, while ongoing gene therapy trials are reinforcing the U.S. as a key innovation hub for next-generation bleeding disorder treatments.

Von Willebrand Disease Treatment Market Segment Highlights

-

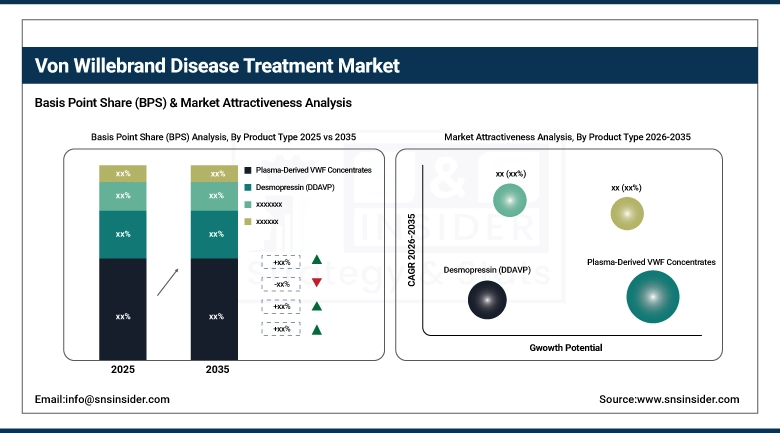

By Product Type, Plasma-Derived VWF Concentrates dominated the Von Willebrand Disease Treatment Market with 41.36% share in 2025; Recombinant VWF (rVWF) is fastest growing CAGR

-

By Disease Type, Type 1 VWD dominated the Von Willebrand Disease Treatment Market with 65.45% share in 2025; Type 2 VWD is fastest growing CAGR.

-

By Route of Administration, Intravenous dominated the Von Willebrand Disease Treatment Market with 72.45% share in 2025; Intranasal is fastest growing CAGR.

-

By End User, Hospitals dominated the Von Willebrand Disease Treatment Market with 56.24% share in 2025; Homecare Settings is fastest growing CAGR.

-

By Distribution Channel, Hospital Pharmacies dominated the Von Willebrand Disease Treatment Market with 60.11% share in 2025; Online Pharmacies is fastest growing CAGR

Von Willebrand Disease Treatment Market Segment Analysis

By Product Type, Plasma-Derived VWF Concentrates segment dominates the Von Willebrand Disease Treatment Market, Recombinant VWF (rVWF) segment expected to grow fastest

In 2025, the Plasma-Derived VWF Concentrates segment maintained its dominant position in the Von Willebrand Disease Treatment Market, accounting for 41.36% of total revenue. This segment includes plasma-derived factor replacement therapies that remain the clinical standard for managing moderate to severe VWD cases, particularly during surgical procedures and acute bleeding episodes.

From 2026 to 2035, the Recombinant VWF (rVWF) segment is projected to witness the fastest growth during the 2026–2035 forecast period. The move towards plasma-free therapies, which are safer, have lower risks of infection, and provide quality production, is becoming more common. The use of recombinant therapies, which enable precise dosage administration, is also gaining ground as a prophylactic therapy.

By Disease Type, Type 1 VWD segment dominates the Von Willebrand Disease Treatment Market, Type 2 VWD segment expected to grow fastest

The Type 1 VWD segment held the largest share of 65.45% in 2025, driven by its high prevalence as the most common and typically milder form of the disorder. Patients suffering from Type 1 VWD frequently have to undergo either irregular or low-frequency treatment procedures that can be achieved through the administration of either Desmopressin or Factor replacement treatments. With rising awareness, advanced diagnosis measures, and widespread screening initiatives, the patient base for this segment has greatly widened, reinforcing its dominance within the market.

The Type 2 VWD segment is projected to witness the fastest growth during the 2026–2035 forecast period. This growth is primarily attributed to the more complex nature of Type 2 variants, which often require specialized and consistent treatment approaches, including VWF concentrates and recombinant therapies.

By Route of Administration, Intravenous segment dominates the Von Willebrand Disease Treatment Market, Intranasal segment expected to grow fastest

The Intravenous segment accounted for the largest share of 72.45% in 2025, since most treatments for VWF deficiencies and more sophisticated biological drugs are given intravenously. Intravenous delivery will continue to be crucial when dealing with life-threatening bleeding events, as well as during surgery, where precise dosage and rapid drug action is critical.

The Intranasal segment is projected to witness the fastest growth, over the forecast period.

By End User, Hospitals segment dominates the Von Willebrand Disease Treatment Market, Homecare Settings segment expected to grow fastest

The Hospitals segment maintained the highest end-user share of approximately 56.24% in the Von Willebrand Disease Treatment Market in 2025. The reason behind this is that hospitals are considered the main venues where the treatment of moderate to severe cases of VWD, along with surgeries, emergencies, and IV VWF treatments, takes place. Hospitals have well-developed infrastructure for the field of hematology, as well as experts and expensive biologics for treating complicated cases.

The Homecare Settings segment is projected to register the highest CAGR during the 2026–2035 forecast period.

By Distribution Channel, Hospital Pharmacies segment dominates the Von Willebrand Disease Treatment Market, Online Pharmacies segment expected to grow fastest

The Hospital Pharmacies segment accounted for the largest share of approximately 60.11% in 2025, Since the majority of treatments for VWD include expensive biological products, which have to be carefully handled and distributed, the inclusion of hospital pharmacies becomes especially important when it comes to managing such medications during bleeding incidents or surgery. Such an inclusion makes it possible to manage stock efficiently and follow the requirements set by authorities, helping the segment maintain its leadership in the market.

The Online Pharmacies segment is anticipated to witness the fastest growth, with a CAGR over the forecast period.

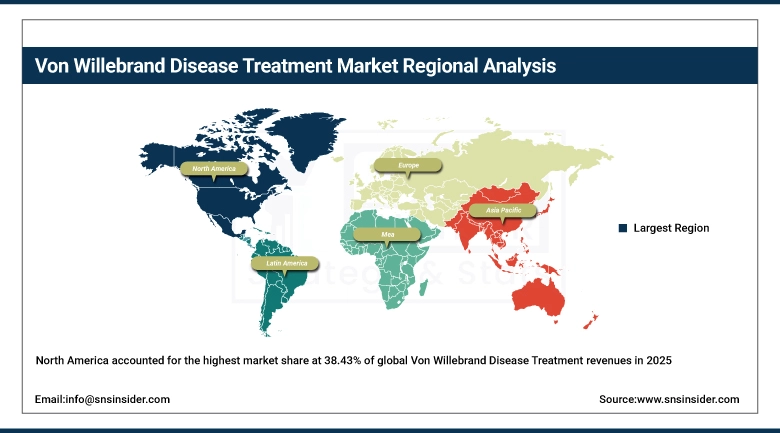

Von Willebrand Disease Treatment Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

38.43% |

|

Europe |

Germany |

30.14% |

|

Asia Pacific |

China |

23.75% |

|

Middle East & Africa |

UAE |

4.64% |

|

Latin America |

Brazil |

3.04% |

North America Von Willebrand Disease Treatment Market Insights

North America accounted for the highest market share at 38.43% of global Von Willebrand Disease Treatment revenues in 2025, owing to well-established healthcare infrastructure in hematology, high prevalence of diagnosis, and favorable reimbursement policies favoring biological treatments. The United States is the frontrunner among regional markets, attributable to the availability of facilities providing hemophilia-specific care and high adoption of recombinant and plasma-based medications.

Supporting this dominance, the Centers for Medicare & Medicaid Services continues to provide favorable reimbursement coverage for clotting factor therapies, enabling broader patient access to high-cost treatments. In addition, according to the Centers for Disease Control and Prevention, increasing screening initiatives and awareness programs are improving diagnosis rates across the country.

Recent developments include continued clinical adoption of recombinant VWF therapies such as Vonvendi, along with ongoing gene therapy trials in the U.S., reinforcing North America’s leadership in innovation and treatment accessibility.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Von Willebrand Disease Treatment Market Insights

The Asia Pacific is forecasted to grow at the fastest CAGR of 8.69% during the period 2026–2035 due to increased healthcare infrastructure, growing awareness regarding rare bleeding disorders, and increased availability of testing centers. The countries that will see growth within the Asia Pacific region include China, Japan, India, and South Korea, among which China contributes to the revenue generated due to its large population size.

Growth across the region is further supported by increasing government focus on rare disease management and expansion of plasma fractionation capabilities. Countries such as Japan and South Korea are witnessing higher adoption of advanced biologics due to strong reimbursement frameworks and developed healthcare systems, while India and China are experiencing rapid improvements in diagnosis rates and treatment accessibility.

Recent developments include increased investments in domestic plasma collection and fractionation infrastructure in China, along with Japan’s continued expansion of reimbursement support for rare disease therapies, accelerating regional market growth.

Europe Von Willebrand Disease Treatment Market Insights

Europe was the second-biggest market segment in the worldwide market, generating in revenues in 2025 due to the presence of highly developed healthcare infrastructure and availability of a large number of networks related to hemophilia care as well as strict regulatory measures. Germany, the UK, France, and Italy were among the leading nations, with extensive use of VWF treatments.

Supporting this position, the European Medicines Agency (EMA) continues to facilitate approvals for advanced biologics and orphan drugs, strengthening treatment availability across the region. Additionally, government-backed rare disease strategies and national patient registries are improving disease tracking and treatment outcomes.

Recent developments include increased funding under EU health programs for rare disease research and continued expansion of recombinant therapy adoption, reinforcing Europe’s position as a mature and innovation-driven market.

Middle East & Africa and Latin America Von Willebrand Disease Treatment Market Insights

The Middle East & Africa (MEA) and Latin America regions are witnessing steady growth in the Von Willebrand Disease Treatment Market, supported by improving healthcare infrastructure, rising awareness, and gradual expansion of access to specialized care. In the MEA region, countries such as Saudi Arabia, the UAE, and South Africa are leading adoption, driven by government-led healthcare modernization initiatives and increasing investment in rare disease management.

In Latin America, Brazil and Mexico represent the primary markets, supported by expanding public healthcare programs and improving availability of plasma-derived therapies. However, limited diagnosis rates and restricted access to advanced biologics continue to pose challenges in both regions.

Recent developments include national healthcare transformation programs in Saudi Arabia aimed at enhancing rare disease treatment access, and regulatory improvements in Brazil to streamline approval and distribution of biologic therapies, supporting gradual market expansion.

Von Willebrand Disease Treatment Market Growth Drivers:

-

Rising diagnosis rates and increasing awareness of bleeding disorders are driving global adoption of von Willebrand disease treatment

The increasing awareness regarding the underdiagnosis of Von Willebrand Disease is now becoming one of the key structural factors driving growth in the market. In the past, there were many instances where patients, especially those suffering from mild or moderate conditions, went undiagnosed owing to poor awareness levels and the absence of any routine screening processes. Nevertheless, things have started changing for the better.

Supporting this trend, the Centers for Disease Control and Prevention estimates that VWD affects up to 1% of the global population, yet only a fraction of individuals are clinically diagnosed, highlighting a substantial untapped treatment population.

In recent developments, healthcare systems across regions are strengthening rare disease frameworks and diagnostic infrastructure. For instance, the U.S. has expanded hemophilia treatment center networks and awareness programs, while several countries in Europe and Asia are investing in national rare disease registries and genetic testing capabilities.

Von Willebrand Disease Treatment Market Restraints:

-

High cost of biologic therapies and limited access in emerging markets creating significant barriers to treatment adoption

One of the most crucial factors that act as an impediment to the growth of this market is the cost of advanced treatments available for Von Willebrand Disease. The treatments like plasma derived von Willebrand factor concentrate or recombinant VWF treatment require a complicated process, strict quality controls and even cold chain transportation leading to high cost-per-patient of treatment. Such treatments are often needed throughout one’s life in case of moderate or severe Von Willebrand Disease.

Von Willebrand Disease Treatment Market Opportunities:

-

Advancing gene therapy and long-acting biologics creating transformative opportunities for durable and potentially curative treatment solutions

The future development of the market for Von Willebrand Disease Treatment will become more and more associated with new technological developments that seek to shift away from merely alleviating symptoms to modifying the course of the disease itself. Some of the promising new directions in gene therapy research include developing methods for providing patients with the ability to produce von Willebrand factor endogenously and thus avoiding injections and the constant dependence on medications for the rest of their lives. Another direction includes creating new long-half-life biologics.

Recent Developments:

-

2026: Takeda Pharmaceutical Company continued to expand global access to its recombinant von Willebrand factor therapy Vonvendi, with broader adoption across Europe and Asia-Pacific, alongside ongoing clinical programs evaluating its use in prophylactic treatment settings to reduce bleeding episode frequency.

-

2026: CSL Behring advanced its plasma-derived VWF portfolio with increased investment in plasma collection infrastructure and fractionation capacity expansion, aiming to strengthen global supply reliability and meet rising demand for bleeding disorder therapies.

-

2025: Grifols reported progress in expanding its plasma fractionation network and enhancing production efficiency for VWF concentrates, supporting improved availability of therapies across North America and Europe.

-

2025: Sanofi, through its rare disease pipeline initiatives, continued to advance clinical research in hematology and bleeding disorders, including exploration of next-generation biologics and extended half-life therapies aimed at improving long-term disease management.

Von Willebrand Disease Treatment Market Key Players

Some of the Von Willebrand Disease Treatment Market Companies

-

Takeda Pharmaceutical Company Limited

-

CSL Behring

-

Grifols S.A.

-

Octapharma AG

-

Sanofi S.A.

-

Novo Nordisk A/S

-

Kedrion S.p.A.

-

Bio Products Laboratory Ltd.

-

LFB Group

-

F. Hoffmann-La Roche Ltd.

-

Bayer AG

-

Pfizer Inc.

-

Shire (now part of Takeda)

-

Octapharma USA Inc.

-

China Biologic Products Holdings Inc.

-

Green Cross Corporation

-

SK Plasma Co. Ltd.

-

Biotest AG

-

Emergent BioSolutions Inc.

-

ADMA Biologics Inc.

Von Willebrand Disease Treatment Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.26 Billion |

| Market Size by 2035 | USD 4.70 Billion |

| CAGR | CAGR of 7.76% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Desmopressin (DDAVP), Plasma-Derived VWF Concentrates, Recombinant VWF (rVWF), Antifibrinolytics, Others) • By Disease Type (Type 1 VWD, Type 2 VWD, Type 3 VWD) • By Route of Administration (Intravenous, Intranasal, Oral, Others) • By End User (Hospitals, Specialty Clinics / Hemophilia Treatment Centers, Homecare Settings, Others) • By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Takeda Pharmaceutical Company Limited, CSL Behring, Grifols S.A., Octapharma AG, Sanofi S.A., Novo Nordisk A/S, Kedrion S.p.A., Bio Products Laboratory Ltd., LFB Group, F. Hoffmann-La Roche Ltd., Bayer AG, Pfizer Inc., Shire (now part of Takeda), Octapharma USA Inc., China Biologic Products Holdings Inc., Green Cross Corporation, SK Plasma Co. Ltd., Biotest AG, Emergent BioSolutions Inc., ADMA Biologics Inc. |

Get in Touch