Wafer Inspection System Market Report Scope & Overview:

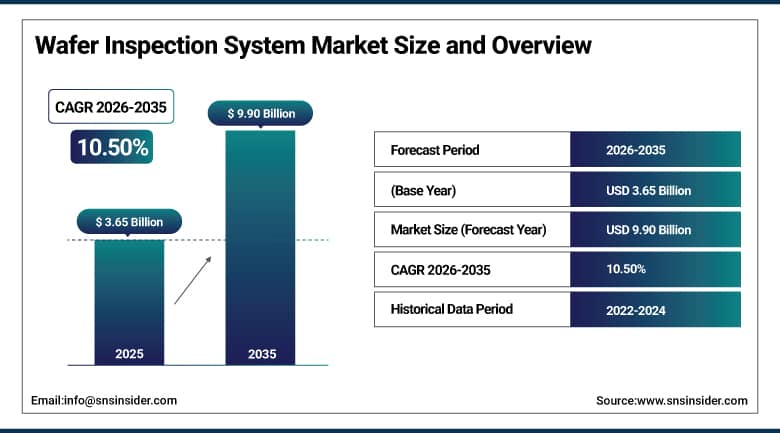

The Wafer Inspection System Market was valued at USD 3.65 Billion in 2025 and is expected to reach USD 9.90 Billion by 2035, growing at a CAGR of 10.50% from 2026 to 2035.

The Wafer Inspection System Market continues to expand as chipmakers push toward smaller process nodes, leaving progressively less room for undetected defects to slip through production. Fabs need tools capable of catching micro- and nano-level flaws long before a finished chip reaches a customer, since a single undetected defect at an advanced node can ruin an entire batch of otherwise expensive silicon. Artificial intelligence and machine learning are reshaping how quickly and accurately these systems can flag problems, rising adoption in MEMS, sensors, and advanced packaging is widening the addressable market well beyond traditional front-end fabrication, and heavy research and development investment paired with active mergers and acquisitions among leading players continues to keep competitive intensity high across the industry.

Applied Materials introduced its SEMVision H20 e-beam inspection system in February 2025, enhancing defect classification accuracy and throughput for advanced semiconductor nodes, while KLA launched its 3935 and 3920 EP broadband plasma defect inspection systems in April 2025, offering high sensitivity for logic and memory nodes at 5 nanometers and below.

Market Size and Forecast

-

Market Size in 2026E: USD 4.03 Billion

-

Market Size by 2035: USD 9.90 Billion

-

CAGR: 10.50% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Wafer Inspection System Market - Request Free Sample Report

Wafer Inspection System Market Trends

-

Adoption of AI, machine learning, and automation is enhancing defect detection accuracy and speeding up wafer inspections across fabs worldwide.

-

Rising demand for advanced nodes at 7nm, 5nm, and below is fueling investment in high-precision inspection systems.

-

Expansion of MEMS devices, sensors, and advanced packaging applications is opening new opportunities for wafer-level inspection.

-

Key players are increasing R&D spending and patent filings in next-generation inspection technologies to strengthen competitive positioning.

-

Asia Pacific leads with rapid fab expansions, while North America and Europe invest in domestic semiconductor supply chains.

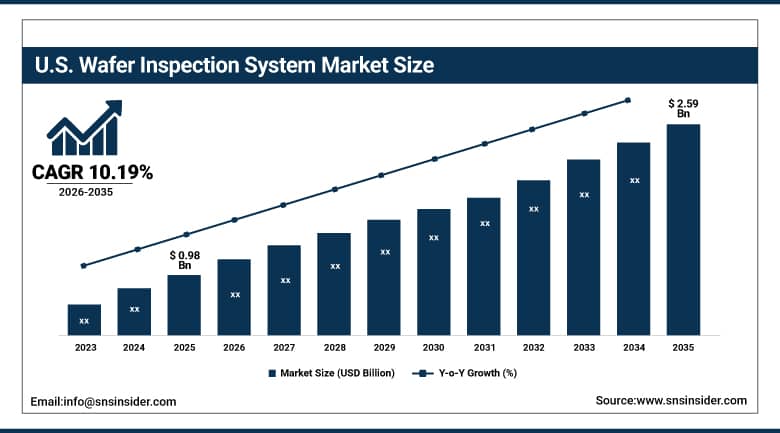

United States Wafer Inspection System Market Outlook

The United States Wafer Inspection System Market was valued at USD 0.98 Billion in 2025 and is expected to reach USD 2.59 Billion by 2035, growing at a CAGR of 10.19% from 2026 to 2035.

The U.S. dominated in terms of having the largest single national market for wafer inspection systems due to the increased investments in semiconductor manufacturing and local chip manufacturing as part of government strategies geared towards lowering dependence on offshore manufacturing facilities. The increased demands for nodes along with the increased spending on research and development of AI and automation enabled wafer inspection equipment by major American corporations fueled innovations in this market, and the growing use of MEMS, sensors, and advanced packaging increased America’s dominance.

ASML reached the “first light” stage of its High NA EUV lithography system in February 2024, an important step towards the manufacture of advanced nodes and with the application of this technology expected for the 14A generation of Intel chips.

Wafer Inspection System Market Segment Analysis

-

By Product, the optical wafer segment dominated the Wafer Inspection System Market with a 55.01% share in 2025, while the electron beam segment is the fastest growing.

-

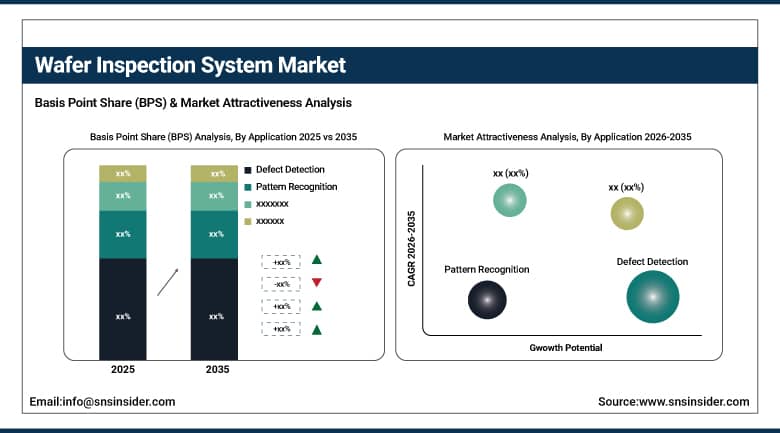

By Application, the defect detection segment dominated the Wafer Inspection System Market with a 60.24% share in 2025, while the pattern recognition segment is the fastest growing.

-

By Type, the wafer scanners segment dominated the Wafer Inspection System Market with a 58.32% share in 2025, while the wafer probers segment is the fastest growing.

-

By Technology, the front-end wafer segment dominated the Wafer Inspection System Market with a 62.10% share in 2025, while the back-end wafer segment is the fastest growing.

By Application, defect detection led the market, pattern recognition grew fastest

The defect detection segment dominated the Wafer Inspection System Market in 2025 with approximately 60.24% market share. Manufacturers' priority on identifying surface and sub-surface defects to improve yields and minimize manufacturing losses continued to reinforce this leadership position, keeping demand for inspection tools consistently strong across nearly every major fab worldwide.

The pattern recognition segment is projected to grow at the fastest CAGR during the forecast period. Increasing complexity of circuit designs at advanced nodes continues to drive this growth. Advanced algorithms and AI-powered solutions are increasingly deployed to identify lithography-related errors, enhancing process control and accuracy in ways manual or simpler automated review methods simply cannot match, a capability gap that continues to widen as chip designs grow more intricate.

By Product, optical wafer led the market, electron beam grew fastest

The optical wafer segment held the highest market share of around 55.01% in the Wafer Inspection System Market in 2025. The high popularity, efficiency, and effectiveness of the segment in offering quick and high-volume throughput defect detection in the manufacturing process of semiconductors were some key reasons for its dominance.

The electron beam segment is expected to grow at the highest CAGR in the forecast period. The growing need for enhanced accuracy more than what can be achieved by optical inspection alone, especially at the advanced node, has been the reason for the above trend. The capability of electron beam wafer inspection systems to achieve high resolution with the capacity to detect defects on the nano level has led to their growing acceptance for defect detection at the advanced node.

By Type, wafer scanners led the market, wafer probers grew fastest

The wafer scanners segment dominated the Wafer Inspection System Market in 2025 with approximately 58.32% market share. Its essential role in inspecting entire wafers with both speed and precision, combined with continuous technological enhancement improving throughput and defect coverage simultaneously, continued to make it integral to high-volume semiconductor manufacturing.

The wafer probers segment is projected to grow at the fastest CAGR during the forecast period. Rising demand for electrical testing and validation of wafers, especially at smaller, more complex nodes, continues to drive this growth. Probers provide critical data for device performance analysis that scanners alone cannot capture, and that expanding role across advanced semiconductor production continues to push prober adoption higher as chipmakers look for more complete validation coverage before wafers move further down the production line.

By Technology, front-end wafer led the market, back-end wafer grew fastest

The front-end wafer segment held the leading position in the Wafer Inspection System Market in 2025, holding about 62.10% market share due to its involvement in the crucial early manufacturing process in which precision is essential to avoid mistakes that are expensive to rectify later, especially in lithography and deposition where even the earliest detection of defects will help save an entire wafer from damage.

The back-end wafer segment is expected to witness the highest CAGR growth during the forecast period. The increasing demand for advanced packaging, MEMS, and heterogeneous integration has been fueling the demand for back-end inspection system segments. These technologies create truly innovative growth prospects and compel manufacturers to come up with innovative back-end inspection systems as packaging technology is increasingly becoming an important means of increasing chip performance.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

80.0% |

|

Europe |

Germany |

29.0% |

|

Asia Pacific |

Taiwan |

34.0% |

|

Middle East & Africa |

UAE |

27.0% |

|

Latin America |

Brazil |

39.0% |

North America Wafer Inspection System Market Insights

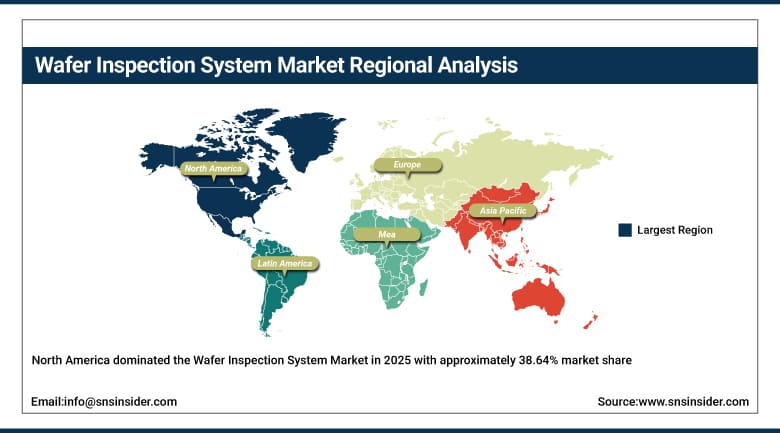

North America dominated the Wafer Inspection System Market in 2025 with approximately 38.64% market share, a leadership position driven by strong technological innovation and the presence of global semiconductor equipment leaders headquartered across the region. Government-backed programs including the CHIPS Act continued to drive fab expansion and local manufacturing growth, and demand was further reinforced by advanced R&D in AI-driven and automation-enabled inspection tools.

The United States accounted for roughly 80% of regional revenue, reflecting large-scale investment in semiconductor manufacturing and domestic chip production initiatives backed by federal policy. Leading companies headquartered in the United States continued to spearhead technological innovation in high-precision inspection, and Canada contributed a smaller but steadily growing share as its own semiconductor supply chain initiatives continued to develop.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Wafer Inspection System Market Insights

The Europe Wafer Inspection System market was driven through investments in the automotive, industrial electronics, and energy-efficient semiconductors industries. Germany, The Netherlands, and France all emerged as key players in promoting adoption in 2025, while the research-oriented nature of the region alongside its commitment to sustainability and next generation automotive semiconductors also contributed to growth, with European firms also making advancements in the field of optical and electron beam wafer inspections.

Germany emerged as the biggest driver of regional demand in 2025 with a share of about 29% of overall European revenues, with this being driven by the automotive and industrial electronics segments within the country. Innovation at semiconductor R&D centers and collaborations with suppliers ensured that rising investments in next generation automotive semiconductors increased demand further.

Asia Pacific Wafer Inspection System Market Insights

The Asia Pacific region witnessed high growth in terms of the market with a CAGR of around 11.26%, which is expected to continue throughout 2035 due to the presence of robust bases of semiconductor manufacturing facilities in Taiwan, South Korea, and Japan. The increasing demand for equipment on account of growing capacity and investments made in advanced technology nodes in the region was supplemented by government policies that supported the independence of the chip industry in the region.

The Chinese market for wafer inspection systems experienced an accelerated pace in 2025 owing to several government policies focused on building a semiconductor manufacturing base in China. Growing investments in fabs, packaging and foundry led to high demand for the inspection equipment, while Taiwan emerged as one of the key markets accounting for about 34% of the region’s total revenues because of the presence of advanced foundry facilities.

MEA & Latin America Wafer Inspection System Market Insights

The Wafer Inspection System Market experienced moderate growth across Latin America and the Middle East & Africa in 2025, driven by increasing interest in electronics manufacturing and government-led diversification strategies across both regions. Limited semiconductor infrastructure posed genuine adoption challenges that restricted large-scale deployment for now, though rising demand for consumer electronics and digitalization initiatives continued to create meaningful future potential, with the UAE accounting for roughly 27% of MEA revenue.

Latin America followed a broadly similar trajectory, with Brazil accounting for roughly 39% of regional revenue as its own electronics manufacturing sector continued to develop. Over time, both regions were expected to gradually emerge as more meaningful markets for wafer inspection solutions as semiconductor infrastructure investment continued to mature and domestic electronics manufacturing capacity expanded further.

Market Dynamics

Growth Drivers: Rising demand for advanced nodes and precision inspection

The Wafer Inspection System Market is driven by increasing adoption of advanced semiconductor nodes such as 7nm, 5nm, and beyond. As device complexity grows, the need for ultra-precise inspection technologies capable of identifying micro-level defects becomes genuinely critical to maintaining yield. This trend is further fueled by rising investment in semiconductor fabrication plants worldwide, all aimed at ensuring higher yield, better performance, and faster production cycles for next-generation electronics across every major chipmaking region.

A substantial share of inspection tools deployed globally now serve 5nm and 3nm nodes specifically, with sub-3nm defect capture accuracy reaching approximately 90% and fabs targeting yield rates around 97%. Global fab spending continues to fuel tool adoption at a rapid pace, while cycle times have fallen considerably, a combination of metrics that illustrates just how central inspection technology has become to modern semiconductor manufacturing economics.

Restraints: High equipment costs and complex integration challenges

Although there is immense potential for growth, wafer inspection systems also have some actual limitations, associated with their capital intensive nature and the fact that they require an extremely complicated installation process. It becomes difficult for small and medium size fabrication facilities to install the latest inspection system and this means that the technology is available to very few, large, well capitalized companies in the semiconductor industry, while small companies are forced to use old inspection techniques.

Maintenance issues, shortage of skilled labor force, and the time required to install the systems are some additional factors contributing to the existing difficulties, preventing the penetration of the market in emerging countries. Prices of parts of the systems are still high in comparison to past standards.

Opportunities: Expanding applications in MEMS, sensors, and advanced packaging

Beyond traditional semiconductor wafers, wafer inspection systems are finding significant opportunity in MEMS, sensors, and advanced packaging applications. The proliferation of IoT devices, autonomous vehicles, and wearable electronics continues to accelerate demand for precise inspection at the wafer level, and these emerging applications not only broaden the customer base for inspection vendors but also encourage genuine technological innovation across the industry as a whole.

MEMS and sensor applications continue to drive a growing share of new inspection demand, with wafer-level packaging inspections expanding rapidly as more vendors launch customized inspection tools built for these emerging applications. That shift toward specialized, application-specific inspection solutions is expected to keep opening new high-growth niches within the broader semiconductor ecosystem through 2035.

Recent Developments:

-

2024: Hitachi High-Tech Corporation launched the LS9300AD, a new system for inspecting the front and backside of non-patterned wafer surfaces for particles and defects, adding a Differential Interference Contrast inspection function to detect shallow, low-aspect microscopic defects.

-

2024: Merck acquired Unity-SC to bolster its semiconductor industry presence and expand its inspection and metrology portfolio, positioning the company to capture growing demand tied to artificial intelligence-driven chip production.

-

2023: Hitachi High-Tech Corporation launched the Hitachi Dark Field Wafer Defect Inspection System DI4600, improving throughput by approximately 20% through reduced wafer transfer time and enhanced data processing power for patterned wafer inspection.

Wafer Inspection System Market key players are:

-

Applied Materials, Inc.

-

KLA Corporation

-

ASML Holding N.V.

-

Pacific Technology

-

Teradyne Inc.

-

Nanda Technologies GmbH

-

Lam Research Corporation

-

Hitachi High-Tech Corporation

-

Hermes Microvision, Inc.

-

NXP Semiconductors

-

Synopsys, Inc.

-

Onto Innovation Inc.

-

Thermo Fisher Scientific Inc.

-

JEOL Ltd.

-

Nikon Metrology NV

-

Camtek Ltd.

-

Lasertec Corporation

-

Nova Ltd.

-

SCREEN Semiconductor Solutions Co., Ltd.

-

Veeco Instruments Inc.

Wafer Inspection System Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.65 Billion |

| Market Size by 2035 | USD 9.90 Billion |

| CAGR | CAGR of 10.50% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Product (Optical Wafer and Electron Beam) • by Application (Defect Detection and Pattern Recognition) • by Type (Wafer Scanners and Wafer Probers) • by Technology (Front-End Wafer and Back-End Wafer) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Applied Materials, Inc., KLA Corporation, ASML Holding N.V., Pacific Technology, Teradyne Inc., Nanda Technologies GmbH, Lam Research Corporation, Hitachi High-Tech Corporation, Hermes Microvision, Inc., NXP Semiconductors, Synopsys, Inc., Onto Innovation Inc., Thermo Fisher Scientific Inc., JEOL Ltd., Nikon Metrology NV, Camtek Ltd., Lasertec Corporation, Nova Ltd., SCREEN Semiconductor Solutions Co., Ltd., Veeco Instruments Inc. |

Frequently Asked Questions

The Wafer Inspection System Market is expected to grow at a CAGR of 10.50% from 2026 to 2035.

The Wafer Inspection System Market was valued at USD 3.65 Billion in 2025 and is projected to reach USD 9.90 Billion by 2035.

Growth is driven by rising demand for advanced semiconductor nodes and high-precision defect inspection to improve yield and manufacturing efficiency.

The front-end wafer segment dominated the Wafer Inspection System Market.

North America dominated the Wafer Inspection System Market in 2025.

Get in Touch