Connected Motorcycle Market Report Scope & Overview:

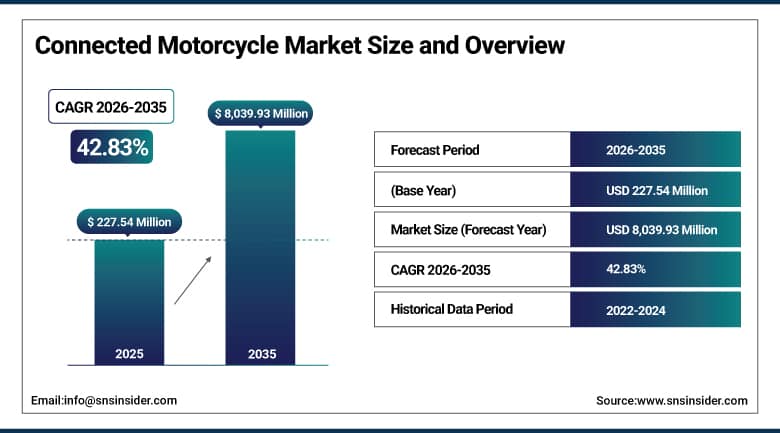

The Connected Motorcycle Market was valued at USD 227.54 Million in 2025 and is expected to reach USD 8,039.93 Million by 2035, growing at a CAGR of 42.83% from 2026–2035.

The global connected motorcycle market is at the beginning of an extraordinary growth trajectory driven by the convergence of mandatory safety regulations, electric motorcycle proliferation, and rider expectations for smartphone-equivalent digital experiences in two-wheeler platforms. Connected motorcycles integrate telematics control units, GPS, advanced rider assistance systems, cellular connectivity, and cloud-based diagnostics into the motorcycle architecture to deliver real-time safety alerts, predictive maintenance, navigation, infotainment, and emergency call capabilities. Governments across Japan, the EU, and India are progressively mandating emergency call systems and electronic stability control that require the connectivity infrastructure upon which broader feature suites are built. Motorcycle accidents account for approximately 28% of global road fatalities, creating a clear public safety imperative for connected safety technology adoption.

BMW Motorrad launched its ConnectedRide Cradle system upgrade in 2024, embedding native smartphone projection, real-time cloud diagnostics, and over-the-air software update capability across its R-series and GS platform lineup. The launch demonstrated BMW’s commercial strategy of using connectivity as a differentiating product feature and recurring service revenue platform, setting a competitive reference point that Honda, Ducati, and KTM are each developing equivalent integrated connectivity platforms to match across their premium motorcycle ranges.

Market Size and Forecast

-

Market Size in 2026E: USD 325.04 Million

-

Market Size by 2035: USD 8,039.93 Million

-

CAGR: 42.83% from 2026 to 2035

-

Fastest Growing Region: North America

-

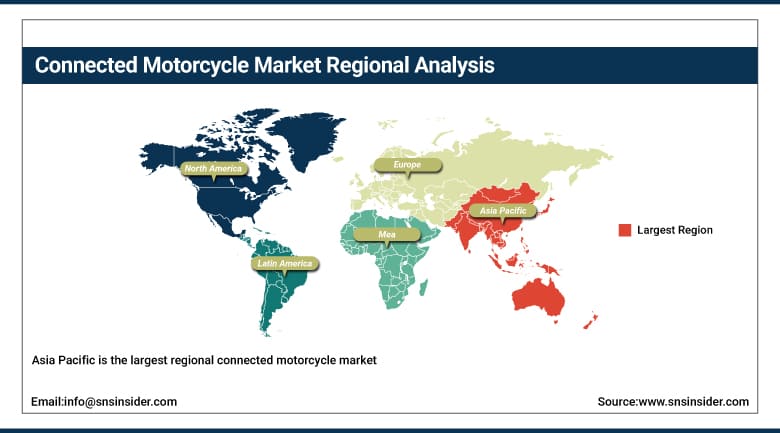

Largest Region: Asia Pacific'

To Get More Information On Connected Motorcycle Market - Request Free Sample Report

Connected Motorcycle Market Trends

-

Advanced rider assistance systems are transforming connected motorcycles into intelligent safety platforms with enhanced accident prevention capabilities.

-

Over-the-air software update infrastructure is enabling motorcycles to continuously improve digital features throughout vehicle ownership lifecycles.

-

Connected electric motorcycles and scooters are driving market growth through battery monitoring, charging optimization, and thermal management requirements.

-

Expanding 5G infrastructure is enabling real-time V2X communication for collision avoidance and smart traffic management applications.

-

Commercial delivery and logistics fleets are increasingly adopting connected motorcycles for telematics, predictive maintenance, and route optimization benefits.

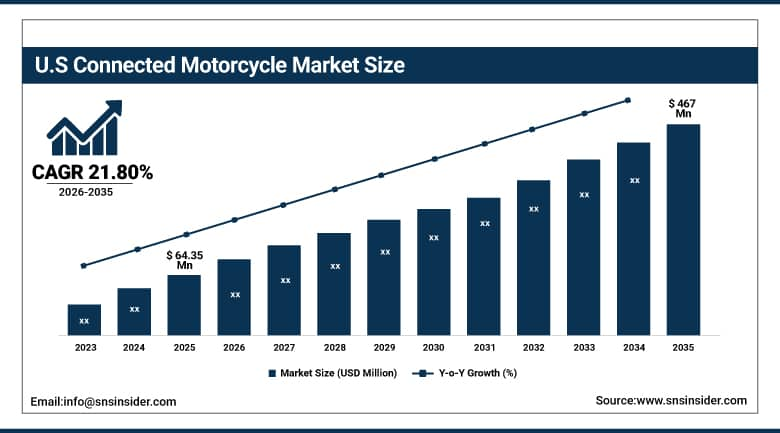

The U.S. Connected Motorcycle Market Outlook

The U.S. Connected Motorcycle Market was valued at approximately USD 64.35 Million in 2025 and is expected to reach approximately USD 467 Million by 2035, growing at a CAGR of approximately 21.80%.

The United States is the world’s leading premium motorcycle market and the commercial center of connected motorcycle technology development in North America. Harley-Davidson’s H-D Connect telematics system, which provides vehicle health monitoring, GPS tracking, and roadside assistance connectivity across its touring and cruiser lineup, represents the most commercially scaled connected motorcycle service programme in the U.S. market. Honda’s Honda Sensing for Motorcycles ARAS system is extending radar-based rider assistance from automotive into two-wheeler platforms, with the U.S. market targeted as a primary launch geography given its premium motorcycle consumer base’s demonstrated willingness to pay for advanced safety technology. Federal Highway Administration smart mobility investment programmes and NHTSA’s motorcycle safety initiatives are simultaneously creating regulatory and funding infrastructure that supports connected motorcycle technology deployment.

Harley-Davidson expanded its H-D Connect subscription service in 2025, adding real-time GPS vehicle tracking, remote diagnostics, battery monitoring, and roadside assistance notifications as standard features across all new Touring models. The expansion demonstrates the commercial viability of recurring subscription revenue models in premium motorcycle connectivity, where consumer willingness to pay for service beyond the initial vehicle purchase creates a durable aftermarket revenue stream that is independent of new motorcycle sales volumes.

Connected Motorcycle Market Segment Analysis

-

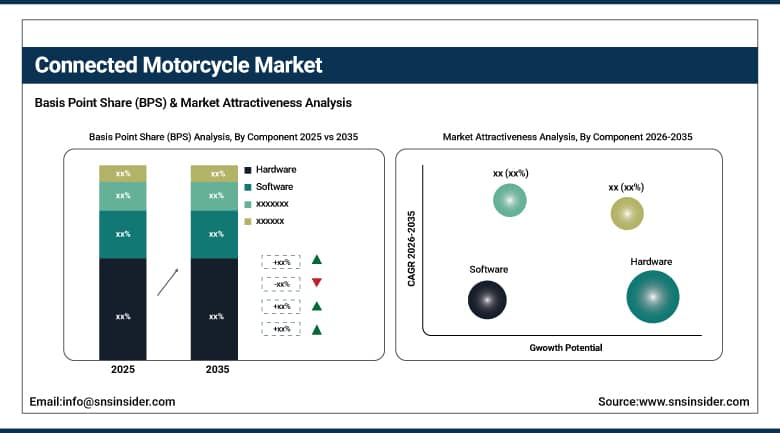

By Component, the hardware segment dominated the connected motorcycle market with 64.8% share in 2025, while the software segment is the fastest growing as OEM digital platform investment and subscription-based service models accelerate during 2026–2035.

-

By Connectivity, the cellular/LTE segment dominated the connected motorcycle market in 2025, while the 5G segment is the fastest growing during 2026–2035.

-

By Application, the infotainment segment dominated the connected motorcycle market with 34.31% share in 2025, while the vehicle health & diagnostics segment is the fastest growing during 2026–2035.

-

By Vehicle Type, the sports bikes segment dominated the connected motorcycle market in 2025, while the electric motorcycles & scooters segment is the fastest growing during 2026–2035.

By Component, hardware dominates, software grows fastest

Hardware retained the dominant component position with 64.8% of the connected motorcycle market in 2025. Telematics control units, GPS receivers, cellular modems, GNSS antennas, accelerometers, and ARAS sensor arrays collectively constitute the physical connectivity infrastructure whose procurement value per vehicle forms the commercial foundation of every connected motorcycle programme. Each new connected motorcycle model requires a defined hardware configuration whose cost is amortized across the vehicle’s purchase price and service programme. OEM investment in miniaturized, low-power TCUs and sensor integration that avoids adding weight or requiring separate battery systems has been the key engineering challenge whose resolution is enabling hardware connectivity to scale from premium flagships into mid-range motorcycle segments without cost-prohibitive per-unit hardware bills.

Software is the fastest-growing component because the commercial logic of software-as-a-service in connected motorcycles creates recurring revenue opportunities that fundamentally change the OEM’s business model. A motorcycle sold once generates a single revenue event. A connected motorcycle with an active subscription service generates annual recurring revenue whose lifetime value over a typical ownership period of 5 to 10 years can substantially exceed the profit contribution of the initial vehicle sale. BMW Motorrad’s ConnectedRide, Harley-Davidson’s H-D Connect, and Ducati’s Ducati Connect are each building software service ecosystems whose features, subscription pricing, and customer engagement model are being refined toward the recurring revenue economics that automotive connected service programmes have demonstrated across Toyota, BMW, and Tesla platforms.

By Application, infotainment dominates, vehicle health & diagnostics grows fastest

Infotainment retained the dominant application position with 34.31% of the connected motorcycle market in 2025. Navigation, smartphone projection, turn-by-turn routing, music streaming, call management, and rider community integration collectively define the infotainment suite whose consumer-facing appeal drives the most immediate and visible connected motorcycle value proposition for the premium rider demographic that defines the market’s current commercial heartland. European premium motorcycle OEMs including BMW Motorrad, Ducati, and KTM have built their connected motorcycle commercial narratives primarily around infotainment capability whose smartphone-mirroring and navigation features create a compelling product differentiation story in segments where technical performance differences between competing models are increasingly narrow.

Vehicle health and diagnostics is the fastest-growing application segment because the electrification of motorcycles has transformed diagnostics from a convenience feature into an operational necessity. Battery state-of-health monitoring, thermal management alerts, charging cycle optimisation, and range estimation accuracy are all mission-critical functions for electric motorcycle and scooter operators whose vehicle utility depends on reliable battery status information that connected diagnostics delivers continuously rather than through periodic service centre visits. Every EV motorcycle platform deployed globally creates a connected diagnostics requirement. As Asia Pacific’s massive electric scooter deployment programme scales toward hundreds of millions of units, the aggregate diagnostics connectivity demand it generates will progressively dwarf the premium European and North American motorcycle infotainment market that currently defines the segment’s commercial focus.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

28.4% |

|

Asia Pacific |

China |

54.6% |

|

Middle East & Africa |

UAE |

32.1% |

|

Latin America |

Brazil |

44.2% |

Asia Pacific Connected Motorcycle Market Insights

Asia Pacific is the largest regional connected motorcycle market, driven by the world’s highest two-wheeler population density, the most extensive electric scooter and motorcycle deployment programme, and government smart mobility investment across China, India, Japan, South Korea, and Southeast Asia. China accounts for approximately 54.6% of Asia Pacific revenues through its extraordinary combination of the world’s largest electric two-wheeler fleet, government mandates for smart transportation integration, and domestic connected motorcycle technology development by companies including NIU Technologies and Ather Energy whose EV platforms embed connectivity as standard architecture.

India represents the most commercially dynamic emerging market within Asia Pacific, where the government’s FAME II and PM E-Drive electric vehicle incentive programmes are accelerating electric two-wheeler adoption at a pace that is creating proportional connected telematics demand. Indian EV manufacturers including Ather Energy, Ola Electric, and TVS Motor Company are building connectivity as a standard feature in their electric scooter platforms, creating a connected motorcycle installed base that is growing at an extraordinary rate relative to the premium European market that historically defined the segment.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Connected Motorcycle Market Insights

North America is the fastest-growing regional connected motorcycle market, with the United States accounting for approximately 87.4% of North American revenues. The region’s above-average growth rate reflects the premium motorcycle consumer’s demonstrated willingness to pay for advanced connected features, the strength of Harley-Davidson’s connected service programme that has created a reference subscription model for the North American market, and the progressive introduction of Honda ARAS and BMW ConnectedRide systems that are elevating safety connectivity from optional accessory to standard specification across premium platforms. U.S. NHTSA motorcycle safety research investment and state-level smart mobility programme funding create regulatory and institutional motivation for connected motorcycle technology adoption.

Canada contributes approximately 12.6% of North American revenues through its premium motorcycle market, growing electric two-wheeler adoption in major urban centres, and the connectivity investment of Canadian delivery and logistics operators deploying connected motorcycle fleets for urban last-mile delivery services whose telematics requirements sustain commercial fleet connectivity demand independent of consumer market trends.

Europe Connected Motorcycle Market Insights

Europe is a technically sophisticated connected motorcycle market where EU mandatory eCall emergency call system requirements for two-wheelers and UNECE vehicle cybersecurity regulation UN R155 are creating compliance-driven connectivity infrastructure deployment across all new motorcycle models sold in European markets. Germany accounts for approximately 28.4% of European revenues as the region’s largest motorcycle market by value and the home market of BMW Motorrad whose ConnectedRide ecosystem is the most technically advanced integrated connectivity platform of any motorcycle OEM globally. The EU’s road safety policy framework targeting zero road deaths by 2050 creates a sustained political and regulatory motivation for connected safety technology mandates that progressively expand the scope of required connectivity beyond emergency call into ARAS and V2X communication.

The United Kingdom, Italy, and France are significant secondary European markets where premium motorcycle culture, strong dealer network connectivity service infrastructure, and the commercial presence of Ducati, Triumph, and Piaggio generate consistent demand for premium connected features. Italy’s Ducati Connect platform and Piaggio’s MyPiaggio connected service represent European mid-market connectivity approaches whose commercial development is demonstrating that subscription connectivity services can generate meaningful recurring revenue at scooter and lower-premium motorcycle price points below the BMW and KTM flagship tiers where connectivity was first commercially established.

MEA & Latin America Connected Motorcycle Market Insights

The Middle East and Africa and Latin America are growing connected motorcycle markets where rising premium motorcycle adoption, expanding electric two-wheeler deployment, and fleet telematics investment in last-mile delivery operations are creating structured demand for connected motorcycle technology. UAE leads MEA revenues at approximately 32.1% of the regional total through Dubai’s smart city investment, the premium motorcycle consumer market’s appetite for technology-laden vehicles, and the growing adoption of connected electric scooters in UAE’s expanding shared mobility and delivery fleet operations.

Brazil leads Latin American revenues at approximately 44.2% of the regional total through its large and commercially active motorcycle market, where delivery platforms including iFood and Rappi are deploying large connected motorcycle fleets whose telematics requirements create professional-grade connectivity demand at commercial scale. Brazil’s delivery motorcycle fleet represents one of Latin America’s most commercially significant connected motorcycle demand pools, as the platform economy’s growth is creating consistent procurement of GPS tracking, route optimization, and driver behavior monitoring systems across the country’s extensive motoboy delivery network.

Market Dynamics

Growth Drivers: Mandatory safety regulation requiring connectivity infrastructure and electric motorcycle proliferation creating technical diagnostic connectivity requirements

Mandatory safety regulation is the most structurally certain growth driver in the connected motorcycle market. The EU’s progressive eCall mandate extension toward two-wheelers, UNECE cybersecurity standards requiring secure vehicle connectivity architecture, and India’s FAME electric vehicle programme requirements collectively create regulatory demand floors that OEMs must satisfy with connectivity investment regardless of consumer feature demand. Each compliance-driven connectivity installation provides the hardware and communication infrastructure upon which infotainment, diagnostics, and ARAS software services are progressively added, creating an expanding per-vehicle connected feature value stack.

Electric motorcycle proliferation creates a fundamentally different connectivity demand dynamic than regulatory compliance. Battery health monitoring, charging management, thermal protection, and range calculation are each operational requirements for EV usability whose failure creates stranded vehicle risk that conventional motorcycle mechanical failure does not. This operational dependency makes connectivity infrastructure investment non-negotiable for EV OEMs whose vehicle reliability reputation depends on continuous diagnostic monitoring. The subscription service revenue potential simultaneously motivates OEM connectivity investment by creating a financially compelling recurring revenue pathway that transforms the motorcycle business model.

Restraints: High system cost limiting connectivity penetration in price-sensitive mass-market segments and data security and cybersecurity concerns in vehicle connectivity architecture

Cost remains the most significant barrier to connected motorcycle adoption beyond the premium segment. Telematics control units, cellular modems, GPS receivers, and ARAS sensor arrays add USD 200 to USD 800 per vehicle in hardware cost depending on feature scope. This cost addition is commercially viable at USD 10,000-plus premium motorcycle price points but economically challenging in the USD 2,000 to USD 5,000 mass-market two-wheeler segment that represents the majority of global motorcycle production volume. OEMs are actively addressing this through modular connectivity architectures and smartphone-tethering approaches that leverage the rider’s existing device as connectivity infrastructure.

Cybersecurity vulnerabilities in connected vehicle systems create both regulatory compliance obligations under UNECE R155 and reputational risk for OEMs whose connectivity platforms are exposed to remote exploitation. Motorcycle connectivity systems that enable remote vehicle tracking, remote diagnostics access, and potentially remote command functions create an attack surface that did not exist in mechanical motorcycles. The investment required to develop and maintain cybersecurity-compliant connectivity architecture raises the engineering cost of connected motorcycle programmes beyond what smaller OEMs can absorb without external technology partnership support.

Opportunities: V2X infrastructure integration creating new safety capability, fleet telematics commercial market growth, and aftermarket retrofit connectivity creating installed base expansion beyond new vehicle sales

V2X communication integration represents the most commercially transformative near-term capability expansion for connected motorcycles. When connected motorcycles exchange position, speed, and hazard information with other vehicles and smart road infrastructure in real time, the resulting situational awareness improvements address the most critical safety gap in motorcycle operation: the challenge of detecting hazards that are outside the rider’s direct field of vision. The commercial value of this capability, quantifiable in accident prevention outcomes whose insurance and human cost is precisely documented in road safety statistics, creates a compelling ROI case for both OEM feature investment and government infrastructure funding.

Fleet telematics represents the most immediately addressable commercial market expansion opportunity in the connected motorcycle sector. Delivery platform operators, motorcycle taxi services, and corporate fleet owners already operate at the scale where telematics investment generates measurable operational cost savings through route optimization, fuel consumption reduction, driver behavior improvement, and predictive maintenance cost avoidance. These commercial operators do not require consumer adoption motivation; they require commercially proven telematics solutions whose performance data from comparable fleet deployments validates the investment return that procurement teams need to approve fleet connectivity programmes.

Recent Developments:

-

2025: Harley-Davidson expanded its H-D Connect subscription service in 2025, adding real-time GPS vehicle tracking, remote diagnostics, battery monitoring, and roadside assistance notifications as standard features across all new Touring models, demonstrating the commercial viability of premium connected motorcycle subscription services in the North American market.

-

2024: BMW Motorrad launched its upgraded ConnectedRide Cradle system across its R-series and GS motorcycle lineup in 2024, integrating native smartphone projection, real-time cloud diagnostics, and over-the-air software update capability that enables BMW to continuously add connected features to existing customer vehicles without requiring hardware replacement or dealership service visits.

-

2024: Honda announced the commercial development of its Honda Sensing for Motorcycles advanced rider assistance system in 2024, incorporating radar-based adaptive cruise control, collision mitigation braking, and blind spot warning that extends Honda’s automotive ADAS expertise into two-wheeler platforms for premium motorcycle models targeting North American and European markets.

Connected Motorcycle Market key players are:

-

Honda Motor Co., Ltd.

-

Yamaha Motor Co., Ltd.

-

BMW Motorrad (BMW AG)

-

Ducati Motor Holding S.p.A. (Volkswagen Group)

-

Harley-Davidson Inc.

-

Robert Bosch GmbH

-

Continental AG

-

KTM AG

-

Kawasaki Heavy Industries Ltd.

-

Suzuki Motor Corporation

-

Triumph Motorcycles Ltd.

-

Piaggio & C. S.p.A.

-

Zero Motorcycles Inc.

-

Ather Energy Pvt. Ltd.

-

NIU Technologies

-

TVS Motor Company Ltd.

-

Hero MotoCorp Ltd.

-

Bajaj Auto Ltd.

-

DENSO Corporation

-

Harman International (Samsung)

Connected Motorcycle Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 227.54 Million |

| Market Size by 2035 | USD 8,039.93 Million |

| CAGR | CAGR of 42.83% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Hardware, Software, Services) • By Connectivity (Cellular/LTE, 5G, Wi-Fi/DSRC, Bluetooth, Others) • By Application (Infotainment, Vehicle Health & Diagnostics, Safety & Security, Navigation, Others) • By Vehicle Type (Sports Bikes, Cruisers, Touring, Scooters, Electric Motorcycles/Scooters) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Honda Motor Co., Ltd., Yamaha Motor Co., Ltd., BMW Motorrad (BMW AG), Ducati Motor Holding S.p.A. (Volkswagen Group), Harley-Davidson Inc., Robert Bosch GmbH, Continental AG, KTM AG, Kawasaki Heavy Industries Ltd., Suzuki Motor Corporation, Triumph Motorcycles Ltd., Piaggio & C. S.p.A., Zero Motorcycles Inc., Ather Energy Pvt. Ltd., NIU Technologies, TVS Motor Company Ltd., Hero MotoCorp Ltd., Bajaj Auto Ltd., DENSO Corporation, Harman International (Samsung) |

Frequently Asked Questions

Asia Pacific dominated the connected motorcycle Market in 2025.

Hardware dominated the connected motorcycle market with 64.8% share in 2025.

Mandatory safety regulations requiring connectivity infrastructure in new motorcycle models.

The connected motorcycle market was valued at USD 227.54 Million in 2025.

The connected motorcycle market is expected to grow at a CAGR of 42.83% from 2026 to 2035.

Get in Touch