Cryocooler Market Report Scope & Overview:

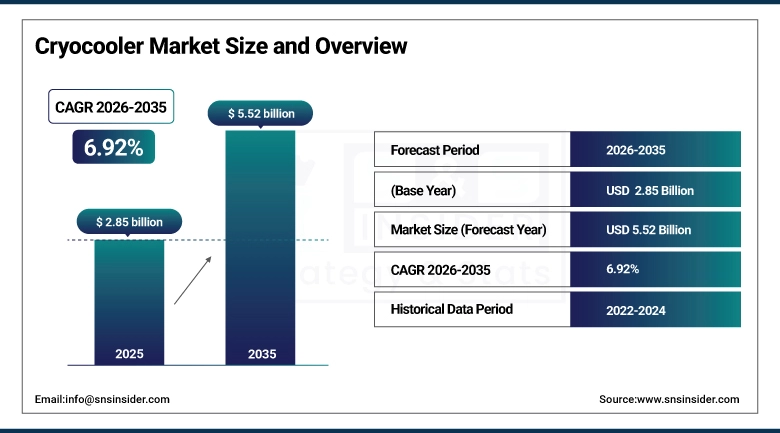

The Cryocooler Market size was valued at USD 2.85 billion in 2025 and is expected to reach USD 5.52 billion by 2035, growing at a CAGR of 6.92% from 2026-2035.

Cryocooler Market is expected to witness growth owing to increasing demand for ultra-low temperature coolers used in various applications such as space exploration, defense technology, superconducting electronics, and medical imaging devices. The increased launch of satellites, increased use of infrared cameras, and the development in quantum computing technology are some of the factors fueling demand for cryocoolers around the globe.

The National Institute of Standards and Technology documents that quantum computing's scaling from current demonstration systems of 100-1,000 physical qubits toward commercially useful systems of 1 million+ qubits will require proportional cryocooling capacity expansion whose infrastructure investment is creating a new industrial cryocooler market segment growing faster than any established application.

Cryocooler Market Size and Forecast

-

Market Size in 2025: USD 2.85 Billion

-

Market Size by 2035: USD 5.52 Billion

-

CAGR: 6.92% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Cryocooler Market - Request Free Sample Report

Cryocooler Market Trends

-

Quantum computing cryocooler demand is emerging as the fastest-growing new application segment where dilution refrigerators and sub-4K cryostats capable of cooling superconducting qubit chips are transitioning from laboratory research equipment into production infrastructure at IBM, Google, and IonQ data centers.

-

Pulse tube cryocooler adoption is growing in applications requiring vibration-free cooling satellite instruments, atomic clocks, and precision metrology instruments where moving displacer mechanical vibration from Stirling and Gifford-McMahon cryocoolers compromises sensor performance.

-

Miniaturization of Stirling cryocoolers for portable medical and defense applications where linear drive Stirling cryocoolers under 500 grams provide 200-500mW cooling at 77K in handheld infrared cameras and portable cryosurgery devices is expanding the addressable market beyond fixed installations.

-

Helium-free cryocooler development driven by chronic global liquid helium supply constraints and price volatility is accelerating adoption of cryocooler-based helium recondensation systems on MRI magnets and laboratory cryostats that previously vented helium to atmosphere.

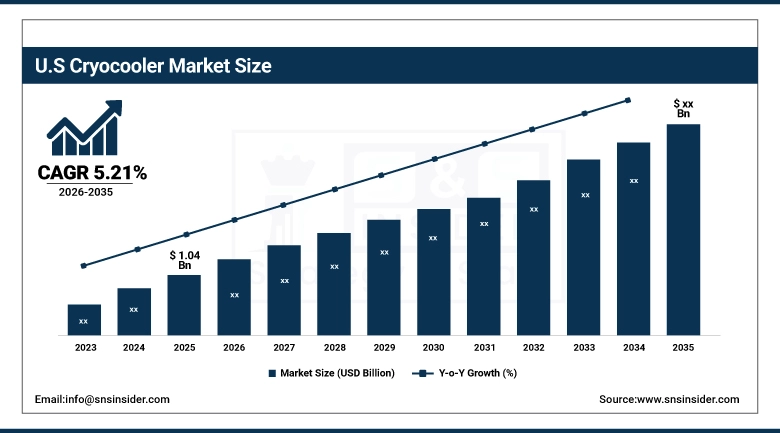

U.S. Cryocooler Market Size Outlook:

The U.S. Cryocooler Market was valued at approximately USD 1.04 billion in 2025 and is expected to grow at a CAGR of 5.21% from 2026-2035. This market is experiencing growth due to various initiatives undertaken towards modernizing defense technology and space exploration projects by NASA as well as other companies. Growing demand for superior infrared sensors and superconductors is adding to the growth witnessed by this market.

Lockheed Martin's cryocooler procurement for its F-35 Lightning II's AN/AAQ-40 Electro-Optical Targeting System and F-22 Raptor sensor cooling represents the largest single U.S. defense cryocooler application by production volume with each tactical aircraft requiring multiple high-reliability Stirling cryocoolers whose 10,000+ hour mean time between failures are validated by U.S. military environmental testing standards.

Cryocooler Market Segment Analysis

-

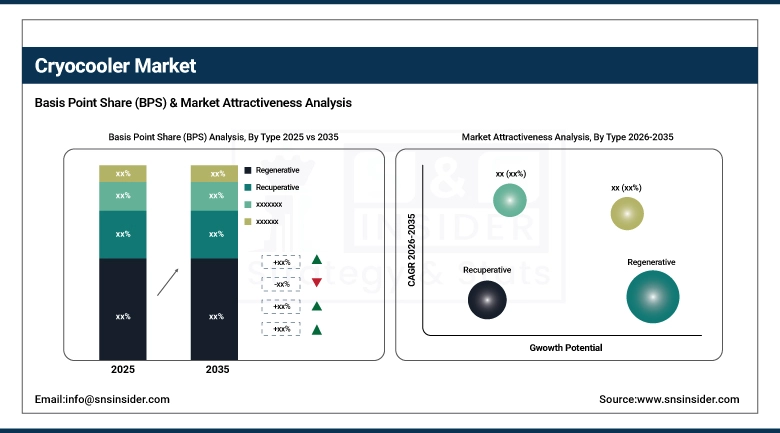

By Type, Regenerative cryocoolers dominated with 56.6% share in 2025; Recuperative cryocoolers growing at the fastest CAGR.

-

By End Use, Military & Defense dominated with 20.5% share in 2025; Healthcare growing at the fastest CAGR.

By Type: Regenerative dominates at 56.6%, Recuperative fastest CAGR

Regenerative cryocoolers held 56.6% of the Cryocooler Industry in 2025, encompassing the Stirling, Gifford-McMahon, and pulse tube designs that use regenerative heat exchangers to achieve the deep cryogenic temperatures required for the market's largest applications. The Stirling cryocooler whose opposed piston design compresses and expands working gas across a regenerator to achieve 77K cooling in portable configurations and below 40K in two-stage configurations is the dominant regenerative design for defense and space applications where compact size and lightweight are primary selection criteria. The Gifford-McMahon design which uses a motorized valve and displacer assembly driven by a separate helium compressor is the standard architecture for laboratory cryostats, MRI magnet recondensation, and industrial helium liquefaction where the displacer mechanism's serviceability advantage outweighs its vibration and acoustic noise disadvantages versus pulse tube alternatives.

Stirling cryocoolers within the regenerative category are growing at the fastest CAGR, driven by portable application adoption handheld thermal cameras, compact cryosurgery systems, and small satellite thermal management where Stirling's superior efficiency at 77-120K and compact linear drive configuration provide specific cooling power advantages that alternative cryocooler designs cannot match at equivalent size and weight constraints. Recuperative cryocoolers Joule-Thomson and Brayton cycle systems using recuperative heat exchangers are growing at the fastest overall type CAGR, driven by their adoption in low-vibration scientific instrument cooling and distributed LNG production where their continuous flow architecture eliminates the vibration of reciprocating machine designs.

By End Use: Military & Defense dominates, Healthcare fastest CAGR

Military and Defense held 20.5% of the Cryocooler Market in 2025, reflecting the defense sector's long-established role as the primary driver of cryocooler technology development and procurement. Infrared sensor cooling where tactical missile seekers, targeting cameras, and surveillance sensors require 77K operating temperatures for the quantum well photodetector materials whose fundamental detection sensitivity is only achievable in the cryogenic regime sustains the largest volume defense cryocooler procurement program globally. Electronic warfare systems, satellite sensors, and directed energy weapon cooling are each additional defense procurement categories whose aggregate demand sustains the defense segment's market leadership. Healthcare is growing at the fastest end-use CAGR, driven by MRI system cryocooler adoption both new system installations in emerging markets and helium recondensation cryocooler retrofits on the large installed MRI base and the growing commercial adoption of cryosurgery for prostate cancer, uterine fibroid, and dermatological applications.

Cryocooler Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

88% |

|

Europe |

Germany |

28% |

|

Asia Pacific |

China |

40% |

|

Middle East & Africa |

Israel |

42% |

|

Latin America |

Brazil |

48% |

North America Cryocooler Market Insights

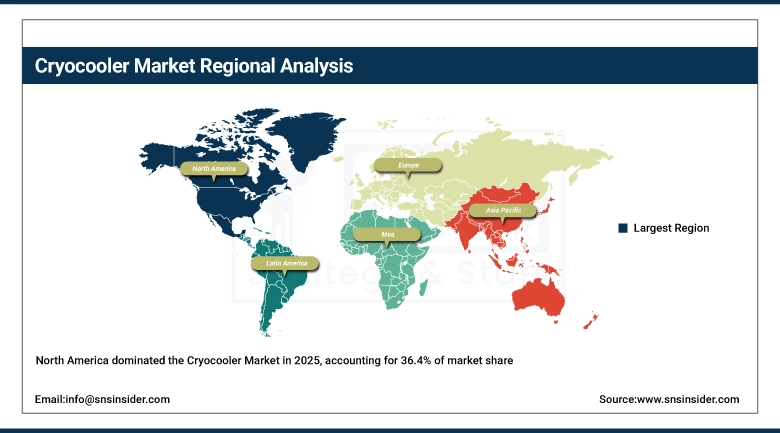

North America dominated the global Cryocooler Market with approximately 36.4% revenue share in 2025, sustained by the United States' defense procurement scale, the growing quantum computing infrastructure investment of U.S. technology companies, and the established MRI infrastructure whose helium management creates ongoing cryocooler demand. U.S. cryocooler manufacturers including Sunpower (Ametek), Raytheon Technologies, Northrop Grumman MESO, and FLIR Systems (Teledyne) sustain domestic defense cryocooler production whose export controls restrict international competitive access to U.S. military-grade cryocooler designs.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Cryocooler Market Insights

Asia Pacific is the fastest-growing regional Cryocooler Industry, driven by China's expanding space and defense cryocooler programs whose domestic satellite manufacturing and missile guidance system development create growing state-sponsored cryocooler demand alongside Japan and South Korea's advanced electronics cooling needs and the region's rapidly expanding healthcare infrastructure adding MRI systems at above-global-average rates. China's space station thermal control and remote sensing satellite programs require specialized cryocooler solutions that Chinese domestic manufacturers including Zhejiang University cryocooler division and CRNL (China Research Institute of Radiowave Propagation) are developing with government investment.

Europe Cryocooler Market Insights

Europe's Cryocooler Market is driven by the European Space Agency's science mission cryocooler procurement whose Herschel, Planck, and upcoming Athena X-ray observatory missions have established Europe as a space cryocooler technology leader and the region's advanced healthcare sector whose MRI installation density sustains helium management cryocooler demand. Thales Cryogenics in the Netherlands and Leonardo DRS in the UK sustain European cryocooler manufacturing whose space and defense procurement provides the development funding for technology that subsequently transfers to commercial healthcare and energy applications.

MEA and Latin America Cryocooler Market Insights

The Middle East's Cryocooler Industry is growing with Israel's advanced defense technology sector whose Rafael Advanced Defense Systems and Elbit Systems infrared weapon systems are significant domestic cryocooler consumers and the Gulf states' growing healthcare infrastructure adding MRI systems. Israel's cryocooler industry which produces miniaturized Stirling cryocoolers for tactical infrared applications that are exported globally through Israeli defense electronics supply chains represents the Middle East's most commercially significant cryocooler manufacturing capability. Latin America's market concentrates in Brazil's healthcare sector MRI installations and Mexico's growing defense procurement.

Market Growth Drivers: Quantum computing infrastructure and defense infrared systems driving sustained cryocooler market growth globally

Cryocoolers for quantum computing and defense infrared systems have been identified as key factors behind the sustained growth of the Cryocooler Market. The quantum computers require extremely low temperatures for maintaining stability within qubits and reducing thermal interference, thus resulting in higher needs for cryogenics technology. Likewise, the infrared detectors for defense purposes also necessitate high-grade cryocoolers in order to maintain the accuracy of infrared sensors.

Market Restraints: High system costs and helium supply dependency creating cryocooler market adoption challenges globally

The high capital cost of cryocooler systems where a production-grade Stirling cryocooler for defense applications costs USD 20,000-80,000 and a dilution refrigerator for quantum computing costs USD 500,000-2,000,000 creates procurement barriers that limit adoption in cost-sensitive markets whose cryocooler need is genuine but budget-constrained. The specialized engineering expertise required for cryocooler system integration — where thermal budgeting, vibration isolation, and cryogenic plumbing require engineering disciplines not widely available outside major research institutions and defense contractors creates deployment complexity that slows commercial adoption beyond established defense and scientific user communities.

Market Opportunities: Quantum computing scale-up and LNG distributed production creating transformative cryocooler market growth opportunities globally

Quantum computing represents the cryocooler market most commercially transformative long-term opportunity where the planned scale-up from current demonstration systems toward commercially viable million-qubit processors requires continuous improvement in cryocooler cooling capacity, vibration isolation, and thermodynamic efficiency. The quantum computing cryocooler industry currently estimated at USD 200-300 million annually is projected to grow at 35%+ CAGR through the decade as IBM, Google, Microsoft, IonQ, and national quantum computing programs worldwide commission increasingly large quantum systems requiring proportionally more cryocooling infrastructure. Distributed LNG production where mid-scale liquefaction plants serving industrial consumers, remote communities, and marine fuel providers create demand for compact, modular LNG liquefaction cryocoolers represents a growing industrial application whose unit economics are improving with each generation of liquefaction cryocooler efficiency improvement.

Recent Developments:

-

2026: Sunpower (Ametek) launched its CryoTel GT third-generation free-piston Stirling cryocooler achieving 7 watts of cooling at 77K from 85 watts of electrical input for a coefficient of performance 18% above its predecessor establishing the world's highest electrical efficiency among mass-produced tactical cryocoolers and qualifying for the U.S. Army's next-generation Common Infrared Countermeasures program whose airborne installation weight constraints require the specific size-weight-and-power profile that the CryoTel GT's redesigned alternator and displacer achieve.

-

2025: Bluefors launched its LD400 dilution refrigerator system providing 400 microwatts of cooling at 20 millikelvin in a compact footprint enabling 50% denser quantum processor rack mounting versus its predecessor receiving purchase orders from IBM Quantum Network, Google Quantum AI, and IQM Quantum Computers totaling over 80 systems across global quantum data center expansion programs that represent the largest commercial dilution refrigerator sales volume in the instrument's 60-year commercial history.

Cryocooler Companies are:

-

Sunpower Inc. (Ametek)

-

Thales Cryogenics BV

-

Raytheon Technologies Corporation

-

Northrop Grumman Corporation (MESO)

-

FLIR Systems (Teledyne)

-

Cobham Advanced Electronic Systems

-

Chart Industries Inc.

-

Stirling Cryogenics BV

-

Bluefors Oy

-

Oxford Instruments NanoScience

-

Sumitomo Heavy Industries Ltd. (SHI Cryogenics)

-

Air Liquide Advanced Technologies

-

Ricor-USA Inc.

-

AIM Infrarot-Module GmbH

-

Global Cooling Inc.

-

Cryomech Inc.

-

RIX Industries

-

Advanced Research Systems Inc.

-

Infrared Focal Plane Array Inc.

Cryocooler Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.85 Billion |

| Market Size by 2035 | USD 5.52 Billion |

| CAGR | CAGR of 6.92% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Regenerative [Stirling, Gifford-McMahon, Pulse Tube], Recuperative [Joule-Thomson, Brayton]) • By End Use (Military & Defense, Healthcare, Semiconductor & Electronics, Energy, Industrial, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Sunpower Inc. (Ametek); Thales Cryogenics BV; Raytheon Technologies Corporation; Northrop Grumman Corporation (MESO); FLIR Systems (Teledyne); Leonardo DRS Inc.; Cobham Advanced Electronic Systems; Chart Industries Inc.; Stirling Cryogenics BV; Bluefors Oy; Oxford Instruments NanoScience; Sumitomo Heavy Industries Ltd. (SHI Cryogenics); Air Liquide Advanced Technologies; Ricor-USA Inc.; AIM Infrarot-Module GmbH; Global Cooling Inc.; Cryomech Inc.; RIX Industries; Advanced Research Systems Inc.; Infrared Focal Plane Array Inc. |

Frequently Asked Questions

Ans: The Cryocooler Market was valued at USD 2.85 billion in 2025.

Ans: North America dominated with approximately 36.4% share; Asia Pacific is the fastest growing.

Ans: Military & Defense dominated with 20.5% share; Healthcare is growing at the fastest CAGR.

Ans: Regenerative cryocoolers dominated with 56.6% share; Recuperative is growing at the fastest CAGR.

Ans: The Cryocooler Market is expected to grow at a CAGR of 6.92% from 2026 to 2035.

Get in Touch