Electronic Design Automation Market Report Scope & Overview:

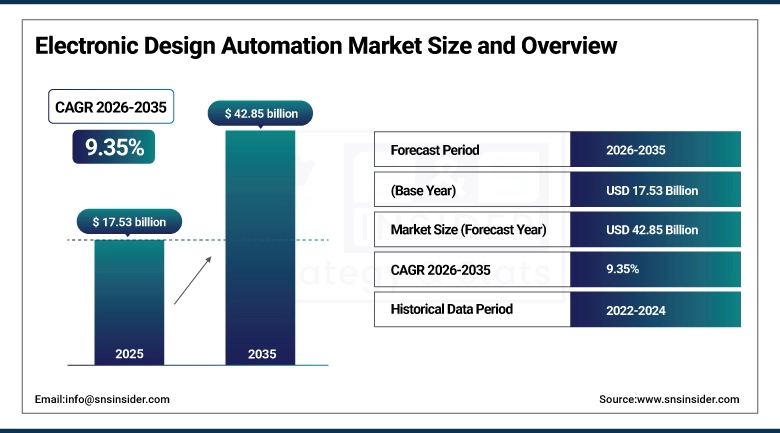

The Electronic Design Automation Market size was valued at USD 17.53 Billion in 2025 and is projected to reach USD 42.85 Billion by 2035, growing at a CAGR of 9.35 % during 2026–2035.

High demand for advanced semiconductor chips for a variety of end-use industries, such as consumer electronics, automotive, telecommunications, and healthcare, is driving growth in the Electronic Design Automation (EDA) market. Three Growing Trends Driving EDA Tool Usage As AI, IoT and 5G Technology Adoption Stimulates Complexity in Chip Solutions Moreover, the move to smaller node technologies and system-on-chip (SoC) designs has driven demand for innovative design solutions. The wider market growth trend during the projection timeframe is likewise aided by rising investments related to semiconductor production and development of fabless firms.

Electronic Design Automation (EDA) Market Size and Forecast:

-

Market Size in 2025: USD 17.53 Billion

-

Market Size by 2035: USD 42.85 Billion

-

CAGR: 9.35 % during 2026–2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Electronic Design Automation Market - Request Free Sample Report

Electronic Design Automation Market Key Trends:

-

There is a growing demand for advanced semiconductor designs across industries such as consumer electronics, automotive, and telecommunications; hence, there is a higher adoption of Electronic Design Automation (EDA) tools globally.

-

A growing trend toward miniaturization of electronic components is increasing the adoption of advanced node design solutions in the long term.

-

A growing number of innovations in AI, IoT, and 5G technologies is improving the complexity of chip design, thereby driving demand for EDA solutions.

-

Technological advancements in cloud-based EDA tools are improving accessibility, scalability, and collaboration in chip design processes.

-

A growing number of fabless semiconductor companies and startups is improving the demand for cost-effective and efficient EDA tools.

-

A growing number of strategic collaborations between semiconductor manufacturers and EDA providers is improving innovation and accelerating product development cycles.

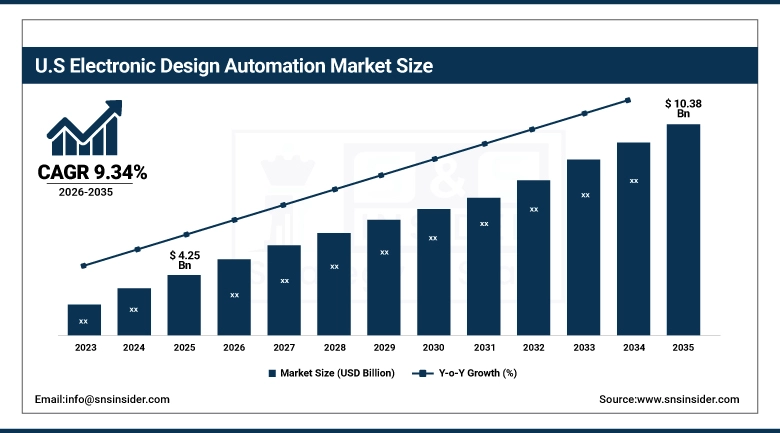

U.S. Electronic Design Automation Market Size Outlook:

The U.S. Electronic Design Automation (EDA) Market was valued at approximately USD 4.25 Billion in 2025 and is projected to reach USD 10.38 Billion by 2035, growing at a CAGR of 9.34% during 2026–2035. Growth in the U.S. EDA market is driven by strong semiconductor innovation, rising demand for AI, 5G, and automotive electronics, increasing chip complexity, and significant investments by leading technology companies, boosting adoption of advanced EDA tools and design solutions.

Electronic Design Automation Market Key Drivers:

-

Rising demand for advanced semiconductor design and increasing chip complexity.

In industries ranging from automotive, consumer electronics, and telecommunications, the semiconductor demand has been driving the Electronic Design Automation Market. More AI, more IoT, more 5G, all of those have greatly elevated the level of complexity in chip design, which in turn requires the use of advanced EDA tools. Moreover, ongoing innovation in system-on-chip (SoC) architectures and increasing investments in semiconductor manufacturing are also helping drive market expansion.

Electronic Design Automation Market Key Restraints:

-

High cost of EDA tools and complexity in design processes are major restraints for market growth.

Another major roadblock is the cost of advanced EDA software and tools, which can be very high, especially for small & medium scale enterprises. The need for highly skilled engineers is further aggravated by the increasing complexity of modern chip design processes leading to an industry talent gap. Integration challenges and lengthy design cycles are further impediments to widespread EDA solution adoption. Overcoming these challenges is crucial for the market to enjoy sustained growth.

Electronic Design Automation Market Key Opportunities:

-

Growing adoption of cloud-based EDA solutions and AI-driven design tools offers significant growth opportunities.

This paradigm shift towards cloud-based platforms is helping enable new scalable and more affordable EDA solutions. Artificial Intelligence and Machine Learning in Chip Design AI/ML-assisted Chip Design with chip design capabilities are improving the efficiency and shortening time to market. Additionally, increasing investments in semiconductor startups and growth of advanced technology such as autonomous vehicle and smart devices are projected to provide lucrative opportunities for market player from 2018 to 2025.

Electronic Design Automation Market Segments:

-

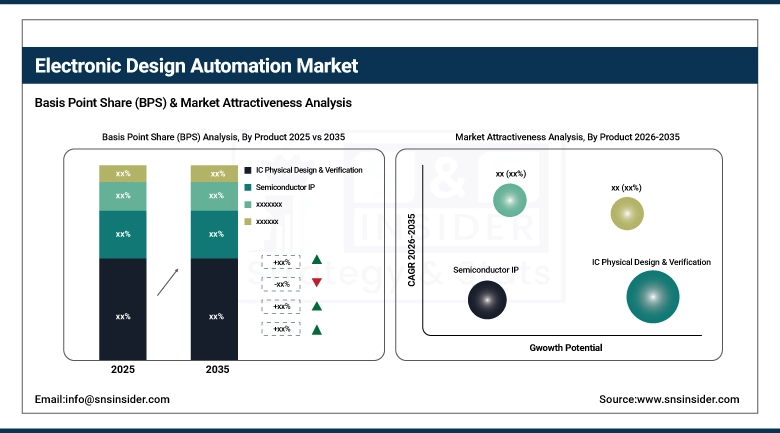

By Product: In 2025, IC Physical Design & Verification dominated with 37% share; Semiconductor IP fastest growing segment during 2026–2035

-

By Deployment Mode: In 2025, On-Premises dominated with 58% share; Cloud-Based fastest growing segment during 2026–2035

-

By Application: In 2025, Microprocessors & Microcontrollers dominated with 41% share; Memory Management Units fastest growing segment during 2026–2035

-

By End User: In 2025, Consumer Electronics Industry dominated with 39% share; Automotive fastest growing segment during 2026–2035

By Product Type, IC Physical Design & Verification Dominates While Semiconductor Intellectual Property Grows Rapidly:

The largest market share, which you can determine from the segment, especially because of the growing complexity of the designs of integrated Circuit (IC), is the IC Physical Design & Verification segment which demands high accuracy. By 2025, robust growth in the segment was seen as advanced node designs and system-on-chip (SoC) development ramped up.

Among market segmentation, Semiconductor Intellectual Property is the fastest growing segment as the demand for reusable units increases with bottle neck reduction and meets the demand for production-ready designs with less design cycle time and at lower development costs. The strong growth in the segment is also expected to accelerate, due to the increased adoption of IP-based design methodologies.

By Deployment, Private Cloud Dominates While Public Cloud Records Fastest Growth:

The Private Cloud (On-Premise) segment dominated the market owing to greater security, control, and reliability for chip design processes that require greater data confidentiality. Five years ago, around 70% of all large enterprises deployed EDA tools on private infrastructure.

The Public Cloud Segment is the fastest growing category, as demand for highly scalable, flexible, and cost-effective design environments continues to rise. Startups and SMEs are taking to cloud-based EDA solutions.

By Application, Microprocessors & Microcontrollers Dominate While Memory Management Units Grow Rapidly:

Microprocessors & Microcontrollers segment had the highest share of 41% in 2025 with their widespread use in consumer electronics, industrial system applications, and communication devices.

The growing demand for high-performance computing and smart devices has been a major contributor to the leadership of this segment. The way it (leads the industry) will keep leading is through advances in processor technologies and integration technologies.

By End User, Consumer Electronics Industry Dominates While Automotive Records Fastest Growth:

In 2025, the Consumer Electronics Industry segment captured a dominant lead in the market in compared to other segments, attaining 39% market share due to high demand for smartphones, laptops, wearable devices and other smart electronics. This segment is attributed to rapid product innovation and the growing consumer emphasis on low power, high-performance devices.

The Automotive segment is the fastest growing segment owing to the higher adoption of electric vehicles (EVs), advanced driver-assistance systems (ADAS), and autonomous driving technologies. This trend leads to an increasing complexity in semiconductor designs, and hence will drive the automotive EDA market growth.

Electronic Design Automation Market Regional Analysis:

North America Electronic Design Automation Market Insights:

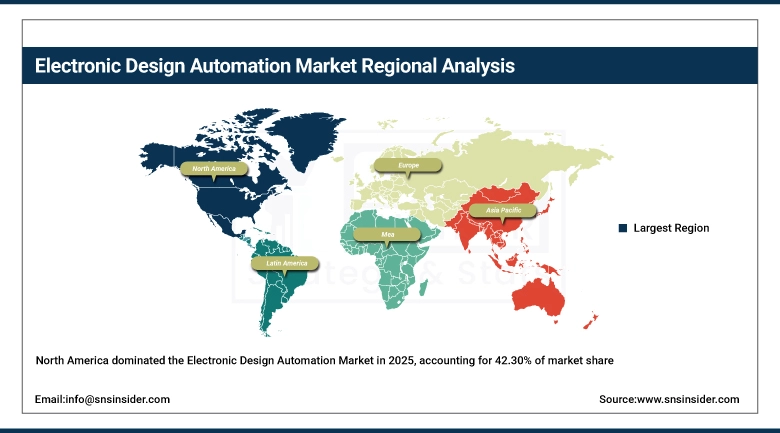

North America holds the dominant share of the market of 42.30% in 2025 in the Electronic Design Automation Market. A healthy share of this dominance is attributed to the presence of several leading semiconductor companies and EDA vendors in the U.S. and Canada. The availability of high investments in developed technologies i.e. AI, 5G, high performance computing & R&D infrastructure contributes majorly to market growth. This leadership is also driven by the need for increasingly complex chip designs as well as ongoing innovation.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia-Pacific Electronic Design Automation Market Insights:

The rapid region in Asia Pacific Electronic Design Automation Market is expected to grow between 2026-2035 at a CAGR of 10.10 %. The area has been widening because of the explosive growth of semiconductor production in China, Taiwan, South Korea, Japan and India. The biggest driving factor in this region is increasing demand for consumer electronics and expansion of foundries, as well as increased investments for chip design capabilities.

Europe Electronic Design Automation Market Insights:

While the strong automotive and industrial sectors drive the Europe Electronic Design Automation Market, increasing investments in semiconductor design and innovation further augments the market growth. Market growth in Germany, France and the UK is driven by commercialization of new electronics to develop automotive for e.g. electric and autonomous vehicles. Regulation enablers and R&D activity are others supporting expansion as well.

Latin America Electronic Design Automation Market Insights:

The steady growth of Latin America Electronic Design Automation Market can be mainly attributed to the growing digital transformation & adoption of electronics in end use sectors. Nations like Brazil and Mexico are experiencing growth thanks to an expanding industrial base and growing investments in technology infrastructure.

Middle East & Africa (MEA) Electronic Design Automation Market Insights:

The Middle East & Africa electronic design automation market is slowly growing with the digital adoption truss same with the smart infrastructure projects. The rise in investments in telecommunications, smart cities and industrial automation in countries like the UAE, Saudi Arabia and South Africa is supporting the market growth in this region.

Electronic Design Automation Market Competitive Landscape:

Synopsys is a top electronic design automation solution provider with a solid place in the semiconductor design and verification space. The core silicon design, IP integration, and software security tools the company offers play a key role in accelerating the design of advanced chips. The emphasis is on innovation including AI-powered chip design, centralized cloud EDA platforms, and SoC design. To defend its leadership position, Synopsys has one of the strongest global customer bases and continues to invest in R&D and strategic partnerships in the market space.

-

In March 2025, Synopsys expanded its AI-driven EDA capabilities by enhancing its cloud-based design platforms to improve chip design productivity and reduce time-to-market for advanced semiconductor solutions.

Cadence Design Systems is a key player in the electronic design automation market, offering a comprehensive portfolio of software, hardware, and IP solutions for semiconductor and system design. The company focuses on advanced technologies such as computational software, AI-driven design tools, and high-performance computing solutions. Cadence serves industries including automotive, aerospace, and telecommunications, and continues to strengthen its market position through continuous innovation and partnerships.

-

In February 2025, Cadence Design Systems introduced new AI-powered design and verification tools aimed at accelerating complex chip development and enhancing design accuracy for next-generation semiconductor applications.

Electronic Design Automation (EDA) Companies are:

-

Synopsys

-

Siemens EDA

-

ANSYS

-

Keysight Technologies

-

Zuken

-

Autodesk

-

Altium

-

Mentor Graphics

-

Silvaco

-

AWR Corporation

-

Magma Design Automation

-

Dassault Systèmes

-

National Instruments

-

ARM Holdings

-

Rambus

-

Xilinx

-

Intel

-

Broadcom

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 17.53 Billion |

| Market Size by 2035 | USD 42.85 Billion |

| CAGR | CAGR of 9.35 % From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (IC Physical Design & Verification, Semiconductor IP, Computer-Aided Engineering (CAE), PCB & MCM, Services), • By Deployment Mode (Cloud-Based, On-Premises), • By Application (Memory Management Units, Microprocessors & Microcontrollers, Others), • By End User (Consumer Electronics Industry, Automotive, Healthcare) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Synopsys, Cadence Design Systems, Siemens EDA, ANSYS, Keysight Technologies, Zuken, Altair Engineering, Autodesk, Altium, Mentor Graphics, Silvaco, AWR Corporation, Magma Design Automation, Dassault Systèmes, National Instruments, ARM Holdings, Rambus, Xilinx, Intel, Broadcom. |

Frequently Asked Questions

Ans: The Electronic Design Automation Market is expected to grow at a CAGR of 9.35 % during 2026–2035.

Ans: The Electronic Design Automation (EDA) Market size was valued at USD 17.53 Billion in 2025 and is projected to reach USD 42.85 Billion by 2035.

Ans: The key drivers of the Electronic Design Automation Market include increasing demand for advanced semiconductor chips, rising complexity in integrated circuit design, growing adoption of AI, IoT, and 5G technologies.

Ans: The IC Physical Design & Verification segment dominated the Electronic Design Automation Market during the projected period due to its critical role in ensuring accuracy and performance in complex chip designs.

Ans: North America dominated the Electronic Design Automation Market in 2025.

Get in Touch