Extracorporeal Membrane Oxygenation Machine Market Report Scope & Overview:

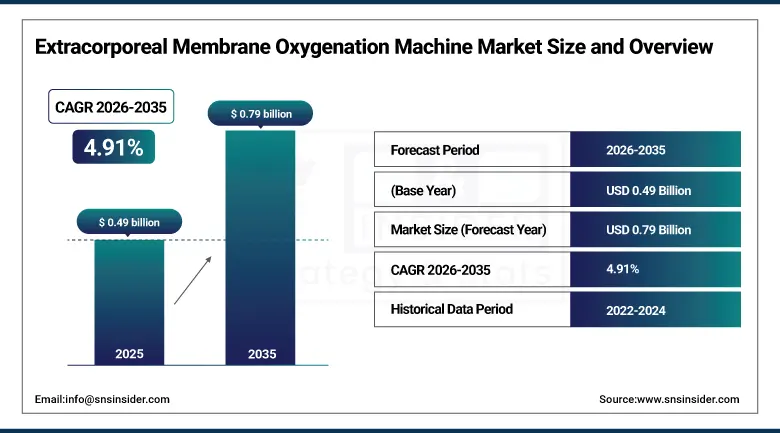

The Extracorporeal Membrane Oxygenation Machine Market was valued at USD 0.49 billion in 2025 and is expected to reach USD 0.79 billion by 2035, growing at a CAGR of 4.91% from 2026–2035.

The ECMO machine market encompasses the integrated system components required for safe extracorporeal life support including centrifugal blood pumps creating the driving force for circuit flow, polymethylpentene hollow-fibre oxygenator membranes enabling efficient gas exchange across several square metres of surface area, polyurethane or silicone cannulae accommodating patient anatomical variation from premature neonates through large adults, heat exchangers maintaining normothermia, and electronic control consoles providing real-time monitoring of flow, pressure, sweep gas, and circuit integrity with alarm systems for clinical safety. The recurring disposable circuit market generates substantial recurring revenue alongside the capital equipment base, as each patient run requires a complete new ECMO circuit encompassing oxygenator, tubing, connectors, and related consumables.

The Extracorporeal Life Support Organization's 2025 Registry documenting over 600,000 cumulative ECMO runs with over 90,000 new cases in 2024 confirms ECMO's transition from experimental rescue therapy to accepted standard of care for defined critical care indications, while highlighting the enormous remaining clinical penetration potential relative to the global burden of severe cardiac and respiratory failure.

Market Size and Forecast

-

Market Size in 2026E: USD 0.51 Billion

-

Market Size by 2035: USD 0.79 Billion

-

CAGR: 4.91% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Extracorporeal Membrane Oxygenation Machine Market - Request Free Sample Report

Extracorporeal Membrane Oxygenation Machine Market Trends

-

Rapid development of miniaturised portable ECMO systems including the Eurosets Xtreme Rescue and Getinge CARDIOHELP that can be transported with patients between facilities or deployed in emergency settings outside the traditional ICU, expanding ECMO from fixed bedside configurations toward mobile extracorporeal life support for inter-hospital transport and community cardiac arrest response.

-

Growing adoption of ECMO-assisted cardiopulmonary resuscitation protocols for refractory cardiac arrest, enabling resuscitation beyond the duration limitations of conventional CPR while oxygenated circulation is maintained as underlying causes are diagnosed and treated, creating a new high-growth application expanding ECMO into emergency medicine and catheterisation laboratory environments.

-

Increasing development of automated ECMO circuit management incorporating AI-assisted titration of pump flow, sweep gas, and anticoagulation based on continuous monitoring data, reducing the specialised clinical expertise barrier that limits ECMO availability to large academic centres with dedicated programme staffing.

-

Rising adoption of ambulatory ECMO configurations allowing stable patients to be mobilised, participate in physical rehabilitation, and in some cases ambulate while receiving ongoing extracorporeal support, improving functional outcomes and reducing deconditioning consequences of prolonged immobility during extended support runs.

-

Expanding ECMO application in high-risk cardiac procedures including complex valve replacements, ventricular reconstruction, and transplant bridge support where preoperative ECMO initiation provides haemodynamic stability during surgical procedures that would carry unacceptable mortality risk without extracorporeal circulatory support.

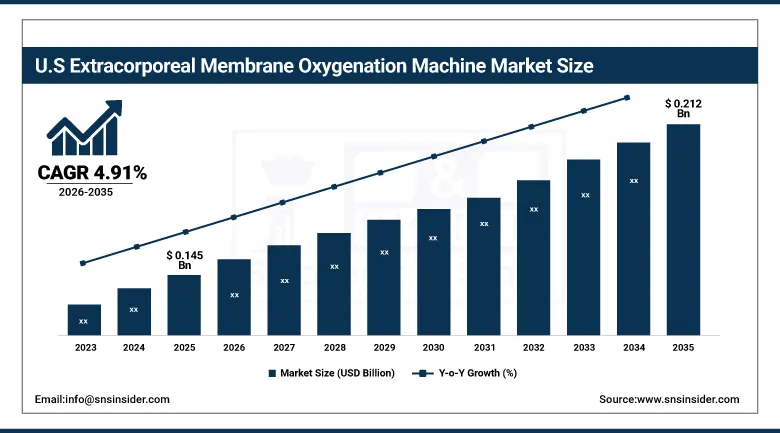

U.S. Extracorporeal Membrane Oxygenation Machine Market Outlook

The U.S. extracorporeal membrane oxygenation machine market was valued at approximately USD 0.145 billion in 2025 and is expected to reach approximately USD 0.212 billion by 2035, growing at a CAGR of 4.91%, driven by the highest ECMO programme concentration globally in U.S. academic medical centres, robust Medicare and commercial insurance reimbursement, and sustained ECMO clinical research expanding the evidence base for emerging applications including ECPR and high-risk cardiac intervention support.

The Prague OHCA randomised trial and the ARREST trial both demonstrated survival advantages for ECPR compared with conventional resuscitation in selected cardiac arrest patients, providing the clinical evidence base that is driving systematic ECPR programme development at major U.S. medical centres with the rapid response infrastructure and catheterisation laboratory access that effective ECPR protocols require.

Extracorporeal Membrane Oxygenation Machine Market Segment Analysis

-

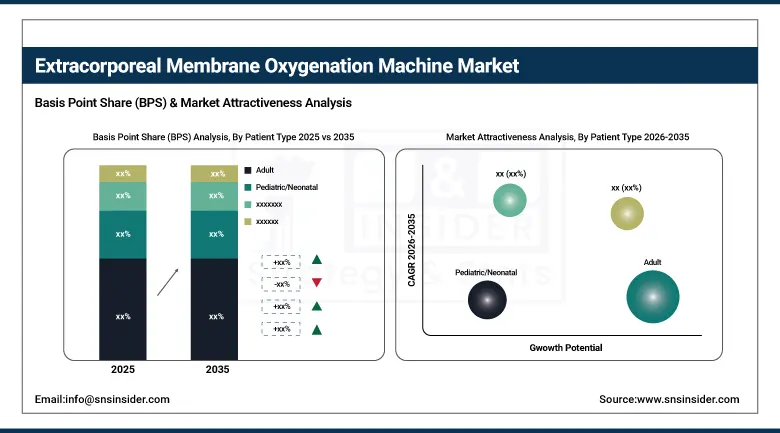

By Patient Type, Adults dominated with approximately 59.13% in 2025 through higher prevalence of cardiac and respiratory conditions requiring ECMO; Pediatric patients are the fastest-growing at a CAGR of 8.20% as improved neonatal and paediatric ECMO techniques, growing clinical evidence, and expanded training drive adoption in neonatal and paediatric intensive care units.

-

By Application, Cardiac applications dominated with approximately 49.38% in 2025 as ECMO's primary role in cardiogenic shock, post-cardiotomy failure, and high-risk cardiac procedure support; ECPR is the fastest-growing application at a CAGR of 7.85% as evidence-supported adoption in emergency cardiac arrest management creates a rapidly expanding new application category.

-

By Product, Venovenous ECMO is the larger segment through exclusive respiratory support for the numerically larger ARDS population; Venoarterial is fastest-growing driven by expanding cardiogenic shock and ECPR applications requiring combined cardiac and respiratory support.

-

By End User, Hospitals dominated as the primary setting for all ECMO procedures requiring specialised equipment, trained staff, and intensive monitoring infrastructure; Academic medical centres represent the highest-volume and highest-revenue segment within the hospital end-user category.

By Patient Type, Adults dominate, Pediatric is expected to grow fastest

Adult patients retained the dominant position with approximately 59.13% of ECMO Machine Market revenues in 2025, reflecting the epidemiological prevalence of cardiogenic shock, decompensated heart failure, post-cardiotomy cardiac failure, and severe ARDS in adult and elderly populations that collectively represent the numerically largest ECMO indication categories. The adult cardiac ECMO market has grown through the expansion of percutaneous venoarterial configurations for cardiogenic shock management that can be initiated in catheterisation laboratories without thoracic surgery, dramatically expanding the programme locations capable of offering ECMO-supported shock treatment and creating a new emergency cardiology subspecialty around rapidly initiated extracorporeal haemodynamic support.

Paediatric and neonatal ECMO is the fastest-growing patient type at a CAGR of 8.20% through 2035, driven by accumulating ELSO registry evidence demonstrating improving outcomes across a widening range of neonatal and paediatric indications, growing neonatologist and paediatric intensivist ECMO training, and the development of paediatric-specific circuit configurations with smaller prime volumes and lower-resistance oxygenators that improve safety for the smallest patients with congenital diaphragmatic hernia, persistent pulmonary hypertension of the newborn, and congenital heart disease.

By Application, Cardiac dominates, ECPR is expected to grow fastest

Cardiac applications retained the dominant position with approximately 49.38% of the ECMO Machine Market in 2025, encompassing venoarterial ECMO for cardiogenic shock from any cause, post-cardiotomy failure, bridge to transplantation or left ventricular assist device, and high-risk percutaneous coronary intervention support. The cardiogenic shock application has grown most substantially through percutaneous cannulation techniques enabling rapid ECMO initiation in catheterisation laboratories and emergency departments without surgical cut-down, dramatically expanding the centre population capable of offering ECMO-supported shock management beyond the cardiac surgery-adjacent programmes that historically initiated ECMO exclusively through surgical arterial access.

ECPR is the fastest-growing application at a CAGR of 7.85% through 2035, representing venoarterial ECMO initiated during refractory cardiac arrest to maintain oxygenated mechanical circulation while the arrest's underlying cause is diagnosed and definitively treated. Multiple randomised trials and systematic ELSO registry analyses demonstrating survival and neurological outcome advantages for ECPR compared with conventional resuscitation in carefully selected patient populations are driving systematic ECPR programme development at major medical centres with rapid cannulation teams and catheterisation laboratory access that effective ECPR protocols require.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

86.4% |

|

Europe |

Germany |

26.8% |

|

Asia Pacific |

Japan |

34.7% |

|

Middle East & Africa |

Saudi Arabia |

28.3% |

|

Latin America |

Brazil |

44.1% |

North America ECMO Machine Market Insights

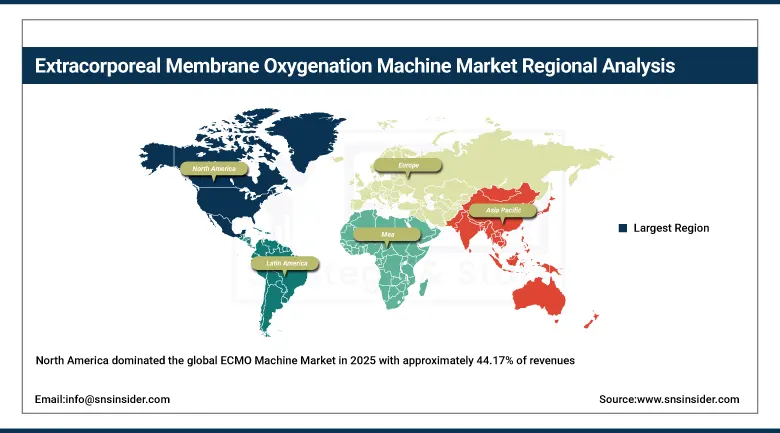

North America dominated the global ECMO Machine Market in 2025 with approximately 44.17% of revenues, with the United States accounting for approximately 86.4% of North American revenues. The region's leadership reflects the world's highest ECMO programme density, robust CMS reimbursement sustaining high utilisation rates, and the presence of major ECMO technology companies whose U.S. operations drive both domestic market supply and global product innovation. The ELSO registry's North American chapter maintains the world's most comprehensive ECMO clinical outcomes database whose continuous quality reporting enables U.S. ECMO programmes to benchmark performance systematically.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe ECMO Machine Market Insights

Europe is a technically sophisticated ECMO market characterised by high programme quality at leading academic centres across Germany, France, the United Kingdom, Italy, and Sweden, active participation in landmark ECMO clinical trials that have defined the evidence base for venovenous ECMO in severe ARDS, and the headquarters of major ECMO technology providers including Getinge in Sweden and Xenios AG in Germany. Germany accounts for approximately 26.8% of European revenues as the region's largest market through its concentration of large academic cardiothoracic surgery and cardiac intensive care programmes and the national insurance system's coverage of ECMO in approved clinical indications.

Asia Pacific ECMO Machine Market Insights

Asia Pacific is the fastest-growing ECMO market with a CAGR of 5.79%, driven by rapidly expanding hospital infrastructure creating new certified ECMO centres in both academic and tertiary private hospital settings across China, Japan, South Korea, Singapore, and Australia, combined with growing intensivist and cardiac surgeon awareness trained at Western centres returning to establish ECMO programmes at Asian institutions. Japan accounts for approximately 34.7% of Asia Pacific revenues through world-class cardiothoracic surgery infrastructure and Terumo Corporation's dominant domestic market position following the Capiox SP-300 2025 launch.

MEA & Latin America ECMO Machine Market Insights

The Middle East and Africa and Latin America are developing ECMO markets where growing critical care infrastructure investment, increasing specialist availability, and rising awareness of ECMO's life-saving potential are gradually expanding access beyond pioneering academic centres. Saudi Arabia leads MEA at approximately 28.3% of regional revenues through advanced cardiac surgery programmes and significant government healthcare investment. Brazil leads Latin American revenues at approximately 44.1% through its concentration of academic cardiac surgery and heart transplantation centres in Sao Paulo and Rio de Janeiro that have developed ECMO capabilities in support of complex cardiac surgical practice.

Market Dynamics

Growth Drivers: Rising severe cardiac and respiratory failure incidence combined with expanding clinical evidence for new ECMO indications and technological advances enabling programme expansion beyond large academic centres

The primary structural growth drivers for the ECMO Machine Market are the expanding patient population with severe cardiac and respiratory failure that ECMO can address as cardiovascular disease, cardiogenic shock, decompensated heart failure, and severe pneumonia burden grows with population ageing and rising metabolic risk factors, combined with accumulating clinical evidence from randomised controlled trials and ELSO registry analyses that progressively expands the indication base where ECMO can be offered with demonstrated clinical benefit. The development of portable, miniaturised ECMO systems enabling safe inter-hospital patient transport on ECMO and emergency ECPR deployment is expanding the geographic and temporal reach of extracorporeal life support beyond fixed ICU bedside configurations that limit access to patients who can be stabilised and transported to capable centres.

Restraints: High system and disposable cost limiting adoption in resource-constrained settings, significant haemorrhagic and thrombotic complications requiring intensive expertise, and specialised workforce training requirements constraining programme capacity expansion

A significant restraint on the ECMO Machine Market is the substantial cost of ECMO therapy that encompasses capital equipment, per-patient disposable circuit costs of USD 15,000 to 30,000, intensive nurse and perfusionist staffing requirements, and total hospitalisation costs frequently exceeding USD 100,000 to 500,000 for complex long-duration runs that place ECMO economically out of reach for lower and middle income country healthcare systems and limit programme development to major tertiary centres in high-income markets. The significant haemorrhagic and thrombotic complication burden associated with ECMO, encompassing bleeding from anticoagulation, thrombosis within the circuit, and oxygenator failure requiring circuit exchange, demands continuous expert bedside management that limits the scalability of ECMO beyond well-resourced specialist programme environments.

Opportunities: Portable ECMO enabling mobile deployment and systematic ECPR programmes, AI circuit management reducing expertise barriers, and growing evidence base attracting new institutional programme investment

The commercialisation of portable miniaturised ECMO systems enabling safe patient transport between facilities while maintaining extracorporeal support creates the most operationally transformative opportunity in the ECMO market, as the clinical outcome advantage of high-volume ECMO programme management motivates regional centralisation strategies that require safe mobile ECMO transport infrastructure to implement. AI-assisted circuit management systems that automate routine monitoring responses and provide decision support for anticoagulation management represent the technology investment most likely to extend high-quality ECMO management capability to centre types that currently lack the continuous specialist bedside coverage that ECMO's current management intensity demands.

Recent Developments:

-

April 2025: Eurosets unveiled the Xtreme Rescue, described as the world's lightest portable ECMO device, and the Landing Breathe advanced respiratory monitoring system at EuroELSO 2025, demonstrating the industry's commitment to miniaturisation enabling mobile deployment in emergency and transport contexts.

-

March 2025: Terumo Corporation launched the Capiox SP-300 heart-lung machine with enhanced sensors and real-time monitoring at EuroELSO 2025, solidifying Terumo's approximately 70% Japanese market share and providing a platform for expanded international development.

-

January 2025: Getinge announced it will phase out its surgical perfusion business to reallocate resources toward higher-growth areas including ECMO and transplant care, reflecting strategic prioritisation of ECMO as a long-term commercial growth platform.

-

2025: LivaNova's RS Rating improved from 67 to 73 reflecting strengthened technical performance following strategic refocusing on cardiopulmonary and neuromodulation core competencies after the ACS business wind-down.

-

2025: Multiple major U.S. academic medical centres formalised systematic ECPR protocols for refractory in-hospital cardiac arrest following positive institutional outcome data, contributing to growing U.S. ECPR programme infrastructure that is expanding ECMO utilisation into emergency cardiac resuscitation.

Extracorporeal Membrane Oxygenation Machine Market Key Players

-

Medtronic plc

-

Getinge AB

-

LivaNova PLC

-

Terumo Corporation

-

Xenios AG (Fresenius Medical Care)

-

Eurosets S.r.l.

-

Microport Scientific Corporation

-

OriGen Biomedical

-

Nipro Corporation

-

ALung Technologies Inc.

-

Thoratec Corporation (Abbott)

-

MAQUET Holding B.V. & Co. KG

-

Fresenius Medical Care AG

-

Hemovent GmbH

-

Novalung GmbH (Xenios)

-

MC3 Cardiopulmonary

-

SciMed Life Systems

-

BioLung

-

Surmodics Inc.

-

Breethe Inc.

Extracorporeal Membrane Oxygenation Machine Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 0.49 Billion |

| Market Size by 2035 | USD 0.79 Billion |

| CAGR | CAGR of 4.91% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Venoarterial ECMO, Venovenous ECMO) • By Component (Pumps, Oxygenators, Cannulae, Controllers & Monitors, Others), • By Patient Type (Adult, Pediatric/Neonatal) • By Application (Cardiac, Respiratory, Extracorporeal Cardiopulmonary Resuscitation, Others) • By End User (Hospitals, Specialty Clinics, Ambulatory Surgical Centers, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Medtronic plc, Getinge AB, LivaNova PLC, Terumo Corporation, Xenios AG (Fresenius Medical Care),Eurosets S.r.l., Microport Scientific Corporation, OriGen Biomedical, Nipro Corporation, ALung Technologies Inc., Thoratec Corporation (Abbott), MAQUET Holding B.V. & Co. KG, Fresenius Medical Care AG, Hemovent GmbH, Novalung GmbH (Xenios), MC3 Cardiopulmonary, SciMed Life Systems, BioLung, Surmodics Inc., Breethe Inc. |

Frequently Asked Questions

The ECMO Machine Market is expected to grow at a CAGR of 4.91% from 2026 to 2035.

The ECMO Machine Market was valued at USD 0.495 billion in 2025.

Rising incidence of severe cardiac and respiratory failure combined with expanding clinical evidence for ECMO in new indications including ECPR and technological advances enabling portable deployment that support programme expansion beyond large academic centres.

Adult patients dominated with approximately 59.13% of revenues in 2025.

North America dominated with approximately 44.17% of revenues in 2025.

Get in Touch