Geophysical Software Service Market Report Scope and Overview:

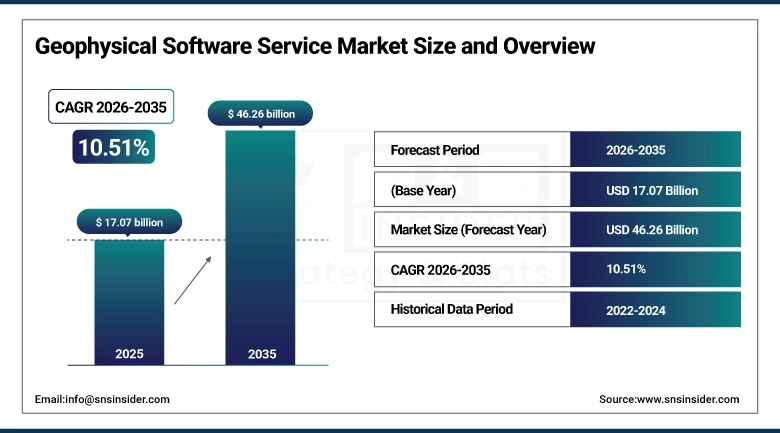

The Geophysical Software Service Market was valued at USD 17.07 billion in 2025 and is expected to reach USD 46.26 billion by 2035, growing at a CAGR of 10.51% from 2026-2035.

The Geophysical Software Service Market encompasses the broad ecosystem of software solutions, analytical platforms, and associated managed services deployed to acquire, process, interpret, model, and visualize subsurface geophysical data across oil and gas exploration, mineral and mining operations, groundwater resource assessment, agricultural land characterization, and environmental monitoring applications. Geophysical software services integrate multiple data acquisition modalities including seismic, gravity, magnetic, electromagnetic, and ground-penetrating radar methods into unified interpretation environments that enable geoscientists, exploration engineers, and resource managers to extract actionable subsurface intelligence from increasingly complex and voluminous datasets. The market encompasses the full spectrum of deployment architectures from traditionally licensed on-premises installation models to rapidly expanding cloud-native Software-as-a-Service platforms that democratize access to enterprise-grade geophysical processing and interpretation capabilities for operators of all sizes across global exploration theaters.

The market is witnessing strong growth fueled by the integration of multiple structural trends driving changes in the worldwide energy and resources exploration industry. The continued high global demand for hydrocarbon fuels along with the gradual exhaustion of easy-to-access conventional oil and gas deposits is pushing upstream companies to venture into the unexplored territories of geological exploration and production that require advanced geophysical software technologies to accurately map subsurface structures, conduct attribute modeling, and assess reservoir probabilities, all of which are essential in mitigating risks in exploration and making informed well location decisions. Meanwhile, the international minerals and mining industry is witnessing a notable boost in exploration activity spurred by escalating demand for battery metals such as lithium, cobalt, nickel, copper, and rare earth minerals used in electric vehicles, renewable energy systems, and electronics manufacturing.

Geophysical Software Service Market Size and Forecast

Market Size in 2025: USD 17.07 Billion

Market Size by 2035: USD 46.26 Billion

CAGR: 10.51% from 2026 to 2035

Base Year: 2025

Forecast Period: 2026-2035

Historical Data: 2022-2024

To Get more information on Geophysical Software Service Market - Request Free Sample Report

Geophysical Software Service Market Trends

-

Integration of artificial intelligence and machine learning technologies into geophysical software solutions has led to automated seismic interpretation, intelligent fault detection, and machine learning-based reservoir property predictions. Such advances have shortened seismic interpretation cycles significantly, making possible the completion of tasks within hours rather than days or weeks, as well as the development of highly reproducible subsurface models in diverse geological environments.

-

A fast shift towards cloud-based SaaS subscriptions as compared to traditional license-based solutions has democratized the access to enterprise-grade geophysical software solutions by allowing independents, NOCs of developing countries, and various exploration consultancy firms to leverage high-performance computing capabilities without requiring costly infrastructure investments.

-

The growing need for 4D time-lapse seismic monitoring among producing oil/gas wells and the associated interest in change analysis tools and time-lapse interpretation capabilities have fueled the development of sophisticated geophysical software solutions aimed at assisting oil and gas companies with reservoir modeling and enhanced oil recovery programs.

-

The global surge in battery minerals exploration driven by electric vehicle adoption and renewable energy infrastructure buildout is generating substantial new demand for geophysical software tools optimized for mineral deposit characterization, including electromagnetic data inversion platforms, potential field processing and modelling software, and integrated multi-method interpretation environments suitable for lithium, copper, nickel, and rare earth element exploration programs.

-

Increasing adoption of high-density broadband seismic acquisition and full-waveform inversion processing technologies is driving demand for advanced imaging software platforms capable of handling petabyte-scale seismic datasets through cloud-distributed high-performance computing architectures, supporting the industry transition toward higher-fidelity subsurface models that reduce drilling risk in structurally complex exploration targets.

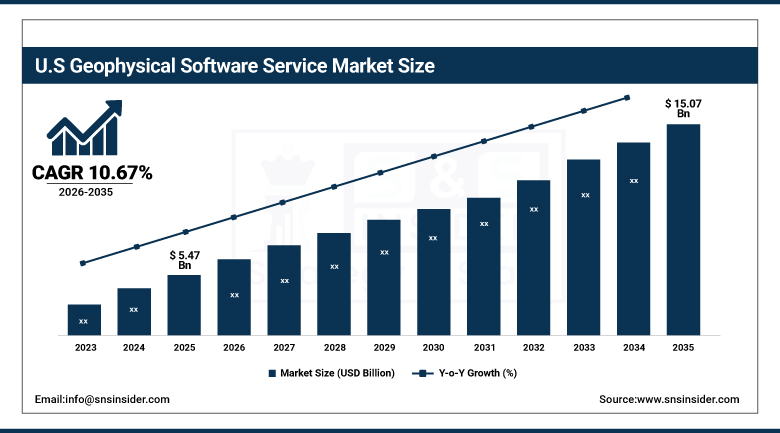

U.S. Geophysical Software Service Market was valued at approximately USD 5.47 billion in 2025 and is expected to reach approximately USD 15.07 billion by 2035, growing at a CAGR of 10.67%.

The United States represents the dominant national market within North America, underpinned by the world largest concentration of independent oil and gas exploration companies, a globally leading shale and tight resource development industry that demands advanced seismic processing and interpretation software for horizontal drilling optimization and hydraulic fracturing design, and a strong presence of the world largest geophysical software development companies including SLB, Halliburton, and TGS. The U.S. Geological Survey and Department of Energy continue to invest in geophysical research programs that advance the capabilities of subsurface imaging technologies applicable to both resource extraction and carbon capture and storage site characterization.

Geophysical Software Service Market Segment Analysis

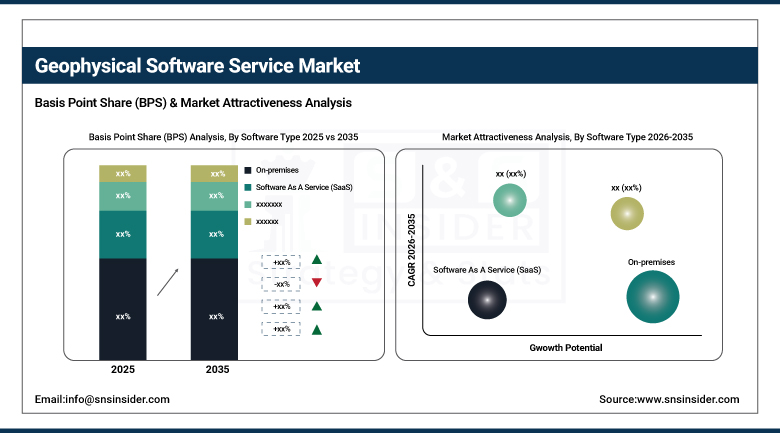

By Software Type, On-premises dominated with ~54.20% share in 2025; Software as a Service (SaaS) is the fastest-growing software type segment with a CAGR of 12.40%.

By Survey Type, Land-Based dominated with ~44.21% share in 2025; Land-Based is also the fastest-growing survey type segment with a CAGR of 11.82%.

By Application, Oil and Gas dominated with ~42.15% share in 2025; Oil and Gas is also the highest revenue application segment with a CAGR of 11.04%.

By Software Type: On-premises dominates, SaaS fastest-growing

On-premises software held approximately 54.20% of the Geophysical Software Service Market in 2025. The continued dominance of on-premises deployment reflects the deeply entrenched workflows and integration requirements of large integrated oil and gas companies, national oil companies, and major mining operators whose geophysical interpretation environments are tightly coupled with proprietary seismic data repositories, high-performance computing clusters, and enterprise data management systems that are impractical to migrate wholesale to cloud environments on short timescales. On-premises deployments also retain important advantages in data sovereignty and confidentiality for operators managing commercially sensitive exploration datasets in competitive basins, where data security requirements and regulatory constraints on data residency in certain jurisdictions support continued on-premises deployment even as cloud capabilities advance.

The Software as a Service (SaaS) segment, is projected to grow at the fastest CAGR of 12.40% through the forecast period, representing the most dynamic and rapidly expanding segment within the geophysical software market. SaaS deployment models enable geophysical software vendors to deliver continuous platform updates and AI capability improvements to subscribers without requiring client-side software installation and version management, creating a superior product development velocity that is increasingly important as AI and machine learning capabilities advance rapidly.

By Survey Type: Land-Based dominates, Marine-Based second largest

Land-Based survey software held approximately 44.21% of the Geophysical Software Service Market in 2025, and is projected to grow at the fastest CAGR of 11.82% through the forecast period. The dominant position of land-based survey software reflects the extensive global scope of onshore oil and gas exploration activity across major hydrocarbon basins in North America, the Middle East, Central Asia, South America, and Sub-Saharan Africa, combined with the growing demand for land geophysical survey software in mining, groundwater assessment, and geotechnical applications that expand the addressable market well beyond traditional hydrocarbon exploration. Advanced land seismic acquisition technologies including nodal recording systems, distributed acoustic sensing, and high-density receiver arrays are generating increasingly large and complex land seismic datasets that require sophisticated processing and imaging software platforms.

By Application: Oil and Gas dominates, Mineral and Mining second largest

Oil and Gas held approximately 42.15% of the Geophysical Software Service Market in 2025, and is projected to grow at a CAGR of 11.04% through the forecast period. The oil and gas sector remains the largest and most technology-intensive application segment for geophysical software services, driven by the continuing global energy demand that requires ongoing exploration investment to replace depleting reserves, the increasing technical complexity of exploration targets in frontier basins and unconventional resource plays that demand advanced seismic processing and interpretation software, and the deployment of 4D time-lapse seismic monitoring programs across mature producing fields that require specialized difference analysis and reservoir change detection software platforms. The energy transition is also creating new geophysical software service demand within the oil and gas application segment through carbon capture and storage site characterization programs that require subsurface seismic monitoring and integrity verification software.

Geophysical Software Service Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

73% |

|

Europe |

Germany |

22% |

|

Asia Pacific |

China |

38% |

|

Middle East & Africa |

Saudi Arabia |

31% |

|

Latin America |

Brazil |

42% |

North America Geophysical Software Service Market Insights

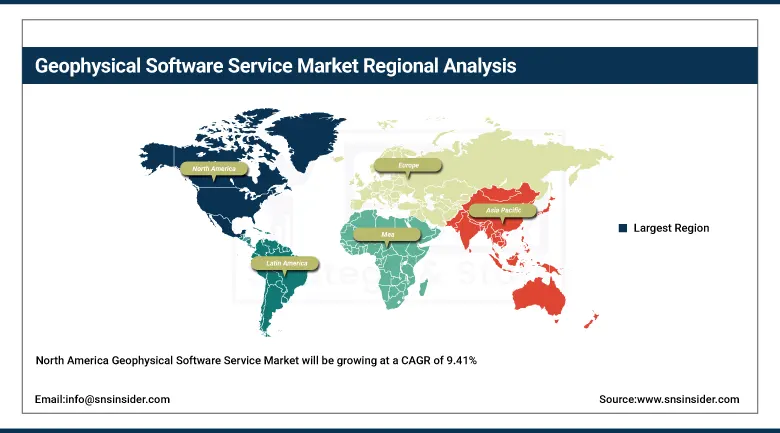

The North America Geophysical Software Service Market will be growing at a CAGR of 9.41%, with the United States representing approximately 73% of regional market value. North America market leadership is underpinned by the United States; position as the world largest producer of oil and natural gas through shale and tight resource development, which requires continuous investment in advanced seismic processing, well correlation, and reservoir characterization software to optimize horizontal drilling programs and hydraulic fracturing operations across the Permian Basin, Eagle Ford, Marcellus, and Haynesville shale plays. The concentration of the world’s leading geophysical software companies including SLB, Halliburton, TGS, and Emerson Electric in the United States creates a self-reinforcing innovation ecosystem that drives continuous product advancement and maintains the region technology leadership. Canada contributes a meaningful secondary market anchored by oil sands development in Alberta, active mineral exploration programs in the Canadian Shield and Cordilleran geological provinces, and offshore exploration activity on the Atlantic continental shelf.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Geophysical Software Service Market Insights

Europe Geophysical Software Service Market with Norway, United Kingdom, France, and the Netherlands as the primary national markets. Norway represents the largest national market within Europe, driven by the country position as the largest oil and gas producer on the Norwegian Continental Shelf where sophisticated geophysical software is routinely deployed for seismic interpretation, reservoir monitoring, and 4D seismic time-lapse analysis across the extensive portfolio of producing fields and active exploration licenses. The United Kingdom North Sea basin supports a mature but technically sophisticated geophysical software market as operators pursue enhanced oil recovery, infill drilling, and exploration in increasingly complex structural settings. European geophysical software companies including CGG (rebranded as Viridien) in France and Ikon Science in the United Kingdom are globally competitive developers of advanced seismic inversion, rock physics, and interpretation platforms.

Asia Pacific Geophysical Software Service Market Insights

Asia Pacific is the fastest-growing regional Geophysical Software Service Market, projected to grow at a CAGR of 12.31%, the highest among all regions, through the forecast period. China represents the largest national market within Asia Pacific, supported by the active exploration programs of CNPC, SINOPEC, and CNOOC across onshore continental basins and deepwater offshore exploration blocks in the South China Sea, combined with the Chinese government prioritization of energy security through domestic hydrocarbon resource development that drives sustained investment in advanced seismic processing and reservoir characterization software. Australia is a significant geophysical software market driven by the country substantial liquefied natural gas export industry, active offshore exploration in the Browse, Carnarvon, and Bonaparte basins, and a globally important minerals and mining sector deploying geophysical software across iron ore, gold, copper, nickel, and lithium exploration programs. India is the fastest-growing national market within Asia Pacific, supported by the National Data Repository initiative that is modernizing seismic data management infrastructure and government-backed initiatives to increase domestic hydrocarbon production through exploration licensing rounds in frontier basins.

Latin America Geophysical Software Service Market Insights

Latin America Geophysical Software Service Market with Brazil, Mexico, Colombia, and Argentina as the primary national markets. Brazil accounts for the largest national market within Latin America, driven by Petrobras; extensive deepwater pre-salt exploration and production program in the Santos and Campos basins that requires world-class seismic processing, full-waveform inversion imaging, and reservoir characterization software to manage the geological complexity of carbonate reservoirs beneath thick salt sequences. Mexico represents a growing market as Pemex and independent operators pursue exploration under the licensing round framework established following Mexico energy reform, with both conventional and deepwater exploration programs generating demand for seismic interpretation and basin modeling software. Argentina Vaca Muerta shale formation is creating growing demand for unconventional resource-specific geophysical software applications.

Middle East & Africa Geophysical Software Service Market Insights

Middle East & Africa Geophysical Software Service Market with Saudi Arabia, the UAE, Iraq, and South Africa as the primary national markets. Gulf Cooperation Council nations represent the most advanced geophysical software markets within the region, supported by the national oil companies of Saudi Arabia (Aramco), the UAE (ADNOC), and Kuwait (KOC) that deploy sophisticated seismic processing and reservoir characterization software across their extensive onshore and offshore hydrocarbon provinces. Saudi Aramco in particular is a significant global investor in advanced geophysical technology including full-waveform inversion, broadband seismic processing, and AI-assisted interpretation platforms that support the company sustained exploration and field development programs. Sub-Saharan Africa represents the most significant growth opportunity within the region, with active exploration programs across East Africa rift basin hydrocarbon provinces, West Africa Atlantic margin deepwater basins, and expanding mineral exploration programs in the Democratic Republic of Congo, Zambia, Tanzania, and South Africa driving growing demand for geophysical software services.

Market Growth Drivers:

Rising energy demand, critical mineral exploration surge, and AI-driven geophysical data interpretation transformation creating structural demand growth for geophysical software services

The geophysical software service market is supported by several robust and mutually reinforcing structural demand drivers. Global energy demand growth driven by industrial development in emerging economies, population growth, and the expanding electricity requirements of the digital economy is requiring sustained oil and gas exploration investment to replace depleting reserves with new discovered resources, ensuring continued demand for advanced seismic processing and interpretation software across global exploration theaters. The global transition to clean energy is paradoxically creating new geophysical software demand through both the battery minerals exploration boom and the emerging carbon capture and storage site characterization market, where subsurface seismic monitoring and integrity verification software is required to demonstrate long-term storage security for injected CO2.

Market Restraints:

High implementation costs, skilled talent shortages, data complexity challenges, and energy transition uncertainty creating adoption barriers and investment hesitancy

Geophysical software services encounter a number of barriers that limit their growth potential to levels lower than what would be possible with full deployment. The steep costs associated with the use and maintenance of geophysical software systems pose a considerable hurdle to independent exploration firms, junior miners, and national geological surveys that lack ample budget resources, thus making it difficult for such entities to adopt fully functional geophysical software packages. The problem of availability of qualified geoscientists capable of exploiting modern software platforms to interpret geophysical data poses a considerable barrier, because the available manpower does not match increased geophysical data and advanced software capabilities.

Market Opportunities:

Cloud platform expansion, energy transition geophysical applications, and emerging market exploration investment creating long-term growth opportunities

The geophysical software service market presents substantial growth opportunities across multiple strategic dimensions. The continued expansion of cloud-native SaaS platforms for geophysical processing and interpretation is creating opportunities to expand the total addressable market by serving exploration organizations that have been historically underserved by expensive on-premises enterprise software, including junior mining companies pursuing battery mineral exploration, independent oil and gas companies in emerging markets, and academic and government geological research institutions. The emerging carbon capture and storage market represents a significant new application domain for geophysical software services, as CCS site operators require sophisticated seismic monitoring, reservoir simulation, and subsurface integrity assessment software to manage injection programs and demonstrate long-term storage security to regulatory authorities and investors.

Recent Developments:

-

2025: Halliburton teamed up with Microsoft to offer strategic collaboration in creating geophysical cloud-based software solutions that would use Microsoft Azure cloud-based technology to offer scalable and elastic processing and interpreting of geophysical data, thus providing operators access to powerful seismic processing capabilities without having to spend money on building computing infrastructures.

-

2025: CGG, launched its innovative software package incorporating machine learning algorithms aimed at providing automated imaging and fault detection processes. This software greatly increased both efficiency and accuracy of seismic interpretations and drastically decreased the time needed to construct regional subsurface models.

Geophysical Software Service Market Key Players

Some of the Geophysical Software Service Market Companies

-

SLB (Schlumberger Limited)

-

CGG (Viridien)

-

Halliburton (Landmark Software)

-

TGS

-

Emerson Electric Co. (Paradigm)

-

Fugro

-

PGS (Petroleum Geo-Services)

-

Shearwater GeoServices

-

LMKR

-

Mira Geoscience Ltd.

-

iXblue (EXAIL Technologies)

-

Ikon Science

-

dGB Earth Sciences (OpendTect)

-

GeoTeric

-

Petrosys

-

Geovariances

-

Eliis

-

SeisWare International Inc.

-

Geophysical Insights

-

IHS Markit (S&P Global)

Geophysical Software Service Market Report Scop:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 17.07 Billion |

| Market Size by 2035 | USD 46.26 Billion |

| CAGR | CAGR of 10.51% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Software Type (On-premises, Software as a Service (SaaS)) • By Survey Type (Land-Based, Marine-Based, Aerial-Based) • By Application (Oil and Gas, Mineral and Mining, Water Exploration, Agriculture) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | SLB (Schlumberger Limited), CGG (Viridien), Halliburton (Landmark Software), TGS, Emerson Electric Co. (Paradigm), Fugro, PGS (Petroleum Geo-Services), Shearwater GeoServices, LMKR, Mira Geoscience Ltd., iXblue (EXAIL Technologies), Ikon Science, dGB Earth Sciences (OpendTect), GeoTeric, Petrosys, Geovariances, Eliis, SeisWare International Inc., Geophysical Insights, and IHS Markit (S&P Global) |

Frequently Asked Questions

Asia Pacific is expected to grow at the fastest CAGR of 12.31% in the Geophysical Software Service Market.

Oil and Gas dominated with approximately 42.15% share in 2025.

On-premises dominated with approximately 54.20% share in 2025.

The Geophysical Software Service Market was valued at USD 17.07 Billion in 2025.

The Geophysical Software Service Market is expected to grow at a CAGR of 10.51% from 2026 to 2035.

Get in Touch