Graphene Chip Market Report Scope & Overview:

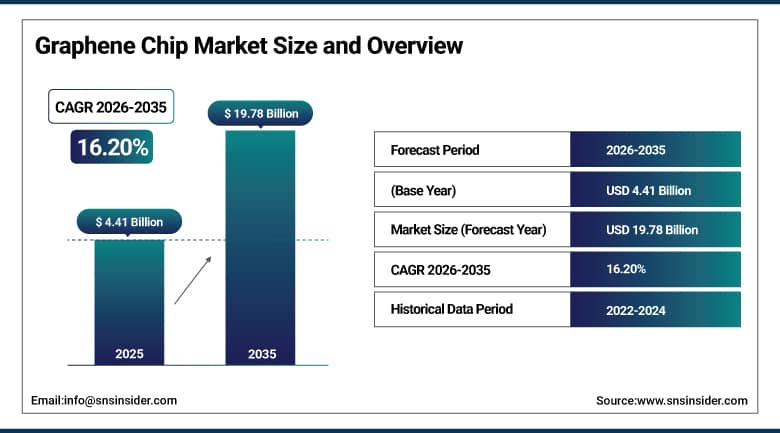

The Graphene Chip Market was valued at USD 4.41 billion in 2025 and is expected to reach USD 19.78 billion by 2035, growing at a CAGR of 16.20% from 2026–2035.

The graphene chip market is witnessing strong growth in the global market owing to the rising demand for high-performance nanoelectronics and advanced semiconductor devices. The increasing adoption of AI, IoT, and 5G technologies is promoting the usage of graphene-based chips in computing and communication applications. Investments made by organizations in next-generation semiconductor R&D and advanced materials innovation are contributing to market growth. Increasing developments in flexible electronics and high-speed transistors are playing a major role in driving the demand for graphene chip solutions. Growth in consumer electronics, automotive electronics, and aerospace applications is fueling the demand for graphene chip technologies.

According to the assessment made by the European Commission's Graphene Flagship, the EU program on graphene and related materials included more than 178 university and industry partners from 23 different countries, supported more than 200 organizations in collaboration networks, obtained more than 80 patents as well as created 20 spin-offs, and trained about 1,000 PhD and post-doctorate students for nanomaterials and semiconductor applications.

Market Size and Forecast:

-

Market Size 2026E: USD 5.12 billion

-

Market Size 2035: USD 19.78 billion

-

CAGR (2026 - 2035): 16.20%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get More Information On Graphene Chip Market - Request Free Sample Report

Graphene Chip Market Trends:

-

Graphene chip fabrication advances enable 40% higher electron mobility compared to silicon accelerating next-generation nanoelectronics integration across industries

-

Global R&D funding increased 35% 2025 for graphene-based semiconductor research driven by advanced photonics and RF applications demand

-

Wafer-scale graphene production capacity expands 28% in 2026 due to improved chemical vapor deposition techniques and yield optimization

-

Environmental regulations push 25% reduction in hazardous chemical usage in graphene chip manufacturing processes across semiconductor supply chains

-

Graphene-based RF chip adoption increases 32% in high-frequency communication systems driven by 5G-advanced and terahertz technology deployment

-

Hybrid graphene-silicon chip architectures achieve 30% reduction in power losses improving thermal management and next-generation AI processing efficiency

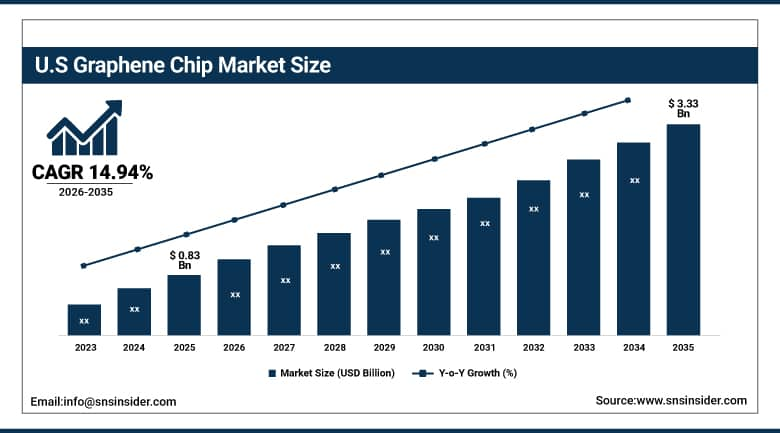

U.S. Graphene Chip Market Size Outlook:

The U.S. Graphene Chip Market was valued at USD 0.83 Billion in 2025 and is expected to reach around USD 3.33 Billion by 2035, growing at a CAGR of 14.94% from 2026–2035.

The U.S. Graphene Chip Market is witnessing strong growth because of increasing demand for advanced semiconductor innovation and AI-driven computing systems. Graphene chip deployment across defense electronics, high-performance computing, and communication infrastructure has been responsible for strong market expansion. Increasing investments by U.S. organizations in semiconductor R&D and nanotechnology development have led to rising demand for next-generation chip materials. Growing development of quantum computing, aerospace electronics, and 5G-enabled devices is further supporting market adoption. Continuous focus on technological leadership and advanced chip fabrication capabilities is strengthening market growth.

According to the CHIPS Program of the Department of Commerce of the United States, the share of semiconductor manufacturing capability in the United States has reduced to only 12% from the global total in 2020 compared to 37% in 1990. Microelectronics projects undertaken by the Department of Energy of the United States are further focusing on studies on advanced materials such as graphene semiconductor integration.

Graphene Chip Market Segment Analysis:

-

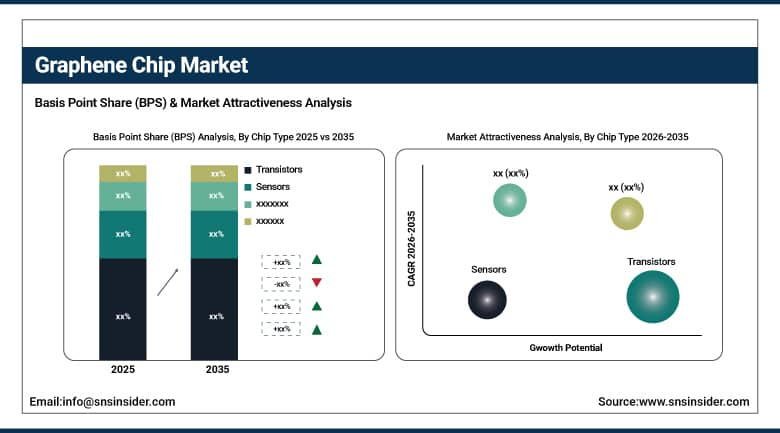

By Chip Type, transistors dominated the graphene chip market with 42.35% share in 2025; while sensors are the fastest growing segment with CAGR of 21.40% during 2026 to 2035.

-

By Application, electronics dominated the graphene chip market with 48.60% share in 2025; while aerospace is the fastest growing segment with CAGR of 21.13% during 2026 to 2035.

-

By Graphene Form, monolayer graphene dominated the graphene chip market with 39.20% share in 2025; while few-layer graphene is the fastest growing segment with CAGR of 18.41% during 2026 to 2035.

-

By Chip Size, 10 nm dominated the graphene chip market with 45.30% share in 2025; while 10–100 nm is the fastest growing segment with CAGR of 18.48% during 2026 to 2035.

By Chip Type, transistors dominated the graphene chip market in 2025, while sensors are the fastest growing segment.

Transistors emerged as the dominant market segment on the basis of revenue share in the global graphene chip market during 2025. The reasons behind the growth of this segment include the use of graphene chips in the production of high-speed switch, computing systems, and semiconductors. The advantage of graphene transistors over silicon transistors is that they offer greater electron mobility, lower power loss, and better thermal conductivity. Rising use in processors, communication, and miniaturized electronic systems would keep them dominant.

The sensors segment is expected to exhibit the fastest CAGR from 2026 to 2035. Reasons behind the growth of this segment include rising use of sensors in applications such as medical diagnostics, automotive safety devices, and environment monitoring devices. These types of sensors offer high sensitivity, fast reaction, and improved conductivity. Increasing adoption of sensors in IoT products, wearable devices, and intelligent infrastructures is anticipated to contribute towards their growing usage in the future.

By Application, electronics dominated the graphene chip market in 2025, while aerospace is the fastest growing segment.

The Electronics segment emerged as the dominating force within the Graphene Chip Market based on its revenue share in 2025 owing to growing preference for consumer electronics and semiconductors that deliver improved performance. They exhibit greater conductivity, faster switching speeds, and lower energy usage. Graphene-based chips are perfect for use in smartphones, personal computers, and wearable technology due to their efficiency. The widespread use of energy-efficient and small-sized components in the design of electronic products boosts its dominance within the market.

Aerospace industry registered the fastest CAGR during the forecast period owing to rising demands for lightweight, durable, and heat-resistant electronic components. Radiation resistance and robustness make graphene chips ideal for use in the aerospace industry. The rise in investment in satellite communication technology and space explorations coupled with technological innovations in avionics will fuel their adoption in future.

By Graphene Form, monolayer graphene dominated the graphene chip market in 2025, while few-layer graphene is the fastest growing segment.

Graphene Chip Market was led by Monolayer graphene chip and accounted for the dominated revenue share in 2025. Some of the factors contributing to the highest revenue generated can be attributed to their high electron mobility, electrical conductivity, and ultra-thin thickness, thus offering ultrafast switching characteristics. It has several applications in semiconductors and nanoelectronics. In addition to this, their wide usage and commercialization in fabricating semiconductor devices played a pivotal role in gaining their market leader position.

Few-layer graphene chip is expected to hold the fastest CAGR in the forecast period from 2026 to 2035. The highest CAGR can be contributed by its easy manufacturing process in comparison to monolayer graphene. It offers a combination of electrical, thermal, and mechanical properties ideal for sensors and flexible electronics. Moreover, increasing use in the automotive, aerospace, and energy sectors drives the demand for few-layer graphene chips.

By Chip Size, 10 nm dominated the graphene chip market in 2025, while 10–100 nm is the fastest growing segment.

The 10 nm segment ruled the Graphene Chip Market in terms of the dominated revenue share in 2025. The segment's dominance was attributed to its extensive application in computing systems and semiconductor fabrication processes. The established manufacturing ecosystem, along with its compatibility with traditional CMOS fabrication process, has augmented its demand. An increasing application in AI chips, consumer electronics, and communication devices has bolstered its dominance across the globe.

The 10–100 nm segment is predicted to register the fastest CAGR in 2026–2035 on account of growing demand for scalable and cost-effective architectures in graphene-based chips. The range represents an optimum combination of performance and scalability for future uses. Growing adoption of the segment in IoT-enabled devices, automobiles, and flexible electronics will further propel market growth. The increasing research activities related to nanotechnology and graphene-based material incorporation in mid-size chips will accelerate growth further.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025(%) |

|---|---|---|

|

North America |

United States |

71.40% |

|

Europe |

Germany |

27.50% |

|

Asia Pacific |

China |

43.20% |

|

Middle East & Africa |

UAE |

14.20% |

|

Latin America |

Brazil |

48.10% |

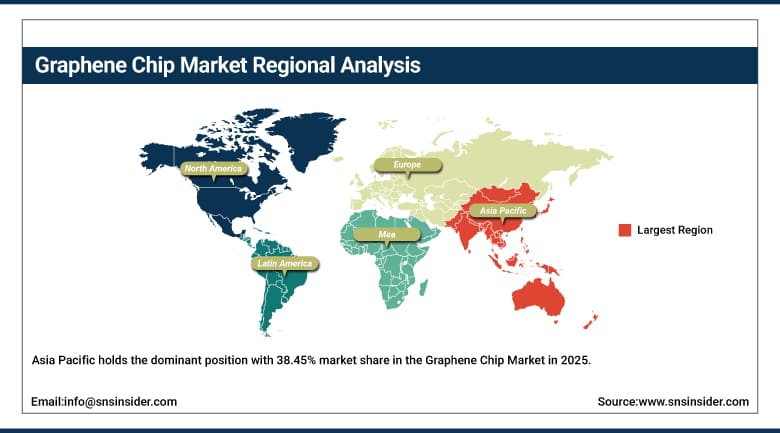

Asia Pacific Graphene Chip Market Insights.

Asia Pacific holds the dominant position with 38.45% market share in the Graphene Chip Market in 2025 and is also the fastest growing region with a CAGR of 17.99% due to strong demand expansion across semiconductor manufacturing and electronics production. China, Japan, South Korea, India, and Taiwan are key contributors. Rising demand for AI chips, consumer electronics, and 5G infrastructure is boosting adoption. Expanding semiconductor fabrication capacity, government-backed chip programs, and graphene material innovation are further strengthening regional market growth.

According to the Ministry of Industry and Information Technology of China and Taiwan Semiconductor Manufacturing Company annual disclosures, Asia Pacific accounts for over 70% of global semiconductor production capacity, with Taiwan contributing more than 50% of advanced logic chip output and South Korea dominating memory chip fabrication exceeding 60% global DRAM share. Japan supplies over 60% of global semiconductor materials including photoresists and wafers.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Graphene Chip Market Insights.

North America in Graphene Chip Market has seen its significant position in 2025 due to a strong semiconductor R&D ecosystem and advanced AI chip innovation. The region benefits from the presence of leading technology companies, defense electronics demand, and high-performance computing infrastructure. Increasing demand for nanoelectronics, quantum computing research, and advanced communication systems is driving steady growth across the United States and Canada. Strong investments in semiconductor fabrication, graphene material research, and digital transformation initiatives are further supporting market expansion.

As mentioned in the European Commission’s Graphene Flagship program, the North American graphene-assisted semiconductor innovation takes place through an international community network with over 200 institutions involved in nanomaterial research and development, while graphene semiconductor research revolves around developing methods that make graphene suitable for semiconductor chips. Based on data of Department of Commerce CHIPS for America program, over $30 billion worth of semiconductor manufacturing incentives have been committed to 40 projects since 2025 in support of chip fabrication and nanomaterial research.

Europe Graphene Chip Market Insights.

The Europe Graphene Chip Market makes an important contribution in 2025 owing to strong research initiatives in advanced materials and semiconductor innovation. Countries like Germany, United Kingdom, France, Italy, and Netherlands are leading contributors to regional demand. High focus on graphene research programs, automotive electronics, and industrial semiconductor applications is supporting consistent market growth. Increasing investments in EU semiconductor strategy and nanotechnology development programs are strengthening adoption across electronics and mobility sectors.

As stated by the European Commission, the European Union makes up around 12.7% of the world market of semiconductors (2023) and has set itself a goal to raise that number to 20% by 2030 through the Chips Act initiative. According to EU policy papers, semiconductor value chains continue to be highly consolidated despite their manufacturing capacity remaining small in Europe.

Middle East & Africa and Latin America Graphene Chip Market Insights.

The Middle East & Africa region along with Latin America will exhibit steady growth in the Graphene Chip Market up to 2025 due to increasing investments in digital infrastructure and telecommunications development. Countries such as UAE, Saudi Arabia, South Africa, Brazil, and Mexico are emerging contributors. Growing demand for smart electronics, broadband expansion, and industrial digitalization is increasing adoption. Infrastructure modernization and smart city projects are further driving market expansion.

Market Dynamics:

Growth Drivers: Rising demand for high performance nanoelectronics and advanced semiconductor computing systems across global industries

With rising needs for high-performance computing and nanoelectronics, the use of graphene-based chip technology is on the rise. Graphene chips have higher mobility of electrons, increased thermal conductivity, and fast signal processing capabilities than silicon-based chips. Therefore, these chips have been used to build artificial intelligence processors, quantum computers, and communication infrastructure among others. As the number of consumer electronic products increases along with developments in the fifth-generation mobile network infrastructure and data-based technologies, the need for graphene chips continues to increase.

According to European Commission in EU Chips Act, Europe aims to be 20% of the global semiconductor market by 2030. Also, the European Graphene Flagship project has received funding worth €1 billion in the span of ten years to promote the development of the use of graphene-based nano-materials. According to OECD, semiconductors-powered ICT goods form a considerable part of high-tech trade to promote computer systems growth.

Restraints: High production complexity and scalability challenges in large scale graphene chip manufacturing processes

The complexity of manufacturing procedures and the problem of obtaining consistent graphene quality have become impediments to widespread commercialization of graphene chips. Ensuring consistent atomic arrangement and free from defects layers is technically difficult. Integration of graphene technology into current silicon-based semiconductor fabrication plants makes manufacturing more complicated and expensive. The lack of specialized facilities has made scaling up of the manufacturing process difficult. The demanding nature of nanotechnology slows the pace of commercialization.

Opportunities: Growing integration of graphene chips in artificial intelligence, quantum computing, and high-speed data processing systems

The rising utilization of graphene chips in artificial intelligence as well as quantum computing systems opens up promising possibilities of future growth. The high electrical conductivity and rapid electron mobility makes them suitable for achieving higher speeds as well as improving energy efficiency. Rising needs of more sophisticated data centers, machine learning algorithms, and processors are pushing their use higher. Other new technologies such as edge computing and autonomous systems make their application possibilities even greater. Ongoing developments in semiconductor design and materials engineering will bring up possibilities of commercializing graphene chips.

According to IBM Research and its official quantum computing documentation, superconducting quantum processors have scaled beyond 100+ qubits, enabling exploration of advanced materials and nanoelectronics architectures relevant to graphene-based chips. As stated by the European Commission under Horizon Europe initiatives and the Graphene Flagship program, multi-institution research networks spanning 150+ academic and industrial partners support high-speed data processing and AI-oriented semiconductor innovation globally distributed research ecosystem development efforts ongoing collaboration

Recent Developments:

-

2026: Intel progresses foundry roadmap and AI chip manufacturing collaborations expanding advanced process technologies across global semiconductor ecosystem resilience growth strategy.

-

2025: TSMC expanded advanced packaging capacity in Taiwan and Arizona supporting AI demand and strengthening global semiconductor supply resilience ecosystems

-

2025: NVIDIA introduced Blackwell AI GPU platform expanding data center adoption and strengthening ecosystem partnerships for large scale computing workloads.

-

2024: Samsung increased investment in AI semiconductor R&D and EUV fabrication strengthening memory and logic chip innovation globally capacity expansion.

Graphene Chip Market Key Players are:

-

Samsung Electronics

-

Intel Corporation

-

Taiwan Semiconductor Manufacturing Company

-

Advanced Micro Devices

-

NVIDIA Corporation

-

Qualcomm Incorporated

-

Broadcom Inc.

-

STMicroelectronics

-

Infineon Technologies

-

SK hynix

-

IBM

-

Huawei Technologies

-

Semiconductor Manufacturing International Corporation

-

GlobalFoundries

-

Applied Graphene Materials

-

Haydale Graphene Industries

-

Versarien plc

-

Graphenea

-

NanoXplore Inc.

-

First Graphene Limited

Graphene Chip Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.41 Billion |

| Market Size by 2035 | USD 19.78 Billion |

| CAGR | CAGR of 16.20% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Chip Type (Transistors, Integrated Circuits, Memory Chips, Sensors, Displays) • By Application (Electronics, Automotive, Energy, Healthcare, Aerospace) • By Graphene Form (Monolayer Graphene, Few-Layer Graphene, Graphene Oxide, Reduced Graphene Oxide) • By Chip Size (10 nm, 10–100 nm, 100–1000 nm, 1000 nm) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Samsung Electronics, Intel Corporation, Taiwan Semiconductor Manufacturing Company, Advanced Micro Devices, NVIDIA Corporation, Qualcomm Incorporated, Broadcom Inc., STMicroelectronics, Infineon Technologies, SK hynix, IBM, Huawei Technologies, Semiconductor Manufacturing International Corporation, GlobalFoundries, Applied Graphene Materials, Haydale Graphene Industries, Versarien plc, Graphenea, NanoXplore Inc., First Graphene Limited |

Frequently Asked Questions

The graphene chip market is expected to grow at a CAGR of 16.20% from 2026 to 2035.

The graphene chip market was valued at USD 4.41 billion in 2025.

Rising demand for high-performance nanoelectronics, AI, IoT, 5G technologies, and advanced semiconductor innovation is driving global graphene chip demand.

Transistors dominated the market in 2025 due to their high electron mobility, low power loss, and wide use in advanced semiconductor devices.

Asia Pacific dominated the graphene chip market due to strong semiconductor manufacturing, high electronics production, and rapid AI and 5G adoption.

Get in Touch