Intelligent Battery Sensor Market Report Scope & Overview:

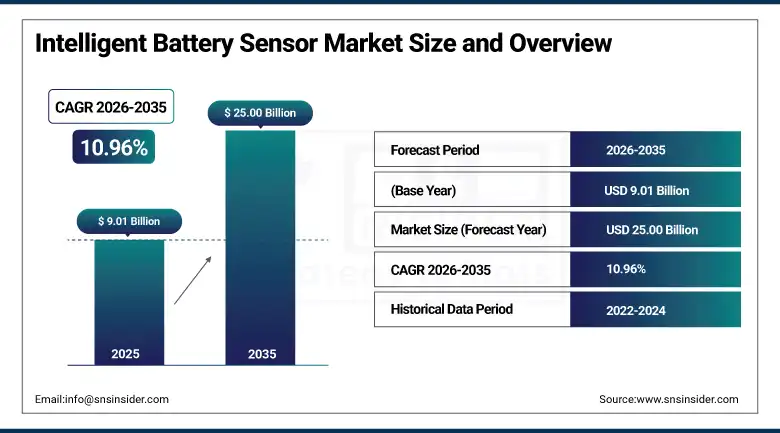

The Intelligent Battery Sensor Market was valued at USD 9.01 Billion in 2025 and is expected to reach USD 25.00 Billion by 2035, growing at a CAGR of 10.96% from 2026–2035.

The global intelligent battery sensor market is growing at an exceptional pace. Intelligent battery sensors (IBS) are advanced automotive and industrial electronic systems that continuously monitor battery voltage, current, temperature, and electrochemical state to enable real-time battery management system optimization, predictive state-of-charge assessment, state-of-health determination, and vehicle start-stop system management. The market is driven by rising adoption of electric and hybrid vehicles, increasing demand for battery management systems, integration of smart automotive technologies, and stringent emission regulations worldwide. IBS top trends include increasing adoption in electric and hybrid vehicles, fleet management systems, and renewable energy storage whose battery efficiency, health monitoring, real-time data accuracy, and failure detection capability improve battery performance and lifespan.

In 2024, Robert Bosch GmbH launched its next-generation Intelligent Battery Sensor with enhanced AI-powered electrochemical impedance spectroscopy capability for real-time battery health assessment in EV and 48V mild hybrid applications. The sensor’s AI-based degradation modelling provides more accurate remaining useful life prediction than conventional coulomb counting methods, enabling vehicle energy management systems to optimize charging strategy and driver range communication with substantially reduced anxiety-inducing range prediction error.

Market Size and Forecast

-

Market Size in 2026E: USD 9.99 Billion

-

Market Size by 2035: USD 25.00 Billion

-

CAGR: 10.96% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get more information On Intelligent Battery Sensor Market - Request Free Sample Report

Intelligent Battery Sensor Market Trends

-

Multi-parameter IBS integrating voltage, current, and temperature is replacing discrete sensors due to lower cost, smaller footprint, and simplified wiring.

-

AI-enabled IBS improves battery health prediction, state-of-charge accuracy, and remaining useful life estimation beyond traditional rule-based systems.

-

Growth of 48V mild hybrid vehicles is increasing demand for advanced IBS capable of managing dual-battery and multi-chemistry systems.

-

Fleet telematics integration with IBS enables predictive maintenance, reducing unexpected battery failures and improving operational efficiency in commercial vehicles.

-

Wireless IBS technologies using Bluetooth and Zigbee are reducing wiring complexity and lowering assembly costs in modern vehicle platforms.

U.S. Intelligent Battery Sensor Market Outlook

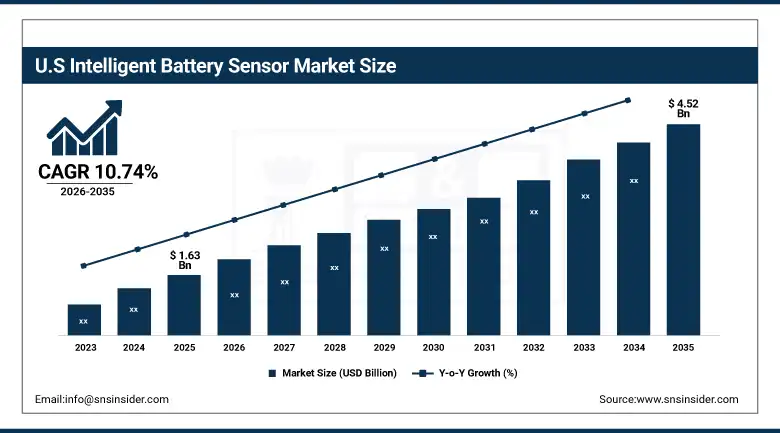

The U.S. Intelligent Battery Sensor Market was valued at approximately USD 1.63 Billion in 2025 and is expected to reach approximately USD 4.52 Billion by 2035, growing at a CAGR of approximately 10.74%.

The U.S. is the most commercially significant intelligent battery sensor market within North America. Robert Bosch’s U.S. automotive electronics operations, Continental AG’s North American commercial presence, HELLA’s U.S. distribution, and domestic tier-1 automotive electronics suppliers collectively define the North American IBS commercial landscape. The extraordinary U.S. EV market adoption, supported by IRA’s EV purchase credit, creates above-average IBS demand from Tesla, GM, Ford, and Stellantis’s EV platform battery management system specifications. The domestic start-stop system adoption in fuel-efficiency-focused ICE vehicles creates additional IBS procurement that compounds with the vehicle electrification transition.

Continental AG expanded its IBS product portfolio in 2024 with new battery monitoring solutions for 800V high-voltage EV architectures, addressing the growing demand from U.S. and European EV manufacturers whose battery pack voltages above 400V create IBS measurement range and isolation requirements substantially beyond the 12V and 48V systems that conventional IBS products were designed to serve.

Intelligent Battery Sensor Market Segment Analysis

-

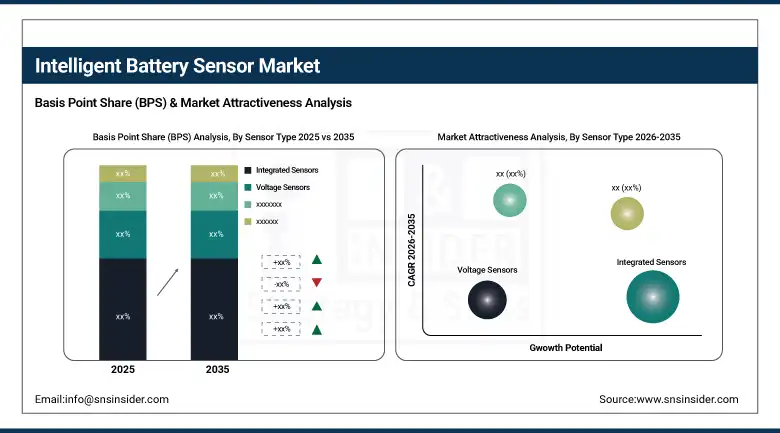

By Sensor Type, the Integrated Sensors segment dominated the intelligent battery sensor market with 38.9% share in 2025, while the Voltage Sensors segment is the fastest growing due to growing demand for real-time battery monitoring of electric vehicles and renewable energy storage systems whose precision voltage measurement creates accurate state-of-charge determination.

-

By Vehicle Type, the Passenger Vehicles segment dominated the intelligent battery sensor market with 47.8% share in 2025, while the Electric Vehicles segment is the fastest growing as dedicated EV battery management system requirements for multi-cell voltage monitoring, thermal management, and state-of-health prediction create above-average per-vehicle IBS content and commercial value.

-

By Communication Technology, the LIN segment dominated the intelligent battery sensor market with approximately 45% share in 2025, while the CAN/SPI segment is the fastest growing as higher-bandwidth communication requirements for EV multi-cell monitoring and 48V system real-time data transmission create structured adoption of faster communication protocols.

-

By Application, the Battery State of Charge Monitoring segment dominated the intelligent battery sensor market with approximately 38% share in, while the Start-Stop System Management segment maintained significant share as micro-hybrid proliferation creates structured IBS demand for predicting engine restart capability.

By Sensor Type, integrated sensors dominate, voltage sensors grow fastest

Integrated sensors retained the dominant type position with 38.9% of the intelligent battery sensor market in 2025. Integrated sensor’s commercial primacy reflects the automotive industry’s systematic pursuit of component consolidation that reduces bill of materials cost, wiring harness complexity, and PCB footprint. The combination of battery voltage measurement, charging/discharging current sensing, and ambient temperature monitoring in a single sensor package creates installation simplicity and connection point reduction that discrete multi-sensor architectures cannot achieve at equivalent total system cost. Bosch’s IBS, Continental’s current sensor module, and HELLA’s multi-parameter battery monitoring devices collectively demonstrate the integrated sensor category’s commercial leadership in automotive battery management infrastructure.

Voltage sensors are the fastest-growing type because EV battery pack’s individual cell voltage monitoring requirement creates a fundamentally different measurement architecture from conventional 12V lead-acid battery single-terminal voltage measurement. Each EV battery pack containing hundreds to thousands of individual cells requires cell-level voltage measurement whose aggregate sensing channel count creates substantial voltage sensor procurement that scales with EV production volume. Renewable energy storage system’s multi-cell lithium-ion battery voltage monitoring creates additional industrial voltage sensor procurement that compounds with grid storage capacity expansion.

By Vehicle Type, passenger vehicles dominate, EVs grow fastest

Passenger vehicles retained the dominant vehicle type position with 47.8% of the intelligent battery sensor market in 2025. The extraordinary global passenger vehicle production volume, exceeding 70 million units annually, creates aggregate IBS procurement whose scale substantially exceeds any other vehicle category. Each passenger vehicle’s battery monitoring requirement, whether for start-stop fuel economy system, 48V mild hybrid energy recovery, or full EV battery management, creates IBS procurement whose combined volume sustains passenger vehicles’ dominant commercial position. ICE vehicle’s continued production volume during the EV transition creates consistent standard 12V IBS procurement that sustains the category’s commercial dominance through the vehicle electrification transition period.

Electric vehicles are the fastest-growing vehicle type because each BEV’s substantially higher per-vehicle IBS content relative to ICE alternatives creates above-average revenue contribution per vehicle unit. While a conventional ICE vehicle requires a single 12V battery IBS, a typical BEV battery management system requires dozens to hundreds of voltages and temperature sensing points across the battery pack who’s combined per-vehicle IBS bill of materials creates commercial scale that sustains EV’s fastest-growing segment status even before the EV market’s extraordinary production volume growth compounding.

By Communication Technology, LIN dominates, CAN/SPI grows fastest

LIN retained the dominant communication technology position with approximately 45% of the intelligent battery sensor market in 2025. LIN protocol’s commercial primacy reflects its cost-optimized single-wire bus architecture whose lower implementation cost relative to CAN creates specification preference for standard 12V lead-acid battery monitoring applications where the sensor data bandwidth requirement is modest. LIN’s established automotive qualification and the extensive installed base of LIN-compatible battery management controllers create ecosystem momentum whose switching cost sustains LIN specification in new vehicle programmes where 12V battery monitoring remains the primary IBS application.

CAN and SPI are the fastest-growing communication technologies because EV battery management system’s real-time multi-cell data transmission requirement creates higher bandwidth communication needs that LIN’s single-wire low-speed architecture cannot satisfy with equivalent data latency performance. Each EV battery management system whose cell-level state-of-charge, state-of-health, and temperature monitoring requires low-latency data transmission creates CAN or SPI protocol adoption whose aggregate across the growing EV fleet creates commercial scale that sustains the faster communication technology’s growing market share.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Intelligent Battery Sensor Market Insights

North America is the fastest-growing regional intelligent battery sensor market, driven by IRA’s EV incentive creating above-average EV adoption, the domestic automotive industry’s 48V mild hybrid programme expansion, and fleet management telematics investment. The United States accounts for approximately 87.4% of North American revenues through Robert Bosch, Continental, HELLA, and Texas Instruments’ automotive electronics commercial operations.

Canada contributes approximately 12.6% of North American revenues through its automotive assembly industry’s IBS specification, the growing EV market’s battery management system procurement, and the commercial fleet sector’s telematics-integrated battery monitoring investment.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Intelligent Battery Sensor Market Insights

Europe is a technically sophisticated IBS market where EU CO₂ emission regulation’s fleet average target creates mandatory fuel economy technology investment, Robert Bosch’s German headquarters, Continental’s Hanover operations, and HELLA’s Lippstadt production create domestic supply. Germany accounts for approximately 22.3% of European revenues through its automotive OEM sector’s above-average hybrid and EV specification, the Tier 1 supplier’s European R&D center, and the premium vehicle segment’s advanced battery management investment.

France, Spain, and the Czech Republic are significant secondary markets where automotive assembly operations, European OEM supply chain localization, and growing EV production create consistent IBS procurement.

Asia Pacific Intelligent Battery Sensor Market Insights

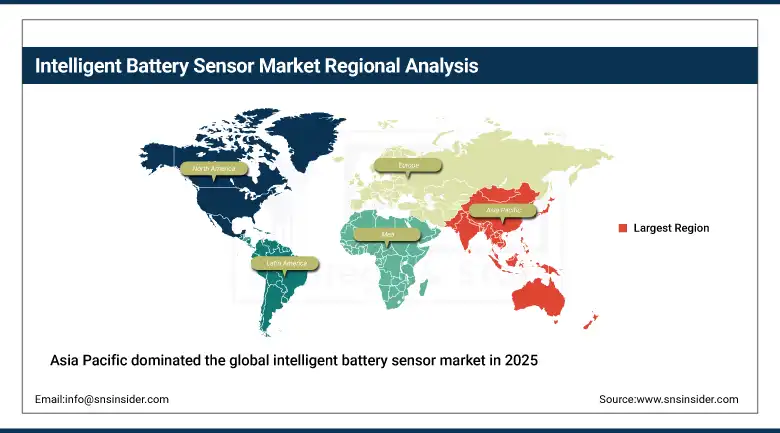

Asia Pacific dominated the global intelligent battery sensor market in 2025 as the world’s largest automotive production region. China accounts for approximately 44.8% of Asia Pacific revenues through its position as the world’s largest EV market whose BYD, SAIC, and Geely’s extraordinary EV production volume creates the most commercially significant IBS procurement globally. Japan’s Toyota’s hybrid system leadership and South Korea’s Hyundai-Kia’s EV programme create significant secondary markets whose sophisticated battery management system specifications create above-average per-vehicle IBS commercial value.

India’s rapidly growing automotive sector, including the two-wheeler market’s electric transition, creates growing IBS demand whose emerging market adoption creates above-average first-time procurement growth that compounds with vehicle electrification pace

MEA & Latin America Intelligent Battery Sensor Market Insights

UAE leads MEA revenues at approximately 38.4% through its premium vehicle import market’s above-average EV and hybrid specification, the growing EV adoption in the luxury segment, and the commercial fleet sector’s telematics battery monitoring investment. Brazil leads Latin American revenues at approximately 44.2% through its large automotive manufacturing sector’s IBS procurement, the growing hybrid vehicle adoption, and Bosch’s and Continental’s Brazilian operations.

Saudi Arabia’s EV adoption programme and South Africa’s automotive assembly industry create significant MEA secondary markets whose IBS procurement reflects progressive vehicle electrification and fuel economy programme adoption.

Market Dynamics

Growth Drivers: EV adoption creating above-average per-vehicle IBS content and emission regulation mandating fuel economy technology

Electric vehicle adoption is the intelligent battery sensor market’s most commercially transformative growth driver. Each ICE vehicle replaced by an EV creates a fundamental IBS content increase from a single 12V battery monitor to a multi-cell, multi-parameter battery management system whose per-vehicle IBS bill of materials represents above-average commercial value. IEA’s projection that EV sales will represent 45% of new vehicle sales by 2030 creates a commercial demand trajectory whose IBS revenue component grows disproportionately with EV market penetration because EV’s IBS content per vehicle substantially exceeds ICE alternatives.

Stringent emission regulations globally create fuel economy technology mandatory investment whose hybrid system and start-stop system content creates IBS specification across both electrified and conventional powertrain vehicle platforms. EU’s CO₂ fleet average target, CAFE standard’s progressive tightening, and China’s NEV mandate collectively create non-discretionary battery technology investment whose IBS component sustains procurement across all automotive market segments simultaneously.

Restraints: Cost pressure from automotive OEM procurement and supply chain concentration in semiconductor components

Automotive OEM procurement’s systemic cost reduction pressure creates IBS supplier margin compression whose annual price reduction target requirements create commercial challenge for IBS manufacturers whose component cost reduction must outpace OEM price concession demands. Each model year’s cost reduction programme creates procurement negotiation whose commercial outcome depends on IBS supplier’s manufacturing efficiency improvement and component cost reduction pace.

Semiconductor supply chain concentration creates IBS production continuity risk whose COVID-19 demonstration created automotive production stoppages that substantially impacted vehicle output. Each semiconductor shortage episode that delays IBS component availability creates vehicle production constraint whose commercial impact motivates automotive OEM procurement strategy toward supply chain diversification investment.

Opportunities: 800V EV architecture IBS development and fleet electrification battery management

800V EV architecture IBS development represents the most commercially premium near-term opportunity whose higher voltage measurement range, enhanced isolation requirement, and precision accuracy creates technical differentiation that conventional 400V and 12V IBS products cannot satisfy. Each new 800V EV platform from Porsche, Hyundai, and Kia whose charging speed advantage creates OEM competitive motivation creates new high-voltage IBS specification relationships whose commercial value substantially exceeds conventional 400V system alternatives.

Commercial fleet electrification battery management represents a growing premium opportunity whose fleet operator’s total cost of ownership optimization creates structured IBS procurement motivation beyond OEM standard specification. Each commercial fleet operator whose battery degradation monitoring and predictive replacement programme creates telematics-integrated IBS procurement sustains above-average revenue per vehicle relative to consumer passenger car IBS economics.

Recent Developments:

-

2024: Robert Bosch GmbH launched its next-generation Intelligent Battery Sensor with enhanced AI-powered electrochemical impedance spectroscopy capability in 2024 for real-time battery health assessment in EV and 48V mild hybrid applications, enabling more accurate remaining useful life prediction.

-

2024: Continental AG expanded its IBS product portfolio in 2024 with new battery monitoring solutions for 800V high-voltage EV architectures, addressing EV manufacturer demand for IBS measurement range and isolation requirements at above-400V battery pack voltages.

-

2024: HELLA GmbH launched its next-generation multi-parameter IBS in 2024 with enhanced wireless Bluetooth communication capability for battery monitoring in commercial vehicle and industrial battery applications where wired connection installation creates assembly complexity.

Intelligent Battery Sensor Market Key Players

-

Robert Bosch GmbH

-

Continental AG

-

HELLA GmbH & Co. KGaA

-

Delphi Technologies (BorgWarner)

-

Murata Manufacturing Co., Ltd.

-

Texas Instruments Inc.

-

NXP Semiconductors N.V.

-

Analog Devices Inc.

-

STMicroelectronics N.V.

-

Vishay Intertechnology Inc.

-

Inomatic GmbH

-

AMS AG (ams-OSRAM)

-

Furukawa Electric Co., Ltd.

-

Denso Corporation

-

Sensata Technologies

-

Elmos Semiconductor SE

-

Infineon Technologies AG

-

Marelli Holdings Co., Ltd.

-

Valeo SA

-

Aptiv PLC

Intelligent Battery Sensor Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 9.01 Billion |

| Market Size by 2035 | USD 25.00 Billion |

| CAGR | CAGR of 10.96% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Sensor Type (Integrated Sensors, Voltage Sensors, Current Sensors, Temperature Sensors, Others) • By Communication Technology (LIN/Local Interconnect Network, CAN/Controller Area Network, SPI/Serial Peripheral Interface, FlexRay, Others) • By Vehicle Type (Passenger Vehicles, Light Commercial Vehicles, Heavy Commercial Vehicles, Electric Vehicles, Two-Wheelers) • By Application (Battery State of Charge Monitoring, Battery State of Health Monitoring, Start-Stop System Management, Regenerative Braking, Battery Management System, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Robert Bosch GmbH, Continental AG, HELLA GmbH & Co. KGaA, Delphi Technologies (BorgWarner), Murata Manufacturing Co., Ltd., Texas Instruments Inc., NXP Semiconductors N.V., Analog Devices Inc., STMicroelectronics N.V., Vishay Intertechnology Inc., Inomatic GmbH, AMS AG (ams-OSRAM), Furukawa Electric Co., Ltd., Denso Corporation, Sensata Technologies, Elmos Semiconductor SE, Infineon Technologies AG, Marelli Holdings Co., Ltd., Valeo SA, and Aptiv PLC |

Frequently Asked Questions

The Intelligent Battery Sensor Market is expected to grow at a CAGR of 10.96% from 2026 to 2035.

The Intelligent Battery Sensor Market was valued at USD 9.01 Billion in 2025.

Rising adoption of electric and hybrid vehicles creating above-average per-vehicle IBS content growth, and stringent emission regulations worldwide mandating fuel economy technology investment whose battery monitoring component creates non-discretionary IBS procurement across all vehicle categories.

Integrated Sensors dominated the Intelligent Battery Sensor Market with 38.9% share in 2025 (SNS confirmed), while Voltage Sensors is the fastest growing segment.

Passenger Vehicles dominated the Intelligent Battery Sensor Market with 47.8% share in 2025 (SNS confirmed), while Electric Vehicles is the fastest growing segment.

Get in Touch