MEMS Sensors Market Report Scope & Overview:

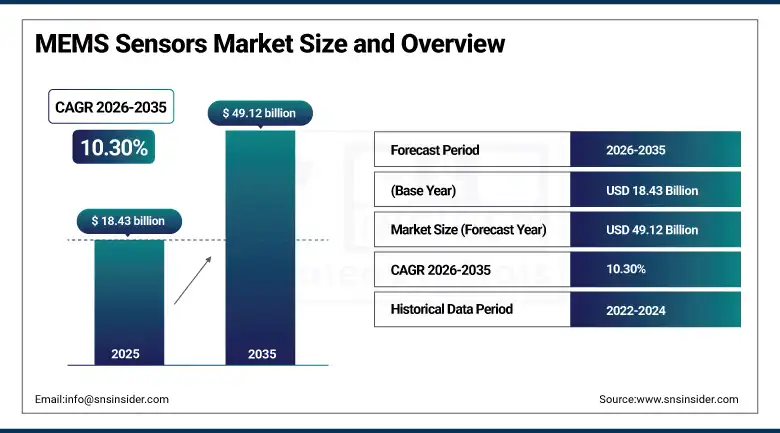

The MEMS Sensors Market was valued at USD 18.43 Billion in 2025 and is expected to reach USD 49.12 Billion by 2035, growing at a CAGR of 10.30% from 2026 to 2035.

Micro-Electro-Mechanical Systems sensors are miniaturized devices that integrate mechanical and electrical components on a single silicon chip using semiconductor fabrication techniques, enabling the precise measurement of physical and chemical phenomena including acceleration, angular rate, pressure, sound, magnetic field, and chemical composition in packages whose dimensions are measured in millimetres or less. MEMS technology has become the enabling substrate for the modern sensor economy, underpinning the motion tracking in every smartphone, the stability control in every modern vehicle, the blood pressure monitoring in wearable health devices, and the noise cancellation in earbuds. The commercial imperative driving MEMS sensor adoption across an expanding array of applications is the unmatched combination of miniaturization, mass-manufacturability, low power consumption, and declining unit cost that silicon MEMS fabrication delivers when scaled to the billions-of-units production volumes that smartphone, automotive, and IoT end markets require. No competing sensor technology combines these performance and economic characteristics at the production scale that MEMS achieves through its shared-process manufacturing infrastructure with the semiconductor industry.

In September 2024, Bosch Sensortec and Pirelli signed a joint development agreement to advance tyre-integrated MEMS sensor systems, combining Bosch's MEMS sensor precision with Pirelli's Cyber Tyre platform to deliver real-time tyre temperature, pressure, and deformation data to vehicle safety and dynamic control systems. The collaboration demonstrated the growing commercial value of embedding MEMS sensing intelligence within physical infrastructure components beyond conventional electronic modules, creating distributed sensing networks whose data density enables vehicle performance and safety optimization at the granularity that autonomous driving and advanced active safety systems require.

Market Size and Forecast

-

Market Size in 2026E: USD 20.33 Billion

-

Market Size by 2035: USD 49.12 Billion

-

CAGR: 10.30% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On MEMS Sensors Market - Request Free Sample Report

MEMS Sensors Market Trends

-

AI-enabled MEMS sensors are enabling edge processing, anomaly detection, and predictive maintenance capabilities.

-

Growing ADAS adoption is increasing MEMS sensor content per vehicle across automotive applications.

-

MEMS microphones are evolving toward voice recognition, acoustic analysis, and biometric authentication functions.

-

Expanding use of MEMS sensors in wearable and continuous health monitoring devices is supporting healthcare innovation.

-

Emerging MEMS chemical sensors for air quality, environmental monitoring, and gas detection are creating new growth opportunities.

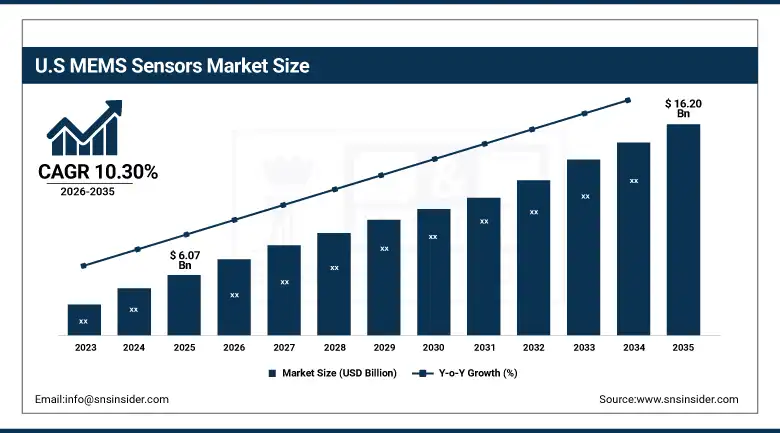

The U.S. MEMS Sensors Market Outlook

The U.S. MEMS Sensors Market was valued at approximately USD 6.07 Billion in 2025 and is expected to reach approximately USD 16.20 Billion by 2035, growing at a CAGR of approximately 10.30%. North America dominates the global MEMS sensors market through its concentration of major MEMS sensor manufacturers and system integrators, the world's most demanding automotive safety regulation environment that mandates advanced sensing infrastructure, and the commercial scale of its consumer electronics and defense sectors.

The United States' automotive industry generates the most commercially significant single national MEMS sensor demand category outside consumer electronics, driven by federal NHTSA mandates for electronic stability control, tire pressure monitoring, airbag systems, and backup cameras that collectively create non-discretionary MEMS sensor procurement across all passenger vehicles sold in the U.S. market. The commercial expansion of ADAS technology from luxury to mid-market vehicles is progressively adding radar, camera, and inertial sensor content per vehicle whose aggregate annual volume creates substantial incremental MEMS sensor demand.

In 2025, STMicroelectronics launched its LSM6DSV16BX smart IMU sensor incorporating an on-chip finite state machine and machine learning core that enables gesture detection, activity recognition, and motion classification directly within the sensor package without external processor involvement. The product demonstrated the commercial maturity of sensor-level AI inference whose ultra-low latency and energy efficiency, consuming less than 200 microamps during continuous motion classification, enables always-on intelligent motion sensing in hearables, wearables, and IoT devices whose battery life constraints make cloud-connected processing architecturally incompatible.

MEMS Sensors Market Segment Analysis

-

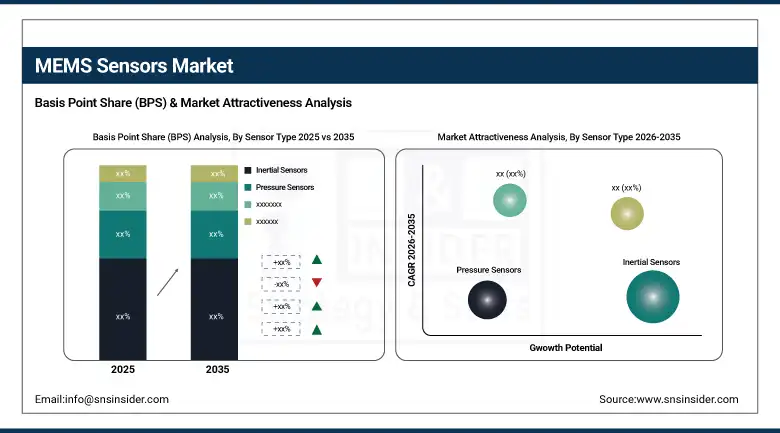

By Sensor Type, inertial sensors segment dominated the MEMS sensors market with 43.00% share in 2025, while the pressure sensors segment is the fastest growing sensor type with a CAGR of 11.43% during 2026 to 2035.

-

By Product Type, accelerometers segment dominated the MEMS sensors market in 2025, while the MEMS microphones segment is among the fastest growing product types during the forecast period.

-

By End User, the consumer electronics segment dominated the MEMS sensors market in 2025, while the healthcare segment is the fastest growing end user with an above-average CAGR during 2026 to 2035.

By Sensor Type, inertial sensors dominate, pressure sensors grow fastest

Inertial sensors, encompassing accelerometers, gyroscopes, and inertial measurement units, generated 43.00% of MEMS sensors market revenue in 2025. Their commercial dominance reflects the breadth and volume of applications whose motion detection, orientation tracking, and navigation requirements are most efficiently served by MEMS inertial sensing. The consumer electronics sector alone deploys multiple MEMS inertial sensors per smartphone for screen orientation, step counting, gaming interaction, image stabilization, and fall detection, creating per-device content that multiplies across billions of annual smartphone shipments into the highest-volume MEMS inertial sensor demand category globally.

Pressure sensors are growing fastest with a CAGR of 11.43%, driven by expanding deployment in automotive TPMS, medical respiratory monitoring devices, industrial process control, consumer barometric altitude estimation. The growing IoT infrastructure monitoring applications whose pressure sensing requirements are creating new MEMS market demand across application categories that did not previously require pressure measurement at consumer-grade cost points.

By End User, consumer electronics dominates, healthcare grows fastest

Consumer electronics generated the dominant end-user revenue share in 2025, reflecting the extraordinary MEMS sensor content per device that modern smartphones, wearables, hearables, gaming controllers, and smart home devices incorporate. A premium smartphone may contain eight or more distinct MEMS sensor types including accelerometer, gyroscope, barometric pressure sensor, microphone array, proximity sensor, ambient light sensor, and magnetometer whose combined per-device MEMS content value creates a large and commercially significant demand pool whose annual volume scales with global smartphone shipments exceeding 1.2 billion units.

Healthcare is growing fastest as the clinical and commercial validation of continuous physiological monitoring through MEMS-enabled wearable sensors establishes patient outcome improvement evidence that drives adoption beyond early technology enthusiast consumers into mainstream clinical practice and chronic disease management programmes. Implantable MEMS sensors for intracranial pressure monitoring, cardiac implant telemetry, and cochlear implant actuation represent a premium healthcare MEMS segment whose per-device value substantially exceeds consumer electronics equivalents, sustaining healthcare market value growth above volume growth rates.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.47% |

|

Europe |

Germany |

28.47% |

|

Asia Pacific |

China |

38.47% |

|

Middle East & Africa |

Israel |

22.84% |

|

Latin America |

Brazil |

43.84% |

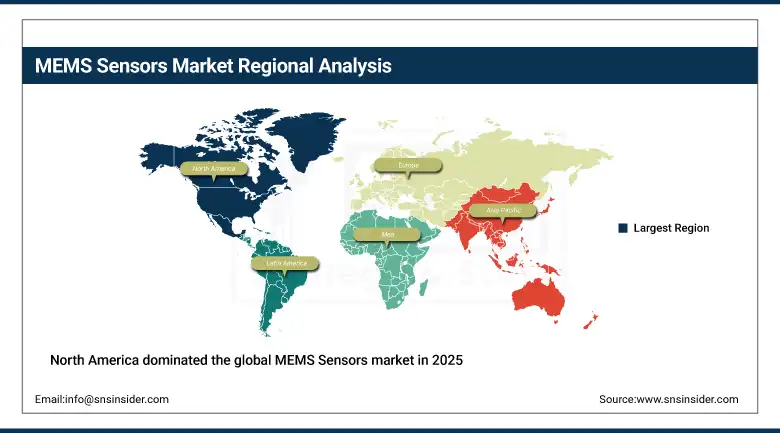

North America MEMS Sensors Market Insights

North America dominated the global MEMS Sensors market in 2025, holding the largest regional revenue share. The United States accounts for approximately 82.47% of regional revenue through its dual role as the world's most commercially advanced MEMS sensor end-market and the headquarters location of major MEMS technology companies including Analog Devices, Honeywell, Texas Instruments, Broadcom, and InvenSense. The commercial scale of the U.S. automotive sector, whose mandatory safety sensor content creates a structurally guaranteed baseline MEMS demand across tens of millions of annual vehicle builds, is the most commercially stable single national MEMS market driver globally. Defense procurement sustains a premium-priced high-reliability MEMS sensor segment whose annual contract value contributes significantly to North American MEMS revenue above its unit volume share.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe MEMS Sensors Market Insights

Europe held a significant share of global MEMS Sensors revenues in 2025. Germany, France, Switzerland, Italy, and the Netherlands are the leading national markets, each hosting significant automotive manufacturing, precision instrumentation, and electronics sectors whose MEMS sensor consumption spans automotive safety through industrial process monitoring through medical device applications. Robert Bosch GmbH, headquartered in Stuttgart, is the world's largest automotive MEMS sensor manufacturer whose ESP and airbag sensor production sustains Germany's position as the highest per-vehicle MEMS sensor consumption market in Europe. STMicroelectronics, whose main MEMS manufacturing facilities are located in Italy and France, represents European MEMS production capability that serves global consumer electronics and automotive markets from its advanced 200mm and 300mm MEMS wafer fabrication lines.

Asia Pacific MEMS Sensors Market Insights

Asia Pacific is the fastest-growing regional MEMS Sensors market, projected to expand at a CAGR of approximately 11.75% through 2035. China accounts for approximately 38.47% of Asia Pacific revenues through its dominant global position in consumer electronics manufacturing, its rapidly expanding automotive sector whose transition to electric vehicles is creating new MEMS sensor content opportunities per vehicle, and the growing domestic MEMS sensor manufacturing industry whose capabilities in inertial and pressure sensing are progressively competing with established Japanese, European, and U.S. suppliers. Japan contributes premium regional demand through Murata Manufacturing, TDK InvenSense, Seiko Epson, and Omron whose MEMS sensor portfolios serve both domestic and global markets in consumer electronics, automotive, and industrial applications. South Korea, Taiwan, and India each contribute growing regional demand through their electronics manufacturing sectors.

MEA & Latin America MEMS Sensors Market Insights

Middle East and Latin America are smaller but developing MEMS Sensors markets where growing electronics manufacturing, automotive sector development, and industrial automation investment are creating expanding commercial demand. Israel leads MEA revenues at approximately 22.84% of the regional total through its globally recognised semiconductor and sensor technology sector whose advanced MEMS research capabilities at institutions including the Weizmann Institute and Hebrew University generate commercialisable sensor technology that sustains a domestic MEMS innovation ecosystem. Brazil leads Latin American revenues at approximately 43.84% of the regional total through its automotive manufacturing sector, growing industrial automation investment, and the commercial presence of international MEMS sensor distributors whose supply chain activities generate regional market revenues.

Market Dynamics

Growth Drivers: Proliferation of IoT devices and automotive ADAS mandates creating structural per-device MEMS sensor content growth across billions of annual unit deployments

The MEMS sensors market's structural growth is powered by three simultaneously expanding demand forces. IoT device proliferation, whose global installed base exceeded 18 billion in 2025 and is projected to surpass 32 billion by 2030, creates incremental sensor demand from environmental, motion, and acoustic sensing. Automotive ADAS expansion from luxury to mid-market fitment adds sensing content per vehicle across annual builds of 80 to 90 million units globally. Declining MEMS unit costs driven by fab process maturation and competitive pricing simultaneously expand the addressable market by making sensing economically viable in application categories previously unable to justify instrumentation cost.

Restraints: MEMS fabrication complexity and the capital intensity of advanced MEMS wafer production create supply chain concentration risks and limit new entrant production capability

MEMS sensor manufacturing requires specialized fabrication processes including deep reactive ion etching, wafer bonding, sacrificial layer release, and hermetic packaging whose process complexity substantially exceeds standard CMOS semiconductor manufacturing and requires dedicated MEMS-compatible fabrication lines whose capital cost and process development investment create significant barriers to new production capacity entry. The concentration of MEMS wafer fabrication capacity among a limited number of qualified fabs in the United States, Europe, Japan, and increasingly China creates supply chain resilience risks during periods of demand surge or geopolitical disruption whose management requires strategic inventory and multi-source qualification investment from MEMS sensor buyers. The performance specifications required for automotive-grade and medical-grade MEMS sensors demand extended qualification programmes that can require 12 to 24 months of validation testing before production ramp, extending the time to revenue for new sensor product programmes and creating long product lifecycle commitments that limit commercial flexibility.

Opportunities: MEMS sensor integration with edge AI inference and expanding healthcare wearable applications represent the highest-value commercial growth frontiers

The integration of machine learning inference capability directly within MEMS sensor packages, enabled by the shrinking power and area requirements of dedicated neural processing units at sensor-compatible process nodes, is creating a new commercial category of smart sensors whose on-device intelligence eliminates the processing latency, energy cost, and privacy exposure of cloud-dependent signal interpretation. Smart MEMS IMUs that classify movement patterns, detect anomalies, and trigger conditional responses without external processor involvement represent a commercially compelling upgrade to the standard MEMS sensor that enables always-on intelligent monitoring at milliwatt power levels achievable from coin cell batteries or energy harvesting. Healthcare wearable MEMS sensors whose continuous physiological monitoring capability is validated by clinical outcome evidence, including the Apple Watch ECG feature's documented ability to detect atrial fibrillation in undiagnosed patients and the growing clinical evidence base for continuous blood pressure estimation through MEMS pulse wave sensors, are creating a healthcare MEMS market that commands premium pricing reflecting its clinical value and regulatory qualification investment.

Recent Developments:

-

2025: STMicroelectronics launched its LSM6DSV16BX smart IMU incorporating an on-chip finite state machine and machine learning core enabling gesture detection, activity recognition, and motion classification at under 200 microamps, demonstrating the commercial maturity of sensor-level AI inference for wearable, hearable, and IoT applications.

-

2024: Bosch Sensortec and Pirelli signed a joint development agreement integrating MEMS sensors into Pirelli Cyber Tyre systems, combining Bosch's MEMS sensor precision with Pirelli's tyre intelligence platform to deliver real-time pressure, temperature, and deformation data for vehicle safety and performance optimisation.

-

2024: TDK Corporation launched the AXO314 MEMS gyro accelerometer as part of its Tronics AXO 300 series for industrial applications, extending the portfolio with enhanced bias stability and vibration rejection performance targeting precision industrial navigation, platform stabilisation, and structural monitoring applications.

MEMS Sensors Market Key Players are:

-

Robert Bosch GmbH (Bosch Sensortec)

-

STMicroelectronics NV

-

Analog Devices Inc.

-

TDK Corporation (InvenSense)

-

Murata Manufacturing Co. Ltd.

-

Texas Instruments Incorporated

-

Infineon Technologies AG

-

Honeywell International Inc.

-

NXP Semiconductors NV

-

Knowles Corporation

-

Seiko Epson Corporation

-

Kionix Inc. (ROHM)

-

Panasonic Corporation

-

Omron Corporation

-

DENSO Corporation

-

Broadcom Inc.

-

First Sensor AG (TE Connectivity)

-

Sensata Technologies Holding NV

-

MEMSIC Semiconductor Co. Ltd.

-

Silicon Sensing Systems Ltd.

MEMS Sensors Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 18.43 Billion |

| Market Size by 2035 | USD 49.12 Billion |

| CAGR | CAGR of 10.30% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Sensor Type (Inertial Sensors, Pressure Sensors, Acoustic Sensors/MEMS Microphones, Optical Sensors, Chemical & Environmental Sensors, Others) • By Product Type (Accelerometers, Gyroscopes, Magnetometers, Pressure Sensors, Microphones, Others) • By End User (Consumer Electronics, Automotive, Healthcare, Industrial, Aerospace & Defense, Telecommunications, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Robert Bosch GmbH (Bosch Sensortec), STMicroelectronics NV, Analog Devices Inc., TDK Corporation (InvenSense), Murata Manufacturing Co. Ltd., Texas Instruments Incorporated, Infineon Technologies AG, Honeywell International Inc., NXP Semiconductors NV, Knowles Corporation, Seiko Epson Corporation, Kionix Inc. (ROHM), Panasonic Corporation, Omron Corporation, DENSO Corporation, Broadcom Inc., First Sensor AG (TE Connectivity), Sensata Technologies Holding NV, MEMSIC Semiconductor Co. Ltd., and Silicon Sensing Systems Ltd. |

Frequently Asked Questions

The MEMS Sensors Market is expected to grow at a CAGR of 10.30% from 2026 to 2035.

The MEMS Sensors Market was valued at USD 18.43 Billion in 2025.

Expanding IoT deployments, increasing ADAS adoption in vehicles, declining MEMS sensor costs, AI-enabled smart sensing capabilities, and growing demand for healthcare wearables are driving MEMS Sensors Market growth.

The inertial sensors segment dominated the MEMS Sensors Market with 43.00% share in 2025.

North America dominated the MEMS Sensors Market in 2025, holding the largest regional revenue share, with the United States accounting for approximately 82.47% of North American revenues.

Get in Touch