Optical Coating Market Report Scope & Overview:

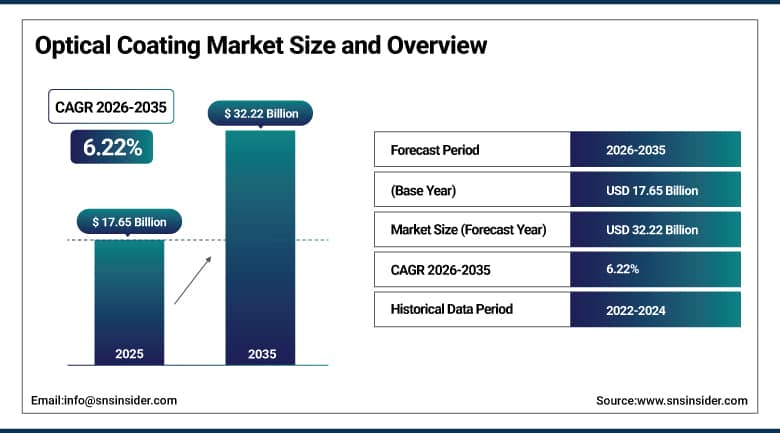

The Optical Coating Market was valued at USD 17.65 Billion in 2025 and is expected to reach USD 32.22 Billion by 2035, growing at a CAGR of 6.22% from 2026 to 2035.

The global optical coating market is evolving rapidly, driven by technological advancements and rising demand across industries including consumer electronics, aerospace, automotive, and renewable energy. Optical coatings are thin film layers deposited on optical components such as lenses, mirrors, prisms, and beam splitters to modify their reflection, transmission, and absorption characteristics, enabling the precise light management that modern optical systems require. Raw material availability and cost trends significantly impact production, with fluctuations in metals and dielectric materials influencing pricing across the supply chain. Growing environmental concerns are shaping sustainability trends and pushing manufacturers toward eco-friendly coating processes that reduce solvent emissions and hazardous material usage.

In 2024, Viavi Solutions expanded its FLEX optical coating platform with new high uniformity filter coating capability for hyperspectral imaging applications in agricultural yield assessment, environmental monitoring, and industrial quality inspection. The expansion addresses the growing hyperspectral imaging market whose per wavelength selectivity requirement creates premium filter coating demand that conventional bandpass filter manufacturing cannot cost effectively serve at the spectral resolution that machine vision and scientific imaging applications require.

Market Size and Forecast:

-

Market Size in 2026E: USD 18.75 Billion

-

Market Size by 2035: USD 32.22 Billion

-

CAGR: 6.22% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Optical Coating Market - Request Free Sample Report

Optical Coating Market Trends:

-

Growing adoption of anti-reflective coatings in OLED, AMOLED, smartphones, tablets, and AR/VR devices is improving display clarity, reducing glare, and enhancing energy efficiency

-

Rising deployment of LiDAR systems in autonomous vehicles and advanced driver assistance systems (ADAS) is driving demand for high-performance optical coatings that enhance sensor accuracy and reliability

-

Increasing use of atomic layer deposition (ALD) technology is enabling ultra-precise optical coatings with superior thickness control and uniformity for advanced optical components

-

Expanding investments in solar energy are accelerating demand for anti-reflective coatings that improve photovoltaic module efficiency and long-term outdoor performance

-

Growing defense and aerospace programs are boosting demand for durable, laser-resistant optical coatings designed to withstand harsh environmental conditions and high-energy laser applications

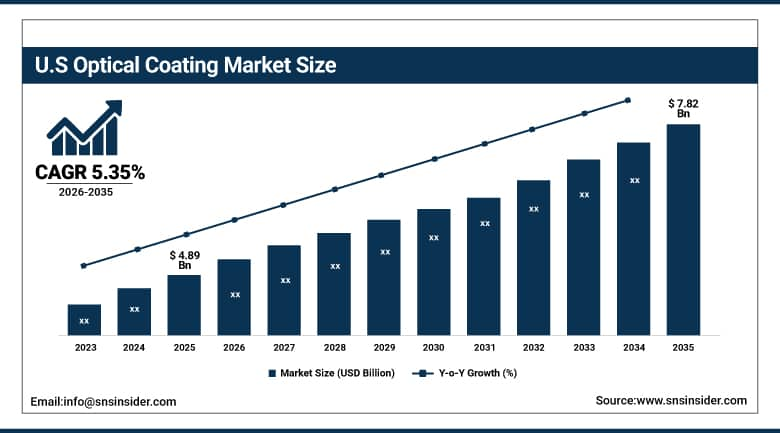

U.S. Optical Coating Market Outlook:

The U.S. Optical Coating Market was valued at approximately USD 4.89 Billion in 2025 and is expected to reach approximately USD 7.82 Billion by 2035, growing at a CAGR of approximately 5.35%.

The U.S. is the most commercially sophisticated optical coating market within North America's dominant regional position, driven by advancements in defense optics, consumer electronics, and telecommunications. Viavi Solutions, Materion Corporation, Edmund Optics, Optical Coating Laboratory, and Raytheon Technologies' optical component divisions collectively define the domestic commercial landscape. Increased investment in nanotechnology and photonics, supported by the National Institute of Standards and Technology's photonics programmes, fosters innovation in high performance coatings for precision applications. The demand for anti-reflective coatings in augmented reality devices and laser resistant coatings in military applications is rising, with sustainability initiatives by the Environmental Protection Agency encouraging the adoption of eco-friendly coating technologies that reduce solvent usage and eliminate heavy metal based coating materials.

In March 2023, Materion Corporation launched its advanced Optiform sputtered coating service expansion for high volume commercial optics, enabling precise uniformity and repeatability for anti-reflective and filter coatings applied to large format lenses for professional photography, cinema, and broadcast imaging applications. The expansion demonstrates the commercial direction of precision optical coating services toward reproducibility at scale that custom coating runs cannot achieve, addressing the optical performance consistency requirement of professional imaging equipment manufacturers whose interchangeable lens systems require matched coating performance across production batches.

Optical Coating Market Segment Analysis:

-

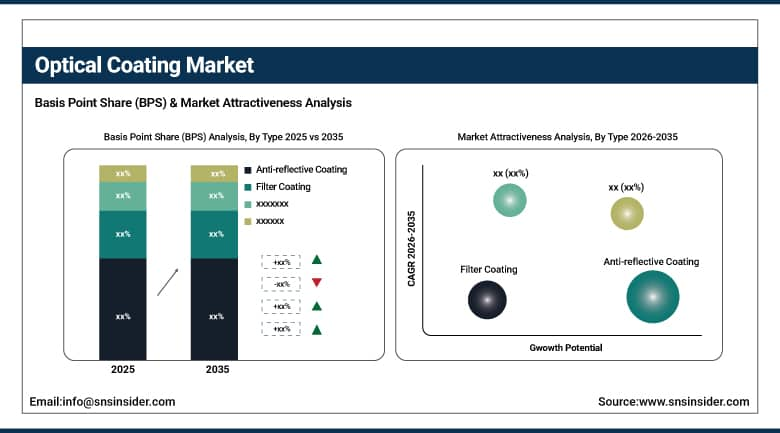

By Type, the Anti-reflective Coating segment dominated the Optical Coating Market with approximately 38% share in 2025, while the Filter Coating segment is the fastest growing.

-

By Technology, the Sputtering Process segment dominated the Optical Coating Market with approximately 42% share in 2025, while the Ion-Assisted Deposition technology segment is the fastest growing.

-

By End-use Industry, the Consumer Electronics segment dominated the Optical Coating Market with approximately 34% share in 2025, while the Solar Power segment is the fastest growing.

By Type, anti-reflective coating dominates, filter coating grows fastest

Anti-reflective coatings retained the dominant type position with approximately 38% of the optical coating market in 2025. Their commercial primacy reflects the extraordinary application breadth of AR coating across virtually every optical system category, from consumer smartphone camera lenses whose multi-layer AR coating reduces surface reflection to below 0.1%, to solar panel modules whose silicon nitride AR coating improves light trapping efficiency by 3 to 5 percentage points of absolute module efficiency. The National Renewable Energy Laboratory has documented that anti-reflective coatings on solar modules improve performance in high irradiance environments while simultaneously reducing the levelised cost of energy, creating measurable commercial value that sustains investment in module AR coating even in cost competitive utility scale procurement environments. BMW and Tesla's incorporation of anti-glare coatings in head-up displays and ADAS optical systems demonstrates the automotive sector's systematic AR coating adoption that adds a commercially significant new procurement stream beyond traditional consumer electronics and scientific instrument applications.

Filter coatings are the fastest growing type because hyperspectral imaging's commercial expansion across agricultural precision monitoring, environmental surveillance, food quality inspection, and industrial process control creates above average procurement for narrowband spectral selection coatings whose per wavelength precision creates premium specification requirements. Viavi Solutions' FLEX platform expansion for hyperspectral filter coatings and the growing telecom wavelength division multiplexing market's demand for dense wavelength filters collectively demonstrate the commercial momentum of filter coating's fastest growing designation. Each new LiDAR programme for autonomous vehicle or robotics application whose wavelength selection requirement specifies narrowband filter coatings creates procurement that compounds with the global autonomous driving technology development investment.

By Technology, sputtering dominates, ion-assisted deposition grows fastest

The sputtering process retained the dominant technology position with approximately 42% of the optical coating market in 2025. Magnetron sputtering's commercial dominance reflects its combination of coating density, uniformity, adhesion, and scalability to large area substrates that vacuum evaporation alternatives cannot match for volume production of anti-reflective and conductive coatings. Each consumer electronics display manufacturing facility whose large format glass coating requires consistent optical performance across the full substrate area creates sputtering system procurement whose technology advantages in coating uniformity directly translate to reduced optical component rejection rate and improved production yield. The architectural glass market's low emissivity and solar control coating requirements, whose large format glass substrate coating at high throughput creates the most commercially intensive sputtering process application, further sustains the technology's dominant market position.

Ion-assisted deposition is the fastest growing technology because the defence optical system market's laser damage resistance requirement, the space optics market's radiation hardness and thermal cycling durability requirement, and the precision scientific instrument market's environmental stability requirement collectively create above average procurement for the superior coating density, adhesion, and durability that IAD produces relative to conventional vacuum evaporation. Each defence programme that specifies laser resistant optical coatings for targeting systems, range finders, or directed energy weapon beam delivery optics creates IAD coating procurement whose technical performance requirement excludes conventional evaporation alternatives. The progressive expansion of IAD from defence into commercial applications including medical imaging optics and high performance camera lenses sustains the technology's fastest growing designation.

By End-use Industry, consumer electronics dominates, solar power grows fastest

Consumer electronics retained the dominant end-use industry position with approximately 34% of the optical coating market in 2025. The extraordinary production volume of smartphones, tablets, laptops, cameras, and emerging AR and VR devices creates the most commercially concentrated optical coating procurement of any industry. Each flagship smartphone model whose multi-camera system contains four to six lenses per module creates anti-reflective coating procurement whose aggregate across 1.4 billion annual smartphone shipments defines the commercial scale of consumer electronics optical coating demand. The OLED and AMOLED display market's adoption of circular polariser stacks incorporating anti-reflective optical coating films, and the progressive expansion of display area per device across smartphones and tablets, create growing per-unit optical coating content that compounds with device production volume growth.

Solar power is the fastest growing end-use industry because photovoltaic module deployment's extraordinary growth trajectory, driven by renewable energy mandates, declining system cost, and utility scale procurement, creates proportional AR coating demand whose commercial aggregate grows with global solar installation capacity. Each gigawatt of solar capacity installed creates optical coating procurement whose aggregate across the industry's annual installation volume of over 400 GW globally creates above average demand growth. Bifacial solar module adoption whose rear surface AR coating creates additional coating procurement per module, and perovskite solar cell development whose thin film coating architecture creates new optical coating specifications, collectively sustain solar power's fastest growing industry designation.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

31.2% |

|

Latin America |

Brazil |

44.2% |

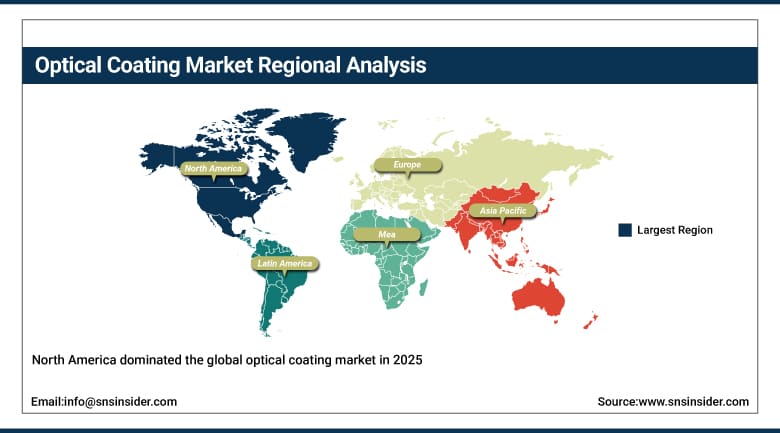

North America Optical Coating Market Insights

North America dominated the global optical coating market in 2025, supported by advanced manufacturing capabilities, robust research and development infrastructure, and significant investments in defence optics, smart city technologies, and consumer electronics. The United States accounts for approximately 87.4% of North American revenues through Viavi Solutions, Materion Corporation, Edmund Optics, Optical Coating Laboratory, and Raytheon Technologies' optical divisions whose combined commercial operations define the domestic precision coating supply landscape.

Canada contributes approximately 12.6% of North American revenues through its telecommunications optical component manufacturing, defence optics programme procurement, and the growing clean technology sector's solar coating investment that sustains consistent optical coating procurement across both commercial and government customer segments.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Optical Coating Market Insights

Europe is a technically sophisticated optical coating market where the defence optical system procurement of major NATO member states, the automotive industry's AR and HUD coating demand, and the scientific instrument market's precision coating requirements create structured institutional procurement. Germany accounts for approximately 22.3% of European revenues through SCHOTT AG's optical glass and coating operations, Carl Zeiss Vision's eyewear coating, and the automotive OEM sector's display and sensor coating demand.

The United Kingdom, France, and the Netherlands are significant secondary markets where BAE Systems’ defence optics programme, Airbus Optronics’ aerospace coating requirements, and ASML’s semiconductor lithography optical component coating create consistent premium specification procurement. Multilayer GmbH and Laser Components GmbH sustain European commercial supply from established precision coating manufacturing operations.

Asia Pacific Optical Coating Market Insights

Asia Pacific is the fastest growing regional optical coating market, driven by China’s extraordinary consumer electronics and solar panel manufacturing scale, Japan’s precision optics and camera lens industry, South Korea’s display and semiconductor manufacturing, India’s growing electronics production, and the region’s combined solar energy deployment acceleration. China accounts for approximately 44.8% of Asia Pacific revenues through its position as the world’s largest consumer electronics and solar panel manufacturer whose combined optical coating demand creates the most commercially concentrated single country procurement of any market.

Japan represents the most technically sophisticated optical coating market within Asia Pacific where Nikon’s and Hoya’s camera lens coating operations, Canon’s optical manufacturing, and Tokyo Electron’s semiconductor optical component coating create precision specification procurement that sustains Japan’s position as a global leader in advanced optical coating technology beyond its market scale.

MEA & Latin America Optical Coating Market Insights

The UAE leads MEA revenues at approximately 31.2% through its solar energy infrastructure investment, the defence sector’s optical system procurement, and the smart city infrastructure’s architectural glass coating demand. Saudi Arabia’s Vision 2030 solar energy programme and NEOM’s advanced materials investment add complementary Gulf demand. Brazil leads Latin American revenues at approximately 44.2% through its solar energy expansion, the growing consumer electronics market, and the defence sector’s optical system procurement. Mexico’s electronics manufacturing and Chile’s solar energy sector collectively sustain regional market growth through 2035.

Market Dynamics:

Growth Drivers: Consumer electronics optical innovation and solar energy deployment creating proportional coating demand

Consumer electronics optical innovation is the optical coating market's most commercially pervasive structural growth driver. The smartphone industry's systematic multi-camera adoption, whose progression from single rear camera to quad camera configurations across flagship and mid-range devices, creates proportional increase in anti-reflective lens coating procurement per device. Each new AR and VR device platform whose optical assembly contains multiple precision lenses, beam splitters, and polarising elements creates above average per-unit optical coating content that compounds with the platforms' user base growth. The professional imaging sector's progression toward higher resolution and lower reflection optical systems sustains premium coating specification investment that conventional coating alternatives cannot satisfy.

Solar energy deployment’s extraordinary global acceleration creates proportional anti-reflective coating demand whose commercial scale grows with annual solar installation capacity. Renewable energy mandates across the EU, India’s national solar mission, and U.S. Inflation Reduction Act incentives collectively create solar installation volumes that sustain above average optical coating procurement growth throughout the forecast period. Each bifacial module whose dual surface AR coating requirement creates twice the coating content per module further amplifies the per-GW optical coating procurement intensity.

Restraints: High capital cost of precision coating equipment and raw material supply chain concentration

High capital investment requirements for advanced optical coating systems, particularly multi-chamber sputtering and ion beam systems whose per-unit equipment cost ranges from USD 2 million to over USD 20 million for large area configurations, create significant entry barriers for new market participants and limit capacity expansion flexibility for established manufacturers. Each coating specification upgrade that requires new deposition equipment investment creates capital expenditure demand whose payback period requirement moderates the pace of technology adoption in commercially cautious manufacturing environments.

Raw material supply chain concentration for rare earth oxides, hafnium dioxide, tantalum pentoxide, and other specialty dielectric coating materials whose geographic production concentration creates supply disruption risk and pricing volatility. China’s dominance in rare earth element production creates strategic procurement risk for optical coating manufacturers outside China whose material supply security requires diversification investment that moderates commercial flexibility.

Opportunities: AR and VR optical system demand and hyperspectral imaging filter coating

Augmented and virtual reality optical system development represents the most commercially transformative near-term growth opportunity for precision optical coatings. Each AR and VR headset platform whose waveguide display architecture requires diffractive and reflective optical coatings with nanometre-scale precision creates above average coating procurement whose premium performance specification sustains pricing substantially above conventional anti-reflective coating commodity markets. The projected consumer AR and VR device market growth creates a compounding demand driver whose optical coating content per device substantially exceeds smartphone equivalents.

Hyperspectral imaging filter coating development represents the most commercially premium filter coating application whose narrowband spectral selection precision creates differentiated commercial relationships with agricultural technology, environmental monitoring, and industrial machine vision customers whose measurement accuracy requirements sustain above-commodity pricing for validated filter performance specifications.

Recent Developments:

-

2024: Viavi Solutions expanded its FLEX optical coating platform in 2024 with new high uniformity filter coating capability for hyperspectral imaging applications in agricultural assessment, environmental monitoring, and industrial quality inspection, addressing the growing machine vision market's spectral precision requirements.

-

2024: SCHOTT AG launched its new AR coating optimised optical glass series for EV head-up display applications in 2024, providing enhanced coating adhesion on curved glass substrates and improved anti-reflective performance across the broadband visible spectrum for automotive display readability in varying ambient light conditions.

-

2023: Materion Corporation expanded its Optiform sputtered coating service in March 2023 with high volume commercial optics capability, enabling precise uniformity and repeatability for anti-reflective and filter coatings on large format lenses for professional photography, cinema, and broadcast imaging applications.

-

2023: Optical Coating Laboratory (OCLI), a Viavi company, was awarded a U.S. defence contract in 2023 for advanced laser damage resistant coatings for next-generation directed energy weapon optical systems, demonstrating the growing defence procurement for IAD-deposited precision coatings with enhanced laser fluence tolerance.

-

2023: Edmund Optics introduced a new series of hard-coated UV-VIS-NIR broadband anti-reflective coatings in 2023 with improved environmental durability under MIL-C-48497 specification testing, targeting aerospace and scientific instrumentation applications requiring long duration optical performance stability under thermal cycling and humidity exposure.

Optical Coating Market Key Players:

-

Viavi Solutions Inc.

-

Materion Corporation

-

SCHOTT AG

-

Edmund Optics Inc.

-

Optical Coating Laboratory Inc. (OCLI)

-

Carl Zeiss AG

-

Hoya Corporation

-

Nikon Corporation

-

Raytheon Technologies Corporation

-

Singulus Technologies AG

-

Applied Materials Inc.

-

Leybold GmbH

-

Satisloh AG

-

Optorun Co. Ltd.

-

II-VI Incorporated

-

Abrisa Technologies

-

Laser Components GmbH

-

Multilayer GmbH

-

Cascade Optical Corporation

-

Chroma Technology Corporation

Optical Coating Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 17.65 Billion |

| Market Size by 2035 | USD 32.22 Billion |

| CAGR | CAGR of 6.22% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Type (Anti-reflective Coating, Reflective Coating, Filter Coating, Conductive Coating, Electrochromic Coating, Others) • by Technology (Vacuum Deposition Technology, E-Beam Evaporation Technology, Sputtering Process, Ion-Assisted Deposition (IAD) Technology) • by End-use Industry (Consumer Electronics, Healthcare, Architecture, Aerospace & Defense, Automotive, Telecommunication, Solar Power, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Viavi Solutions Inc., Materion Corporation, SCHOTT AG, Edmund Optics Inc., Optical Coating Laboratory Inc. (OCLI), Carl Zeiss AG, Hoya Corporation, Nikon Corporation, Raytheon Technologies Corporation, Singulus Technologies AG, Applied Materials Inc., Leybold GmbH, Satisloh AG, Optorun Co. Ltd., II-VI Incorporated, Abrisa Technologies, Laser Components GmbH, Multilayer GmbH, Cascade Optical Corporation, Chroma Technology Corporation |

Frequently Asked Questions

The Optical Coating Market is expected to grow at a CAGR of 6.22% from 2026 to 2035.

The Optical Coating Market was valued at USD 17.65 Billion in 2025.

Consumer electronics optical innovation creating growing anti-reflective coating procurement per device through multi-camera system adoption, and solar energy deployment growth creating proportional AR coating demand that compounds with global solar installation capacity expansion rates.

Anti-reflective Coating dominated with approximately 38% share in 2025, while Filter Coating is the fastest growing segment.

North America dominated the Optical Coating Market in 2025, while Asia Pacific is the fastest growing region driven by China's consumer electronics and solar manufacturing scale.

Get in Touch