The Organic Scintillators Market Report Scope & Overview:

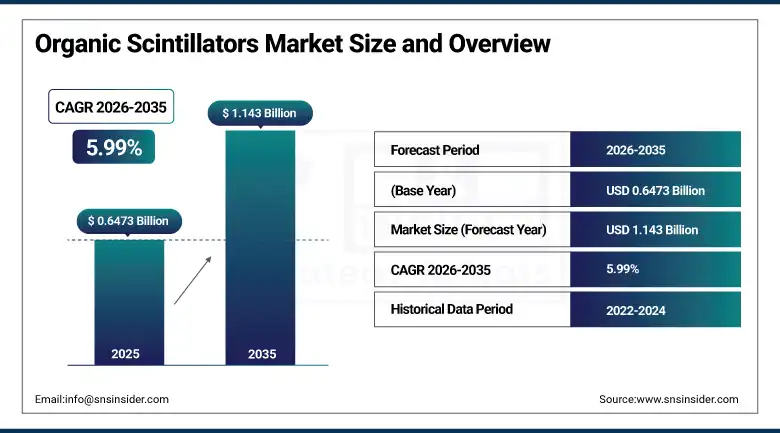

The Organic Scintillators Market was valued at USD 0.6473 Billion in 2025 and is projected to reach USD 1.143 Billion by 2035, expanding at a CAGR of 5.99% during the forecast period 2026–2035.

Scintillators such as Plastics, liquids, and crystal play a big role in imaging and monitoring systems. You'll find them in nuclear medicine, radiation monitoring, physics research, and industrial testing. These materials are becoming more popular. This may be due to increased investment in nuclear safety and the installation of more PET systems. Hospitals and security checkpoints are also upgrading their radiation detectors. Scientists are using AI to improve scintillators for better pulse discrimination and signal processing. Some now have fiber integration, so also improved wavelength conversion.

Some now have fiber integration, so also improved wavelength conversion. Advanced organic scintillator detectors with AI pulse-shape discrimination and cloud-connected data management are being ordered by defense and research teams, showing they’re quickly upgrading nuclear detection systems around the world.

Market Size and Forecast

-

Market Size 2026E: USD 0.6771 Billion

-

Market Size 2035: USD 1.143 Billion

-

CAGR: 5.99% from 2026 to 2035

-

Fastest Growing Region: Middle East & Africa

-

Largest Region: North America

To Get more information On Organic Scintillators Market - Request Free Sample Report

Organic Scintillators Market Trends

-

AI-integrated signal processing and pulse-shape discrimination workflow expansion

-

Rising deployment of RFID-enabled scintillator inventory tracking systems in nuclear facilities

-

Expansion of cloud-based radiation monitoring and real-time event analytics platforms

-

Increasing sterilization compliance and certified calibration traceability for medical-grade scintillators

-

Growth in demand for customized high-performance organic crystal scintillator assemblies

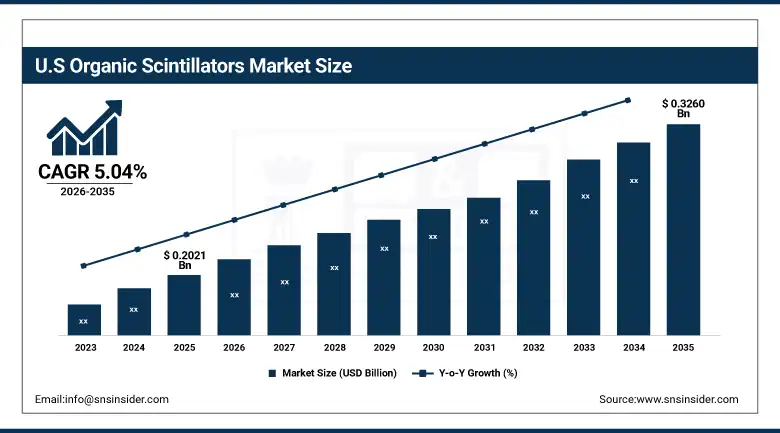

The U.S. Organic Scintillators Market Size Outlook

The U.S. Organic Scintillators Market was valued at USD 0.2021 Billion in 2025 and is projected to reach approximately USD 0.3260 Billion by 2035, expanding at a CAGR of 5.04% during 2026–2035

They’ve invested heavily in advanced medical imaging and defense radiation monitors. Federal teams, DOE labs, and top research centers keep purchasing scintillator systems for physics and security work. Hospitals and imaging facilities across the nation are shifting to digital scintillators. These use smart coincidence detection and cloud-based image retrieval.

This tech is the biggest money-maker because of high demand from nuclear power plants, government groups, industrial radiography firms, and hospitals. It’s really leading the way right now.

In 2025-2026, several U.S. nuclear detection programs got AI-assisted scintillator detectors that use cloud data and RFID for tracking. This big upgrade helped with real-time radiation monitoring at key research and security sites.

Organic Scintillators Market Segment Analysis

-

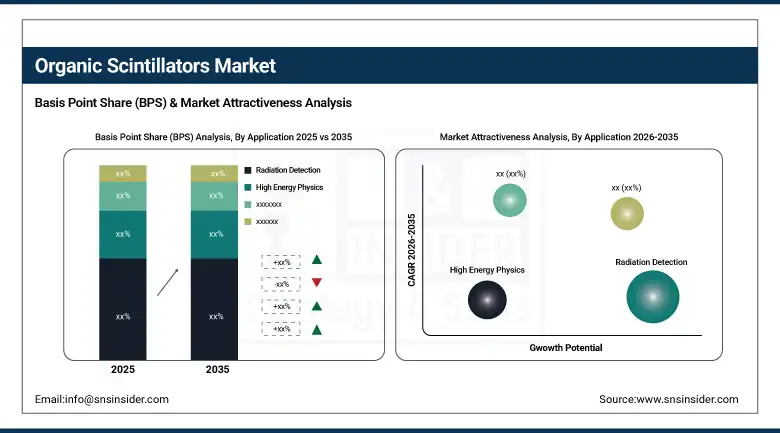

By Application, the radiation detection segment dominated with a 32.00% share in 2025, while industrial applications is projected to witness the fastest growth through 2035.

-

By Type, plastic scintillators held a 48.40% market share in 2025, while organic crystal scintillators are projected to register the highest CAGR of 7.39% through 2035.

-

By Form Factor, standard scintillator products dominated with a 65.00% share in 2025, while the customized segment is projected to register the fastest growth at 7.44% CAGR.

-

By End User, research institutions held the largest share of 38.00% in 2025, while the defense and security segment is projected to register the fastest growth during the forecast period.

By Application: radiation detection segment dominates; industrial applications segment fastest growing.

In 2025, the radiation detection segment made about USD 0.2071 billion, staying the biggest earner due to strong demand from nuclear power plants, government groups, industrial radiography firms, and hospitals. The push for mandatory adherence to both national and global safety standards keeps driving purchases of scintillator-based tools across radiation-controlled zones. Looking ahead, industrial applications is expected to grow the quickest with a 11.21% annual rate until 2035. This growth comes from bigger investments in key particle physics projects, facility upgrades, and the spread of advanced next-gen systems needing top-notch organic scintillator parts.

In 2025, the industrial applications segment dominated with about USD 0.2071 billion. This was thanks to nuclear power plants, government groups, industrial radiography firms, and hospitals needing lots of safety equipment. So, it stayed the top earner.

By Type: plastic scintillators segment dominates; organic crystal scintillators segment is fastest-growing.

The growth is due to the increasing investment in large physics projects and upgrades, and the growing adoption of advanced systems that require high-quality organic scintillator components. Plastic scintillators created a leading 48.40% market share with approximately USD 0.313 billion in 2025 due to their extensive use in radiation portal monitors, vehicle inspection systems, handheld detectors, and gamma-ray spectroscopy equipment.. On the other hand, organic crystal scintillators are expected to register the fastest growth with a Compound Annual Growth Rate of 7.39% during the forecast period. They’re increasingly used in very sensitive neutron detectors, beta-radiation measuring tools, and top-of-the-line liquid scintillation counters.

In 2026, several national nuclear safety agencies upgraded their radiation checkpoint tech. They bought plastic scintillator portal systems with RFID tracking, AI threat detection, and cloud logging platforms.

By Form Factor: standard segment dominates; customized segment is fastest-growing.

The standard form factor segment accounted for approximately USD 0.421 billion in 2025, representing 65.00% of the market. The segment’s dominance was due to its affordability, many suppliers, and good compatibility with existing systems. They were also easier to certify for critical locations such as hospitals and nuclear facilities. In the meantime, the customized segment was the fastest growing part of the business and was set to grow at 7.44% per annum. This was because specialized groups need unique shapes and tailor-made properties that you don’t get off the shelf.

By 2026, manufacturers had increased the design of custom organic scintillator components with complex geometries and special fibers, aiming at the major physics centers and defense teams, improving the performance of their equipment and detectors.

By End Use: research institutions segment dominates; defense & security segment is fastest-growing.

In 2025, research institutions contributed around USD 0.246 billion, snagging the largest end-use share. This highlights how key organic scintillator tech is to experimental nuclear physics, particle physics, astrophysics, and materials science. The primary buyers, big national labs, uni-based nuclear research centers, and international physics groups. These folks bulk order for major detectors but also pick specialty parts for development projects. For defense and security, things look set to grow the fastest at an 8.19% CAGR till 2035. This is due to continuous government spending on better rad portal monitoring, improved nuke mat detect capabilities, plus upgrading systems.

Advanced organic scintillator detectors with AI for neutron-gamma separation and RFID for tracking were rolled out by defense agencies. This upgrade boosted radiation detection at borders and key infrastructure sites, making security way better.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

40.01% |

|

Europe |

Germany |

25.00% |

|

Asia Pacific |

China |

22.00% |

|

Middle East & Africa |

UAE |

5.99% |

|

Latin America |

Brazil |

7.00% |

North America Organic Scintillators Market Insights

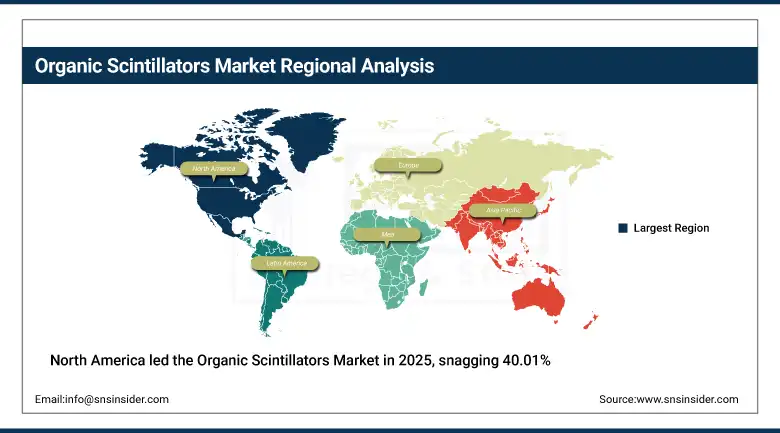

North America led the Organic Scintillators Market in 2025, snagging 40.01% of the global revenue. The US was the main player here, accounting for 78.02%, driven by active spending from the Department of Energy, Department of Homeland Security, and top physics research universities. Canada chipped in with the rest, holding 21.98% of regional revenue. This split was due to increasing investment in nuclear operations oversight and studies in neutron detection back in Canada. So, both countries benefited from strong funding in nuclear, medical, and defense areas.

In 2025-2026, several U.S. security agencies bought more advanced plastic scintillator portal systems. These had AI for signal sorting and cloud-based event analysis. This made radiation monitoring better at key borders and facilities.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Organic Scintillators Market Insights

In 2025, Europe made up around 25% of the global Organic Scintillators Market. This is thanks to its highly skilled customers, including big names in particle physics, nuclear watchdogs, and high-tech med imaging firms. Germany, France, the UK, and Switzerland are way out front in Europe when it comes to nuclear research, top-notch healthcare tech, and strict radiation safety rules. Approved scintillators continue to be in high demand, with the EU insisting on proper paperwork, material certifications and precise calibrations. They are a staple product for hospitals, industrial X-ray users and nuclear sites.

Some European companies released new organic scintillator detectors with AI capabilities that could tie into the Cloud and track component life cycles with RFID in 2026. They worked well in both academic physics and hospital radiation safety.

Asia Pacific Organic Scintillators Market Insights

Asia Pacific represented approximately 22.00% of global Organic Scintillators Market revenue in 2025, emerging as the most dynamically growing major regional market driven by expanding nuclear power infrastructure, accelerating investment in advanced physics research programs. China maintained the dominant national contributor position within the region, supported by major state-funded particle accelerator construction programs, expanding nuclear power plant monitoring requirements, and growing domestic production capability in organic scintillator material science. Japan, South Korea, and India represent the next tier of commercially significant national markets, characterized by mature nuclear power operational monitoring demand, advanced medical imaging adoption, and growing academic physics research investment.

Several Asia Pacific-based nuclear technology providers and physics research institutions expanded procurement of advanced organic scintillator detector arrays integrated with AI-assisted pulse-shape discrimination and real-time cloud monitoring platforms during 2025–2026.

Middle East & Africa and Latin America Organic Scintillators Market Insights

The Middle East and Africa region is projected to register the highest CAGR of approximately 7.63% during the forecast period, driven by accelerating investment in nuclear energy infrastructure development, expansion of homeland security radiation monitoring networks, and growing adoption of advanced nuclear medicine imaging systems within premium healthcare facilities. National nuclear energy programs in the UAE, Saudi Arabia, and Egypt are creating sustained demand for radiation monitoring instrumentation, including organic scintillator-based portal systems and environmental monitoring arrays.

By 2026, operators of nuclear energy programs in the Middle East purchased more advanced radiation monitoring systems. These include organic scintillators with AI and cloud connections for improved event management, aligning with the region’s goals to update nuclear safety tech.

Market Dynamics

Growth Drivers: Expanding nuclear safety infrastructure and medical imaging investment accelerating organic scintillator adoption.

The organic scintillator market is growing due to higher nuclear safety investments, more PET and SPECT use in health care, and bigger high-energy physics projects. Plus, governments are boosting radiation detection at borders and nuclear sites by using new plastic and liquid scintillators and updating tech. Hospitals are also chipping in by expanding nuclear medicine departments and adding these detectors to top-of-the-line PET machines. On top of that, they’re leveraging AI, cloud technology, and RFID to enhance detection capabilities in various areas.

Radiation monitoring system providers ramped up cloud-connected organic scintillator detectors with AI and RFID. This upgrade helps spot threats and manage component lifecycles more effectively. Safety monitoring is now far more advanced and digital because of these changes.

Restraints: Performance trade-offs, regulatory certification complexity of materials, and market penetration constraints.

The demand for organic scintillators market is high, but there are some major commercial challenges as well. This is related to the material performance limitations and strict regulatory approvals in the nuclear and medical applications. Compared to the inorganic counterparts such as sodium iodide and lanthanum bromide, the organic range is lacking. They produce less light, have poorer energy resolution, and don't absorb photons as well either. So, they struggle in gamma-ray spectroscopy, which needs top-notch precision.

Several scintillator technology developers reported extended regulatory review timelines for advanced organic scintillator formulations intended for medical imaging applications, reflecting increasing scrutiny of novel material compositions and performance characterization requirements under applicable regulatory frameworks

Opportunities: AI-integrated detection platforms and smart nuclear infrastructure creating long-term commercial potential.

The move toward AI based radiation detection systems is creating huge opportunities for those working on organic scintillator technology. These advances in technology help modern digital systems better process information. This is pushing the need for top-notch scintillator materials that play nicely with hi-tech gear. Smart hospitals, too, are revamping their nuclear medicine set-ups. Centralized AI management and real-time detector checks mean there's lots of ongoing maintenance. It's driving the creation of super-stable scintillator parts essential for reliable digital imaging.

Multiple organic scintillator material developers and detection system integrators expanded AI-assisted radiation monitoring platforms incorporating advanced pulse-shape discrimination, RFID-enabled component tracking, and cloud-based operational analytics to serve growing smart nuclear infrastructure procurement programs.

Recent Developments

-

2026: Multiple advanced organic scintillator detector system providers launched AI-integrated radiation portal monitoring platforms incorporating cloud-based event analytics and RFID-enabled component lifecycle tracking for national border security infrastructure programs.

-

2026: Several nuclear medicine technology developers advanced commercial deployment of next-generation organic scintillator PET detector modules featuring enhanced coincidence timing resolution and AI-assisted image reconstruction algorithms.

-

2025: Leading organic scintillator manufacturers introduced enhanced plastic scintillator formulations with improved radiation hardness and light yield characteristics for deployment in high-flux particle physics research environments

-

2025: Multiple radiation monitoring infrastructure operators expanded adoption of cloud-connected organic scintillator monitoring systems integrated with AI-driven signal discrimination and centralized RFID-based detector inventory management platforms.

Organic Scintillators Market Key Players are:

-

Saint-Gobain Crystals (Scintillation Products Division)

-

Amcrys Ltd.

-

Rexon Components & TLD Systems Inc.

-

Eljen Technology

-

SCIONIX Holland B.V.

-

Hamamatsu Photonics K.K.

-

Epic Crystal Co. Ltd.

-

Nuvia a.s.

-

Zecotek Photonics Inc.

-

Kuraray Co., Ltd.

-

Dynasil Corporation of America

-

Radiation Monitoring Devices Inc. (RMD)

-

Bicron (formerly a Saint-Gobain brand)

-

CRYTUR spol. s r.o.

-

Ametek Inc. (Ortec Division)

-

Berthold Technologies GmbH & Co. KG

-

Scintacor Ltd.

-

Scionix USA Inc.

-

Applied Scintillation Technologies Ltd.

-

LabLogic Systems Ltd

The Organic Scintillators Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 0.6473 Billion |

| Market Size by 2035 | USD 1.1430 Billion |

| CAGR | CAGR of 5.99% from 2025 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Market Size Analysis, Revenue Forecasting, Segment Analysis, Competitive Landscape, Regional Analysis, Radiation Detection Technology Assessment, Nuclear Medicine Integration, High Energy Physics Applications, Industrial Scintillation Use Cases, Defense & Security Procurement Trends, Research Institution Adoption Analysis, Customized vs. Standard Scintillator Demand Assessment, Plastic vs. Liquid vs. Organic Crystal Performance Benchmarking, End-Use Sector Investment Analysis, Hospital and Research Infrastructure Trends, Regulatory Compliance Analysis (NRC, IAEA, FDA), AI-Driven Material Optimization, Supply Chain Disruption Assessment, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Application (Nuclear Medicine, Radiation Detection, High Energy Physics, Industrial Applications) • By Type (Plastic Scintillators, Liquid Scintillators, Organic Crystal Scintillators) • By End Use (Healthcare, Research Institutions, Defense & Security) • By Form Factor (Standard Scintillators, Customized Scintillators) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Russia, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America) |

| Company Profiles | Saint-Gobain Crystals, Amcrys Ltd., Rexon Components & TLD Systems Inc., Eljen Technology, SCIONIX Holland B.V., Hamamatsu Photonics K.K., Epic Crystal Co. Ltd., Nuvia a.s., Zecotek Photonics Inc., Kuraray Co., Ltd., Dynasil Corporation of America, Radiation Monitoring Devices Inc. (RMD), Bicron (formerly a Saint-Gobain brand), CRYTUR spol. s r.o., Ametek Inc. (Ortec Division), Berthold Technologies GmbH & Co. KG, Scintacor Ltd., Scionix USA Inc., Applied Scintillation Technologies Ltd., LabLogic Systems Ltd. |

Frequently Asked Questions

The Organic Scintillators Market was valued at USD 0.6473 Billion in 2025.

The market is projected to reach USD 1.143 Billion by 2035.

The market is expected to expand at a CAGR of 7.39% during the forecast period.

North America dominated the global market owing to deep institutional investment in nuclear safety infrastructure, advanced medical imaging systems, and defense-grade radiation monitoring networks, accounting for 40.01% of global revenue in 2025.

Plastic Scintillators accounted for the largest revenue share of 48.40% in 2025, driven by widespread deployment across radiation portal monitors, handheld dosimetry instruments, and gamma-ray spectroscopy platforms.

Get in Touch