Precision Harvesting Market Report Scope & Overview:

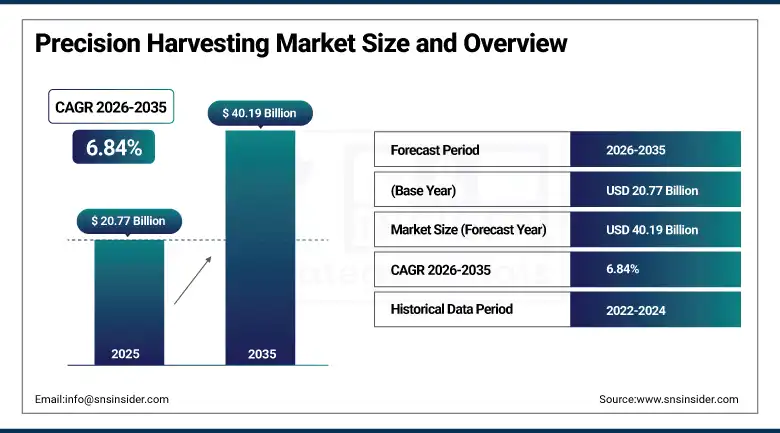

The Precision Harvesting Market was valued at USD 20.77 Billion in 2025 and is expected to reach USD 40.19 Billion by 2035, growing at a CAGR of 6.84% from 2026-2035.

The global precision harvesting market is growing at a significant pace. It encompasses the technologies, equipment, and data systems that enable accurate, efficient, and minimally wasteful crop collection including GPS-guided combine harvesters, AI-enabled harvesting robots, yield monitoring systems, and data analytics platforms that optimize harvest timing and field coverage. The market is driven by rising global food demand, critical agricultural labor shortages prompting automation investment, IoT and AI-enabled equipment creating data-driven harvest optimization, and government sustainability initiatives supporting smart farming adoption.

On 5 June 2025, John Deere announced two new forage harvesting products to improve forage quality, fuel savings, and efficiency. The products feature up to 1,020PS horsepower and HarvestMotion Plus technology that automatically adjusts feed roll speed to maintain consistent crop throughput. The development reflects John Deere's commercial strategy of combining mechanical performance improvement with digital precision control whose combined value proposition sustains premium specification in large-scale forage harvesting operations globally.

Market Size and Forecast

-

Market Size in 2026E: USD 22.19 Billion

-

Market Size by 2035: USD 40.19 Billion

-

CAGR: 6.84% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Precision Harvesting Market - Request Free Sample Report

Precision Harvesting Market Trends

-

AI yield prediction optimizes harvest timing using crop maturity, weather, and market price data.

-

Autonomous harvesting robots expand due to labor shortages and declining manufacturing costs globally.

-

Telematics enables real-time monitoring of harvesting fleets, improving efficiency, fuel use, and coverage.

-

Variable rate technology adjusts combine parameters using crop sensing, reducing grain loss significantly.

-

Government subsidies in major economies accelerate precision harvesting adoption among small and medium farmers.

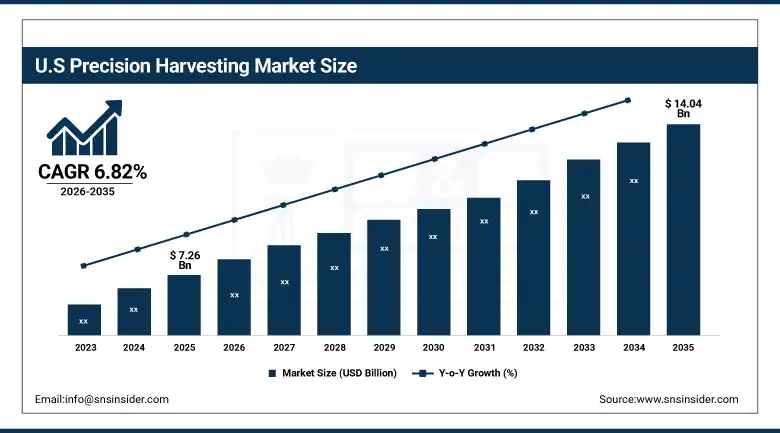

The U.S. Precision Harvesting Market Outlook

The U.S. precision harvesting market was valued at approximately USD 7.26 Billion in 2025 and is expected to reach approximately USD 14.04 Billion by 2035, growing at a CAGR of approximately 6.82%.

The U.S. is the world's most commercially sophisticated precision harvesting market within North America's dominant revenue position. John Deere, AGCO Corporation, and CNH Industrial's Case IH brand collectively define the North American precision harvesting commercial and technology landscape. The extraordinary scale of U.S. grain production across the Corn Belt, the wheat belt's combine harvester fleet, and the California specialty crop sector's labor-driven robotic harvesting adoption collectively create the world's most commercially diverse precision harvesting demand. USDA's precision agriculture support programmes and the Farm Bill's conservation technology provisions create structured government procurement motivation.

AGCO Corporation launched the Fendt IDEAL 10T combine harvester in 2024 with enhanced AI-driven threshing system that automatically adjusts separation parameters based on real-time grain loss sensing, reducing harvest losses by up to 15% compared to conventional fixed-parameter threshing systems. The launch reflects the commercial direction of premium combine harvester development toward autonomous performance optimization whose sensor fusion and machine learning capability creates operational improvements that justify premium pricing over conventional mechanical alternatives.

Precision Harvesting Market Segment Analysis

-

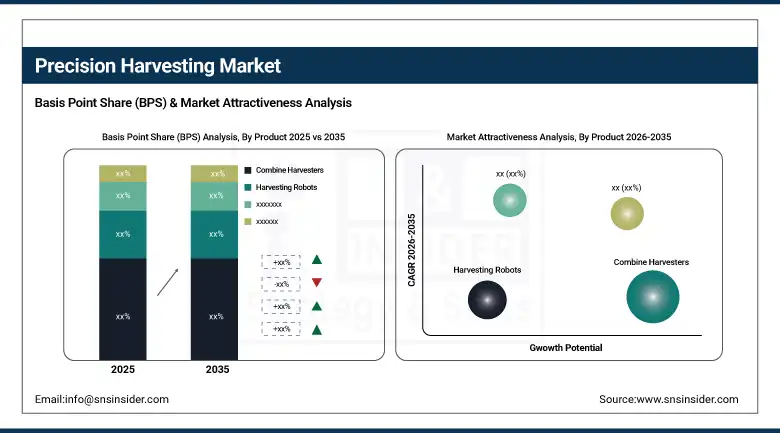

By Product, the combine harvesters segment dominated the market with 58% share in 2025, while the harvesting robots’ segment is the fastest growing as AI and robotics advancement combined with agricultural labor shortages drive autonomous picking system adoption.

-

By Offering, the hardware segment dominated the market with approximately 65% share in 2025 owing to the increasing adoption of high-tech machinery and equipment, while the software segment is the fastest growing as growing adoption of AI, and data analytics in farm management creates software demand for crop health monitoring.

-

By Application, the crop harvesting segment dominated the market with approximately 62% share in 2025 as staple crops are among the widely cultivated globally, driving the demand for precision harvesting for improved efficiency and reduced losses, while the horticulture segment is the fastest growing.

By Product, combine harvesters dominate, harvesting robots grow fastest

Combine harvesters retained the dominant product position with approximately 58% of the precision harvesting market in 2025. Their commercial primacy reflects the extraordinary commercial scale of global grain production whose wheat, rice, corn, soybean, and barley harvesting creates the largest aggregate precision harvesting equipment procurement category. The precision technology integration within modern combine harvesters creates premium procurement above conventional mechanical alternatives whose performance data justifies the investment for large commercial farming operations.

Harvesting robots are the fastest-growing product. The cost of manual fruit and berry picking in California, Spain, Australia, and New Zealand whose seasonal labor availability is declining creates robotic picking ROI whose payback period is compressing with each generation of improved picking speed and fruit damage rate. Companies including Agrobot for strawberry harvesting, Harvest CROO Robotics for berry picking, and Dogtooth Technologies for soft fruit demonstrate the commercial progression from prototype to deployment-ready robotic harvesting systems whose adoption creates new market volume.

By Offering, hardware dominates, software grows fastest

Hardware retained the dominant offering position with approximately 65% of the precision harvesting market in 2025. Hardware's commercial primacy reflects the foundational capital procurement that precision harvesting programme establishment requires. Each combine harvester, forage harvester, or robotic picking system represents a capital investment whose magnitude substantially exceeds the annual software and service procurement it generates over its operational life.

Software is the fastest-growing offering because data-driven farm management's commercial value is progressively creating structured procurement for analytical platforms whose yield mapping, field variability analysis, harvest schedule optimizations, and predictive maintenance capability improve operational and financial outcomes that equipment-only precision harvesting cannot achieve. Farm management software whose integration with John Deere Operations Center, AGCO's Fuse Technologies, and CNH's AFS Connect creates cloud-connected harvest data ecosystem whose analytical value sustains subscription procurement that compounds with connected equipment installation growth.

By Application, crop harvesting dominates, horticulture grows fastest

Crop harvesting retained the dominant application position with approximately 62% of the precision harvesting market in 2025. Each major grain-producing country's harvest season creates defined combine harvester and forage harvester procurement whose commercial scale sustains the crop harvesting application's dominant position independent of the faster growth rates visible in smaller application categories.

Horticulture is the fastest-growing application because the economic pressure of labor shortage creates the strongest per-hectare precision harvesting investment motivation. Each hectare of strawberry, grape, or tomato production whose manual picking labor cost represents 50-70% of total production cost creates robotic picking adoption motivation. The horticulture sector's progressive robotic picking adoption creates new commercial market development that was not commercially accessible before robotic picking technology's performance maturation.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Precision Harvesting Market Insights

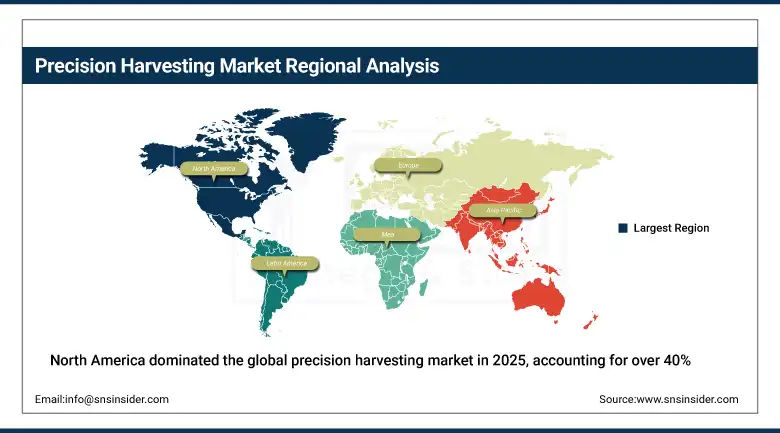

North America dominated the global precision harvesting market in 2025, accounting for over 40% of global revenues. The United States accounts for approximately 87.4% of North American revenues through John Deere's domestic market leadership, AGCO's Challenger and Gleaner combine brands, and CNH Industrial's Case IH harvesting equipment whose combined portfolio defines the commercial North American precision harvesting standard. The Corn Belt's extraordinary grain production scale creates the world's largest single regional combine harvester fleet whose annual replacement and upgrade cycle creates consistent precision technology procurement.

Canada contributes approximately 12.6% of North American revenues through its prairie grain production sector's combine harvester fleet, the canola crop's precision harvesting requirement, and the government's agricultural technology adoption programme whose subsidy creates structured precision harvesting investment.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Precision Harvesting Market Insights

Europe is a technically sophisticated precision harvesting market where CLAAS's German leadership, CNH Industrial's European operations, and the EU's Common Agricultural Policy's precision farming support create structured institutional procurement. Germany accounts for approximately 22.3% of European revenues through CLAAS's domestic manufacturing and market presence, the advanced German agricultural sector's technology adoption, and the precision harvesting equipment export manufacturing whose domestic market serves as the development and launch platform.

France, the United Kingdom, and Ukraine are significant secondary markets whose grain production creates consistent combine harvester procurement. The EU's Farm to Fork Strategy's precision agriculture support and member state subsidy programmes create above-average precision technology adoption motivation that sustains European market growth above the global average.

Asia Pacific Precision Harvesting Market Insights

Asia Pacific is the fastest-growing regional precision harvesting market, driven by China's extraordinary rice and wheat production whose mechanization investment is creating above-average combine harvester and precision technology adoption, India's government subsidy programmes for agricultural mechanization, Japan's advanced agricultural robotics development, and Southeast Asia's growing commercial agriculture sector. China accounts for approximately 44.8% of Asia Pacific revenues through its massive grain production machinery fleet, government Made in China 2025 agricultural technology investment, and the domestic precision harvesting equipment manufacturer development.

India represents the most commercially dynamic emerging market within Asia Pacific where the government's Sub-Mission on Agricultural Mechanization whose equipment subsidy programme creates structured precision harvesting procurement across smallholder farming cooperatives whose aggregate equipment demand creates commercial scale that international equipment suppliers are progressively addressing through locally adapted lower-cost precision harvesting solutions.

MEA & Latin America Precision Harvesting Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through its commercial agricultural investment, Vision 2030's food security programme creating precision farming adoption, and the wheat and date palm production sectors’ harvesting mechanization. Brazil leads Latin American revenues at approximately 44.2% through its extraordinary soybean and sugarcane production whose commercial farming scale creates significant precision harvesting equipment procurement. AGCO, CNH Industrial, and John Deere's Brazilian operations serve the domestic market whose large-scale agricultural operations create world-class precision harvesting demand that sustains significant regional commercial scale.

Argentina's large-scale grain production and Chile's fruit export sector create significant secondary Latin American markets whose precision harvesting investment reflects both the large-scale grain crop's combine harvester requirement and the labor shortage-driven robotic picking opportunity in export fruit production.

Market Dynamics

Growth Drivers: Agricultural labor shortages driving automation and global food demand requiring yield optimizations

Agricultural labor shortages are the most commercially compelling near-term growth driver. The structural decline of agricultural workforce availability across developed markets, reflecting ageing rural populations, urban migration, and immigration policy constraints on seasonal worker availability, creates economic urgency for mechanical and robotic harvesting adoption whose commercial motivation exceeds the gradual efficiency improvement case that characterizes normal technology adoption. Each harvest season whose labor shortage creates crop loss or delayed harvesting whose quality impact reduces farm income creates quantifiable motivation for precision harvesting investment that sustains procurement through commodity price cycle variation.

Global food demand's progressive increase toward feeding 10 billion people by 2050 creates the most structurally certain long-term precision harvesting growth driver. Each percentage point increase in food production efficiency that precision harvesting's reduced crop loss, optimized harvest timing, and reduced post-harvest waste creates generates economic value whose aggregate across global agricultural production sustains government subsidy and farmer investment in precision harvesting technology. The FAO's estimate that 30% of global food production is lost between farm and fork creates the performance improvement opportunity whose commercial capture through precision harvesting sustains innovation investment.

Restraints: High capital cost limiting adoption among smallholder farmers and connectivity limitations in rural agricultural areas

Precision harvesting equipment's high capital cost creates adoption barriers for smallholder and medium-scale farming operations whose agricultural income cannot justify the capital investment in premium precision harvesting systems whose ROI is most visible at large commercial farming scales. Each smallholder farms whose hectarage creates insufficient operational scale for precision harvesting ROI creates a market segment whose adoption requires either equipment sharing cooperatives, custom hiring services, or government subsidy programmes to create commercial accessibility.

Connectivity limitations in remote agricultural areas create precision harvesting software and telematics adoption barriers. Each precision harvesting system whose performance depends on cloud connectivity for yield mapping data upload, remote diagnostics, and software updates creates operational gaps in areas where network coverage is absent whose practical impact limits precision technology adoption in large portions of global agricultural production geography.

Opportunities: Harvesting robot commercial scale-up and emerging market government subsidy programmes

Harvesting robot commercial scale-up represents the most commercially transformative near-term opportunity whose successful realization would create a new premium market category whose annual procurement value compounds with horticulture sector labor shortage urgency. Each new robotic harvesting system that achieves commercial picking speed and fruit damage rate comparable to manual picking creates adoption justification whose economic case in labor-shortage markets requires only competitive capital cost to sustain volume deployment. The USD 1 billion investment committed by global agricultural robotics companies in 2024 demonstrates commercial conviction in the harvesting robot market's near-term realization.

Emerging market government subsidy programmes in India, Southeast Asia, and Africa represent the most commercially significant demand creation mechanism for precision harvesting technology adoption beyond the established North American and European large commercial farming markets. Each subsidy programme that reduces capital cost barriers for smallholder cooperative equipment procurement creates new market volume whose aggregate across developing country agricultural sectors creates commercial scale that sustains international equipment manufacturer market development investment.

Recent Developments:

-

2026: CNH Industrial improved Raven precision harvesting solutions using AI-driven guidance, retrofit kits, and real-time machine performance analytics optimization system upgrade.

-

2025: John Deere announced two new forage harvesting products on 5 June 2025 featuring up to 1,020PS horsepower and HarvestMotion Plus technology that automatically adjusts feed roll speed for consistent crop throughput, developed based on direct customer feedback for improved forage quality and fuel savings.

-

2025: AGCO enhanced Fendt IDEAL combine automation with variable rate harvesting, grain loss reduction, and smart field optimization capabilities integration platform.

Precision Harvesting Market Key Players

-

Deere & Company (John Deere)

-

AGCO Corporation

-

CLAAS KGaA mbH

-

CNH Industrial N.V. (Case IH & New Holland)

-

KUBOTA Corporation

-

Trimble Inc.

-

Topcon Corporation

-

Yanmar Co., Ltd.

-

Hexagon Agriculture division

-

TeeJet Technologies

-

Kinze Manufacturing Inc.

-

Ag Leader Technology

-

FarmWise Labs Inc.

-

Clearpath Robotics Inc.

-

Sentera Inc.

-

Farmers Edge Inc.

-

DICKEY-john Corporation

-

Taranis Visual Inc.

-

Harvest CROO Robotics

-

Agrobot S.L.

Precision Harvesting Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 20.77 Billion |

| Market Size by 2035 | USD 40.19 Billion |

| CAGR | CAGR of 6.84% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Combine Harvesters, Harvesting Robots, Self-Propelled Forage Harvesters) • By Offering (Hardware, Software, Services) • By Application (Crop Harvesting, Greenhouse, Horticulture, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Deere & Company (John Deere), AGCO Corporation, CLAAS KGaA mbH, CNH Industrial N.V. (Case IH & New Holland), KUBOTA Corporation, Trimble Inc., Topcon Corporation, Yanmar Co., Ltd., Hexagon Agriculture division, TeeJet Technologies, Kinze Manufacturing Inc., Ag Leader Technology, FarmWise Labs Inc., Clearpath Robotics Inc., Sentera Inc., Farmers Edge Inc., DICKEY-john Corporation, Taranis Visual Inc., Harvest CROO Robotics, Agrobot S.L. |

Frequently Asked Questions

The Precision Harvesting Market is expected to grow at a CAGR of 6.84% from 2026 to 2035.

The Precision Harvesting Market was valued at USD 20.77 Billion in 2025.

Rising global food demand requiring yield optimization through precision harvesting efficiency improvement, and agricultural labor shortages.

Combine Harvesters dominated the Precision Harvesting Market.

North America dominated the Precision Harvesting Market with over 40% of global revenues in 2025.

Get in Touch